Mortgage tech firm Blend has launched a lower-cost version of its mortgage suite for retail independent mortgage banks, the company announced this week.

This offering, called Blend IMB Essentials, includes many of the same features of its standard offering for mortgage lenders.

Blend IMB Essentials will streamline the application process, will facilitate pulling soft credits instead of tri-merge credits during the initial phase of application. It will also serve loan officers on-the-go with a mobile application, Nima Ghamsari, C.E.O of Blend told HousingWire.

“The mortgage market is grappling with the effects of high interest rates, home affordability, and low inventory, so reducing costs is top of mind for everyone,” Ghamsari said in a prepared statement. “Retail IMBs have helped build Blend into what it is today and we stand by the industry during this time. We will make sure every loan officer can offer the best possible borrower experience while also being able to conveniently manage their pipeline on the go with the LO Mobile App.”

Additionally, Blend integrates with the most common loan origination systems, pricing engines, as well as other key systems.

Earlier in September, Blend added an assets-derived income capability to its existing “Blend Income” product. This enhancement gives lenders “additional ways to verify more income sources far earlier in the application process than traditionally feasible,” HousingWire reported.

On a day when mortgage rates are officially close to hitting 8%, I decided to write a post about why they might be a lot lower in 2024.

Call me a contrarian. Or an optimist. Or perhaps just an individual that is looking at data and drawing some conclusions.

While the trend for mortgage rates lately has undoubtedly been higher, higher, higher, we could be close to hitting a peak. I know, I’ve said that before…so much for the mortgage rate plunge.

But maybe we just need to cross that psychological 8% threshold before things can turnaround.

Sometimes you need to see/experience the worst before a recovery can take place.

Here Come the 8% Mortgage Rates…

The threat of 8% mortgage rates might last longer than the 8% mortgage rates themselves, assuming they actually materialize.

This isn’t a new threat. I wrote all the way back in September 2022 to watch out for 8% mortgage rates. At that time, we inched closer to those levels before rates pulled back.

More recently, Shark Tank’s Mr. Wonderful called for the same, arguing that the Fed wasn’t messing around when it came to its inflation fight.

And now it appears he might be right, with the 30-year fixed averaging 7.92%, at least by MND’s daily survey.

But despite higher and higher mortgage rates over the past month and a half, the Fed has become more and more dovish.

There have countless comments of late from Fed speakers essentially signaling a pause in rate hikes. Basically arguing that no further tightening is necessary.

That doesn’t mean 10-year bond yields can’t keep rising, nor does it mean mortgage rates can’t also increase.

While the Fed is saying one thing, everyone else is looking at the data, which continues to come in hotter than expected.

About 10 days ago, it was a big jobs report print, and today it was retail sales coming in much higher than forecast.

Per the Commerce Department, retail sales increased 0.7% in September, more than double the 0.3% Dow Jones estimate.

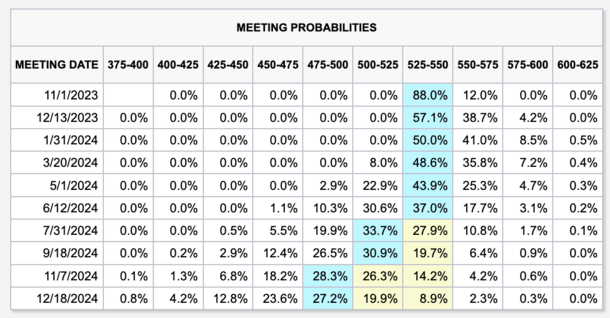

This has pushed the odds of another Fed rate hike up for the December meeting to near parity with a pause.

Per the CME FedWatch Tool, chances of a rate hike at the December 13th meeting are now at 41.9%. That’s up from 32.7% yesterday and 25% a week ago.

Should We Listen to the Fed or the Data?

It’s been a strange contrast lately, with the Fed becoming more dovish as hot data continues to come down the pipe.

But ultimately it appears as if the interest rate traders are more focused on the data than they are what Fed speakers have to say.

Even so, the odds remain ever so slightly in favor of a pause, which is good news for the time being.

Of course, those numbers can change quickly, as evidenced in the daily and weekly movement highlighted above.

And if consumers keep spending, despite economic headwinds and higher prices, it might be difficult to see the cooler economic reports the Fed wants.

However, the Fed may still stand pat at these levels and wait for conditions to deteriorate, as would be expected after 11 rate hikes.

Today, Richmond Fed President Thomas Barkin said the hot data “doesn’t match with his on-the-ground observations that demand seems to be slowing.”

So perhaps we just need more time to let the restrictive monetary policy do its thing. It’s not as if consumers immediately stop spending just because costs are higher.

People still need to buy things, especially gas, groceries, clothing, and other essentials.

And thanks to all the credit floating around, whether it’s 0% APR credits cards or buy now, pay later platforms, the party can continue for a lot longer.

The 10-Year Yield Is Forecast to Fall in 2024, Pushing Mortgage Rates Down with It

At last glance, the 10-year bond yield, which tracks 30-year fixed mortgage rates pretty well, was a sky-high 4.86%.

Meanwhile, the mortgage rate spread was over 300 basis points, when it’s typically closer to 170.

Combined, that means a yield of 5% would signal 8% mortgage rates. In normal times, it would translate to a rate of say 6.75%. But these are not normal times.

Mortgage rates keep rising and mortgage lenders continue to price defensively as the threat of more inflation and Fed rate hikes remains.

But maybe, just maybe, we are approaching the worst of it, as consumers teeter on the brink of a possible recession.

And perhaps 8% mortgage rates will signal a peak and possible turning point.

After all, the 10-year treasury yield is expected to fall to 3.41% by April 2024, per a September 27th note from Statista.

Meanwhile, Capital Economics market economist Hubert de Barochez predicts the 10-year yield will fall about 80 basis points by the end of the year thanks to slowing growth and the possibility of a mild recession.

De Barochez says this would allow the Fed to cut rates sooner, ideally leading to lower mortgage rates in the process.

Yes, such forecasts are subject to change (or can be completely wrong), but the general consensus is that we’ll be lower by mid-2024 or earlier. Just maybe not that low.

If we take a lower 10-year yield and sprinkle in a more traditional mortgage rate spread, say just 200 basis points, that puts mortgage rates back in the 6% range.

Mortgage rates in the 6s, or even high-5s if paying discount points at closing, would usher in some normalcy to the housing market.

If accompanied by a mild recession and some job losses, it could also mean slightly lower home prices as well, instead of a return to bidding wars.

And that could be good for the long-term health of the housing market, which is clearly broken right now.

Banking with an online-only financial institution can offer a lot of perks, like higher interest rates on deposit accounts, lower (or no) monthly fees, and even features like fee-free overdraft protection. But not every online bank is equal.

When you’re evaluating an online bank for a checking and savings account, it’s important to consider the features of the bank’s online platform and mobile app. Depending on your preferences, you may prioritize some features of mobile banking — like peer-to-peer transfers and mobile check deposit — over others.

Here, you’ll learn about some of the most important attributes to look for when investigating the features of online and mobile banking. This list can help you make the best choice for your own particular financial services needs.

Ready for a Better Banking Experience?

Open a SoFi Checking and Savings Account and start earning up to 4.50% APY on your cash!

The Benefits of Having a Good Banking Website and Mobile App

There are many pros of online and mobile banking, typically including a higher annual percentage yield (APY) on your savings, low or no monthly fees, easy ATM access, and sometimes no minimum balance requirement.

But a good online-only bank should also include features on its website platform and mobile app that offer security and convenience. Finding an online bank account with a safe, easy-to-use platform and app can add so much convenience into your everyday life. You’ve just got to know which features to look for.

