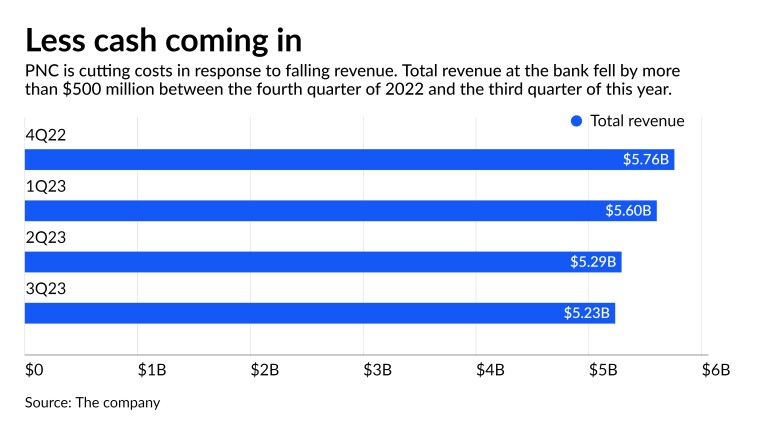

Amid falling revenue, PNC Financial Services Group said it will trim 4% of its workforce to curtail costs by $325 million and prop up its profitability in 2024.

The $557 billion-asset bank’s executives said during a third-quarter earnings call Friday that PNC initiated the staff cuts earlier this month in response to lower lending activity and declining interest income. Total revenue of $5.3 billion was down $60 million from the prior quarter and down $316 million from a year earlier.

The Pittsburgh-based bank had acknowledged earlier this week that it was cutting jobs. But it left many of the details of the plan, which will span PNC’s geographic footprint and business lines, for its earnings presentation and call on Friday.

“What’s new is basically dropping the run rate related to personnel and just tightening the ship in what is a tougher revenue environment,” CEO Bill Demchak told analysts on the call.

The projected savings, which amount to about 2% of PNC’s expected 2023 expenses, are projected to drop to the bottom line next year. They will come on top of $400 million-$450 million of savings from an annual “continuous improvement program” that was already underway, PNC said.

In July, the bank initiated a round of layoffs in its mortgage and home equity divisions. Home lending is under heavy pressure across the industry after mortgage rates more than doubled over the past two years.

In total, PNC is targeting $725 million of 2024 expense cuts, though the layoffs will necessitate a $150 million one-time charge in the fourth quarter.

The cuts will likely boost PNC’s bottom line next year, but its fourth-quarter earnings will be adversely impacted by the staff reduction charge, Autonomous Research analyst John McDonald wrote in a note to clients.

Meanwhile, Raymond James analyst Michael Rose lowered his 2024 earnings per share projection for PNC. He cited a belief that the bank’s net interest income and fee income will be lower than previously expected, and that its credit costs will be higher than previously projected, as factors offsetting the bank’s cost savings.

Rose estimated operating earnings per share of $13.45 for this year and $12.65 for 2024. Still, he maintained his “market perform” rating on PNC’s shares.

PNC Chief Financial Officer Robert Reilly explained the expense reductions by saying that 11 Federal Reserve interest rate hikes since early 2022 have taken a toll on bread-and-butter interest income and pushed up funding costs.

The trends crimped PNC’s net interest margin, which declined by eight basis points from the second quarter to 2.71%. The bank’s net interest income declined by $92 million, or 3%, from the prior quarter.

Third-quarter loans were down 2% from the prior quarter and averaged $320 billion, as more commercial borrowers moved to the sidelines amid the lofty rates.

Deposits were down 1% to $423 billion, even as PNC paid up for funding. The rate the bank paid on interest-bearing deposits increased to 2.26%, up from 1.96% for the prior quarter. That trend more than offset gains on loan yields of 18 basis points in the quarter to 5.75%.

PNC started 2023 with about 61,500 employees. It said the layoffs would be nearly completed by the end of this year.

“While decisions involving personnel are never easy, we believe they will help us more effectively and efficiently deliver for our customers and stakeholders, and we’ll continue to be diligent in our expense management going forward,” Demchak said.

