If you’re putting your home on the market, you may be wondering how to style it. Home staging is a popular house-selling strategy that presents your home in its best light.

Staging a house is meant to show off your home’s features, create a move-in-ready look and help potential buyers see themselves living in the space. From tidying up your space to redecorating, home staging can give your home a clean and inviting ambiance that welcomes buyers — and may even entice them to pay more.

When preparing a home for sale, many sellers hire professional home stagers to create a warm, inviting place that buyers will want to call home. But, there are many changes you can make on your own.

Declutter Your Space

Declutter, declutter, declutter. Staged homes shouldn’t have piles of paper on the countertops. Take a moment to reassess your space and ask yourself, “Do I need this?” Determine which books, loose mail and magazines can be stored elsewhere to create a more spacious look.

Getting rid of clutter shows that your home is organized. Potential buyers may also infer that you take good care of your home and that it’s well-maintained.

Focus on a Neutral Color Palette

Home stagers always prefer neutral palettes to make a room look balanced and timeless. Colors such as beige, white or light gray are good choices. Then, add aesthetically pleasing decor, such as a black or green pillow for the couch. Try to create a fun look that’s not too matchy-matchy.

Find Long-Term Storage for Everything on the Counters

In the bathroom, find a long-term storage solution for items like cotton swabs and hair brushes so they’re not littering countertops. Add mirrors to walls to increase light in a small or dark bathroom. Even consider a new set of white, solid brown or light gray towels to give your bathroom a clean, seamless look.

Clear off your kitchen countertops by storing away small appliances, kitchen tools and knick-knacks. You want to accentuate the positives — cabinets for storage and plenty of countertop space for food prep. What can you keep on the table? A bowl of fresh fruit, like lemons or oranges, to add a pop of color and style.

Professionally Organize Your Closet

Show off your generous closet space by making each one neat and tidy. Remove everything from your closets and sort it into piles: keep, donate, sell and recycle.

If there are items you’d like to keep that you’re not currently using, store them away until you’re ready to move. You want potential homebuyers to see uncluttered closets with plenty of space. A bonus? Paring down your belongings means you’ll have less to pack.

Make Your Bedrooms Feel Hotel-Like and Inviting

Stick with one neutral color in the bedroom, perhaps all white, gray or beige, for example. To make your room hotel-like, tuck your comforter into the end of your mattress. Place two pillows on the bed, then add another three to five on top for a luxurious feel. For an attractive touch above the headboard, hang either one large piece of artwork or a set of three smaller ones.

Look to Odd Numbers

Group items in odd numbers, such as three or five. This classic design rule helps create visual interest and calming, naturally appealing displays. It’s a trick that makes a room look more luxurious versus symmetrical. On the dresser or bedside table, arrange a small vase of flowers with two books.

Use Glass for Small Dining Spaces

Make a tiny dining room’s layout appear larger with a glass-topped table. The more solid the furniture, the smaller a place looks.

Add a rug to “anchor” the room, even if you have an open-plan house. But keep in mind the room’s scale — in grander rooms, go big, and in smaller spaces, use a more petite rug that fits under the table. Place a generously sized centerpiece to draw the eye upward toward the room’s ceiling light.

Take Window Treatments to the Ceiling

To create height (even in small rooms), take window treatments as high to the ceiling as possible. Window treatments make the room look taller. And there’s no need to splurge on fancy panels; drapes are one way to use fun patterns in an otherwise neutral room.

Hang a Mirror in the Entryway

At the entryway, set up a sofa table or console with a lamp and accessories in sets of three. Above the console, hang a mirror or a larger piece of artwork to create a welcoming feel whether you’re coming or going.

Don’t Forget About the Curb Appeal

Curb appeal is all about making that beautiful first impression. Fortunately, it doesn’t take much to make a big impact. Fresh paint, a new mailbox, a healthy manicured lawn, a clean walkway and flower-filled containers are easy ways to improve your home’s exterior appearance. You may also want to consider investing in outdoor lighting to enhance both safety and aesthetic appeal and, potentially, even your appraisal.

Remove Bulky Furniture

When staging a home for sale, put oversized furniture in storage. Furniture that is too large for a space can make a room feel cramped. Rent or purchase some inexpensive pieces better scaled to the room to make the area appear more airy and comfortable.

Depersonalize Your Home

Your home may be filled with years of special memories, but you’ll want to remove personal photos, collectibles and keepsakes when selling. The goal is to eliminate distractions and help prospective buyers envision themselves living in the space. You want them to concentrate on your home’s unique features, not your personal memories.

Have a Pleasant Scent in the Home for Tours

A gentle, refreshing scent creates a cozy feel and can trigger pleasant emotions. When it’s time to show your home, think about spraying a dash of essential oils throughout your rooms or using a diffuser.

You’ll also want to make sure to remove any bad smells. Open the windows to let fresh air in and thoroughly clean your carpets, sinks, trash cans, bathrooms and pet areas.

With this advice, your home’s spacious, balanced and livable look will be ready to list and show off to potential buyers.

And if you’re selling your home and purchasing a new one, let Pennymac guide you in the mortgage loan process. Get a custom instant rate quote from Pennymac today.

Inside: Are you looking for a way to help your kids learn about money? If so, Cash App for kids is the ideal answer. This guide will teach you how to manage money simply by using apps.

Ever wondered why it’s crucial for your kids and teens to have a cashless payment option?

In this digital age, teaching money management skills early to our younger generation is vital.

Having features likeCash App for kids is a great way to introduce them to responsible spending. Not only does it provide a secure method for purchases without the need for carrying physical money, but it also serves as an excellent tool for setting spending limits and tracking budgeting habits.

Plus, it’s a win-win for parents and teens as you can visually monitor transactions while they enjoy a sense of financial independence.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What is Cash App?

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

It offers a range of services including a free custom Visa debit card and the option to receive paychecks up to two days earlier.

Additionally, with the Cash App, users can instantly buy and sell stocks commission-free and even trade in bitcoin.

Can a child have Cash App?

Yes, a child can have a Cash App account if they are 13 years old or older. However, it requires parental approval.

Remember, this gives your child the opportunity to learn money management, but it also comes with the responsibility of overseeing their spending.

Why would kids need Cash App?

Well, we are moving to a cashless world. There are thousands of stores and restaurants that only offer cash. We learned this when our son went to an MLB baseball game with his middle school. No cash. Only debit or credit cards were accepted as well as Visa gift cards.

So, we needed to give our kids an introduction to modern, simple, and secure ways of money management.

Cash App might be the perfect solution. Another great option is Greenlight for kids.