Recommended: Online Banking vs. Traditional Banking

12 Must-Have Features of Online and Mobile Banking

So what are the top features of online banking to consider when looking for a new bank account? We’ve rounded up 12 must-have online bank features that you may want to prioritize:

1. Highly Rated Mobile App

Unless you spend a lot of time at a desk, you may be doing more of your banking on the go with your smartphone. That means you’ll likely want to find a bank that is renowned for its mobile app.

When shopping for a new bank account, it’s a good idea to compare interest rates and fees, but you can also head to the Apple App Store and Google Play to see how other consumers have rated the bank’s mobile app.

If a bank’s mobile app has consistently negative reviews, that could be a red flag.

2. Safety and Security Features

You may wonder, Is mobile banking safe? It’s worth making sure certain security features are in place. Just like traditional brick-and-mortar banks, online-only banks should offer FDIC insurance on your funds.

Whether you’re visiting an online or traditional bank’s website, you can always verify that it’s legitimate using the FDIC’s database, BankFind .

But beyond insuring the money in your account, a bank should also offer online and mobile banking safety features, like:

• Two-factor authentication, multi-factor authentication, or biometric authentication (like thumbprint or face ID)

• Fraud alerts via text, email, and mobile app

• Debit card freezes

• Credit score monitoring

• Automatic logout

Tip: Not sure what security features a bank has? You may be able to find a breakdown of all the security features a bank offers on its website.

3. Account Alerts

Fraud alerts aren’t the only valuable alerts you may want to prioritize when selecting an online bank. Such financial institutions typically offer a wide array of online banking alerts — sent via email, text, or even push notification — about different kinds of bank activity.

Banks may send alerts for:

• Low balances

• Direct deposits

• Unusual activity on your account

• New log-ins

• Large purchases

• Overdrafts

• Username and password changes

• Withdrawals

These and other alerts can make managing your finances easy — and get your attention if something goes wrong.

4. Account Activity, Balances, and Statements

Before the advent of online banking, many people tracked their bank activity using a physical register in their checkbook. They could then compare this against a paper statement they’d receive in the mail each month.

But now, you can eliminate all this manual work. Online banking typically features tools that allow consumers to log in to their account online or via the mobile app at any time to check recent activity, access e-statements, and review balances.

Recommended: Current Balance vs. Available Balance

5. Self-Service Options

If you’re interested in managing your account without having to talk to a live bank teller, you may want to find a bank that offers self-service options.

For example, with many online accounts, you can do a lot of things on your own online or in the app, including:

• Setting up direct deposit

• Setting up bill pay

• Resetting your debit card PIN

Being able to do these things without calling customer service or visiting a physical branch can add convenience and flexibility to everyday life.

6. Early Direct Deposit

Speaking of direct deposit, some online banks offer early access to your paycheck when you set up qualifying direct deposits. If you want to access your paycheck up to two days early, consider prioritizing a bank account with this unique online banking feature.

7. Mobile Check Deposit

Direct deposit isn’t the only deposit feature to consider. If you occasionally receive paper checks from friends, family, or even customers for your small business, you’ll need a way to deposit the checks without going to a physical branch.

Many online banks allow you to deposit a check wherever you may be, by using your mobile phone. Among the benefits of mobile check deposit: the ability to snap a photo of your endorsed check to deposit via the smartphone app. You can even do it from the couch.

8. Easy Transfers

Transferring money is an important part of the banking experience. When you open a new account, for instance, you may want to transfer money from one bank to another. You might also need to transfer funds between two accounts at the same bank.

If you anticipate regular transfers, it may be smart to prioritize a bank account that lets you initiate transfers easily online or in the mobile app. This can save you the hassle of visiting a physical branch or calling a bank teller to initiate a transfer.

Sometimes, you may want to transfer money to friends and family using your mobile device. This is called a peer-to-peer transfer (or person-to-person transfer, or P2P). Some mobile banking apps have their own P2P platforms, others may offer Zelle transfers in app, and others may simply allow you to connect your bank account, debit card, or credit card to popular P2P transfer apps like Venmo and Cash App.

Recommended: How to Pay Someone Instantly

9. ATM Finder

Because online-only banks don’t have any physical branches for consumers to visit, they generally offer an extensive network of ATMs that make it easy to withdraw cash on the go. If you regularly take out or deposit cash at an ATM, it’s a good idea to prioritize a bank with a large ATM network.

But you should also consider how easy it is to find nearby ATMs. Some mobile bank apps, for example, have ATM finders that can help you navigate to the closest fee-free ATM near you. This can be a real plus when you want to quickly get a check deposited.

10. Automatic Savings Tools

An online banking feature to consider is one that can help you build your savings account faster. You can usually opt into these automated savings features online or in the mobile app. Check for rounding-up functions and other ways to grow your wealth, little by little.

11. Online Bill Pay

One of the best features of online banking is how online bill pay works, though not every financial institution may offer this. If you occasionally forget to pay a bill, you may benefit from a bank that lets you set up this feature and want to make sure it’s available.

Paying your bills on time is a significant contributing factor to a solid credit score, so it’s worth your attention.

Recommended: Pros and Cons of Automatic Bill Payment

12. Great Customer Support

When you choose an online-only bank, you won’t be able to walk into a local branch and chat with a bank teller when you need help. Instead, you’ll connect with virtual assistants and live agents via chat (in-app or online), email, and phone.

If you think you may need help from time to time, it’s a good idea to review a bank’s customer service hours and read reviews of customer service interactions. An online bank with a stellar reputation for customer service could enhance your overall banking experience.

The Takeaway

For many, the appeal of online bank accounts continues to be the high APYs, low fees, and extensive ATM networks. But the unique features of online banking — like mobile check deposit, account alerts, peer-to-peer transfers, and online bill pay — make an even more compelling case for switching to online banking.

When you open an online bank account with SoFi, you’ll enjoy a hyper competitive APY and no account fees, which can help your money grow that much faster. Plus you’ll be able to spend and save in one convenient place with our Checking and Savings account.

Better banking is here with up to 4.50% APY on SoFi Checking and Savings.

FAQ

What are the features and benefits of online banking?

Online banks are known for offering high APYs on savings accounts, no monthly fees or minimum balance on checking accounts, and even cutting-edge features like fee-free overdraft, early paycheck access, mobile check deposit, and automatic savings tools. Each online bank account will vary, but it’s a good idea to prioritize one that offers these and other key features — and has a highly rated mobile app.

Is mobile banking safe?

For the most part, mobile banking is safe. Like a traditional bank account, an online bank account should be insured by the FDIC. Furthermore, a good online bank should offer a wide range of safety and security features, like multi-factor authentication, instant transaction alerts, and Secure Socket Layer (SSL) encryption to protect accounts and your personal information.

What are the pros and cons of online banks?

Because they have lower overhead costs, online-only banks can typically offer consumers higher interest rates, lower fees, and a superior mobile banking experience. They may have compelling features like automatic savings tools, fee-free overdraft, extensive ATM networks, and mobile check deposit.

However, these banks do not have in-person banking, may not always offer live assistance, and might have a more limited roster of banking services. Depending on the online bank, some consumers may find it more challenging to deposit cash.

Photo credit: iStock/Ridofranz

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with direct deposit activity can earn 4.50% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Direct Deposit means a deposit to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Direct Deposit”) via the Automated Clearing House (“ACH”) Network during a 30-day Evaluation Period (as defined below). Deposits that are not from an employer or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, do not constitute Direct Deposit activity. There is no minimum Direct Deposit amount required to qualify for the stated interest rate.

