For most people, the Chase Sapphire Preferred® Card is a better starting point in the travel rewards market. (There’s a reason NerdWallet describes it as “nearly a must-have for travelers.”) It offers higher rewards earnings on everyday purchases, and those rewards carry a 25% higher redemption value when used to book travel through the Chase travel portal. That’s a lot of value for a modest annual fee of $95.

The Platinum Card® from American Express is marketed as a premium travel card. Its rewards earning rates focus on select travel spending, and it carries more luxury benefits, including lounge access, high-end fitness, shopping and hotel credits. However, those premium benefits come with a premium annual fee of $695 — a hard cost to justify for many people.

Here’s a side-by-side comparison so you can decide which card is right for you.

How the cards compare

Chase Sapphire Preferred® Card

on Chase’s website

The Platinum Card® from American Express

Annual Fee

Welcome offer

Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That’s $750 toward travel when you redeem through Chase Ultimate Rewards®.

Earn 80,000 Membership Rewards® Points after you spend $8,000 on purchases on your new Card in your first 6 months of Card Membership.

Terms apply.

Rewards

5 points per $1 spent on all travel purchased through Chase Ultimate Rewards®.

3 points per $1 spent on dining (including eligible delivery services and takeout).

3 points per $1 spent on select streaming services.

3 points per $1 spent on online grocery purchases (not including Target, Walmart and wholesale clubs).

2 points per $1 spent on travel not purchased through Chase Ultimate Rewards®.

1 point per $1 spent on other purchases.

Through March 2025: 5 points per $1 spent on Lyft.

Points are worth 1.25 cents apiece when redeemed for travel through Chase Ultimate Rewards®.

5 Membership Rewards points per $1 spent on flights booked directly with airlines or with American Express Travel.

5 points per $1 spent on prepaid hotels booked through American Express Travel.

2 points per $1 spent on other eligible travel booked through AmEx.

1 point per $1 spent on all other purchases.

Other benefits

A $50 annual credit on hotel stays purchased through Ultimate Rewards®.

Each account anniversary, cardmembers will earn bonus points equal to 10% of total purchases made the previous year.

1:1 transfer partners, including United, Southwest, JetBlue, Marriott and Hyatt.

$200 annually for airline incidentals, like bag fees, on one designated airline when you enroll.

$200 annually for prepaid hotel bookings through American Express Travel at more than 2,000 hotels. (Fine Hotels and Resorts or The Hotel Collection properties.)

$189 annually for Clear membership.

$100 statement credit every 4 years for a Global Entry application fee or a statement credit up to $85 every 4.5 years for a TSA PreCheck when charged to your card.

1:1 transfer partners, including Air Canada, Air France, British Airways, Delta and Virgin Atlantic.

Terms apply.

Lounge access

Access for you and 2 guests to over 1,400 lounges worldwide from partners including Priority Pass and Plaza Premium Group. Terms apply.

Access to over 40 American Express Centurion and Escape lounges. Terms apply. Fees may apply for guest access.

Foreign transaction fee

Still not sure?

Why the Chase Sapphire Preferred® Card is better for most people

Lower annual fee

The Chase Sapphire Preferred® Card packs a lot of punch in terms of travel rewards value, all with a manageable $95 annual fee. Compare that with The Platinum Card® from American Express’s eye-popping $695 annual fee — an intimidating figure for many travelers. While the Amex Platinum does advertise a wide range of travel and shopping credits to offset that fee, taking full advantage of those benefits can be burdensome.

More value, more dometic transfer partners

When using your points to book travel through the issuer’s portal, Chase Ultimate Rewards® are more valuable. Points earned from the Chase Sapphire Preferred® Card are worth an impressive 1.25 cents per point. That’s an outsized value compared with the American Express travel portal, where Membership Rewards points are redeemed at one cent per point on flights and certain hotel bookings. Other hotel bookings made through AmEx carry a value of 0.7 cent per point.

Plus, Chase’s transfer partners include several well-known domestic airlines and hotel brands, offering easy accessibility for points redemption. American Express offers more transfer options than Chase, and savvy travelers can find outsized value for their points. But AmEx’s transfer partners are primarily foreign airlines, making Membership Rewards points more challenging to transfer for U.S.-based domestic travelers.

Full list of Chase transfer partners

Aer Lingus (1:1 ratio).

Air Canada (1:1 ratio).

Air France-KLM (1:1 ratio).

British Airways (1:1 ratio).

Emirates (1:1 ratio).

Iberia (1:1 ratio).

JetBlue (1:1 ratio).

Singapore (1:1 ratio).

Southwest (1:1 ratio).

United (1:1 ratio).

Virgin Atlantic (1:1 ratio).

Hyatt (1:1 ratio).

InterContinental Hotels Group (1:1 ratio).

Marriott (1:1 ratio).

Full list of AmEx transfer partners

Aer Lingus (1:1 ratio).

AeroMexico (1:1.6 ratio).

Air Canada. (1:1 ratio).

Air France/KLM (1:1 ratio).

ANA (1:1 ratio).

Avianca (1:1 ratio).

British Airways (1:1 ratio).

Cathay Pacific (1:1 ratio)

Delta Air Lines (1:1 ratio).

Emirates (1:1 ratio).

Etihad Airways (1:1 ratio).

Hawaiian Airlines (1:1 ratio).

Iberia Plus (1:1 ratio).

JetBlue Airways (2.5:2 ratio).

Qantas (1:1 ratio).

Qatar Airways (1:1 ratio).

Singapore Airlines (1:1 ratio).

Virgin Atlantic Airways (1:1 ratio).

Choice Hotels (1:1 ratio).

Hilton Hotels & Resorts (1:2 ratio).

Marriott Hotels & Resorts (1:1 ratio).

Better earnings rates on everyday spending

Both cards earn 5x per $1 spent on travel booked through their travel portals, but the Chase Sapphire Preferred® Card is the clear winner for everyday spending. It earns 3x on dining, streaming services, and online grocery purchases (excluding Walmart, Target and wholesale clubs), while the Amex Platinum earns 1x in each of those categories. Terms apply.

Get a card that takes you farther

Sign up with NerdWallet to get a full picture of your spending and personalized recommendations for cards that will help you see the world.

Why you might want The Platinum Card® from American Express

Lounge access

In this category, there’s no competition. If airport lounge access is a high priority, you’ll be best served by The Platinum Card® from American Express.

Where the Chase Sapphire Preferred® Card offers no lounge access, the AmEx Platinum is known for its top-notch airport lounge benefits, including access to over 1,400 lounges in more than 500 airports worldwide. Those include more than 40 American Express Centurion and Escape lounges, and additional access through partners like Priority Pass and Plaza Premium Group. Terms apply.

Booking with the airline

When it comes to booking flights, experienced travelers know that the way you book can make a big difference in the ease of changing or canceling your plans. So while both the Chase Sapphire Preferred® Card and Amex Platinum offer 5 points per dollar spent on flights booked through their respective travel portals, The Platinum Card® from American Express has a leg up in offering that same earnings rate for flights booked directly through the airline. Terms apply.

The Sapphire Preferred, on the other hand, offers the 5x points rate only if you book your flights through the Chase travel portal. That can pose a problem in the event of a weather delay, cancellation, or any other trip interruption.

The prestige factor

Both cards are metal, but The Platinum Card® from American Express carries a certain luxury gravitas that the Chase Sapphire Preferred® Card can’t compete with — and doesn’t try. That prestige has some cash value, too. When used correctly, the card’s luxury perks add up quickly to help offset its eye-popping annual fee. When you enroll, those include statement credits of up to $300 per year toward an Equinox gym membership, $50 twice per year at Saks Fifth Avenue, $200 per year in Uber cash ($15 per month plus an extra $20 in December), and $200 a year for prepaid hotel bookings through The Hotel Collection or Fine Hotels + Resorts properties, just to name a few. Terms apply.

However, if these benefits don’t match your lifestyle, you’ll be paying mostly for the cachet of pulling the famous platinum card out of your wallet. Only you can decide how much that prestige is worth.

Which card should you get?