Cash App – Do More with Your Money

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

What are the benefits of using Cash App for kids?

Education: Cash App can be an effective way to teach your children about responsible money handling and the dynamics of a digital economy.

Control: You have the flexibility to set spending limits and disable certain features, ensuring responsible use of the application.

Security: Cash App’s encrypted connection adds an extra layer of security, keeping your kid’s transactions and personal data secure.

Emergencies and convenience: It’s an incredibly handy tool for sending cash to your kid during emergencies. No need to rush, just a tap on your phone, and you can send money.

What cash apps can 13 year olds use?

In today’s cashless society, it’s more important than ever for kids to learn how to manage money digitally.

Below are some alternatives to Cash App that serve well for 13-year-olds:

Description:

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track your child’s spending and saving habits.

Learn to earn, save, and invest together. The banking and investing app for kids and teens.

Comes with a debit card

Allows kids to make savings goals.

Limited deposit methods

Monthly fee

Starts at $4.99/month

Description:

Prepaid cards and a family finance app for kids, teens, and parents.

More than money.

A financial education.

If you want your child to learn money habits that match your values, you’re in the right place.

Description:

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

Description:

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track your child’s spending and saving habits.

Learn to earn, save, and invest together. The banking and investing app for kids and teens.

Comes with a debit card

Allows kids to make savings goals.

Limited deposit methods

Monthly fee

Starts at $4.99/month

Description:

Prepaid cards and a family finance app for kids, teens, and parents.

More than money.

A financial education.

If you want your child to learn money habits that match your values, you’re in the right place.

No bank account needed.

No fancy phone needed.

Affordable for all! Plus free trial!

Mobile setup is not user friendly.

No investing option.

$5.99 month or $3.33/month for 12 months

Description:

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

Only able to spend what is loaded on Card.

Free CashApp debit card.

No maintenance or annual fees.

Not FDIC insured.

No parental controls.

Remember, each app has its own unique strengths and weaknesses. Do some research and try out a few to see which one best suits your teen’s financial needs.

How do I create a Cash App account for my child?

Teaching kids about money management is vital for their financial future.

One excellent way to do this effectively is by setting up a Cash App account for children, giving them practical experience in handling finances while under a parent’s supervision. Also, known as a sponsored account.

This guide will walk you through the process of creating a Cash App account for your child and highlight the numerous benefits it offers.

Step 1: Download Cash App

To download Cash App, click this Cash App link to make sure you are in the right spot. Both you and your teen will need to do this step.

It’s easily recognizable – look for the white dollar sign on a green background. Once you’ve found it, simply hit ‘Install’ and sit back while your phone does the work.

Remember, this green goodness is only accessible to users in the United States.

When learning which payment type is best when trying to stick to a budget, you will be pleasantly surprised at how well Cash App works.

Step 2: Create an Account

This is a simple process. Both the teen and the adult will need to do this step separately. If as the parent you don’t have a Cash App account, then you will need to do this step.

To create a Cash App account, follow these steps:

Once installed, open the application and follow the on-screen instructions to set up your account.

You will have to enter your phone number or email address.

For security certification, the Cash App will send you a secret code to verify you. Enter it.

Select a $cashtag, which is a unique username to send and receive money (similar to Venmo)

Step 3: Connect a Bank Account

For the parent account, you need to complete this step and the teen will need to wait.

Remember, in “My Cash” you’ll spot the “Add Money” option for funding.

Open Cash App; it’s the icon with a white dollar sign on a green background.

Tap the top-right profile icon.

Navigate to “My Cash” – it’s a tab on the home screen.

Click “Link a Bank,” nestled within the options.

Follow the prompts to add your bank account or debit card info.

Once your card is linked, you’re all set.

Learn where can I load my Cash App card.

Step 4: Authorization Request of a Family or Sponsor Account

Now, you must link the two accounts together. Cash App calls this a sponsored account. There are one of two ways to accomplish this.

Option #1 – Parents Initiate the Request

To invite someone 13-17, then open the app:

Tap the Profile Icon on your Cash App home screen

Select Family

Tap Invite a teen

Follow prompts to share links using text or email

Option #2 – By the Teen

On the Home Screen, tap the Cash App profile icon.

Proceed to Family Accounts and choose the option “I’m a Teen”.

Complete the Cash App for Kids application form with your details including your name and birthday.

Hit the Request Approval button.

Enter the name, email, phone number, or $CashTag of your parent/guardian.

Lastly, tap Send. This will send an authorization request to your parent or guardian’s Cash App account. They need to approve this request before you can start using the app.

Note: You can’t add funds, send payment, or request a Cash Card until this authorization is approved.

Step 5: Have Your Child Design and Order a Free Cash Card

Now, the fun part! Ordering your own Cash App Card.

Designing and ordering your Cash Card is packed with creativity and ease.

Customize your card to represent your unique personality, with choices ranging from the material, font size, and base design, to text lines.

You can seek inspiration from an array of cool Cash App Card design ideas. Notably, the glow-in-the-dark cards are quite popular among minors.

The whole process is about making your debit card unmistakably yours.

Step 6: Limitations on Certain Features

Certain financial apps cater to teens by setting limits on transactions.

For example, a teen on Cash App can send and receive up to $1,000 every 30 days. This safeguard is designed to prevent overspending and encourage smart budgeting practices.

Furthermore, parents and guardians have the option to impose their own customized spending limits through the app according to their teen’s financial maturity. However, it’s essential to keep in mind, that these apps are not recommended to be used by teens just like regular accounts due to the risks of misspending and overspending.

Be aware that certain transactions are blocked, including bars, dating services, and rental car services

Encourage your kids to use robust, unique passwords and activate features like PIN lock and facial ID to enhance security.

You can ensure safety by setting a PIN, turning on notifications, and limiting money requests to ‘contacts only’.

This is similar to understanding the advantages of mobile phones for kids.

Step 7: Pick a unique $Cashtag

Tell your child to select a unique and fun $Cashtag for their Cash App account. It’s like a username and can be used in transactions.

Emphasize the originality of the $Cashtag as it needs to be unique.

Expert Tip: To secure their $Cashtag, avoid using personal information like birthdate or social security number. Instead, opt for quirky, fun, and uncommon word combinations.

Step 8: Send & receive money

Cash App provides an easy-to-use platform for instantly transferring money between friends and family at no cost.

A few quick taps allow users to request, receive, or send money, presenting a convenient method for paying a dinner, settling rent with roommates, or any other financial interactions.

In addition, users get a free custom Visa debit card, which they can order directly from the Cash App for both virtual and physical use. The card enables users to make purchases from any merchant accepting Visa cards.