SoFi members with Qualifying Deposits can earn 4.50% APY on savings balances (including Vaults) and 0.50% APY on checking balances. Qualifying Deposits means one or more deposits that, in the aggregate, are equal to or greater than $5,000 to an account holder’s SoFi Checking and Savings account (“Qualifying Deposits”) during a 30-day Evaluation Period (as defined below). Qualifying Deposits only include those deposits from the following eligible sources: (i) ACH transfers, (ii) inbound wire transfers, (iii) peer-to-peer transfers (i.e., external transfers from PayPal, Venmo, etc. and internal peer-to-peer transfers from a SoFi account belonging to another account holder), (iv) check deposits, (v) instant funding to your SoFi Bank Debit Card, (vi) push payments to your SoFi Bank Debit Card, and (vii) cash deposits. Qualifying Deposits do not include: (i) transfers between an account holder’s Checking account, Savings account, and/or Vaults; (ii) interest payments; (iii) bonuses issued by SoFi Bank or its affiliates; or (iv) credits, reversals, and refunds from SoFi Bank, N.A. (“SoFi Bank”) or from a merchant.

SoFi Bank shall, in its sole discretion, assess each account holder’s Direct Deposit activity and Qualifying Deposits throughout each 30-Day Evaluation Period to determine the applicability of rates and may request additional documentation for verification of eligibility. The 30-Day Evaluation Period refers to the “Start Date” and “End Date” set forth on the APY Details page of your account, which comprises a period of 30 calendar days (the “30-Day Evaluation Period”). You can access the APY Details page at any time by logging into your SoFi account on the SoFi mobile app or SoFi website and selecting either (i) Banking > Savings > Current APY or (ii) Banking > Checking > Current APY. Upon receiving a Direct Deposit or $5,000 in Qualifying Deposits to your account, you will begin earning 4.50% APY on savings balances (including Vaults) and 0.50% on checking balances on or before the following calendar day. You will continue to earn these APYs for (i) the remainder of the current 30-Day Evaluation Period and through the end of the subsequent 30-Day Evaluation Period and (ii) any following 30-day Evaluation Periods during which SoFi Bank determines you to have Direct Deposit activity or $5,000 in Qualifying Deposits without interruption.

SoFi Bank reserves the right to grant a grace period to account holders following a change in Direct Deposit activity or Qualifying Deposits activity before adjusting rates. If SoFi Bank grants you a grace period, the dates for such grace period will be reflected on the APY Details page of your account. If SoFi Bank determines that you did not have Direct Deposit activity or $5,000 in Qualifying Deposits during the current 30-day Evaluation Period and, if applicable, the grace period, then you will begin earning the rates earned by account holders without either Direct Deposit or Qualifying Deposits until you have Direct Deposit activity or $5,000 in Qualifying Deposits in a subsequent 30-Day Evaluation Period. For the avoidance of doubt, an account holder with both Direct Deposit activity and Qualifying Deposits will earn the rates earned by account holders with Direct Deposit.

Members without either Direct Deposit activity or Qualifying Deposits, as determined by SoFi Bank, during a 30-Day Evaluation Period and, if applicable, the grace period, will earn 1.20% APY on savings balances (including Vaults) and 0.50% APY on checking balances.

Interest rates are variable and subject to change at any time. These rates are current as of 8/9/2023. There is no minimum balance requirement. Additional information can be found at http://www.sofi.com/legal/banking-rate-sheet..

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

The ultra-charming Santa Monica estate of late Emmy Award-winning SNL writer John Bowman is looking for a buyer to join the ranks of its famous owners.

A sprawling coastal estate with three separate structures and over half an acre of exquisite outdoor space, the property recently hit the market for $16,850,000 (Justin Alexander of The Alexander Group at Compass holds the listing).

Since 1995, the property has served as home to John Bowman and his wife, Shannon. Bowman, who passed away in 2022, was an accomplished TV showrunner, an Emmy Award-winning SNL writer, Martin series co-creator and producer who also led the WGA’s negotiating committee during the 2007-08 strike.

Photo credit: Engel Studios courtesy of Compass

A three-time Emmy nominee, Bowman is known for writing on In Living Color, co-creating the ’90 sitcom Martin, and for his countless writing credits, which include The Fresh Prince of Bel-Air, It’s Garry Shandling’s Show, Men Behaving Badly, The Hughleys, and Murphy Brown. He served as an executive producer on the latter three, as well as on Frank TV, Root of All Evil, Cedric the Entertainer Presents, The Show, and Princesses.

But he wasn’t the only famous resident of the Santa Monica estate.

John and Shannon bought the 1917-built home from singer/songwriter and Rock and Roll Hall of Famer, Jackson Browneand his then-partner, actress Daryl Hannah, who owned it back in the day.

But despite its roster of famous residents, the Santa Monica house is known as the Witbeck House — after its first owner, businessman Charles Witbeck. Witbeck commissioned the property, with Arts and Crafts architects Charles and Henry Greene delivering the East Coast-inspired shingle house that we see today.

Inside the celebrity-favorite Witbeck House in Santa Monica

Photo credit: Engel Studios courtesy of Compass

Set among over a half-acre of park-like grounds, this rare three-structure estate in the heart of Santa Monica boasts a five-bedroom main house with grand formal and gathering rooms and a hidden playroom, a detached two-story A-frame studio, and a detached two-bedroom guest house.

The East Coast shingle-style main house has four large bedrooms upstairs, including a stunning primary suite with soaring cathedral ceilings and a luxurious spa bath, an office, and a hidden playroom.

Downstairs we find another full bedroom with its own bathroom, as well as grand, formal gathering rooms — each featuring French doors that open into the backyard.

Photo credit: Engel Studios courtesy of CompassPhoto credit: Engel Studios courtesy of CompassPhoto credit: Engel Studios courtesy of CompassPhoto credit: Engel Studios courtesy of CompassPhoto credit: Engel Studios courtesy of CompassPhoto credit: Engel Studios courtesy of CompassPhoto credit: Engel Studios courtesy of CompassPhoto credit: Engel Studios courtesy of CompassPhoto credit: Engel Studios courtesy of Compass

Also on the property, a storybook A-frame cottage serves as a detached two-story studio, perfect for creators, musicians, writers, and innovators to carry on the legacy of the estate. An additional two-bedroom guest house with a kitchen and bath is also included.

The park-like grounds feature a custom patio firepit with an al-fresco dining deck, a resort-inspired swimming pool, an expansive grass lawn, a rose garden, and a private sports court. Adding an extra note of privacy, the property is surrounded by beautiful mature trees and extra tall hedges.

Photo credit: Engel Studios courtesy of CompassPhoto credit: Engel Studios courtesy of Compass

But despite the home’s many attributes, it’s the location that makes it all the more desirable.

The Palisades Ave property sits on one of the most sought-after streets in all of Santa Monica, just two blocks from the beach, and within reach of the best shops and restaurants on Montana, the Jonathan Club, and a short drive to LA’s premier Westside golf courses.

More stories

The wildly imaginative homes of our favorite movie directors

Inside Guillermo del Toro’s spine-chilling Bleak House: A treasure trove of horror memorabilia

George Lucas’ Skywalker Ranch is a fanboy paradise with Victorian roots

Editor’s Note: Due to major changes coming to the FAFSA, the form for the 2024-2025 academic year is delayed until December 2023. This article reflects the most recent information, but final details will not be available until the new FAFSA form is released.

Students who are enrolled at least half-time at an eligible school, are a U.S. citizen or eligible non-citizen, and meet other requirements can receive financial aid through the Free Application for Federal Student Aid (FAFSA®).

According to Education Data Initiative, the average cost for undergraduate students attending a four-year private nonprofit institution is $38,768 in tuition and fees per year. For students attending in-state public four year institutions, the average is $9,678 in tuition alone. Living on campus bumps these numbers up to $55,840 and $26,027 per year, respectively.