The Chase Sapphire Preferred® Card and The Platinum Card® from American Express are two of the best travel rewards cards on the market, but they have different strengths and weaknesses. Chase Sapphire Preferred® Card is a great choice for travelers who want a card with a low annual fee and great rewards for everyday spending. The Amex Platinum may be the better choice for frequent travelers who value lounge access and luxury benefits — but given the card’s steep $695 annual fee, it’s important to make sure you can take full advantage of all those benefits before you sign up.

To view rates and fees of The Platinum Card® from American Express, see this page.

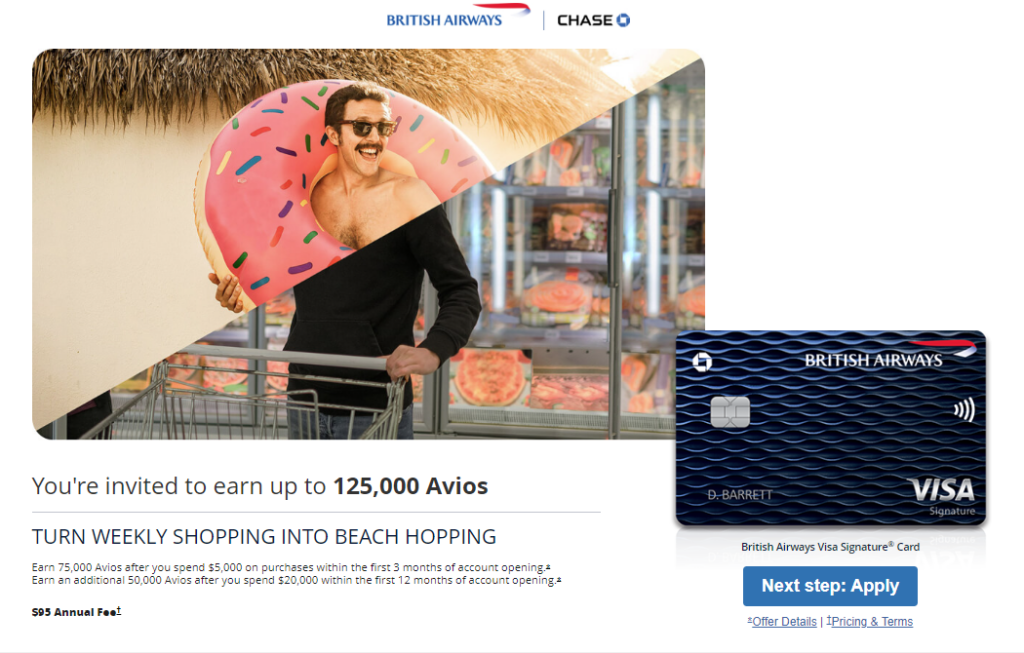

Direct link to offer : British Airways | Aer Lingus | Iberia

Chase is offering up to 125,000 points on the Chase British Airways card

75,000 points after $5,000 in spend within the first 3 months

An additional 50,000 points after $20,000 in spend within the first 12 months

Card Details

$95 annual fee not waived first year

Chase’s 5/24 rule does apply to this card.

Card earns at the following rates:

Earns 3 Avios per $ on British Airways purchases

Earns 1 Avios per $ on all other purchases

As a general rule, Chase does match offers.

Our Verdict

We’ve previously seen a 100,000 bonus with $5,000 in spend, but recently bonuses were 75,000 points after $5,000 in spend or 100,000 points after $20,000 in spend. Not really worth it for most people due to the high spend requirement. We won’t add this to our list of the best credit card bonuses for now.

You may hit one of those life moments where you need a bundle of cash and fast. Maybe you have been hit with a major car repair bill, you want to attend a destination wedding, or you’re motivated to pay off your student loans ASAP.

Whatever the situation, there are smart strategies that will help you accrue that money as quickly as possible. Tactics like trimming your expenses, selling your unwanted stuff, and bundling your insurance can help you meet a savings goal at top speed.

In this guide, you’ll learn those techniques and more to help you finance whatever is most urgent on your financial to-do list.

How to Save Money Fast 10 Ways

One person’s goal for saving money quickly might be, “I need $500 by the end of the week.” For another, it could be, “I’m going to stash away $10,000 within the next year.” Wherever you may fall in terms of your short-term financial goals, these 10 tactics will help you save money daily and achieve your aspiration.

💡 Quick Tip: Make money easy. Open a bank account online so you can manage bills, deposits, transfers — all from one convenient app.

1. Getting Rid of Unnecessary Expenses

In an age of automated billings and subscriptions, it is easy to lose track of what exactly you’re paying for each month. It is entirely possible that you’re paying for something you’re not even using.

In order to pinpoint any potentially unwanted expenses, review a month’s worth of auto debits from your bank account. You may find that you’re paying $5 a month for a digital magazine you no longer read or that you could save on streaming services by dropping one or two you don’t watch but are paying $15 a month for.

Once you’ve canceled, you could reroute the money you would have spent directly into your savings account. While $20 or $30 a month saved on subscriptions might not seem like much, even small amounts can quickly add up over time. In combination with other savings techniques, this might help you build your savings fast.

Ready for a Better Banking Experience?

Open a SoFi Checking and Savings Account and start earning up to 4.50% APY on your cash!

2. Negotiating and Automating Your Bill Payments

Did you know that some companies offer discounts when you set up automatic bill payments, or autopay? This means connecting a bill directly to your bank account and allowing the company to automatically withdraw the amount of the bill on the due date.

Some companies offer a discount in these situations because automatically debiting your account gives the company assurance that the bill will be paid on time. The bonus for you is double: You might get a little discount on your bills, and you won’t have to remember to manually pay the bill each month.

Autopay might also help you avoid unexpected late fees, which in turn could help you build up savings faster. There might be some downsides to autopay, however. If you set up an autopay agreement but then don’t have enough money in your account to cover the charge, you might end up with a canceled subscription or overdraft or NSF fees from your bank.

3. Carefully Considering Big Decisions

Yes, it’s hard to save money, but learning to be mindful about your purchases can help. Instead of buying something as soon as you want it, you might want to sleep on it overnight and see if you still want it the next morning. Giving yourself more time before pulling out your credit card could help you determine if you really need the item or if you were just caught up in the excitement of shopping.

This can be especially useful when making big purchases because they might require more research anyway. For example, if you’re buying a couch and you fall in love with a sectional sofa, waiting overnight might give you a chance to read reviews, double-check the measurements of your space, and look to see if there are similar styles available online that might cost less.

Some people wait longer still. They use the 30-day rule, which involves writing a note in your calendar for 30 days after you see the item you want. If you still are determined to buy it when the calendar alert pops up, then you can probably feel confident that it isn’t an impulse buy and go for it.

By delaying purchases this way, you may be able to avoid compulsive shopping and save funds, which can go towards your savings goal.

4. Considering a Spending “Fast”

Ready to learn another way to save money quickly? Some savers find that they can save money fast with a challenge: They plan a day or two every week where they eliminate all unnecessary spending. That’s what’s called a “fast”: You avoid spending money, similar to the way a dietary fast means you eat nothing.

For example, if you decide to do a two-day spending fast, you might decide that on Tuesdays and Wednesdays you don’t spend any money other than what it costs to commute to work. That means that on those days, you might choose to forgo your daily pitstop at the coffee shop, a lunch from the salad place (you’d bring food from home), or ordering the brand new book you’ve been waiting to read.

Planning to not spend could help you reign in unintentional spending. Chances are that you barely think about that $4 you spend at the coffee shop, but if you give it up twice a week, that’s $8 that could be going into your savings.

If you save an average of $40 a week with a two-day fast, that could add more than $2,000 to your savings in a year.

5. Putting Your Accounts to Work

Choosing the right account for your money can be a great way to save funds fast. Some checking accounts charge monthly or annual account maintenance fees, with little to no interest.

Savings accounts might offer higher interest rates than a checking account, but the reality is that the average interest rates on a standard savings account can still be very low. Instead, you might shop around for a no-fee, high-interest account to make your money work harder for you. These kinds of accounts are often found at online vs. traditional banks.

If you currently have, say, $5,000 sitting in a checking account, earning no interest, if you were to put it in a savings account at 4.50% interest compounded daily, you’d have an extra $230.12 a year later, with no effort on your part.