Plus, with the Cash Boost feature, users gain from immediate discounts at select restaurants, stores, applications, and websites when they use their Cash App card.

An Alternative – Use Greenlight Debit Card for Kids

Looking for an all-in-one alternative to the Cash App for your kids?

Explore the Greenlight Debit Card for kids – a superb choice for money management and financial education.

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track their child’s spending and saving habits.

Plus it offers 1% cash back on all purchases and up to 2% interest on savings, this card is accepted anywhere MasterCard is used and comes with built-in features that include educational programming and real-time notifications for every transaction.

Greenlight

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track your child’s spending and saving habits.

Pros:

Offers a comprehensive financial education pathway

Broad acceptance due to affiliation with Mastercard

Parents retain control over spending limits

Real-time notifications improve security

Cashback rewards are an added bonus

Cons:

Greenlight charges a monthly fee starting from $4.99

Limitations on direct deposits

No possibility for payments from Paypal, Venmo or Apple Cash

Kids under 13 require parental access

Some transaction types are blocked

It’s an innovative and secure financial platform for kids, with plans starting at $4.99 a month.

Safety Measures for Using Cash App for Kids

Educating children about safety measures while using cash apps and debit cards is crucial in today’s digital age.

With increased online scams, it’s important that kids understand the equivalence of digital cash to real money and how to protect their accounts.

This brief overview will highlight key practices to ensure your child’s safety when handling digital transactions.

1. Know the App’s Safety Features

Knowing the app’s safety features is crucial for maintaining security while using cash apps.

These features can include password protection, two-step verification, and biometric scans such as fingerprint or facial ID. Many apps also offer robust encryption to secure data and transactions.

Keeping abreast of the app’s safety protocols not only helps safeguard against potential scams but also instills a better understanding of digital literacy. Understanding these safety measures and functionalities can greatly lessen the likelihood of falling victim to fraudulent activities.

Make sure they don’t learn how to unlock borrow on CashApp!

2. Talk to Your Kids About Money

It is essential to talk to your children about financial literacy from an early age especially if your parents never spoke about money.

Start by making them aware of the concept of saving by using tools like a piggy bank and elucidate the value of delayed gratification.

As they mature, introduce them to the functionalities of debit cards and apps like Cash App that provide hands-on experience in managing finances. Teach them about budgeting, saving, and investing in an age-appropriate manner.

Above all, impart the message that money doesn’t just grow on trees and that every purchase needs to be evaluated against future needs and plans.

3. Use Account Alerts to Stay Up to Date

Account alerts on Cash App are not only handy but critical to your kid’s financial safety. Setting them up is a breeze.

Firstly, head to the “Notification” tab in your app settings.

Thereafter, opt for “Account alerts” and switch it on. This will ensure you’re notified of all transactions.

For an added layer of security, enable “Suspicious activity” alerts; this helps to flag any odd movements swiftly.

4. Set Up a Strong Account Passwords

It is crucial to ensure that your online accounts are secured with robust and unique passwords.

Complex passwords that incorporate a mix of uppercase and lowercase letters, numbers, and special characters can provide a strong line of defense against unauthorized access. Also, you should look at changing these passwords regularly, which further enhances security.

Using a password manager, either online or paper-based, can assist in maintaining and keeping track of different account credentials, maximizing security while minimizing the risk of forgetting passwords.

However, if opting for a paper-based version, it is crucial to store it in a secure and confidential location to prevent unauthorized access.

5. Have a Conversation About Scams and Fraud

The proliferation of digital transactions and cash transfer apps has given rise to numerous scams, making it critical for users to look out for fraud.

Online scams can result in financial loss, with cash apps often not assisting in the recovery of misdirected funds due to errors or fraudulent activities.

Additionally, cybercriminals use these scams to steal personal data, leading to issues like identity theft and fraudulent transactions. Furthermore, the anonymity of digital platforms enables scammers to disappear without a trace after executing a scam, sometimes befriending and exploiting minors.

Therefore, everyone must stay vigilant about potential scams to protect their money, personal information, and overall digital safety.

Key Tips to Watch for:

Discuss current scams happening. Use reliable resources to educate them about how fraud works and precautions to take.

Teach them to *slow down* during transactions to avoid sending money to the wrong contacts.

Advise against sending money to strangers to avoid being scammed.

6. Check Bank Accounts for Any Unauthorized Payments

As a parent, it is essential to regularly check your teen’s checking accounts linked to their mobile wallet for unauthorized payments.

By staying vigilant, you can detect suspicious activity early and prevent possible instances of fraud.

Tracking their spending patterns also helps you understand if they are managing their digital money wisely or if there are sudden changes in their spending habits.

Remember, it is better to be proactive in monitoring these accounts, as most money transfer app funds are not FDIC insured, making the recovery of accidental transfers or payments a challenging task.

7. Ability to Give Your Kids an Allowance

If you choose to do so, giving your kids an allowance on Cash App is a safe and effective way to teach them about responsible money management. It provides hands-on experience while putting the power of monitoring in your hands.

To set this up, simply create an account for your minor and periodically send money to it as an allowance. They can spend or save it, while you observe their spending habits.

This is a simple way for kids and teens to start managing a small amount of money.

Cash App – Do More with Your Money

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

Which cash app will you choose for your kids

To sum it up, equipping your kids with financial responsibility via Cash App or Greenlight is an intelligent move.

These apps provide a platform for learning about savings, investments, and the value of money.

Although risk exists its potential scams, with proper guidance, your teen can safely navigate this. The added perks of trading, direct cash exchanges, and options like BusyKid and Bankaroo can further enrich their financial literacy journey.

So, which digital wallet will you pick for your kid’s first leap into financial independence?

Know someone else that needs this, too? Then, please share!!

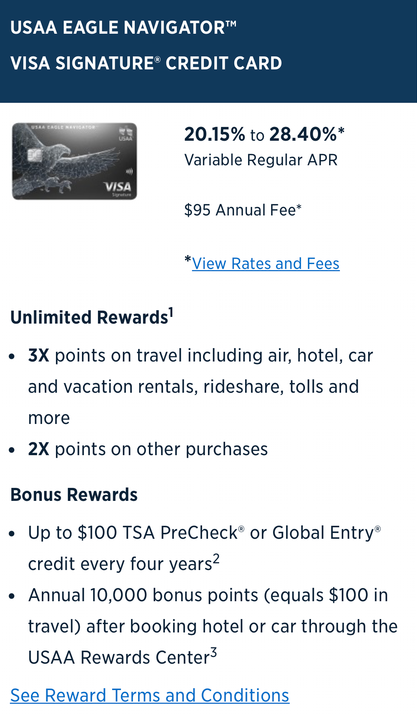

USAA has launched a new credit card called ‘Eagle Navigator’, card isn’t listed on the credit card page but is being offered to existing users. Card basics are as follows:

$95 annual fee

Card earns at the following rates:

3x points on travel

2x points on all other purchases

10,000 annual bonus points after booking hotel or car travel through the USAA booking portal

$100 TSA PreCheck/ Global Entry Credit

Given that a lot of cards earn at 2%+ and don’t have an annual fee I don’t really see this card of being any use. Dead on arrival unless they add more benefits/more lucrative earning categories or a large sign up bonus.