If you can’t afford to pay for this cost out-of pocket, understanding the FAFSA requirements can help you possibly fund this worthwhile expense.

What Is FAFSA?

The FAFSA is the official application form to request financial aid for higher education from the U.S. government. It determines whether undergraduate and graduate students are eligible to receive federal grants, work-study, and federal student loans. Federal aid can only be used toward qualifying college expenses.

It’s also often used by states and schools to see if you’re eligible for its student aid programs. Some private entities might also use it to determine your eligibility for their own financial aid programs.

Recommended: What Costs Does a Student Loan Cover?

How FAFSA Works

Students must complete the FAFSA before each college year. Applications must be received by the June 30 deadline. However, you can begin submitting your FAFSA for the following school year starting on October 1 (for the 2024-25 FAFSA, the FAFSA will be available in December 2023), and states and colleges often have earlier deadlines for state- and school-sponsored aid.

Some federal aid is granted on a first-come, first-served basis. Many of the aid programs are based on need, though some — like Direct Unsubsidized Student Loans and Direct PLUS Loans — are not.

To start, you’ll have to create a Federal Student Aid (FSA) ID online. If you’re a dependent student, one of your parents also needs to create their own FSA ID. While filling out the FAFSA, you may need to reference or submit supporting documentation, such as your Social Security number, bank account statements and tax return details, and possibly a parent’s financial paperwork, too.

After submitting the FAFSA, you’ll receive a Student Aid Report (SAR), which is an overview of the information you included on your FAFSA. Once your FAFSA is processed, you’ll receive a financial aid offer from your school. It will outline the types of federal student aid you’re eligible for, the amounts, and instructions on how to accept the award offer.

After you’ve selected the financial aid options you want to accept, the funds will be sent directly to your school. Then, your school will apply the funds to your unpaid account balance.

The FAFSA may also be used to apply for financial aid for summer classes.

Recommended: 2024-2025 FAFSA Changes, Explained

FAFSA Requirements

FAFSA qualifications include academic and financial criteria. Although some federal aid programs, like the federal Pell Grant, require you to demonstrate financial need, you might still qualify for other federal aid options if you meet the remaining FAFSA eligibility requirements.

Education Requirements

The level of education you’ve completed must meet the minimum requirements to qualify for a college or career school program. This includes a high school diploma or General Education Development certificate from a state-approved school or setting.

Citizenship or Residency and Social Security Number

Another of the FAFSA eligibility requirements is that students must be a U.S. citizen or U.S. National with an active Social Security number.

Eligible non-citizen students might still be eligible for federal aid if they have:

• A permanent resident Green Card (Form 1-551, I-151, or I-551C)

• An arrival-departure record (I-94)

• A T-VISA

• Battered Immigrant Status

Be Enrolled or Accepted

Students must also be enrolled as a regular student at a degree- or certificate-granting school. To meet FAFSA qualifications for a Direct student loan, you must be enrolled at least half-time.

Maintain Satisfactory Academic Performance

Returning students who are applying for federal financial aid must maintain Satisfactory Academic Progress (SAP).

Each school determines its own SAP criteria, which includes minimum GPA, minimum passing grades for courses, number of required course credits or hours, and the timeline it deems necessary to advance toward a degree or certificate.

Age and Dependency Status

Your dependency status determines whose information you’ll need to include on your FAFSA. Dependent students are required to provide their parents’ financial information on their FAFSA while independent students might not need to.

Generally, you’re considered an independent student if at least one of the following applies to you:

• For the school year you’re applying for aid, you’ll be 24 years old by January 1.

• You’re married or separated (but not divorced).

• You’re a graduate-level student.

• You have children and provide more than half of their support.

• You have other dependents in your household whom you provide more than half of their support.

• You’re in the U.S. armed forces and on active duty (non-training).

• You’re a U.S. armed forces veteran.

• Since turning age 13, your parents were deceased, you were in foster care or a ward or dependent of the court.

• You’re an emancipated minor or are in a legal guardianship.

• You’re an unaccompanied homeless or self-supporting youth at risk of homelessness.

Income Limits

A common misconception is that students or their parents must earn below a certain income to meet FAFSA eligibility requirements. However, there is not a FAFSA income limit for student applicants and their families.

Required Documents to Submit FAFSA

Although you won’t need to submit copies of additional documents with your FAFSA, you’ll need to refer to certain documents to complete your application. It may also be helpful to keep these documents on file in case your school requests to see them.

Social Security Number

You’ll need your Social Security number to include on your FAFSA form. If you’re a dependent, the form also asks for your parents’ Social Security number. If they don’t have one, enter all zeros without dashes.

W-2s and Untaxed Income Records

A main FAFSA requirement to successfully complete the application is reporting your income, and your parents’ income, if applicable. Make sure to reference all W-2s and untaxed income documentation, like interest income, child support, or other noneducation benefits.

If you are a dependent student, you’ll need to provide information from both yours and your parent’s W-2.

Tax Returns

You’ll need to reference your most current tax return information as well as your parents’ tax returns if you’re a dependent student. If you’ve already filed your tax return for the year, you might be eligible to use the IRS Data Retrieval Tool to transfer your tax information into the FAFSA.

Asset Records

You’ll also need to include your and your parents’ deposit account balances, like checking and savings, on your FAFSA. Similarly, investments, like stocks, bonds, and real estate that isn’t your primary home, must be included on your FAFSA form.

Alternatives to Federal Aid

Outside of the FAFSA application, there are other avenues to secure funds to pay for your higher education.

Savings

Consider tapping into existing savings, if your financial aid award comes up short. Doing so might help you avoid taking on more student loan debt.

There are certain accounts such as 529 savings plans that are designed to help parents and families save for their child’s education.

Grants

Research non-federal grants from your state, school, nonprofit, or other private organization. These funds don’t need to be repaid.

Scholarships

Scholarships are another aid source that doesn’t need to be repaid after leaving school. Find state-, school-, or private-sponsored scholarships to find more cash. There are online databases such as Scholarships.com that aggregate information on available scholarships. Take a look to review eligibility criteria and application requirements.

Part-Time Work

If you can manage balancing schoolwork with a part-time job, earning an income while enrolled in school can help you pay your way through your education.

Private Student Loans

Private student loans are available through private lenders, like banks, credit unions, and online institutions. These loans come with varying terms and interest rates, and can help cover the gap between your cost of attendance and existing financial aid.

When comparing private student loans and federal student loans, know that private lenders aren’t required to offer the same benefits or protections as federal student loans. As a result, private student loans are generally considered an option only after other sources of financing have been exhausted.

The Takeaway

Regardless of your or your family’s income, it’s generally worth submitting an application if you meet the FAFSA requirements. Since it’s a free application, there’s nothing to lose and much to gain if you’re eligible for aid, including scholarships and grants that don’t need to be repaid.

If you still need financial aid after submitting your FAFSA and searching for scholarships, consider a SoFi private student loan. It’s a zero fee loan option that offers competitive rates for qualifying borrowers.

Get pre-qualified in just a few minutes.

FAQ

How much or little income do you need to qualify for aid through FAFSA?

There are no income requirements for FAFSA applicants. Instead, a variety of factors determine whether a student is eligible for federal aid, including the school’s cost of attendance, the student’s year in school, their dependency status, family size, and more.

What is the maximum amount of money FAFSA gives?

The maximum amount of aid you can receive through the FAFSA depends on which federal aid programs you qualify for. Different programs have varying limits.

For example, the maximum Pell Grant award changes annually; for the 2022-23 award year the limit is $6,895. Direct Loans also have their own annual and aggregate borrowing limits.

How does parent income affect FAFSA aid?