Reilly emphasized that, following the July cuts, every expense category in the third quarter remained stable or declined from the second quarter. Overall noninterest expense of $3.2 billion was down 4%. Still, with no end in sight to high rates, more actions were needed to keep costs in check next year, he said.

“The current environment poses meaningful pressures,” Reilly said. “As a result, we took a hard look at our organizational structure and identified opportunities to operate more efficiently through staff reductions.”

PNC reported third quarter net income of $1.57 billion, or $3.60 per share. That was up from $1.5 billion, or $3.36, for the prior quarter but down from $1.64 billion, or $3.78, a year earlier. Analysts polled by FactSet Research Systems were expecting third quarter earnings of $3.10 per share.

Mortgage rates remain at jarringly lofty levels. In late September, the average rate on a 30-year home loan surged past 7.5 percent for the first time since November 2000, according to Bankrate data.

For October, experts don’t expect rates to depart much from that high point.

The biggest risk to mortgage rates is a broad souring of sentiment for Treasurys — a low-probability but extremely high-impact event. Barring that, October will likely bring renewed concerns about a weakening economy and strained consumer, helping reel mortgage rates back in a bit, but not enough to get below the 7 percent threshold.

— Greg McBride, Bankrate chief financial analyst

Fed’s ‘higher for longer’ keeps pressure on mortgages

Mortgage rates broke through 7 percent faster than anticipated. The average rate on a 30-year home loan was 7.42 percent as of early September, according to Bankrate’s weekly national survey of lenders. That figure surged all the way to 7.55 percent in Bankrate’s final survey of the month.

For a 30-year loan at that rate, you’d pay $702 per month for every $100,000 borrowed. At the current median national price of $407,100, that equates to about $2,775 per month, assuming you’re making a 3 percent down payment.

Not long ago, experts thought rates might fall to 5 percent this year.

At its September meeting, the Federal Reserve declined to boost its policy rate again, but did signal it doesn’t expect to cut rates any time soon.

That new outlook led to a spike in 10-year Treasury yields, which are correlated with 30-year mortgage rates.

“Higher for longer seems to be the mentality of the Fed right now,” says Scott Haymore, head of Capital Markets and Mortgage Pricing at TD Bank. “They pushed out any decrease in rates until Q2 2024.”

For months, the major mortgage rate driver was inflation and the Fed’s response. While the policymaker doesn’t directly control mortgage rates, its moves set the overall tone for borrowing costs.

Outlook hazy for the rest of the year

Economists agree that the pandemic-era 3 percent rates aren’t coming back. The question now is how much higher they’ll go.

“The biggest risk to mortgage rates is a broad souring of sentiment for Treasurys — a low-probability but extremely high-impact event,” says Greg McBride, chief financial analyst for Bankrate. “Barring that, October will likely bring renewed concerns about a weakening economy and strained consumer, helping reel mortgage rates back in a bit, but not enough to get below the 7 percent threshold.”

Some are optimistic. The Mortgage Bankers Association (MBA) predicts rates will drop to 6.3 percent by the end of 2023.

Haymore, of TD Bank, sees little change in rates in the near future.

“I think over the remainder of the year, we’ll be within a quarter point of where we are now,” says Haymore. “I don’t think we’ll see 8 percent.”

Lawrence Yun, chief economist at the National Association of Realtors, says that threshold is very much in the realm of possibility.

“In the short run, it’s possible mortgage rates may go to 8 percent,” says Yun.

More forecasts

A roadblock in more ways than one

Despite rising mortgage rates, home price appreciation hasn’t slowed and listings are still moving quickly. As the height of homebuying season fades, buyers are now weighing whether to take a higher rate — in hopes of refinancing later — or, perhaps more frustrating, wait things out.

If your aim is to close by the end of 2023, don’t delay, and carefully consider a rate lock.

“The trend has not been our friend and rates continue to get worse than I had expected based on recent data,” says James Sahnger of C2 Financial Corporation in Jupiter, Florida, adding “until we receive additional data to indicate a decidedly weaker economy, take a defensive posture when locking your rate.”

Rates above 7 percent are as much a psychological barrier as a financial one, says Lisa Sturtevant, chief economist at Bright MLS, a listing service in the Mid-Atlantic region.