The city is a major banking center and home to the Levine Museum of the New South. You can see Broadway productions, listen to the symphony, visit the NASCAR Hall of Fame and escape to the countryside, all in one weekend.

Like most cities, Charlotte has many different neighborhoods to choose from when you’re deciding where to live. Whether you prefer to live in the hippest neighborhoods with the best nightlife and newest restaurants or a quiet neighborhood with parks and sidewalks or something in between, you’re sure to find it Charlotte.

Here are the 15 best neighborhoods in Charlotte for renters to live in 2022.

Median 1-BR rent: $1,622

Median 2-BR rent: $2,049

Walk Score: 50/100

Uptown is the hub of the action in Charlotte. It’s where the majority of the major companies are and subsequently, where most people work. If you like restaurants, pubs and nightclubs, this is where you’ll find an endless variety of all of them. Uptown is also home to most of the city’s major sporting events.

This neighborhood has four wards. Second and Fourth Ward are mainly residential, but are walkable to the First and Third Ward, which are the commercial districts. Frazier Dog Park on the edge of the neighborhood is great for your four-legged friends, while sports fans will have plenty to do watching the Carolina Panthers play at Bank of America stadium.

Median 1-BR rent: $1,687

Median 2-BR rent: $2,357

Walk Score: 71/100

This is Charlotte’s historic showpiece. Dilworth features many renovated Victorian houses and is a registered historic district. The neighborhood is walkable and is also connected to Downtown by a streetcar line. Most of the residents are professionals and families with young children. There’s a splash pad for kids at Latta Park.

You can find plenty of cafés and shops, as well as houses here, and the Carolinas Medical Center is nearby. It’s a short commute to Uptown and Downtown, which is why this neighborhood was Charlotte’s first suburb.

Median 1-BR rent: $1,225

Median 2-BR rent: $1,350

Walk Score: 60/100

Elizabeth was Charlotte’s second streetcar suburb, and it still boasts a streetcar connection to Downtown. Many of the neighborhood’s historic homes are now popular restaurants. But don’t worry, the neighborhood still has plenty of residential housing left and it’s highly walkable, making it one of the best neighborhoods in Charlotte.

One of Charlotte’s oldest theaters, the Visulite Theater, is found in Elizabeth. Another unique feature of this neighborhood is that it borders the Little Sugar Creek Greenway, putting outdoor activities within easy reach.

Median 1-BR rent: $930

Median 2-BR rent: $1,165

Walk Score: 39/100

Located on the south side of the city just outside the city center, East Forest is a quiet, solidly middle-class neighborhood that’s mostly inhabited by young professionals and families. It ranks No. 20 on the list of the most diverse neighborhoods in Charlotte and has a very urban feel.

Though mostly residential, this neighborhood does have a good selection of restaurants and a few choices for nightlife. There are many parks and good schools. One of the biggest draws of this neighborhood is its convenience — it’s just a short drive to anywhere in the city.

Median 1-BR rent: $1,795

Median 2-BR rent: $2,108

Walk Score: 69/100

Charlotte residents call this neighborhood “NoDa.” It’s second only to South End as a draw for young and hip Charlotteans. It’s also second in the number of craft breweries and live music shows you’ll find. There’s a diverse range of restaurants, too, many of which are locally owned.

NoDa is famous as the home of the Neighborhood Theatre, which hosts acts big and small. Art galleries, small artisan shops and tattoo parlors dot the entire neighborhood. Bonus: this historic neighborhood is on the National Register of Historic Places.

Median 1-BR rent: $1,119

Median 2-BR rent: $1,264

Walk Score: 25/100

Hickory Ridge is a newer suburb on the eastern side of the city. While still within the city limits and part of Charlotte, it has a suburban feel that attracts many who want to be close to city amenities while being in a quiet part of town. Many families find this neighborhood attractive because of the good schools and the number of parks.

There aren’t many options for arts and entertainment in this area. Disco Rodeo is the only nightclub within the neighborhood. One unique feature is the presence of the Charlotte Murder Mystery Company, a performing arts venue. If quiet is what you’re looking for, this is the neighborhood for you.

Median 1-BR rent: $1,012

Median 2-BR rent: $1,162

Walk Score: 33/100

This neighborhood is on the southwestern side of the city not too far from Downtown. It has a suburban look and feel despite its proximity to the city center. The biggest attraction of this neighborhood is its convenient location and its affordability, which is why it’s one of the best neighborhoods in Charlotte.

Montclaire South does have a couple of parks and nightclubs. It’s home to one of Charlotte’s many community colleges and the local Costco.

Source: Rent./Camden Ballantyne

Median 1-BR rent: $1,349

Median 2-BR rent: $1,819

Walk Score: 46/100

Ballantyne East is on the far southern end of the city. It’s a mostly residential neighborhood that’s distinctly suburban. There are some restaurants but there are few other commercial shops in the area. This neighborhood is No. 3 on the list of best places to live in all of North Carolina.

A unique feature of Ballantyne East is the presence of the Big Rock Nature Preserve, a popular local attraction. The neighborhood is also home to a public golf course and pro shop.

Median 1-BR rent: $1,059

Median 2-BR rent: $1,316

Walk Score: 27/100

This is a large neighborhood on the east side of Charlotte within easy reach of the hippest areas, such as Plaza Midwood and NoDa. It’s also not too far from the University District and Downtown. Many locals live here and commute to their jobs in other districts.

Eastside is a diverse neighborhood. It starts off with an urban feel but becomes more suburban as you move further east from the center of the city. It’s home to the Hindu Center of Charlotte and numerous parks, including Sherman Branch Mountain Biking Park.

Median 1-BR rent: $2,042

Median 2-BR rent: $2,415

Walk Score: 66/100

Myers Park is an elite, formal neighborhood by design. One of the best neighborhoods in Charlotte, it’s highly sought after by both new residents and old Charlotteans alike. Here you’ll find large Tudor and Colonial-style houses with elegant gardens and tree-lined drives.