Parent income that’s reported on a student’s FAFSA is used to calculate the applicant’s Expected Family Contribution (EFC). The EFC is a number on an index that helps schools determine your financial need if you attend its school. It also identifies your eligibility for certain financial aid programs like the Pell Grant or Direct Subsidized Loans.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

SoFi Private Student Loans Please borrow responsibly. SoFi Private Student Loans are not a substitute for federal loans, grants, and work-study programs. You should exhaust all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

SoFi Private Student Loans are subject to program terms and restrictions, and applicants must meet SoFi’s eligibility and underwriting requirements. See SoFi.com/eligibility-criteria for more information. To view payment examples, click here. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Rent prices are on the rise, with the average cost increasing 18% between 2017 and 2022. But buying a home requires a hefty down payment and good credit. Renting to own your home can give you the best of both worlds, but there are some downsides.

If you’re thinking about signing a rent-to-own agreement, it’s important to weigh the pros/cons of rent-to-own home deals. Here’s what you need to know before you sign on the dotted line.

What are rent-to-own homes?

When you own a home, part of your monthly payments goes toward paying off the principal. If you stay in the home long enough, you’ll own it.

The same doesn’t apply to rentals. Your monthly rent solely covers your costs of living in that home, whether it’s a condo, apartment, townhouse, or single-family house.

A rent-to-own home lets you pay rent to live on the property, with the option to buy it when the lease runs out. In some cases, a portion of your rent goes toward the purchase price, but that isn’t always the case.

How does rent-to-own work?

A rent-to-own agreement is essentially a lease agreement with an option to buy. Rent-to-own contracts should be read thoroughly. Those options can vary from one contract to another.

When you sign a rent-to-own contract, you pay an upfront fee called an option fee. This is typically 1 to 5% of the home’s purchase price, and it’s non-refundable.

It’s important to note that a lease does not relieve you of the requirements to buy a house. You’ll still have to qualify for a mortgage and make a down payment. It’s merely a way to buy yourself some time and possibly put some of your rent toward the purchase price of a home.

Lease Option vs. Lease Purchase

Before you sign, pay close attention to the lease agreement you’re signing. There are two types, and one contractually obligates you to buy the property.

Lease Option Agreement

A lease option agreement is the best deal of the two for you, the buyer. You’re signing a lease option contract that merely gives you first rights to the house when the lease is up. If you change your mind, find a better deal, or can’t qualify for a mortgage, you can find somewhere else to live and move your belongings out.

Since the option fee is nonrefundable, it’s important to note that you will lose money if you choose not to buy. Calculate this loss when you’re deciding whether to buy.

Lease Purchase Agreement

Unlike a lease option agreement, lease purchase agreements obligate you to buy at the end of the lease. Since it’s a contract, that means you’re legally obligated to purchase the house.

This can be risky for a couple of reasons. Once you’re in the house, you may see issues you didn’t notice when you were first touring the house. Things could change with the neighborhood or your circumstances that you couldn’t know at the outset.

But the biggest issue with a lease purchase contract could simply be that you aren’t eligible for a mortgage to buy the house. Make sure you know, up front, what penalties or liabilities you’ll face if you can’t buy the house when your lease is up.

Even though both agreements operate differently on your end, they do obligate the seller to give you the option to buy when your lease expires. This puts you in a position to own a home at a predetermined future date, giving you the opportunity to start planning.

Length of a Rent-to-Own Agreement

Rent-to-own contracts start with a lease period that can be up to five years but is usually less than three. The thought is that the rental period will give a renter time to qualify for a mortgage. During this time, you’ll work on building your credit, if necessary, and saving for a down payment.

In some cases, a rent-to-own arrangement could have renewal terms. That means if you reach the end of the lease and want more time, you can extend the lease. With this option, though, the property owner could increase your monthly rent or the purchase price.

Preparing for Homebuying

During your lease term, you’ll make each monthly rent payment in exchange for remaining in the house. But it’s important during that time that you work toward purchasing the house when your time is up. Here are some things to do to boost your chances of landing a mortgage once your lease expires.

Boost Your Credit Score

Your rent-to-own deal requires that you qualify for a mortgage once the term is up. To do this, you will need to meet the minimum credit score requirements. You can get a free copy of your credit report each year at AnnualCreditReport.com, but there are also credit monitoring services that can help you stay on top of things.

Although requirements can vary from one lender to the next, Experian cites the following credit scores as necessary to land a mortgage:

FHA: If you qualify, a Federal Housing Association loan will accept credit scores as low as 500.

USDA loans: Those who meet the requirements can qualify with a score as low as 580.

Conventional loan: Generally 620 or higher, but some lenders require 660 at minimum.

VA loans: Eligible military community members and their families can obtain loans with scores as low as 620.

Jumbo loan: These loans cover houses at a higher price, so you’ll need a score of at least 700.

Save for a Down Payment

In addition to a good credit score, you’ll need to put some money down on your new home. Down payment requirements vary by loan type, but it’s recommended that you put at least 20% down. That means if you’re buying a $200,000 home, you’ll need at least $40,000 by closing.

There are lower down payment options, but if you choose those, your mortgage payments will include something called private mortgage insurance. This will increase your monthly payment by $30 to $70 per $100,000 borrowed.

If you can’t save up 20%, you may qualify for an FHA loan, which requires as little as 3.5% down. Both VA and USDA loans have zero down payment options, and there are programs offering down payment assistance to those who qualify.

The best part about rent-to-own properties, though, is that some come with rent credits. With a rent credit, a percentage of your rent will go toward your required down payment. Calculate in advance how much you’ll have in that escrow account at the end of your lease to make sure you save enough to supplement it.

What are the pros of rent-to-own?

Rent-to-own homes can be a great option, especially during a tight housing market. If there’s a house you want to buy, but you can’t make a down payment or your credit isn’t where it should be, it could be a great workaround. Here are some of the biggest benefits of rent-to-own agreements.

Rent May Go Toward Purchase Price

Depending on the terms of the rental agreement, renting to own could help you work toward paying for the home. Instead of the full amount of your rent being pocketed by a landlord, a percentage of your rent could go toward the eventual purchase price. Before signing, pay attention to rent credits and try to negotiate the best deal possible.

The Purchase Price Is Locked In

When a landlord agrees to a lease option, the home’s purchase price is written into the contract. That price will typically be higher than what the market says it’s currently worth. This means if the U.S. housing market sees an unexpected increase, you’ll be buying the home for less than its value. Even if the market dips, once you purchase the house and remain there for a few years, you may be able to sell it at a profit.

You’ll Buy Extra Time

For many renters, the rent-to-own period provides time to qualify for a mortgage. If you’ve researched all the options and found you’re close but not quite there yet, a rental period could be just what you need.

Before you choose this option, though, take a look at your circumstances. If substantial existing debt and poor credit mean you won’t qualify, you may need more than the few years you’ll get with a rent-to-own agreement.

No Moving Necessary

Let’s face it. Moving can be a pain. You have to pack everything up, line up a moving truck and get help moving, and unpack your items once you’re in the new location.

With a rent-to-own agreement in place, you skip the hassle of moving. You’ve already been in that home, making monthly rent payments, for at least a couple of years. You’ll simply go through the closing process and switch from rent payments to mortgage payments.

What are the cons of rent-to-own?

If you can get a mortgage, that’s always going to be a better option than renting or leasing to own. But there are some instances where renting without the buy option could be better for you. Here are some things to consider.

Rent-to-Own Home Maintenance

Before you sign any lease agreement, it’s important to read the fine print. One thing to note, specific to own agreements, is who will be responsible for maintenance during the rent-to-own period. If you rent without the promise of eventual ownership, your landlord will take care of those costs. In some cases, rent-to-own agreements require the renter to handle all repairs.