💡 Quick Tip: Want a simple way to save more each month? Grow your personal savings by opening an online savings account. SoFi offers high-interest savings accounts with no account fees. Open your savings account today!

6. Bundling Your Insurance

Insurance can be one of those “set it and forget it” expenses. You might buy a policy and then never really focus on the cost of the premium again.

Many insurers, however, will reduce your rate if you give them more of your business. Typically, this means having your auto and home insurance with the same company. You might be able to save a chunk of change and put it towards your savings goal.

It can also be wise to review your insurance annually. You might be paying for coverage you don’t really need.

7. Starting a Side Hustle

Sure, cutting back on your spending is one way to save money fast. But so is bringing in more cash. Many people find starting a side hustle is a good way to bring in more income. This could mean anything from selling your nature photography on Etsy or providing social media services to a local business or two.

While one of the key benefits of a side hustle is the money it can bring in, you also might find it personally rewarding and even an entry to a new full-time career.

8. Saving on Essentials

Looking for another idea for how to save money fast? There’s no doubt that many things you spend money on are necessities. Food, personal-care items, and gas for your car. But there are plenty of ways you can trim those costs.

• To save on food, you could do some meal-planning so you can more efficiently manage your grocery budget. Using up what you buy vs. wasting food can help you save a bundle towards your goals.

• You could get a gas card to save at the pump. There are also plenty of apps that point you towards the cheapest gas stations in your area.

• Joining a warehouse or wholesale club can help you save on your typical purchases. If you find the quantities too large (say, a 12-pack of shampoo), partner up with a friend of two to share the wealth.

9. Selling Your Stuff

If you’re trying to save money fast, you might be able to “find” a pile of cash by selling your used items that you no longer need. This could mean anything from selling gently worn clothes online (say, on Poshmark or thredUP) or IRL (at Buffalo Exchange perhaps); putting functional electronics up for sale on eBay; or offering items on places like Nextdoor or Facebook Marketplace.

Just be cautious as there are scammers who try to prey on direct sellers.

10. Checking Your Tax Withholding

Here’s another idea for accumulating money quickly: Double-check your tax withholding. If you get a sizable tax refund every year, you may feel as if you are getting “free money.” Not at all! That’s actually your hard-earned money that you overpaid to the government and are now getting back. It could have been earning interest in the bank rather than being whisked out of your paycheck.

If you typically receive a refund, tweak your withholding, and then put the additional money that stays in your paycheck into your savings.

Is Saving Money Fast Realistic?

Saving money fast can be realistic, as long as you keep in mind your income and the fact that most financial experts say to save 20% of that figure. That’s one of the principals of the popular 50/30/20 budget rule. Fifty percent of your money goes towards essential spending, 30% goes to discretionary expenses, and 20% gets socked away as savings.

So, if you earn $100,000 a year and have an important goal in mind, such as the down payment for a house, you might be able to stash $20K in a single year. That might involve pausing your retirement savings for a year as you go all-in on accumulating as much cash as possible for a home purchase.

Also, if you are able to bring in more income (whether by selling your stuff, starting a side hustle, or via passive income ideas), that can accelerate your savings as well.

Keeping Your Savings Safe With SoFi

Whichever strategies (or combination of tactics) you try, it’s important to find the right banking partner where your money can grow. You’ll likely want a financial institution with Federal Deposit Insurance Corporation coverage, low or no fees, and a healthy interest rate.

Interested in opening an online bank account? When you sign up for a SoFi Checking and Savings account with direct deposit, you’ll get a competitive annual percentage yield (APY), pay zero account fees, and enjoy an array of rewards, such as access to the Allpoint Network of 55,000+ fee-free ATMs globally. Qualifying accounts can even access their paycheck up to two days early.

Better banking is here with up to 4.50% APY on SoFi Checking and Savings.

FAQ

How can I save $1,000 fast?

To save $1,000 fast, you can try a combination of such techniques as trimming subscriptions, essential, and discretionary spending; bundling insurance to cut costs; selling your unwanted items; and/or using the 30-day rule.

How to save up $10,000 in 3 months?

To save $10,000 in three months, you need to save $3,333 after-tax dollars per month. Your income and expenses will influence how doable this is. Some ways to save this amount include going on a spending fast (meaning you eliminate all possible discretionary spending) and starting a side hustle to bring in more money.

How to save $5,000 ASAP?

To save $5,000 ASAP, you can try cutting your expenses, avoiding big purchases, making sure your money is earning a good interest rate, and bringing in more cash via a side hustle.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with direct deposit activity can earn 4.50% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Direct Deposit means a deposit to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Direct Deposit”) via the Automated Clearing House (“ACH”) Network during a 30-day Evaluation Period (as defined below). Deposits that are not from an employer or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, do not constitute Direct Deposit activity. There is no minimum Direct Deposit amount required to qualify for the stated interest rate.

SoFi members with Qualifying Deposits can earn 4.50% APY on savings balances (including Vaults) and 0.50% APY on checking balances. Qualifying Deposits means one or more deposits that, in the aggregate, are equal to or greater than $5,000 to an account holder’s SoFi Checking and Savings account (“Qualifying Deposits”) during a 30-day Evaluation Period (as defined below). Qualifying Deposits only include those deposits from the following eligible sources: (i) ACH transfers, (ii) inbound wire transfers, (iii) peer-to-peer transfers (i.e., external transfers from PayPal, Venmo, etc. and internal peer-to-peer transfers from a SoFi account belonging to another account holder), (iv) check deposits, (v) instant funding to your SoFi Bank Debit Card, (vi) push payments to your SoFi Bank Debit Card, and (vii) cash deposits. Qualifying Deposits do not include: (i) transfers between an account holder’s Checking account, Savings account, and/or Vaults; (ii) interest payments; (iii) bonuses issued by SoFi Bank or its affiliates; or (iv) credits, reversals, and refunds from SoFi Bank, N.A. (“SoFi Bank”) or from a merchant.

SoFi Bank shall, in its sole discretion, assess each account holder’s Direct Deposit activity and Qualifying Deposits throughout each 30-Day Evaluation Period to determine the applicability of rates and may request additional documentation for verification of eligibility. The 30-Day Evaluation Period refers to the “Start Date” and “End Date” set forth on the APY Details page of your account, which comprises a period of 30 calendar days (the “30-Day Evaluation Period”). You can access the APY Details page at any time by logging into your SoFi account on the SoFi mobile app or SoFi website and selecting either (i) Banking > Savings > Current APY or (ii) Banking > Checking > Current APY. Upon receiving a Direct Deposit or $5,000 in Qualifying Deposits to your account, you will begin earning 4.50% APY on savings balances (including Vaults) and 0.50% on checking balances on or before the following calendar day. You will continue to earn these APYs for (i) the remainder of the current 30-Day Evaluation Period and through the end of the subsequent 30-Day Evaluation Period and (ii) any following 30-day Evaluation Periods during which SoFi Bank determines you to have Direct Deposit activity or $5,000 in Qualifying Deposits without interruption.

SoFi Bank reserves the right to grant a grace period to account holders following a change in Direct Deposit activity or Qualifying Deposits activity before adjusting rates. If SoFi Bank grants you a grace period, the dates for such grace period will be reflected on the APY Details page of your account. If SoFi Bank determines that you did not have Direct Deposit activity or $5,000 in Qualifying Deposits during the current 30-day Evaluation Period and, if applicable, the grace period, then you will begin earning the rates earned by account holders without either Direct Deposit or Qualifying Deposits until you have Direct Deposit activity or $5,000 in Qualifying Deposits in a subsequent 30-Day Evaluation Period. For the avoidance of doubt, an account holder with both Direct Deposit activity and Qualifying Deposits will earn the rates earned by account holders with Direct Deposit.

Members without either Direct Deposit activity or Qualifying Deposits, as determined by SoFi Bank, during a 30-Day Evaluation Period and, if applicable, the grace period, will earn 1.20% APY on savings balances (including Vaults) and 0.50% APY on checking balances.