“For many would-be homebuyers, a mortgage rate above 7 percent simply means that the numbers do not work for them,” says Sturtevant. “Consumer confidence has started to stumble as individuals and households are becoming more anxious about the economy.”

Indeed, 42 percent of respondents to a recent Bankrate survey cited paying for housing, either a mortgage or rent, as a negative influence on their mental health.

Still, American homeowners have proven their ability to adapt. In the 1980s, mortgage rates averaged 12 percent, but we kept buying homes.

Of course, home values weren’t nearly as high then. Add those two things together, Sturtevant says, and “the seemingly unstoppable housing market may be about to finally and truly stall out.”

It’s that time again, when presidential candidates boost rhetoric into overdrive, which sadly has revolved around the nation’s housing problems for the past couple elections.

Four years ago, Republican hopeful John McCain and Obama exchanged jabs, with the former strongly opposed to a government bailout, noting at the time that, “the fundamentals of our economy are strong.”

He got a lot of flack for that statement, especially after he couldn’t remember how many houses he owned when put on the spot (it turned out to be seven).

McCain also said he was opposed to lower down payment requirements for FHA loans (which I agreed with) and the idea of Fannie and Freddie insuring underwater mortgages – the latter eventually happened.

Housing Under Obama

As we know, Obama went on to become president and introduced a variety of programs to reduce foreclosures and improve the housing situation, most notably the Making Home Affordable plan.

It includes HAMP, HARP, HARP 2.0, FHA-HAMP, HAFA, HAFA II, and many other initiatives.

Thus far, millions of Americans have taken advantage of the programs, which include loan modifications, refinancing to lower interest rates, principal reductions, forbearance, and so on.

The President has also cut costs for FHA streamline refinances, making it much cheaper and easier for those who hold such loans to snag a lower rate.

Oh, and mortgage rates on the popular 30-year fixed are nearly three percentage points below where they stood back in 2008.

Unfortunately, there has been no magic bullet to “save” or “fix” housing thus far. Indeed, it has been a long and difficult road, and many, many Americans have lost their homes.

Perhaps one of the biggest pieces missing at the moment is a wide scale program that addresses underwater loans not owned by Fannie and Freddie.

These private-label mortgages make up a large chunk of the problem loans, but haven’t been addressed by the government, only via individual lender-based programs.

Obama actually pushed a plan to tackle these types of loans back in February, but it seemed to fall on deaf ears because it required Congressional approval.

And now Oregon Senator Jeff Merkley has proposed a similar plan, though that too has been largely ignored.

Romney Says Obama Has Failed Housing

So it appears as if a variety of programs and initiatives have been introduced under the Obama administration to help housing.

And whether you’re left or right leaning, they appear to have done some good. I’m sure many Republicans and Democrats have taken advantage of the programs on offer.

But now Republican hopeful Mitt Romney has unloaded on Obama, as we all knew he (or any opponent) would in this situation.

He noted that under Obama, home prices have fallen, 8.5 million homeowners have received foreclosure notices, and 11 million Americans owe more on their mortgages than their homes are worth.

Unfortunately, what goes up astronomically must come down, and it takes time for bad things to unravel (just look at lengthy foreclosure timelines).

That’s what we have seen over the past several years. And of course the person in charge at the time of the carnage takes the blame, even if it’s the result of actions taken years before.

Ironically, it now appears as if housing is beginning to improve, if just marginally. Home prices are finally up, negative equity levels are dropping, and homes are selling faster.

So if Romney wins the election, and housing continues on its current path, he would likely receive the praise.

Mitt’s Housing Plan

That brings us to Romney’s “plan to end the housing crisis.” Sounds pretty ambitious, doesn’t it?

So what exactly does it entail?

Well, for starters, Romney wants to unload the 200,000 vacant foreclosed homes owned by the government in a “responsible” fashion.

Romney says he’ll return these homes to productive uses and increase neighborhood values, but doesn’t specify how.

Additionally, he will facilitate foreclosure alternatives for those who can’t afford to make their mortgage payments.

Again, no specifics here, but it’ll be “creative.”

Next, Romney will replace the new “complex rules” born out of the crisis with “smarter regulations” that hold banks accountable and restart lending to creditworthy borrowers.