But there’s an upside to handling repairs on your own. To your landlord, the property is technically yours. That means you likely will give it more TLC. Still, it’s well worth it to pay for a home inspection before you agree to a rent-to-own agreement. This will identify any serious issues that will need to be addressed before you buy.

Option Fee

One distinguishing feature of a rent-to-own property is the option fee. This is usually between 1 and 5% of the purchase price and is non-refundable. That means if you don’t ultimately qualify for a mortgage, you’ll lose that money.

Home Values Could Drop

Property values aren’t guaranteed. Your landlord estimates the value of the property, but if you’re in a rising market, you might get that home at a steal. While that’s good news for you, the reverse can happen. If housing prices drop substantially during that time frame, you could find yourself buying a property for more than it’s worth.

Contract Breaches Can Be Costly

Rental agreements are a legal obligation. If you don’t pay your rent, your landlord can evict you and keep your security deposit. But rent-to-own contracts bring an additional level of risk. Missed payments mean you could be evicted and lose all the money you’ve put in. That includes the upfront fee and any rent credit you’ve earned.

All that money will also be lost if you can’t qualify for a mortgage when your rental time is up. These agreements can give you some breathing room. However, if your low credit scores, income, lack of a down payment, or employment situation make you ineligible for a mortgage, you could be searching for another rental while losing everything you’ve paid on the lease-to-own home.

Steps to Buy a Rent-to-Own Home

Once you’ve decided renting to own is the route you want to take, you may wonder what to do next. The following steps can help you ensure you get the best deal in a rent-to-own agreement.

1. Find a Home

This is more challenging than it might sound, especially if you’re looking in a competitive real estate market. Rent-to-own homes are extremely rare, so you may have to find a home for sale and try to negotiate this type of setup.

Typically, homeowners become renters when they can’t sell their homes. This means your rent-to-own contract might be on a home that’s in a less desirable or convenient area of town. For someone whose home has been on the market for a while, being able to collect rent money with the promise of a sale in a few years can be a huge relief.

For best results, find a real estate agent who can help you track down a home and negotiate with the seller. The National Association of REALTORS® maintains a directory of real estate agents, but you can also ask for a referral or find real estate agents nearby who have brokered these types of deals recently.

2. Research the Home

Even if it’s tough to find a lease-to-own home in your area, don’t snatch up the first one you find. Crunch the numbers to make sure the rent and purchase price make financial sense for you. Look at the sale history of the home to verify that the owner’s estimated purchase price is somewhat within what the median home price will likely be when your lease expires.

3. Research the Seller

The seller needs to be looked into as well. This is even more important with rent-to-own agreements since this person will be your landlord for the entire lease period. If you see any red flags during your interactions with the seller, move on.

4. Choose the Right Terms

Before you make a real estate purchase, you would have a closing attorney review the documents. The same goes for a rent-to-own agreement. Run all the paperwork past a real estate attorney to make sure there’s nothing in the contract that will hurt you in the long run.

Your real estate agent should be able to negotiate the best terms for you, including how each rent credit will help you build equity and what happens at the end of the lease.

5. Get a Property Inspection

Any time you make a home purchase, it’s essential to know what you’re buying. The same is true for rent-to-own properties. A home inspector can check things out and make sure you aren’t purchasing a home with serious issues.

6. Start Preparing to Buy

Once you start making rent payments, it’s time to start preparing for your eventual home purchase. Chances are, you’ll have to make a sizable down payment on a home loan, so plan to have that ready. Also, keep an eye on your score with all three credit bureaus and make sure you’ll qualify.

A rent-to-own contract can be a good deal for both the buyer and the seller. It can give you time to save money and improve your credit score. A real estate lawyer should take a look at your contracts and make sure your best interests are protected.

Bottom Line

Rent-to-own homes present a unique option for potential homeowners. This approach offers the opportunity to enter the homeownership arena at a slower pace, allowing individuals to build credit, save for a down payment, and experience living in the home before making a final purchase decision.

However, the rent-to-own path isn’t free from drawbacks. Potential buyers should be wary of unfavorable terms, higher monthly payments, and the risk of losing money if they decide not to buy. Ultimately, like all significant decisions in life, choosing a rent-to-own option requires careful consideration and thorough research.

Frequently Asked Questions

Where can I find rent-to-own houses?

Rent-to-own houses can be found through specialized websites dedicated to these types of listings, local real estate agents familiar with the concept, or sometimes through classified advertisements in local newspapers or online platforms.

Can I find rent-to-own homes on Zillow?

Yes, Zillow does list rent-to-own homes. When searching for properties, you can filter the search results to show only rent-to-own options. However, availability may vary based on the region and market conditions.

How long is the typical rent-to-own contract?

The typical lease term ranges from one to five years, but terms can vary based on the agreement between the homeowner and tenant.

Do I have to buy the house at the end of the lease?

No, the decision to buy is optional. However, if you decide not to purchase, you may lose any upfront fees or additional monthly amounts set aside for the potential purchase.

Can the seller change the purchase price once set?

Generally, the purchase price is fixed in the initial agreement. However, some contracts may have clauses allowing price adjustments based on market conditions.

What happens if the property value decreases during the lease period?

If the home’s value decreases and you’ve agreed on a set purchase price, you could end up paying more than the current market value. It’s crucial to negotiate terms that protect your interests.

Who is responsible for repairs and maintenance?

The agreement should clearly outline these responsibilities. In most cases, the tenant bears the responsibility for maintenance and repairs during the lease term.

What’s the benefit of a rent-to-own agreement for sellers?

Sellers can generate rental income while waiting to sell, often at a premium. It also widens the pool of potential buyers, especially those who need time to improve their credit or save for a down payment.

How do property taxes work in a rent-to-own agreement?

In a rent-to-own scenario, the property taxes are typically the responsibility of the homeowner, as they still retain ownership of the property during the rental period. However, the specific arrangement can vary based on the terms of the agreement.

Some contracts may stipulate that the tenant pays the property taxes directly or reimburses the homeowner. It’s crucial for both parties to clearly understand and agree upon who will cover the property tax obligation before entering into a rent-to-own contract.

If I don’t buy, do I get a refund for the extra money paid?

Typically, the extra money paid above regular rent, often referred to as “rent premium,” is forfeited if you decide not to buy.

Is the rent in a rent-to-own agreement higher than usual?

Often, yes. A portion of the monthly rent may be used for the potential down payment or purchase price, making it higher than the average rent for similar properties.

What’s the difference between rent-to-own and mortgage?

Rent-to-own is an agreement where a tenant rents a property with the option to buy it at the end of the lease. No bank is involved initially, and the tenant isn’t obligated to buy. A mortgage, on the other hand, is a loan specifically for purchasing a property. The buyer borrows money from a bank or lender and agrees to pay it back with interest over a predetermined period.

Does rent-to-own hurt your credit?

A rent-to-own agreement, in itself, doesn’t usually affect your credit. However, if the homeowner reports late payments to credit bureaus, it could hurt your credit score. On the positive side, consistently paying on time and eventually securing a mortgage can benefit your credit.

What is another name for rent-to-own?

Rent-to-own agreements can go by various names, including:

Lease to purchase

Lease option

Rent-to-buy

Rent-to-purchase option

Lease purchase

Each of these terms represents the concept of renting a property with the potential option to buy it after a set period.

The difference between the two travel cards mostly comes down to basic math: As a mid-tier travel card, the Sapphire Preferred has a$95 annual fee, but the Venture X is considered a premium travel card — and has the hefty price tag to match. The Venture X certainly delivers when it comes to luxury perks, but the card won’t be the right choice if you won’t make use of any of those benefits, or aren’t willing to pay for them.