Interest rates are variable and subject to change at any time. These rates are current as of 8/9/2023. There is no minimum balance requirement. Additional information can be found at http://www.sofi.com/legal/banking-rate-sheet..

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

Update 9/21/23: Bonus is at 30,000 if you apply via the Credit Karma link (ht RJ)

As rumored Wells Fargo has launched the new Autograph card. Card details are as follows:

Welcome bonus 30,000 points on $1,500 in first 3 months (worth $300)

Card earns at the following rates:

3x on dining, transit, travel, and streaming services, gas, phone plans

1x everywhere else.

Redemption details:

Rewards can be redeemed in $25 increments for 2,500 points. Or get in $20 increments for 2,000 points at the Wells Fargo ATM.

Minimum of 100 Rewards Points or $1 in Cash Rewards in your Rewards Account is required.

Redeem for Purchases is another option.

Automatica redemptions can be set up in $25 increments.

Points do not expire while this Credit Card account is open.

No annual fee.

No foreign transaction fees.

Visa Signature benefits.

Update History:

Update 5/13/23: Bonus now 20,000 instead of 30,000.

Update 3/25/23: Bonus is 30,000 points when you do a google search for Wells Fargo Autograph. Hat tip to TheBigDonDom. You can also use this link.

Update 1/12/23: Bonus reduced to 20,000 points.

Update 7/20/22: It’s now possible to product change to this card. Most Visa® credit card types are available to switch with the exception of College, Secured, The Private Bank, Wells Fargo Advisors, Hotels.com® and any Propel American Express® cards.

Collecting and trading Pokémon cards has been a popular hobby since the 1990s for both children and adults. In fact, as a kid, I was obsessed with Pokémon cards. I enjoyed opening new packs, collecting cards, and trading with my friends. And, I know I’m not alone. So many people have enjoyed Pokémon cards over…

Collecting and trading Pokémon cards has been a popular hobby since the 1990s for both children and adults.

In fact, as a kid, I was obsessed with Pokémon cards. I enjoyed opening new packs, collecting cards, and trading with my friends. And, I know I’m not alone. So many people have enjoyed Pokémon cards over the years as well.

As the value of certain cards continues to rise, finding the best places to sell your collection of Pokémon cards is more important than ever.

Whether you’re looking to make some extra cash, simply downsize your Pokémon card collection, or if you are decluttering everything you own and find a long lost box of childhood mementos, knowing where and how to sell your Pokémon cards can be important to make the most money.

In this article, I’ll discuss some of the best places to sell Pokémon cards online and locally and provide tips on how to price and present your cards in the best way.

Quick Summary

Identify and evaluate the value of your Pokémon cards before selling. Some cards are worth way more than others. For example, one card may be worth $0.10, and another may be worth over $100,000.

Look at your different selling options to see how you can get the most money.

Learn effective selling tips and strategies for presenting your cards to potential buyers.

How To Sell Pokemon Cards

Selling your Pokémon cards can be an exciting and profitable way to make money, especially if you have rare, holographic, or near-mint-condition cards in your collection.

To help you make the most profit, follow these tips to find the best places to sell your Pokémon cards. Before starting your Pokémon cards selling journey, it’s important to know your cards’ condition, rarity, and type.

Related: How I Made $40,000 In One Year Selling Items

Near-mint cards with no creases, scuffs, or whitening edges tend to have a higher value. Also, rare and holographic cards, like the famous Charizard, are highly wanted by fans, collectors, and trading card game enthusiasts, making them valuable in the Pokémon card market.

To figure out how rare your Pokémon card is, look for the symbols in the bottom right corner of your card and if you have a lot of cards, then you should become familiar with the Pokémon card rarity indicators, as well as the different sets and booster packs in which your cards were released.

For more accurate valuations, you may even look for professional grading services, such as Professional Sports Authenticator (PSA). They evaluate and grade cards based on their condition, ensuring buyers of their authenticity and quality.

If you’re selling Pokémon cards online, make sure to take clear, high-quality pictures that showcase your cards’ condition, as this will give potential buyers a better idea of what they’re purchasing.

By following these tips and tricks, you’ll be prepared to sell your Pokémon cards and get the most amount of money.

Best Places To Sell Pokemon Cards Online

There are many ways to sell Pokémon cards online. Here are some Pokémon selling sites to start with:

1. eBay

eBay is one of the most popular marketplaces for selling Pokémon cards due to its large reach of customers around the world.

I did a quick search on eBay and there are currently over 160,000 Pokémon cards for sale – so they definitely have a huge market!

You can choose to sell your cards through auctions or fixed price listings. When selling on eBay, be mindful of the seller fees and PayPal fees that will be deducted from your earnings. Shipping will also be another cost.

eBay is especially good for selling valuable cards, such as holographic cards or rare Charizard cards. To reach a wider audience and increase the chances of a successful sale, make sure you write detailed descriptions and add high-quality photos of your cards so that people are more likely to click on your listing.

2. Troll and Toad

Troll and Toad is an online store that specializes in collectible card games, such as selling Pokémon cards and they have been around for over 25 years.

They offer a buy list where you can sell your cards for cash or store credit. To sell on Troll and Toad, simply use their search bar to find the cards you want to sell, add them to your cart, checkout, and then ship your cards to them.

This is a great feature of Troll and Toad – the fact that you can see the exact cards they will accept and the exact amount that they will pay you for each Pokémon card. As you will learn below, many of the Pokémon card selling websites have this same feature, which is so helpful!

After you complete the list of cards that you plan on selling to them, you will print out an invoice that they give you, and then choose a payment method. Then, you will ship your box of Pokémon cards to them. Once they receive the package, they will verify the cards that you have sent to make sure they are in the correct condition as you stated. After that, they will pay you.

Troll and Toad also accepts Pokémon cards in bulk.

Keep in mind that they may be selective about the cards they accept, so it’s important to research and determine the value of your cards beforehand.

3. Mercari

Mercari is a site where you can quickly set up an account and start selling your used items, such as Pokémon cards. This site is not dedicated to just Pokémon cards, but they do have many listed and it is an easy option for Pokémon collectors.

There are well over 1,000 Pokémon cards listed on Mercari.

It’s important to create persuasive listings with photos and a relevant, detailed description, and include relevant keywords related to Pokémon cards. (Remember, they don’t just sell Pokémon cards, they also sell clothes and other items, so keywords are important!). Also, Mercari takes a minimum 10% fee from each sale you make on their platform.

4. TCGplayer

TCGplayer is a popular site with card game collectors in the U.S. and Europe.

People love selling on this site because they say it’s easy to use and they have great customer service.

To sell Pokémon cards on TCGplayer, simply list your cards on the TCGplayer marketplace, set your prices, and wait for potential buyers to purchase them. The marketplace handles the transactions, making the selling process easy.

Note: You will have to pay a commission fee of around 12–13% for each sale you make on TCGplayer, and you might also have shipping costs.

Here’s a quick guide on how to sell Pokémon cards on TCGplayer:

Create a seller account – You will need an account to get started selling Pokémon cards.

Set up your inventory – Once your seller account is created, you can start listing your Pokémon cards for sale. Enter details like the card’s name, set, condition, and quantity available.

Pricing your cards – Decide on the prices for your Pokémon cards. You can either manually set the prices or use TCGplayer’s automated pricing tool to match the market rates. TCGplayer has a pricing algorithm to help sellers be competitive and adjust prices based on the market demand.

Shipping options – Decide on the shipping options you will have for buyers.

Receiving payments – TCGplayer usually collects payments from buyers, processes the orders, and then deposits the money into your seller account. From there, you can withdraw your funds.

Maintain your inventory – Keep your inventory up to date. Remove sold items and add new ones to reflect the current availability of your Pokémon cards.

5. Card Cavern

Card Cavern is an online store that specializes in buying and selling Pokémon cards.

They have a straightforward buylist system where you can quickly find the cards they’re interested in and the prices they’re willing to pay.

Then, you ship your cards to them (they recommend purchasing tracking and insurance).

If you choose to sell your cards to Card Cavern, you’ll receive payment through PayPal or receive store credit, depending on your preference.

Their buy rates only apply to near-mint, English, tournament legal cards. You can send as many or as little Pokémon cards as you want to Card Cavern.