The Mint Museum Randolph features modern and contemporary art. There are several chic cafés and boutiques within walking distance. Myers Park is also home to the Wing Haven Gardens and the Discovery Nature Place Museum. The Booty Loop bike trail runs through Myers Park, too.

Median 1-BR rent: $2,801

Median 2-BR rent: $4,031

Walk Score: 71/100

Plaza Midwood was one of Charlotte’s first suburbs, back in the days when commuting meant riding a streetcar from Downtown or the banking district. Today, it combines old with new, trendy with historic and is one of the up-and-coming neighborhoods on the east side of the city.

A vibrant restaurant scene includes everything from barbecue to gastropubs. This is one of the best neighborhoods in the city if you want a range of dining options. Trendy boutiques and consignment shops are offset by dive bars and tattoo shops. Parts of the neighborhood are historic districts, while others were redeveloped. In short, it’s one of the most diverse areas of the city.

Median 1-BR rent: $1,379

Median 2-BR rent: $1,825

Walk Score: 21/100

The University of North Carolina at Charlotte occupies the heart of University City and gives it its name. This is a classic university neighborhood, with plenty of cheap restaurants and pubs. It gets loud and crowded sometimes, particularly on game days.

There’s more to this neighborhood than the school, however. Duke Energy and TIAA-CREF both have their national headquarters here. Charlotte’s light rail system terminates at the local station, making commuting to other sections of the city a breeze.

Median 1-BR rent: $1,634

Median 2-BR rent: $2,050

Walk Score: 50/100

This inner ring suburb was established right after the Second World War and consists mainly of residential housing but is within walking distance of both the SouthPark Mall and the Park Road Shopping Center.

Charlotte’s light rail line runs right to Madison Park and a bike path runs through it, making your commute to work easy. Both the Little Hope Creek and Little Sugar Creek Greenways run through and are adjacent to the neighborhood. Charlotte’s senior center is in Marion Diel Park.

Median 1-BR rent: $1,709

Median 2-BR rent: $2,489

Walk Score: 74/100

South End is a quick train ride away from Uptown, which means it’s a favorite among the professionals who work in the latter and one of the best neighborhoods in Charlotte. This is currently the “hippest” area in Charlotte. Here’s where you’ll find music festivals, art shows and antique stores galore.

This neighborhood is also home to farmer’s markets, dozens of restaurants and most of the city’s craft breweries. The Atherton Mill and Market is becoming famous across the state. That not your style? You also won’t find better nightlife anywhere in Charlotte, even in Uptown.

Median 1-BR rent: $2,035

Median 2-BR rent: $2,467

Walk Score: 63/100

Located on the south end of Charlotte, Southpark is a mini version of Uptown, complete with its own array of financial firms and upscale shopping centers. It’s preferred by many young professionals, who love both the proximity to work and the wide array of shopping and dining options.

SouthPark is both popular and trendy, while still being more three-piece suit than hip. Symphony Park has an outdoor amphitheater featuring live music and entertainment. Upscale nightclubs also abound in this neighborhood.

Find the best Charlotte neighborhood for you

Are you ready to pack your bags for the big move to Charlotte but not sure what neighborhood is best for you? Check out this neighborhood quiz to help you decide. You’re sure to find the perfect place for you, given the wide variety of neighborhoods available in the city.

If you’re ready to make the move and need to find your next home, you can check out apartments for rent in Charlotte here. Enjoy the Queen City!

The rent information included in this article is based on a median calculation of multifamily rental property inventory on Apartment Guide and Rent. as of November 2021 and is for illustrative purposes only. This information does not constitute a pricing guarantee or financial advice related to the rental market.

Regardless of how you celebrate, the right credit card can help you hold on to more of your cash this holiday season.

Chase Freedom Flex℠

Wholesale clubs.

Select charities.

Discover it® Cash Back and select Discover cards

Amazon.com.

Target (in store and online).

Both cards earn 1% back on all other non-bonus-category spending. You must activate the 5% categories to be eligible for bonus rewards.

Chase cardholders can activate bonus categories online or in the Chase app by Dec. 14, 2023, and bonus rewards can be earned retroactively. For eligible Discover cards, bonus rewards can be earned starting from the date cash-back categories are activated online.

Here are some tips to maximize your bonus categories this quarter:

Overall tip: Set your default payment method

Whether you’re earning cash back with Chase or Discover, you’ll want to set your card as the default payment method for each eligible bonus category. This will ensure you don’t miss out on bonus rewards when you pay.

PayPal is widely accepted by online merchants, and even by some brick-and-mortar stores. Regardless of where you use it, add the Chase Freedom Flex℠ to your PayPal account and set it as your primary payment method, if you haven’t already.

Shopping on Amazon or Target.com? Set your Discover it® Cash Back or other eligible Discover card as the default card in those accounts.

Optimizing the Chase Freedom Flex℠

Use PayPal, both in-store and online

Most people associate PayPal with online shopping — but did you know you can also use PayPal to checkout in-store at some major retailers like Best Buy and Walmart, and even for in-flight purchases with United Airlines? According to PayPal, the payment platform is now accepted at millions of small and large merchant locations globally. That huge acceptance footprint should make it even easier to maximize your rewards this holiday season. Just be sure to set your Chase Freedom Flex℠ as the preferred payment card in your PayPal app so you don’t miss out on that bonus cash back.

🤓Nerdy Tip

Rewards won’t “stack” if you make one transaction across multiple bonus categories. For example, if you make a qualifying charitable contribution through PayPal, you’ll only be eligible to earn up to 5% cash back on that transaction.

Buy in bulk at wholesale clubs

From cleaning supplies to bulk food items and beyond, wholesale clubs like Sam’s Club and BJ’s offer a great way to stock up on supplies you’ll use well after the holiday season. With some thoughtful spending, you can lock in that bonus cash back for items you won’t use until 2024. Just be aware of exclusions: You won’t earn bonus cash back on gas or other in-club services like cell phone plans, insurance or travel packages.

Another major caveat: Costco stores don’t accept Mastercard, meaning you can’t use the Chase Freedom Flex℠ (which runs on the Mastercard payment network) for in-club purchases. However, you can still earn bonus cash back by using your card through the Costco website. This works even for purchases you make online but pick up at your local store.

Make a charitable donation

The holidays are a perfect time to give back. If your personal budget allows for charitable giving, you can earn bonus cash back for using your Chase Freedom Flex℠ to make a donation to select charities (see below for a complete list). Be sure to account for any transaction fees you may incur for using a card before making the donation. If the fee is greater than the rewards you’ll earn, you’d be better off writing a check. Depending on your tax situation, donations to a qualifying charity may be tax-deductible, leading to additional savings.