Here’s how to decide between the Chase Sapphire Preferred® Card and Capital One Venture X Rewards Credit Card.

At a glance

How the cards compare

Capital One Venture X Rewards Credit Card

Chase Sapphire Preferred® Card

on Chase’s website

Annual fee

Welcome bonus

Earn 75,000 bonus miles when you spend $4,000 on purchases in the first 3 months from account opening, equal to $750 in travel.

Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That’s $750 toward travel when you redeem through Chase Ultimate Rewards®.

Rewards

10X miles on hotels and rental cars booked through Capital One Travel.

5X miles on flights booked through Capital One Travel.

2X miles on all other purchases.

Earn 5X points on travel purchased through Chase Ultimate Rewards®, excluding hotel purchases that qualify for the $50 annual Ultimate Rewards® hotel credit.

Earn 3X points on dining, including eligible delivery services, takeout and dining out.

Earn 3X points on online grocery purchases (excluding Target, Walmart and wholesale clubs).

Earn 3X points on select streaming services.

Earn 2X on travel purchases not booked through Chase Ultimate Rewards® .

Earn 1X per dollar spent on all other purchases.

Extra benefits

$300 annual credit for bookings through Capital One Travel.

$100 credit for Global Entry or TSA PreCheck.

Get 10,000 bonus miles (equal to $100 toward travel) every year, starting on your first anniversary.

Every year, earn bonus points equal to 10% of your total purchases made the previous year.

Up to $50 in statement credits each account anniversary year for hotel stays purchased through Chase Ultimate Rewards.

Still not sure?

Why Chase Sapphire Preferred® Card is better for most people

Lower annual fee

Annual fees for credit cards aren’t inherently bad, and in most cases the more you pay, the more you get. Still, forking over a large fee for a travel card can be a tough pill to swallow. The annual fee for the Chase Sapphire Preferred® Card is several hundred dollars less than the Venture X’s. And when you consider how much value you get for the Chase Sapphire Preferred® Card and its $95 annual fee, many people will find it hard to justify paying hundreds more for another travel credit card.

Better transfer partners

Transfering points to a partner airline or hotel is one of the best ways to squeeze more value out of them. While Chase has fewer transfer partners than Capital One, most travelers will find Chase’s to be more attractive. For example, only Chase partners with United and Hyatt, and Hyatt boasts perhaps the best transfer value at 2.3 cents per point, according to NerdWallet’s analysis.

Capital One also boasts an array of airline and hotel transfer partners, but they are largely foreign brands. Savvy travelers can find outsize value from Capital One’s partners, but many travelers will find Chase’s options more accessible.

Full list of Chase transfer partners

Aer Lingus (1:1 ratio).

Air Canada (1:1 ratio).

Air France-KLM (1:1 ratio).

British Airways (1:1 ratio).

Emirates (1:1 ratio).

Iberia (1:1 ratio).

JetBlue (1:1 ratio).

Singapore (1:1 ratio).

Southwest (1:1 ratio).

United (1:1 ratio).

Virgin Atlantic (1:1 ratio).

Hyatt (1:1 ratio).

InterContinental Hotels Group (1:1 ratio).

Marriott (1:1 ratio).

Full list of Capital One transfer partners

Aeromexico (1:1 ratio).

Air Canada (1:1 ratio).

Air France-KLM (1:1 ratio).

Avianca (1:1 ratio).

British Airways (1:1 ratio).

Cathay Pacific (1:1 ratio).

Emirates (1:1 ratio).

Etihad (1:1 ratio).

EVA (2:1.5 ratio).

Finnair (1:1 ratio).

Qantas (1:1 ratio).

Singapore Airlines (1:1 ratio).

TAP Air Portugal (1:1 ratio).

Turkish Airlines (1:1 ratio).

Accor (2:1 ratio).

Choice Privileges Hotels (1:1 ratio).

Wyndham Rewards (1:1 ratio).

Broader rewards structure

The rewards structure on the Chase Sapphire Preferred® Card makes the card more suited for everyday spending than the Venture X. The latter has the potential to earn up to an eye-popping 10x on travel, but you’ll have to book that travel through the Capital One portal. The card earns a respectable 2x on everything.

With the Chase Sapphire Preferred® Card you’ll earn 3x points on dining, including delivery services and takeout; streaming services; and online grocery purchases. If your spending habits sync with the Sapphire Preferred’s rewards structure, you’ll be able to effortlessly rack up points to pay for your next vacation.

🤓Nerdy Tip

By adding another no-fee card or two to your wallet, you can create a Chase Trifecta and supercharge your Ultimate Rewards® earnings. The Chase Freedom Flex℠ earns 5x up to $1,500 per quarter in rotating bonus categories when you activate (1x on everything else), plus 3x at drugstores.

Points worth 25% more

As major card issuers, both Chase and Capital One have their own travel portals through which cardholders can book flights, hotels and car rentals. However, Chase’s Ultimate Rewards® travel portal offers slightly better value. Points are worth 1.25 cents each when used to book through Chase while one Capital One mile is worth 1 cent.

Who might prefer the Capital One Venture X Rewards Credit Card

You want lounge access

True to its classification as a premium travel card, the Venture X grants its cardholders and two guests unlimited access to more than 1,000 airport lounges including Priority Pass lounges and Capital One lounges.

If you want lounge access but prefer Chase’s lineup of credit cards, your only option is the $550-annual-fee Chase Sapphire Reserve®.

You like Capital One’s travel portal

Booking travel through Capital One’s portal is the best way to offset most of the Venture X’s annual fee. Cardholders will receive a $300 annual credit toward travel expenses, which can be used in a single transaction or across multiple purchases. If you don’t mind booking through the portal, the $300 credit plus the 10,000 anniversary points you’ll get each year you renew (worth $100) will cover the entire annual fee of the card.

The Chase Sapphire Preferred® Card offers an annual credit, too, but it’s $50 and only good for hotel bookings through the Ultimate Rewards® portal.

You want trusted traveler program credit

Skipping the line in a crowded airport can be a huge perk, and Capital One Venture X Rewards Credit Card cardholders get a $100 credit for Global Entry or TSA PreCheck. The Chase Sapphire Preferred® Card offers no such reimbursement. Note, though, that you must pay for the Global Entry or TSA PreCheck fee with the Venture X card, and the $100 credit renews every four years, not annually.

Which card should you get?

The Chase Sapphire Preferred® Card, with its reasonable annual fee, top-tier travel partners and access to Chase’s travel portal, is the perfect entree into the world of travel credit cards. Plus, the $95 annual fee can be partly recouped by redeeming the hotel travel credit. Only if you’re after luxury perks and are comfortable paying a triple-digit annual fee should you commit to the Capital One Venture X Rewards Credit Card.

Direct Link to offer (this is a stripped down affiliate link which isn’t affiliated with anyone; support your favorite blogger by using their link; we don’t use bank affiliate links on DoC)

Chase is offering a brand new signup bonus on the Chase Freedom Unlimited card:

Signup for the Chase Freedom Unlimited card and Chase will match all cash back earned after your first 12 months of spending.

The card also offers 0% intro APR for 15 months from account opening on purchases and balance transfers. After the intro period, a variable APR of 20.49% – 29.24%. Balance transfer fee applies.

The Fine Print

This product is available to you if you do not have this card and have not received a new cardmember bonus for this card in the past 24 months.(Editor’s note: If you have the OG Freedom or Freedom Flex cards you should still be eligible for the Unlimited card and for this signup offer.)

Only Cash Back rewards earned by making purchases, including through other bonus offers, are eligible for this bonus. Statement credits and Cash Back rewards moved into your account through the Ultimate Rewards Combine Points feature or any other transfer are ineligible.