6. Dave & Adam’s

Dave & Adam’s is an online store for trading cards, including Pokémon cards, and it has been around for over 30 years.

They offer a buy list where you can see which cards they’re currently interested in purchasing. If your cards match their buy list, you can submit a sell request, ship your cards to them, and receive payment via check, PayPal, or store credit.

If you have a big collection, they will even travel to you.

7. Pokémon Facebook Groups

Pokémon Facebook Groups are communities of Pokémon card collectors and enthusiasts who use the platform to buy, sell, and trade cards. Pokémon Facebook Groups are exactly what you think – Facebook groups for Pokémon card collectors.

This can be a great place to sell your Pokémon cards because these groups are filled with people who are very interested in buying Pokémon cards.

These groups allow you to talk directly with fellow collectors and cater to various interests, such as specific regions, sets, or rarity levels.

To sell your Pokémon cards in these groups, make sure you follow group rules, post clear photos, and respond quickly to potential buyers’ inquiries.

8. CCG Castle

CCG Castle is a website that specializes in games since 2007.

They buy Pokémon cards that you no longer need and have a buy list on their site that will tell you exactly what they are accepting and how much they will pay you for it. They pay in either PayPal cash or store credit.

Best Places To Sell Pokemon Cards Near Me

If you’re looking to sell your collection or particular Pokémon cards, there are several options near you to consider. This section will cover the best local places where you can sell your cards, such as Facebook Marketplace, comic book stores, pawn shops, and Craigslist.

9. Facebook Marketplace

A popular and easy way to sell your Pokémon cards is through Facebook Marketplace. Nearly everyone has a Facebook account, so it can be easy for you to get started, and it allows you to connect with local buyers who might be interested in your cards.

Posting on Facebook Marketplace is simple, and you can include photos, descriptions, and set your price. Also, you can communicate with potential buyers through Facebook Messenger, making it easy to negotiate and set up a meeting location.

There are no listing fees when selling on Facebook Marketplace, which means that you get to keep everything you earn. But, you do have to handle everything yourself.

10. Local comic book stores

Comic book stores, particularly those that specialize in trading cards, card games, and board games, can be a great place to sell your collection.

Many local comic shops are interested in buying Pokémon cards to stock their inventory for other gamers and collectors.

You can visit stores in your local area, ask if they purchase Pokémon cards, and provide the store owner with a list or photos of your cards. They may make an offer on the spot or ask you to come back later. Remember, each comic store is different, so it’s a good idea to try a few stores near you to compare offers and don’t stop at just one.

11. Pawn shops

Another option to consider is pawn shops.

Pawn stores are known for buying various items, including sports cards and collectibles like Pokémon cards. Take your cards to a few pawn shops near you and see if they’re interested in buying your collection.

Keep in mind that pawn shops usually offer lower prices than other options (this is because selling Pokémon cards is not their sole business), but they can be a quick and convenient way to sell more popular cards.

12. Craigslist

Craigslist is a site for buying and selling various items locally – I’m sure you’ve heard of it. You can create a detailed listing for your Pokémon cards, including pictures, descriptions, and asking prices.

Interested buyers in your area can contact you, allowing you to arrange a meetup in a safe and convenient location.

Craigslist is usually a little more difficult to sell Pokémon cards on and that is because this site does not specialize solely in Pokémon cards and is very localized.

Where to Sell Pokemon Cards in Bulk

Selling your Pokémon cards in bulk may be something that you are interested in if you simply don’t have the time to look each one up.

When selling your Pokémon cards in bulk, it’s important to find the right platform. In this section, we’ll focus on three popular options: Full Grip Games, Safari Zone, and Sell2BBNovelties. With their unique offerings and easy-to-sell process, these companies can help you get the most value for your collection if you simply don’t have the time or have too many cards to sort through.

13. Full Grip Games

Full Grip Games is a local game shop in Ohio that buys bulk Pokémon cards online and in person.

At Full Grip Games, they make it easy for you to sell your bulk cards in increments of 100 or 1,000. Also, they accept rares and other card types as well. To make things simpler for you, their website has a bulk buy list that breaks down all the packs and cards they accept along with individual prices.

To get started, follow these easy steps:

Click on the “Buylist Instructions” link on their website.

Choose their full singles buylist or their bulk buylist.

Select the cards in your collection according to the buylist.

Review the pricing and total value of the cards submitted.

Once done, send the cards following their shipping instructions.

Once they receive your bulk cards, it will take them around one week to go through them. For the cards they accept, you can get paid via PayPal, store credit (you will get a 30% bonus if you choose the store credit option), or check via USPS mail.

14. Safari Zone

Safari Zone is another great option to consider for selling your Pokémon cards in bulk. They accept a wide range of cards, but they do need to be in near-mint condition.

Here’s what you should do to sell your cards on Safari Zone:

Create an account on the Safari Zone website.

Review the cards they purchase on their buy list.

Enter the card details.

After submitting the card information, you’ll receive a quote for your collection.

Ship your cards to Safari Zone, and they will process your payment after validating the cards.

Safari Zone only pays via store credit.

15. Sell2BBNovelties

Sell2BBNovelties is a website that has been around since 1999 that specializes in toys and collectibles, such as Pokémon cards.

They have an easy platform to sell your Pokémon cards in bulk and accept various card types, including rares, holographic, and common/uncommon cards.

To sell your Pokémon cards on Sell2BBNovelties, simply:

Go to their website and click on the “Buying Prices” tab.

Select the cards you’re selling according to their buying list.

When you’re ready, submit the form. You’ll receive a confirmation email with the total value of the cards and further instructions.

Ship your cards to Sell2BBNovelties, and they will process your payment upon receiving and verifying your cards.

You can receive payment for the cards they accept in either PayPal cash or store credit.

How to Make a Website to Sell Pokemon Cards

If you have the time and a lot of cards, you may even be interested in starting a website to sell your Pokémon cards.

Creating a website to sell your Pokémon cards is a great idea to reach a wider audience and have lower fees. Of course, there will be more work in this because you will be managing everything yourself.

Choose a platform and create your design – Look for an easy-to-use platform to build your website – my favorite is WordPress. You will want to pick a clean looking design that customers can look at on both computer and phone. Most platforms have a variety of premade themes that you can use. You can also personalize your website by adding your logo, choosing colors that represent your brand, and adding images.

Organize your products – Categorize your Pokémon cards by sets, rarity, or other criteria that make sense for your target audience. Clear product descriptions and high-quality images of each card will help potential buyers too.

Set up payment and shipping – Choose a payment gateway to securely process transactions. Options like PayPal, Stripe, or Square are widely used and reliable. Choose shipping options and rates based on your preferred carriers and shipping destinations.

Create valuable content – In addition to listing your Pokémon cards, consider creating helpful content such as blog posts or videos that add value to your website and attract more readers and buyers. Providing informative content will establish you as an expert in the field and help drive traffic to your site.

Promote your website – Use social media, search engine optimization (SEO), or even paid advertising to increase page views to your website.

Related: How To Start A Website Free Course

Pokemon Card Selling Tips and Strategies

Selling your Pokémon cards can be an exciting way to make extra money, but it’s important to have a little strategy so that you can make the most money and find the most buyers.

Here are some tips for selling your Pokémon cards successfully.

Determine the value of your cards. You should research how rare the card is, the origin, and the condition of your cards, as these factors will affect their worth. Keep an eye out for rare and valuable cards (such as first edition cards and illustrations), as these will attract more interest from collectors. Grading your cards can help with this process – professional grading services can rate the condition of your cards and encapsulate them in a case, increasing their value.

Consider where to sell your cards.There are numerous platforms for selling Pokémon cards online, such as eBay, where you can list your cards as single items or in an auction format. There are also more specialized Pokémon selling websites which are dedicated to trading cards. These sites often have dedicated communities of potential buyers who are very interested in Pokémon cards.

Write clear and accurate descriptions of your cards.You should always be clear and honest about your card’s condition. For example, are there any scratches or bends? Is there a tear or water damage?