List of eligible charities

American Red Cross.

Equal Justice Initiatives.

Feeding America.

Habitat for Humanity.

International Medical Corps.

International Rescue Committee.

Leadership Conference Education Fund.

NAACP Legal Defense and Educational Fund.

National Urban League.

Thurgood Marshall College Fund.

United Negro College Fund.

UNICEF USA.

United Way.

World Central Kitchen.

Out and Equal.

Chase Freedom® and Chase Freedom Flex℠ bonus rewards categories for 2023

Q1 (Jan. 1-March 31)

Grocery stores.

Fitness clubs and gym memberships.

Q2 (April 1-June 30)

Amazon.com.

Q3 (July 1-Sept. 30)

Gas stations and electric vehicle charging.

Select live entertainment.

Q4 (Oct. 1-Dec. 31)

Wholesale clubs.

Select charities.

Optimizing the Discover it® Cash Back

Earn cash back from your couch

In today’s busy world, Amazon has become synonymous with convenience. From electronics to pet food, you can shop from your couch for almost anything at the world’s largest retailer. And through the last quarter of 2023, paying with an eligible Discover card can earn you bonus cash back.

Qualifying purchases include those made on Amazon.com and through the Amazon app, including digital downloads, Amazon Fresh orders, Amazon Local Deals, Amazon Prime subscriptions and items sold through third-party merchants.

If you don’t need to make an immediate purchase, reload your Amazon gift card balance and grab that bonus cash back for a future purchase. Amazon also sells a selection of third-party gift cards. If you’re making a purchase at another retailer, first see whether Amazon sells a gift card to that retailer. You could earn bonus cash back on the gift card purchase, then use the gift card with the other merchant.

Target bonus cash back

Jeans? Groceries? A new flat-screen TV? Whatever you’re looking for, there’s a good chance Target sells it. And for the fourth quarter of 2023, purchases made in Target stores, at Target.com and on the Target app all qualify for bonus cash back with your eligible Discover card. If you’re shopping online or in the app, be sure to make your eligible Discover card the default payment method.

Gift cards make for a perfect stocking stuffer, and Target stores carry an extensive selection of third-party gift cards. Just head to the gift card rack and get rewarded for rewarding your friends, loved ones or colleagues.

Discover bonus rewards categories for 2023

Q1 (Jan. 1–March 31)

Grocery stores.*

Drugstores.

Select streaming services.

Q2 (April 1–June 30)

Restaurants.

Wholesale clubs.

Q3 (July 1–Sept. 30)

Gas stations.

Digital wallets.

Q4 (Oct. 1–Dec. 31)

Amazon.com.

Target, including Target.com and the Target app.

*The grocery stores category does not include grocery purchases at Walmart or Target or at other superstores or wholesale clubs.

The Chase INK Cash and INK Unlimited signup offer recently increased to 90,000 points, and yet the offer via referral link is (for now) still just 75,000 points. A lot of people wonder if they can signup using a referral link to get their friend the 40,000 bonus points, and then request a match from Chase to get the signup offer bumped up to 90,000 points.

We’ve now seen multiple recent reports of Chase agreeing to match the offer (1, 2, 3, 4), and this lines up with the other INK signup offers we’ve seen lately. Simply send Chase a Secure Message from within the online login with a link to the 90,000 offer (Cash link | Unlimited link) and ask if they can match it.

And so I’d be comfortable signing up for the 75,000 offer via a friend’s referral link with the assumption that I’ll be able to get the bonus increased to 90,000.

Crossing over the Ohio River from Kentucky right into the Queen City is breathtaking, as it’s known for its architecture and expansive skyline. After a decline in population since the 1950s, Cincinnati has been slowly but steadily growing since the aughts.

Today, the greater Cincinnati population clocks in just below 1.8 million, with a median age of 32 years old. The average income of Cincinnati residents is a little over $40,000. Cincinnati isn’t the cheapest for its cost of living, but it’s definitely not the most expensive, so many are able to live comfortably.

Cincinnati’s culture is booming, as the city works with local businesses to bring bold colors, flavors and brews into town. The fine arts scene is expansive and residents love festivals, so there’s always something to do. Cincinnati is home to the University of Cincinnati and Xavier University, along with pro sports teams like the Cincinnati Bengals, Cincinnati Reds, FC Cincinnati and the minor-league hockey team, Cincinnati Cyclones. Made up of 52 neighborhoods with individual cultures, events and perks, there truly is something always going on in the Queen City! Here are the best neighborhoods in Cincinnati.

Median 1-BR rent: $685

Median 2-BR rent: $915

Walk score: 67/100

Clifton is historic and eclectic. Located in the heart of Cincinnati, it’s pretty convenient. Just nine minutes away from Downtown, it’s near the University of Cincinnati and its medical centers. Thanks to its location, the residents are a good mix of doctors, young professionals, students and artists alike.

The homes are what you might expect from a downtown area. Lots of trees line the old streets and cottages and mansions are speckled throughout the residential areas. But there’s one thing that’s different about Clifton: The neighborhood isn’t too partial toward chain restaurants and shops. So, in the heart of the borough on Ludlow Avenue, all the dining and shopping is local.

Median 1-BR rent: $710

Median 2-BR rent: $950

Walk score: 42/100

College Hill used to have two colleges. Although both colleges have closed down, the area maintains the well-manicured streets typical of college campuses. That combined with the local revitalization efforts going on thanks to the College Hill Community Urban Redevelopment Corporation (CHCURC) and $43.1 million building plans split between rentals and retail spaces, College Hill has been building up to the cusp of a big boom for years.

Plus, the area has big breweries coming in to join existing pubs, bringing in more outside traffic and attention to the area.

Median 1-BR rent: $675

Median 2-BR rent: $860

Walk score: 44/100

Columbia Tusculum, sometimes referred to as the oldest neighborhood in Cincinnati (dating back to a month before Cincinnati debuted in 1788), is home to the Victorian “Painted Ladies,” a row of brightly painted architectural homes overlooking the Ohio River.

The area has plenty of pubs and breweries — arguably more than restaurants — along with plenty of gyms and fitness centers. Here, residents can enjoy the hilly, river-view 94-acre Alms Park. Easy to see why this is one of the best neighborhoods in Cincinnati.

Median 1-BR rent: $1,532

Median 2-BR rent: $2,381

Walk score: 52/100

Downtown Cincinnati is the place for residents constantly looking for something to do. It’s got a little bit of everything for everyone. The kids enjoy the splash pad in Washington Park during hot summer days, and everyone in the family loves a trip to the Play Library to rent out games and toys for family game nights. There are ample boutiques and shops downtown to score local finds, clothes, vintage goods, plants and greens, kitchen utensils and even an old-school hat shop.