(“Purchases” do not include balance transfers, cash advances, travelers checks, foreign currency, money orders, wire transfers or similar cash-like transactions, lottery tickets, casino gaming chips, race track wagers or similar betting transactions, any checks that access your account, interest, unauthorized or fraudulent charges, and fees of any kind, including an annual fee, if applicable.)

Cash Back rewards must be earned by the end of your 12th monthly billing cycle to be included in the bonus. Please note that in some cases Cash Back rewards will not be earned until a billing cycle that occurs after the one in which a purchase is made, in particular when purchases are made near the end of a billing cycle. As a result, Cash Back rewards earned on some purchases made during your first 12 monthly billing cycles may not be eligible to be included in the bonus.

Please allow 6 to 8 weeks from the end of your 12th monthly billing cycle for bonus Cash Back rewards to post to your account.

To receive your bonus, your account must be open and not in default at the time of fulfillment. See your Rewards Program Agreement for more details about earning Cash Back rewards.

5/24 applies to the Freedom Unlimited card

Card Details

No annual fee

Card earns the following points rates:

5% on Travel purchased through Chase Ultimate Rewards (10% for the first year with this offer)

5% on Lyft through March 2025 (10% for the first year with this offer)

3% on Dining (6% for the first year with this offer)

3% on Drugstore (6% for the first year with this offer)

1.5% unlimited cash back (3% for the first year with this offer)

Our Verdict

This is an amazing offer for someone who has a lot of spend, especially for someone who spends a lot on Dining and Drugstores since you’ll earn unlimited 6x on Dining/Drugstores and unlimited 3x everywhere. It would be sweet if this offer becomes available via referrer link which would let you help a friend get a bonus along the way.

Unclear whether shopping portal earnings or referrer earnings will get doubled at year-end. The fine print is clear that cash back earned through bonus offers will be doubled, but cashback earned through statement credits will not be doubled. Based on the verbiage I believe portal and referral cashbacck would be doubled, but we’ll have to find out more. (I’m not sure how it ended up working 5 years ago when this offer was around.)

Note, someone with limited annual spend will do better signing up for the standard offer which gives $200 back after $500 spend + 5% cashback on Grocery/Gas during the first year, up to $12,000.

Check out these Things To Know About Chase Credit Cards before applying.

Depending on the severity of your symptoms, the Social Security Administration (SSA) may consider asthma a disability. This means you might qualify for Social Security Disability Insurance (SSDI). You might also qualify for work accommodations under the Americans with Disabilities Act (ADA).

How much are SSDI benefits for asthma?

The average monthly SSDI benefit for disabled workers was $1,486.83 as of August 2023

.

To determine a person’s monthly SSDI benefits, the Social Security Administration uses a fairly complicated calculation based on the person’s past earnings.

SSDI applicants also usually need 40 work credits (20 of which must have been earned in the 10 years before the disability began) to qualify for benefits. The amount needed to earn a work credit changes every year. In 2023, workers earn one credit for each $1,640 in wages or self-employment income

.

What types of asthma qualify for disability?

Because asthma can have several symptoms, “when evaluating asthma, SSA does categorize the disability with a broad use of the word,” says Amanda Bonnesen, managing partner at Berger and Green law firm in Pittsburgh.

“Being diagnosed with asthma does not automatically render an individual disabled,” Bonnesen says. “The condition must impair their ability to work and function, despite all medical options and care.”

The SSA Blue Book provides general terms for what’s covered, but separate medical diagnoses you might see in your medical records that could be covered include allergic asthma, Aspirin-exacerbated respiratory disease (AERD), cough-variant asthma, exercise-induced asthma, nighttime asthma, steroid-resistant asthma and occupational asthma, Bonnesen says.

Jennifer Cronenberg, who is senior counsel and director of legal information with the National Organization of Social Security Claimants’ Representatives, says the SSA will likely consider any form of asthma that prevents an individual from full-time work.

“Some considerations that might come into play are [when asthma causes] time off task, absences, unscheduled breaks, intolerance to dust, fumes and odors and limited stamina,” she says. “While one limitation might not knock out all work, a combination of limitations might leave a person with such limited residual functional capacity that they are unable to perform any competitive, substantially gainful full-time work activity.”

How to apply for SSDI

You’ll need several things on hand when filling out your SSDI application, including:

Your work history, including employer names, dates of employment, a list of previous jobs and information about workers compensation benefits you’ve received.

Medical records, lab and test results and information about your medications.

Contact information for your doctors, care providers and their offices, as well as the dates of your visits.

Information about family members who might qualify for benefits.

The SSA first determines if the application meets some basic requirements for benefits. Then it forwards the case to the Disability Determinations Services office in the applicant’s state. At that point, an adjuster and state physicians make the decision to approve the application.

During that time, you’ll be asked to fill out additional forms regarding your work history and daily functioning. “These forms are imperative, as it is your way to communicate with your adjudicator about your symptoms and daily struggles,” Bonnesen says. You may even be required to undergo an independent medical evaluation.

You can appeal if the SSA denies your application. When that occurs, “the case is transferred to a different adjudicator, and a new and independent decision is made on the previous medical evidence and any new medical evidence provided,” Bonnesen says.

If the SSA denies your appeal, you can hire an attorney and ask for a hearing before an administrative law judge. If you disagree with the judge’s decision, you can request a review from the Social Security Appeals Council. The final option is federal court

.

Work accommodations for asthma

People with respiratory impairments can consult the Job Accommodation Network, which is a service of the U.S. Department of Labor’s Office of Disability Employment Policy, for examples of workplace accommodations under the Americans with Disabilities Act. Examples include:

Providing air conditioning, heat and dehumidification as needed, as well as a smoke- and fragrance-free environment.

Additional rest breaks for fresh air or to take medications as necessary.

Alternative work arrangements during certain periods, such as when construction is taking place in the office and it’s causing breathing issues.

Removing the need to use stairs or walk long distances to get to your desk

.

How likely is it that the SSA will approve my SSDI application?

“The SSDI process can last up to three years before a favorable decision is made,” Bonnesen says. “It’s impossible to provide a likelihood of approval rate, since humans are on the other side of the decision.”

Statistics show, though, that the SSA denies the majority of disability claims it receives

. To set up your case with the best odds, Bonnesen recommends two things.

Maintain care. Refraining from all drug, alcohol and cigarette use during the process and remaining in medical treatment can help, Bonnesen says. For example, establishing care with specialists such as pulmonologists and allergists, undergoing all necessary testing and remaining compliant with all prescribed medications can help improve your odds.

Track your condition. Cronenberg recommends keeping a symptom journal that details things such as how often you use rescue inhalers, how often you have to take breaks after performing simple household tasks, how long those breaks last and if you have to take additional breathing treatments.

Many people love showing their holiday spirit with Christmas lights, whether just a strand of twinkle lights around a window or going all-out like the Griswolds.

While these lights are festive, it’s worth noting that they aren’t free. In fact, the cost of running holiday lights rose 13% last year, costing the average household $15.48 vs. $13.41 the prior year.

In this economy, every dollar can count, so if you want to learn how much it costs to run Christmas lights for a month and how to reduce that expense, read on.

Here, you’ll learn more about:

• How much do Christmas lights cost to run?

• How much does it cost to run Christmas lights for a month?

• How can you save money on your holiday light electric bill?

Factors Affecting the Cost of Running Christmas Lights

Running Christmas lights uses energy, which can translate to higher utility bills. How much of an increase you see in your electric bill can depend on a number of factors, including:

• How many strands of lights you use

• The type of bulbs used in each strand

• The number of hours you run your lights each day

• How many days you run Christmas lights for

• Where you live and what you pay per kilowatt hour for electricity.