Ship your cards carefully.Carefully package your Pokémon cards to protect your cards from damage during transit. You will want to keep your cards waterproof and not use rubber bands (rubber bands can damage the cards). Also, consider offering a tracking number and insurance to your buyer as an additional layer of security. Many of the Pokémon selling sites above have a very exact way they want you to ship the cards to them to prevent any damage, so be sure to see what their rules are.

By following these Pokémon card selling tips and tricks, you can increase the chances of finding the best places to sell your Pokémon cards.

Frequently Asked Questions

Here are answers to common questions about selling Pokémon cards.

How do I know if my Pokemon cards are worth money?

So, how do you know if the Pokémon cards that you have are worth anything? Many people have Pokémon cards, probably stuffed in a box somewhere, or maybe you came across some.

Whatever your reason is, yes, your Pokémon cards may be worth something.

Knowing the value of your Pokémon cards is important before selling, and there are a few key things to think about.

First, look at the rarity symbols on your cards: a circle indicates a common card, a square represents an uncommon card, and a star denotes a rare card. These symbols help you determine the rarity of your cards and their potential worth.

The condition of your cards also plays a big role in their value. Cards in mint condition, meaning they have no visible wear or damage, are worth more than cards with minor imperfections. Holographic cards, especially in mint condition, can be more valuable.

To take it a step further, you could even get your Pokémon cards professionally valued and graded by a reputable company like PSA. Grading involves a professional inspection of your card’s condition, assigning a numerical grade based on factors such as centering, corners, edges, and surface. The higher the graded number, the better the condition and, often, the higher the value.

Keep in mind that while Pokémon cards typically have higher values, other trading card games like Yu-Gi-Oh can also be valuable. Make sure to research the prices of similar cards sold recently, and compare the condition of your cards to decide if they’re worth selling.

How do I sell Pokemon cards for cash?

To sell your Pokémon cards for cash, first organize your cards by set and look for rare ones to see what you have. Once you’ve prepared your collection, follow the selling instructions on your chosen platform.

You can sell your Pokémon cards online, locally near you, and even in bulk.

Where can I find buyers for my Pokemon cards?

You can find buyers for your Pokémon cards on online marketplaces, local card shops, and social media groups. Websites like eBay and TCGplayer are popular places for selling Pokémon cards, as well as community forums and local collector’s events.

What are some reputable websites to sell Pokemon cards?

There are many reputable sites to sell Pokémon cards as we discussed above, such as:

eBay

Troll and Toad

Mercari

TCGplayer

Card Cavern

Dave & Adam’s

Pokémon Facebook Groups

Full Grip Games

Safari Zone

Sell2BBNovelties

Where is the best place to sell Pokemon cards?

The best place to sell your Pokémon cards depends on your preferences. eBay gives you a worldwide market and you are probably already familiar with their platform.

TCGplayer and Troll and Toad specialize in trading card sales and have a lot of Pokémon cards for sale.

Pokémon Facebook Groups are a great way to connect with those interested in Pokémon cards, and there are no listing fees – but you would be dealing with people on your own and handling everything yourself.

Are there any local stores that buy Pokemon cards?

Some local stores, like comic book shops, game stores, and pawn shops, may buy Pokémon cards. You can call local stores to see if they buy cards before bringing your collection in person.

Can you sell Pokemon cards on Etsy?

Etsy is generally geared towards handmade and vintage items, so it’s not an ideal platform for selling Pokémon cards. It’s best to stick with platforms like eBay, TCGplayer, or Troll and Toad for selling trading cards.

I did a search for Pokémon cards on Etsy and it said there were 43,326 results, but I think many of these are for custom art, in that they would be turning a picture of you or your pet into a Pokémon card. So, not the same thing.

Can I sell Pokemon cards on eBay?

Yes, you can sell Pokémon cards on eBay. It is one of the most popular sites for selling Pokémon cards and it gives you control over pricing and listing options.

Can you sell Pokemon cards at GameStop?

GameStop typically does not buy or sell individual Pokémon cards.

Do pawn shops buy Pokemon cards?

Some pawn shops may buy Pokémon cards, especially if they are valuable or rare. Call your local pawn shops or visit them in person to inquire about their interest in buying Pokémon cards. Remember, they do not specialize in Pokémon cards and have a smaller market, so you may not get as much for your Pokémon cards at a pawn store.

What does TCG and CCG mean?

As you’re going through the sites above looking for one of the best places to sell your Pokémon cards, you may come across these two terms. CCG means collectible card game and TCG means trading card game.

How can I determine the value of my Pokemon cards?

Figuring out the value of your Pokémon cards involves considering factors like:

rarity

condition

age

Websites like TCGplayer and Troll and Toad provide price guides and historical sales information to help you estimate the value of your cards.

How do I check the value of my Pokemon cards?

Check the value of your Pokémon cards by researching on websites like TCGplayer, eBay, and Pokémon Price. These platforms can give you a good idea of the current market value for individual cards.

Do you need a license to sell Pokemon cards?

You generally do not need a license to sell Pokémon cards, unless you’re planning to sell them by opening an in-person store. Check your local regulations to make sure you’re following any required guidelines.

How much is Charizard Pokemon card worth?

Charizard cards vary widely in value and can be worth anywhere from $25 to over $50,000. The Charizard Pokémon card that is worth the most is typically a mint condition 1st Edition from the base set.

What Pokemon cards are worth more than $100?

Some Pokémon cards worth more than $100 include rare Pokémon cards, such as first edition holographic cards from the original sets, high-grade cards, misprints, and promotional cards like the Pokémon Illustrator card.

What is the most expensive Pokemon card?

The most expensive Pokémon card varies over time; some examples include the Pokémon Illustrator card, the 1st Edition Charizard, or unique, one-of-a-kind promo cards handed out during official Pokémon events. The rarest Pokémon cards obviously cost more money and sell for more.

According to TCGplayer, the most expensive Pokémon cards include:

Pokémon World Championships No. 2 Trainer Promo

No. 2 Trainer Toshiyuki Yamaguchi (2000)

Neo Genesis 1st Edition Lugia (2000)

Super Secret Battle No. 1 Trainer (1999)

Family Event Trophy Kangaskhan (1998)

Test Print Blastoise Gold Border (1998)

Tsunekazu Ishihara Signed Promo (2017)

Trophy Pikachu No. 3 Trainer Bronze (1997)

Commissioned Presentation Blastoise Galaxy Star Holo (1998)

First Edition Shadowless Holographic Charizard #4 (1999)

Illustrator Pikachu (1998)

These were all sold for over $100,000 each.

Best Places To Sell Pokemon Cards – Summary

I hope you enjoyed this article on the best places to sell Pokémon cards and how to sell Pokémon cards for cash.

If you have Pokémon cards that you no longer want, there are many ways you can sell them. And, they may be worth a lot of money!

To figure out the value of the Pokémon cards that you want to sell, you’ll want to look at their rarity symbols, Pokémon card condition, grading (if applicable), and market comparisons. Understanding these factors will help you decide if your cards are worth selling and where to find the best prices.

Once your cards are sorted and evaluated, it’s now time to choose the best places to sell your Pokémon cards. Here are some popular options:

eBay – This site has millions of Pokémon cards sold every year. It’s a great place to find a worldwide audience, but remember to factor in shipping costs and eBay fees.

Facebook Marketplace and Pokémon Facebook Groups – Connect with local collectors or fans without worrying about shipping fees. This option may mean that you will meet the buyer in person.

Local comic shops – These stores can be an easy place to sell your cards, especially if they specialize in Pokémon cards or trading card games.

TCGplayer – Catering specifically to trading card game fans, this site has a dedicated space for buying and selling Pokémon cards.

Other options include Troll and Toad, Card Cavern, Dave & Adam’s, Sell2BBNovelties, pawn shops, and more.

Good luck selling your Pokémon cards!

What do you think is the best place to sell Pokemon cards for cash?

American Express has changed the terms on Delta personal cards to exclude getting the sign up bonus across the Delta family of cards. The previous terms stated:

Welcome offer not available to applicants who have or have had this or previous versions of this Card. We may also consider the number of American Express Cards you have opened and closed as well as other factors in making a decision on your welcome offer eligibility.