The Cincinnati Museum Center at Union Terminal is home to several museums inside the 1933 Art Deco train station. Look for the Cincinnati History Museum, the Duke Energy Children’s Museum, the Museum of Natural History & Science and the Cincinnati Historical Society Library. Bonus: It’s home to the OMNIMAX Theatre, too. Throw in some amazing dining and bar options, plus a few outdoor shows and concerts, and Downtown really is fun for everyone.

Median 1-BR rent: N/A

Median 2-BR rent: N/A

Walk score: 52/100

East End is one of the oldest neighborhoods in Cincinnati. Back in the day, it was known for the sublime wooden ships built in the shipyard. Located right off the bend of the Ohio River, this area saw a mass exodus, like much of the rest of the city, as residents fled for the suburbs. But now, seeing its potential, developers have started returning to the riverside area, bringing with it new amenities and residencies, retailers and restaurants.

Median 1-BR rent: $1,150

Median 2-BR rent: $1,100

Walk score: 70/100

Since 1896, Hyde Park has sought to provide residents with a quiet place to call home. It’s done just that, while providing a well-balanced mix of nature-driven and architectural respite, too.

At the heart of this best neighborhood in Cincinnati is the Square, a well-manicured lawn perfect for sitting under the shady trees to enjoy the weather, rest after browsing local shops or eateries or meet up with friends.

Median 1-BR rent: $1,100

Median 2-BR rent: $1,725

Walk score: 66/100

If you dream of a chill neighborhood with a view overlooking the city and the Ohio River, Mount Adams is what you’ve been looking for! Located on a hilltop for peak visibility, Mount Adams is the perfect mix between San Francisco and a European village.

As one of the more upscale areas, doctors, lawyers and young professionals tend to call this place home. But don’t let that fool you. While it’s a quiet area throughout the week, these professionals and neighboring college students line the streets to enjoy the nightlife. With loads of different food options, residents’ palettes are rarely bored.

Close to Downtown, there’s also an outdoor amphitheater and Playhouse in the Park, where visitors can catch a play or performance throughout the year.

Median 1-BR rent: $1,254

Median 2-BR rent: N/A

Walk score: 54/100

Mount Lookout is a hilly, slightly ritzy neighborhood with incredible views. It’s home to the country’s oldest working telescope at the Cincinnati Observatory (National Historic Landmark) and has an incredible vineyard-turned-park that’s a fan-favorite among locals.

The area is also packed with great dining and café options, along with a beautiful town square lined with shops and businesses.

Median 1-BR rent: $1,081

Median 2-BR rent: $1,430

Walk score: 66/100

Northside is a quick 15-minute commute north of Downtown and has become quite the hipster hangout. With coffee houses, breweries and pubs to call home, it’s no wonder there’s such a Northside following, making this one of the best neighborhoods in Cincinnati.

The neighborhood is notably a safe space for LGBTQ+ members thanks to the presence of allies and supporters. With an annual 4th of July parade and other events, everyone can feel at home in Northside.

Median 1-BR rent: $955

Median 2-BR rent: $1,350

Walk score: 95/100

Located just north of Downtown, German immigrants tended to settle into this area back in the day. Having to cross the Miami and Erie Canal to get to work, residents started calling it “the Rhine,” like the river that runs through Germany. Thus, the neighborhood’s name, Over the Rhine, was born.

It’s hard to imagine now, but Over the Rhine was once seen as one of the most crime-infested and dangerous areas in the city. However, over the past decade, Cincinnati has been pouring money and investments into the area to revitalize it. These efforts have worked and many Cincinnatians say OTR is now one of the most interesting and eclectic neighborhoods the city has to offer.

Once the city funding came through, trendy bars, restaurants and shops started coming into the area. The new businesses and the community mainstays, like the 1878 Music Hall that hosts symphonies, operas and ballets, have made OTR a beloved Cincinnati staple.

Median 1-BR rent: $1,299

Median 2-BR rent: $1,510

Walk score: 52/100

Pendleton, located to the east of Over the Rhine, is often referred to as the arts district. Not only is the Pendleton Art Center located there, but many residents have livened up the area by bringing bright colors to their homes’ exteriors and businesses have followed suit, as there are ample murals all over local shops and restaurants.

Aside from art, there’s a great food scene, lots of things to keep kids busy and cafés and bars for the adults. The supportive neighborly vibes run deep in this bright, cheery area.

Median 1-BR rent: $849

Median 2-BR rent: $1,054

Walk score: 46/100

Pleasant Ridge is one of Cincinnati’s oldest neighborhoods, dating back to 1795. Now, it holds up its end of a storied past, as most of the businesses have been locally and independently owned for years and years, earning Cincinnati’s first Community Entertainment District title.

After a push to reinvigorate the area in the early 2000s, Pleasant Ridge has been basking in the rays of success and is still a trending neighborhood today. The charming town is colorful, too, as its business district has murals throughout.

Median 1-BR rent: $1,299

Median 2-BR rent: $1,510

Walk score: 52/100

Traditionally, South Fairmount has been an overlooked area. Most people wrote it off as hopeless. But with $100 million being funneled into the neighborhood, it’s quickly turning around.

Thanks to the Lick Run Greenway, a creek with wide sidewalks running alongside the water, South Fairmount is on the upswing. What was once dreary and gloomy, this area is getting a lot of attention from businesses and restaurants looking to capitalize on the new Greenway’s attention and it’s the perfect time to join in on the commotion.

Median 1-BR rent: $944

Median 2-BR rent: $1,124

Walk score: 67/100

Founded back in 1804, Walnut Hills is rich with history and culture. One house in the neighborhood was a stop for the Underground Railroad, thanks to its resident, author of “Uncle Tom’s Cabin,” Harriet Beecher Stowe. Her house is now a historic landmark and offers tours.

Just two miles from Downtown Cincinnati, Walnut Hills serves as an overflow area for top professionals and creatives alike. Home to Eden Park, Walnut Hills residents can enjoy a lovely scenic stroll scattered with fountains, sculptures and playgrounds, along with the Art Museum and Kohn Conservatory.

Median 1-BR rent: $736

Median 2-BR rent: $760

Walk score: 29/100

Westwood is the city’s biggest neighborhood and has been through quite a revolution over the past couple of years. It’s still in the process of its makeover and newer residents have been smart to jump aboard and join the team.