The new terms differ based on the card you’re apply for:

Delta gold:

You may not be eligible to receive a welcome offer if you have or have had this Card the Delta SkyMiles® Platinum American Express Card, the Delta SkyMiles® Reserve American Express Card or previous versions of these Cards.

Delta Platinum:

You may not be eligible to receive a welcome offer if you have or have had this Card, the Delta SkyMiles® Reserve American Express Card or previous versions of these Cards.

Delta Reserve:

You may not be eligible to receive a welcome offer if you have or have had this Card or previous versions of this Card.

Basically gold has the most restrictive terms and Reserve has the same terms as before. It’ll be interesting to see if similar language gets added to the business cards or if they will remain the same. Seems like the play is to get the gold card first, then platinum, then reserve and that way you can still hit all three bonuses without issue.

Cybersecurity, Warehouse, Accounting, Marketing Tools; New Broker Products; CFPB Co-Marketing Case

<meta name="smartbanner:author" content="We now have a native iPhone and Android app. Download the NEW APP”>

This website requires Javascrip to run properly.

Cybersecurity, Warehouse, Accounting, Marketing Tools; New Broker Products; CFPB Co-Marketing Case

By: Rob Chrisman

Fri, Sep 15 2023, 8:34 AM

“Happy” 15-year anniversary of Lehman Brothers going belly up. “I was struggling to understand how lightning works and then it struck me.” One of the conversation topics here at the NAMMBA event in Orlando is how Florida has its share of estimated lightning strikes every year. (As does the rest of the nation: here’s a link to an interesting real-time map.) Another topic is Florida’s Senate Bill 264 which prohibits the direct or indirect ownership of specific categories of real estate by “foreign principals” from a foreign “country of concern,” defined as the People’s Republic of China, the Russian Federation, the Islamic Republic of Iran, the Democratic People’s Republic of Korea, the Republic of Cuba, the Venezuelan regime of Nicolás Maduro, or the Syrian Arab Republic… The Statute prohibits the acquisition of (1) any interest in agricultural land by a foreign principal, (2) any interest in real property located near a military installation or critical infrastructure by a foreign principal, and (3) any real estate interest by a foreign principal of the People’s Republic of China, subject to very limited exceptions. There are challenges, of course. (Today’s podcast can be found here and this week’s is sponsored by SimpleNexus, an nCino Company, and award-winning developer of mortgage technology for modern lenders. Hear an interview with Simple Nexus’ Lori Brewer on areas in the mortgage space that technology and innovation will impact most.)

Lender and Broker Software, Products, and Services

“Our latest blog, ‘FEMA, Floods, Fires, and Funding, Oh no!’, highlights the early impact of this year’s hurricane season, blustered by Idalia’s trail of destruction and fanned by the Maui fires. This year packs a bigger punch as FEMA, the primary lifeline for relief, faces serious funding concerns that have led to restrictions on access to assistance. Where does this leave homeowners and servicers who face more disasters before yearend? Servicers, it’s time to evaluate your workflow automation, ensuring distressed borrowers have immediate access to relief and that your operations are streamlined accordingly. CLARIFIRE® delivers the speed, accuracy, and results that servicers need to succeed in the face of the volumes and complexities of all the parties involved. Arm your servicing team when disaster strikes with CLARIFIRE, delivering better results, better software, and BRIGHTER AUTOMATION®.

It used to be that our postal mailboxes were stuffed with all kinds of marketing materials. It still happens today of course, but mostly in our online mailboxes instead. But one thing has stayed the same: marketing still needs a special spark to stand out in a crowd, and that’s why utilizing a far less crowded medium might now be the “old-is-new-again” way to reach your prospects. Not to mention, it’s also one of the best ways for mortgage professionals to make a lasting impression on homebuyers during the holidays! Connect with the ICE team to learn how easy it can be to start with Surefire℠ CRM and Mortgage Marketing Engine.

More than ever, mortgage brokers and correspondents need a lending partnership that empowers them to exceed client expectations with elite service, speed, and simplicity. Rocket Pro TPO’s technology team delivered Pathfinder, the most powerful technology ever for brokers, created in partnership with Google. Combining multimillion-dollar AI and machine learning tech, it’s a first-of-its-kind centralized platform, right at your fingertips, 24/7/365. Also, their partners outpace the competition by leveraging Rocket Connect portal technology which connects brokers to the right team right away, including operations leaders for any question or escalation need. Their industry-leading Pricing Calculator quickly produces loan options to share with clients using Clear Quote, an easy-to-download PDF. To learn more, watch EVP, Mike Fawaz discuss more details. Interested in learning more about a Broker or Non-Delegated Correspondent partnership? Contact Rocket Pro TPO.

In challenging down economic times, Loan Vision is your solution to maximizing profitability and reducing costs in your business. With Loan Vision, companies see improvements of 25 to 35 percent decrease in days to close the books, 20 percent reduction in accounting headcount, complete LOS to G/L automation, and improved reporting and visibility that allow for better business decisions. Don’t accept a competitive disadvantage or get caught flat footed in a recovering market. To improve your cash position, gain a competitive edge, and prepare your business for sustained growth, contact Carl Wooloff to schedule a call today.

“Mortgage Industry Veterans Announce Fund It, New Startup Venture to Automate Warehouse Lending. Fund It is redefining how the mortgage industry manages its warehouse banking processes. Most IMBs still handle their warehouse funding manually. The Fund It platform, built with AI-powered algorithms, provides an automated warehouse lending solution. View capital needs projections in the next 30 to 60 days, eliminate human data errors, and access robust reporting tools that drive data-driven decisions. It also seamlessly integrates with many popular mortgage tools that IMBs currently use. Fund It’s platform tracks fundings, collateral administrations, and loan purchases. It also pinpoints cost leakages. These features help IMBs save time and increase profit on every warehouse-funded mortgage loan. FundIT optimizes every element of an IMB’s warehouse lending process. Use Fund It to enjoy higher profits by automating a traditionally manual-heavy process. Visit our website to learn more how to manage your company’s warehouse funding operations.”

Click links, ask questions later. The most common attack vector for a cyberattack is the human element. It’s what phishing emails, phone calls and text messages all have in common. Yet while it’s the weakest link, the human element could be your organization’s greatest prevention layer if trained correctly. In an industry that incentivizes people based on sales goals, every mortgage lead has bottom line potential. And in the current market, it’s only human to go after leads without stopping to consider their legitimacy. But recent data shows just how risky clicking without thinking can be. According to ISACA, in 2022 social engineering (tricking humans) was the #1 attack vector, and even the best teams are vulnerable. Learn how to do a better job at testing and training your team to identify legitimate leads. Talk to Richey May’s cybersecurity experts for help assessing and defining your cybersecurity training needs.

The CFPB and Co-marketing

Ken Perry with the Knowledge COOP writes, “The Freedom mortgage case should capture the attention of every mortgage broker, lender, and real estate agent. This is the biggest statement the CFPB has made about their feelings on co-marketing in a long time! The fact that they targeted a mortgage company providing free open house flyers, and free access to a subscription they pay for is huge because these arrangements exist in so many mortgage companies, including wholesale lenders, and rarely does the referring entity have to pay for these things. This is truly a case of, ‘if everybody is doing it then is it even wrong?’ Well, it looks like the CFPB has answered that question. Now we wait and see if $1.75 million was enough of a deterrent to force people to look at their business practices and make some immediate changes. These settlements usually come in groups. I can’t help but wonder if we will see more soon…”

Capital Markets

Much like the Consumer Price Index on Wednesday, the Producer Price Index report for August came in above expectations yesterday (0.7 percent versus consensus 0.4 percent). Other data on the day also included better than expected August Retail Sales (0.6 percent month-over-month, largely due to gasoline stations), and a smaller than expected increase in weekly jobless claims. Low jobless claims reflect a fairly tight labor market, which helps to explain why consumer spending continues to hold up in the face of inflation pressures and rising rates.

On the central bank front, the European Central Bank raised interest rates for the 10th consecutive time, to 4 percent, as President Lagarde signaled a shift that could mean the peak has been reached, though she insisted that she can’t yet say if that’s the case. As far as our Fed, there is zero likelihood the central bank is going to signal they’re done hiking rates at the conclusion of the FOMC meeting next week.

Despite all the major events over the past couple days that have influenced bonds, including the beginning of an auto worker’s strike last night, today’s calendar also has some market moving potential. We’ve already received Empire manufacturing, import prices (-3.0 percent, ex-gas flat), and export prices (-5.5 percent from the prior year). Later this morning brings August industrial production and capacity utilization, and preliminary September Michigan sentiment that includes inflation expectations. We begin the day with Agency MBS prices worse .125 from Thursday evening, and the 10-year yielding 4.32 after closing yesterday at 4.29 percent; the 2-year is up to 5.03.

Employment

Crescent Mortgage Company, a subsidiary of United Bank, named “Most Trusted Bank in America” for 2023 by Newsweek, is celebrating its 30th anniversary and rapidly expanding its retail division in the southeast. We welcome ambitious Loan Originators seeking growth and unparalleled support. Seasoned veteran David Rapson, CMB serves as SVP – Retail Lending, guiding us to new heights. President and CEO Fowler Williams, CMB emphasizes our unique commitment to allowing originators to do what they do best, originate loans, we will handle the rest! Backed by advanced technology and curated product offerings including agency, 1X close construction or renovation, low down payment options, non-QM, as well as unique portfolio offerings, Crescent has built a platform for Loan Officer success, a platform for you. Join our journey. Experienced Loan Originators or Branch Managers, explore possibilities by contacting David Rapson to elevate your success. The future is bright at Crescent Mortgage.

Supreme Lending is pleased to announce Rachel Saylor Brown as its newest Producing Tampa Bay Area Manager. Leveraging 10 years of remarkable industry experience, Brown will steer Supreme’s Florida expansion strategy, together with her husband Chris Brown, and a best-in-class team: Kaitlin Schiro, Nancy Myrick and Anna Livingston, all seasoned mortgage professionals. Rachel and her team are known for providing exceptional client experiences through transparent communication, meaningful relationships, and industry-leading technology. Supreme Lending is thrilled to welcome her to the team!

“Revolutionize Your Leadership: Meet Your Visionary Executive! Are you on the hunt for a C-suite dynamo to steer your organization to new heights? Look no further! I am a strategic powerhouse primed to tackle the role of President, CEO, COO/CSO. With a proven track record in strategy, team building, P&L mastery, and agile execution, I’m all about results, not magic. My extensive network includes GSE’s, investors, regulators, vendors, PE sources, and compliance experts. My experience spans Mortgage, Insurance, Tech and more. I don’t just lead; I innovate. I seamlessly integrate tech into strategy diversifying revenue streams while boosting traditional sales. Fintech? Consider it a bonus. Comfortable with boards and stakeholders, I’m a goal-driven, creative problem solver and an adept communicator. West Coast-based, but I’m open to relocation or remote work. Ready to transform your organization? Email Chrisman LLC’s Anjelica Nixt today for more details and a game-changing connection.

Download our mobile app to get alerts for Rob Chrisman’s Commentary.

Share via Social Media:

All social media shares will include the image and link to this page.

While some states offset the high cost of college with substantial financial aid programs, Rhode Island’s offerings are much more limited. In fact, it has one of the lowest rates of state grant aid per full-time undergraduate student; Rhode Island provides about $170 in funding per student, the seventh-lowest amount in the country, according to a 2022 College Board report.

To put that in perspective, consider that South Carolina — the state with the highest level of state grant aid — provided about $2,590 per student.

Though limited, there are still some state aid programs. Whether you have your heart set on attending Brown University, The University of Rhode Island or the Rhode Island School of Design, here are the available financial aid programs specific to Rhode Island.

The cost of education in Rhode Island

There are 13 public and private non-profit colleges and universities in Rhode Island.

Higher education in Rhode Island tends to be much more expensive than it is in other states. Even public universities and community colleges, which are typically lower-cost options, are costly.

Based on the average rates of tuition, fees and room and board for the 2020-2021 academic year, here’s how much you can expect to pay, according to data from the National Center for Education Statistics:

Public four-year school (in-state): $26,946 per year, about 26% more than the national average of $21,337.

Private four-year school: $61,692 per year, about 33% higher than the national average of $46,313.

Community college (in-state): $4,806 per year, about 37% higher than the national average of $3,501. (Community college costs don’t include room and board.)

Several factors are behind the high college costs. In addition to Rhode Island’s high cost of living and limited financial aid, it’s also home to several well-known private universities with hefty price tags that drive up average tuition rates. For example, a student’s estimated total cost for the 2023-2024 academic year at the Rhode Island School of Design is $81,810 — nearly double the national average for private schools.

Financial aid options in Rhode Island

Although public schools are more expensive in Rhode Island than in other states, attending a public university is still cheaper than private school — but only if you qualify for in-state tuition.

You qualify for in-state tuition if you meet one of the following criteria:

You attended an approved Rhode Island high school for at least three years.

You graduated from an approved Rhode Island high school.

You lived in the state for at least 12 months prior to enrollment.

Unlike some states, Rhode Island extends residency to undocumented students, including those with Deferred Action for Childhood Arrivals (DACA) status. As a result, undocumented and DACA students are eligible for in-state tuition and state aid in Rhode Island if they meet the other residency requirements.

Students may also have trouble finding funding opportunities in Rhode Island because its aid programs aren’t listed in one central location. Programs are usually provided through partnerships with other organizations, so they’re often listed on non-government websites that can be difficult to find if you don’t already know about them.

Although Rhode Island’s options are more limited than those of other states, you may be able to use one or more of the following programs to finance your education:

529 plans.

In-state tuition.

Scholarships.

Tuition waivers.

Student loans.

Other aid programs.

Student loan repayment assistance.

529 plans

Rhode Island doesn’t have a prepaid tuition plan, but families can use a CollegeBound Saver 529 account to save and invest for a child’s future education. The money can grow tax-deferred in a CollegeBound Saver account, and the withdrawals are tax-free as long as they’re used for qualifying education expenses. Beneficiaries may use the funds at any U.S.-accredited college; they aren’t limited to Rhode Island schools.

Rhode Island has a higher-than-usual maximum contribution limit; families can contribute to an account until its total market value reaches $520,000 per beneficiary.

The CollegeBound Saver 529 has two other benefits:

State income tax deduction: Rhode Island taxpayers who contribute to this account may qualify for a state income tax deduction. They can deduct up to $500 in contributions individually, or $1,000 if they are married and file a joint return.

Starter Bonus: If you have a newborn or recently adopted a child, Rhode Island will contribute $100 if you open a new CollegeBound Saver account and deposit at least $100.

In-state tuition

The average total cost of attendance for in-state students at Rhode Island public schools is less than half the average cost of attending a private school.

However, students who want to attend college outside of Rhode Island may qualify for the New England Board of Higher Education’s Tuition Break program. Students who are residents of member states — Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island and Vermont — can enroll in an eligible program at a public community college or university in another participating state at a reduced rate.

According to NEBHE , the average full-time student saves $8,600 per year with Tuition Break. Exact savings depend on the program and state. You can view the eligible programs and schools on the NEBHE website.

Rhode Island scholarships

Rhode Island offers just two state scholarship programs, both of which are awarded based on academic merit and financial need. The programs are typically very limited in scope and are only available to students at particular schools.

The two Rhode Island scholarship programs are:

Rhode Island Promise Scholarship Program

Through the Rhode Island Promise Scholarship Program, the state will cover up to the full cost of tuition and fees for qualifying students who attend the Community College of Rhode Island (CCRI) full-time for two years..

To qualify, students must be Rhode Island residents and enroll full-time at CCRI for the semester beginning immediately after their high school graduation.

Rhode Island College Hope Scholarship

The Rhode Island College Hope Scholarship is a state-funded award offered to eligible students at Rhode Island College (RIC). It is a last-dollar award, meaning it covers the student’s remaining tuition and fees after other grants and scholarships are applied.

To qualify, students must be Rhode Island residents and in their junior or senior years at RIC with a GPA of at least 2.5. Applicants must be on track to graduate or earn an approved certificate in a total of four years.