Residents tend to stick around and for good reason. They see real potential in the neighborhood and they’re willing to find out they were right. Westwood’s foodie scene has popped off. From pizza to delis to more adventurous options like Ethiopian food, just about anything you try in Westwood is something worth writing home about

Find the best Cincinnati neighborhood for you

If one of these neighborhoods sounds like your ideal future home, be sure to check out these apartments for rent in the best neighborhoods in Cincinnati.

The rent information included in this article is based on a median calculation of multifamily rental property inventory on Apartment Guide and Rent. as of November 2021 and is for illustrative purposes only. This information does not constitute a pricing guarantee or financial advice related to the rental market.

After many years of using the Bank of America Premium Rewards card as my primary driver, I finally decided to close out the card and avoid the upcoming annual fee. The card’s main draw for me is the 2.62% on everyday spend with relationship status, and I’m getting that on the no-fee Unlimited Cash Rewards card.

Sure, there’s the $100/yr. travel benefit which can basically offset the $95 annual fee, and there’s the 1.5x on travel & dining along with some other perks, but I wasn’t getting enough value from that and decided it’s time to break up. (I’m also considering signing up for the Elite version of the Premium Rewards card near year-end for a potential triple-dip…)

First, I paid down the balance and cashed out all rewards on the Premium Rewards card. Then, I called in and easily reallocated most of the credit line over to my Unlimited Cash Rewards card. (There does not appear to have been any hard pull for me with the reallocation.) The BofA rep was surprised that the system allowed him to bring the credit line down under $5,000 on the premium card.

After giving a few days to let the payment settle and rewards cashout process, I called in to close out the card. I made sure to call in a few days before the annual fee posts since there’s no guarantee of getting a refund, even if you cancel soon-after it posts (though you often will get a refund). Luckily, a few weeks before the annual fee date, BofA send me a notice mail warning of an impending annual fee.

I did not ask for a retention offer, and the rep did not mention any offer.

The rep mentioned that instead of closing it out, we can product change to one of their no-fee cards and avoid the annual fee. I had somehow forgotten about product changing. She mentioned the Customized Cash Rewards card which earns 3%/5.25% on the category of your choice, up to $2,500 per quarter. And so instead of closing the Premium Rewards card, I opted to product change it to a Customized Cash Rewards card. I’ll choose the Online Shopping category and see if it turns out useful for me.

After completing the card conversion, the rep was easily able to reallocate $5,000 of the credit line from my Unlimited Cash Rewards back to the new Customized Cash Rewards card. The new credit line shows up immediately after logging back in. She mentioned that the card number might change, but the full card credit history will remain on my credit report with all of the years that the card has been open.

After completing the product change and reallocation, the rep mentioned that there’s a retention offer available for me. I was honestly confused given that she had already retained the card account. Apparently, once they saw me consider leaving they wanted to give me a spend offer to keep me happy.

The retention offer was to get $175 statement credit after spending $1,500 by December. Per the rep, the spend can be done on any single one of my BofA personal credit cards, but only on a card already open at this time. For me, that’s the Unlimited Cash Rewards card, the Travel Rewards card, and the Customized Cash Rewards card.

Easy win. I found this new kind of “retention” offer interesting. Hopefully I’ll have $1,500 of online shopping spend for my shiny new Customized Cash Rewards card which will trigger the $175 bonus, alongside the regular 5.25% earn rate.

There are many reasons you might want to pay a loan with a credit card. Maybe you want to earn rewards on your mortgage payment. Or maybe you want a reprieve from interest on your auto loan by paying off the balance with a card’s 0% APR offer.

Unfortunately, most loan types prohibit you from making a payment directly with a credit card. Yes, there are some workarounds, but higher interest rates, processing fees and potential risk factors generally make those methods inadvisable.

Here are some potential ways to pay a loan with a credit card.

Ready for a new credit card?

Create a NerdWallet account for insight on your credit score and personalized recommendations for the right card for you.

Transfer your loan to a credit card

You may be able to transfer your existing loan balance to a credit card. However, this would make sense only if the interest rate on the credit card is lower than the rate on your existing loan.

While interest rates will vary based on your credit scores, most credit cards will carry a higher APR than other types of loans. As of May 2023, the average APR across all consumer credit cards that charged interest was 22.16%, according to the Federal Reserve. By comparison, the average rate on auto loans for the same period was 6.63% for new cars and 11.38% for used cars (according to Experian), and the average APR for new federal student loans was 5.50%.

One exception could be a balance transfer to a credit card that offers an introductory 0% APR period — but there are risks. The longest 0% intro APR periods generally cap out at 18 to 21 months, and you’ll need to be approved for a credit limit on the card greater than your existing loan amount to transfer the full balance. You’ll usually incur a fee to transfer the loan, typically between 3% and 5% of the total balance. And if you don’t pay off the transferred balance before the 0% APR period expires, you’ll then start to incur interest on the remaining balance at the normal, ongoing (and much higher) APR.

Use a third-party service

Some third-party payment processors, such as Plastiq, allow you to use a credit card to pay vendors that don’t otherwise accept cards. This might be an option if you’re temporarily strapped for cash or you’re trying to snag a sign-up bonus. But be aware that you’re going to incur a healthy processing fee for using the service, and if you don’t end up paying off your card balance on time, you’ll owe interest on it at whatever rate your credit card normally charges.

Tap your card’s cash advance limit

A credit card cash advance is a short-term loan against the credit line on your card. A cash advance can let you quickly access cash to pay down your loan, but it’s among the most expensive ways to pay a loan with a credit card. You’ll incur a cash advance fee from your card issuer, which could be either a flat rate or a percentage of the total advance amount. There’s also no grace period, so you’ll start accruing interest the second you receive the advance. And that interest rate on cash advances is usually higher than for regular purchases.

Because these costs will likely be higher than the interest payment on your existing loan, a cash advance is inadvisable.

Use your card’s ‘flexible financing’

“Flexible financing” programs like My Chase Loan and Citi Flex Loan allow you to get a loan against your card’s existing credit line. You’ll pay a fixed interest rate and pay the loan back over time, typically from six to 24 months. Similar to a cash advance, this could give you an immediate cash infusion directly to your bank account, which you’d use to pay off your existing loan. But if the APR your card gives you for that loan is higher than the existing loan you’re trying to pay off, it won’t make sense.

Should you pay a loan with a credit card?

While it’s possible to pay a loan with a credit card, it will almost always cost you to do so. That cost usually comes in the form of transaction fees and higher interest rates.

Transferring an existing loan to a credit card offering a 0% intro APR on balance transfers could make sense for some people, but typically only if you know you’ll be able to pay off the balance in full by the time that promotional window ends.