By the way, he blames Obama’s housing programs for making it more difficult for Americans to get a mortgage.

Last I checked, it’s more difficult to get a mortgage because they were handing them out to anybody with a pulse before the wheels fell off.

Finally, Romney plans to reform Fannie Mae and Freddie Mac, but again, doesn’t identify how.

Aside from not providing any details, it appears as if many of Romney’s “ideas” have already been implemented or addressed by the current administration.

And at the end of the day, there isn’t a magical solution to solve the current mess we’re in. It took time to get into this mess, and it will take many more years to get back on track, that is, before the next crisis hits.

There is a sinking feeling in your gut that comes with credit card debt, especially when it starts to feel unmanageable. While negotiating a credit card settlement might not sound like a fun solution, there are scenarios when it may make sense. Let’s dive in.

The Difference Between Secured and Unsecured Debt

First, let’s talk about the type of debt a credit card typically is. When a credit card company issues a credit card, it’s taking a big chance on getting its money back, plus interest. It’s more than likely that the credit card you have is considered “unsecured.”

All that means is that it isn’t connected to any of your assets that a credit card company can seize in the event that you default on your payments. Essentially, the credit card company is taking your word for it that you are going to come through with the monthly payments.

Secured debt works a bit differently. They’re backed by an asset, like your car or home. If you default on a secured debt, your lender could seize the asset and sell it to pay off your debt. Mortgages and auto loans are two common types of secured debt. 💡 Quick Tip: With lower fixed interest rates on loans of $5K to $100K, a SoFi personal loan for credit card debt can substantially decrease your monthly bills.

Credit Card Debt Negotiation Steps

The process of negotiating credit card debt usually begins when you have multiple late or skipped payments — not just one. A good first step is to find out exactly how much you owe, and then research the different options that may be available to you. Examples include a payment plan, an increase in loan terms or lowered interest rates.

Once you have that information, you’re ready to negotiate. You can start by calling your credit card company and asking for the debt settlement department. Or, you can send a note by email or regular mail.

You may have to go through a number of customer service reps and managers before striking a deal, but taking the initiative can show creditors that you are handling the situation honestly and doing what you need to do.

When you do reach an agreement, be sure to get the agreed-upon terms in writing.

Types of Credit Card Debt Settlements

Lump Sum Settlement

This type of agreement is perhaps the most obvious option. Essentially, it involves paying cash and instantly getting out of credit card debt. With a lump sum settlement, you pay an agreed-upon amount, and then get forgiveness for the rest of the debt you owe.

There is no guarantee as to what lump sum the credit card company might go for, but being open and upfront about your situation could help your cause.

Workout Agreement

This type of debt settlement offers a degree of flexibility. You may be able negotiate a lower interest rate or waive interest for a certain period of time. Or, you can talk to your credit card issuer about reducing your minimum payment or waiving late fees.

Hardship Agreement

Also known as a forbearance program, this type of agreement could be a good option to pursue if your financial issues are temporary, such as the loss of a job.

Different options are usually offered in a hardship agreement. Examples include lowering interest rate, removing late fees, reducing minimum payment, or even skipping a few payments.

Why a Credit Card Settlement May Not Be Your Best Option

Watching your credit card balance grow each month can be scary. Depending on your circumstances, a settlement may be the best solution for you.

However, it’s not without its drawbacks. For starters, a settlement may result in your credit card privileges being cut off and your account frozen until a settlement agreement is reached between you and the credit card company.

Your credit score could take a hit, too. This is because your debt obligations are reported to the credit bureaus on a monthly basis. If you aren’t making your payments in full, this will be noted by the credit bureaus.

That said, by negotiating a credit card settlement, you may be able to avoid bankruptcy and give the credit card company a chance to recoup some of its losses. This could stand in your favor when it comes to rebuilding your credit and getting solvent again.

Solutions Beyond Credit Card Debt Settlements

Personal Loan

Consolidating all of your high-interest credit cards into one low-interest unsecured personal loan with a fixed monthly payment can help you get on a path to pay off the credit card debt. Keep in mind that getting a personal loan still means managing monthly debt payments. It requires the borrower to diligently pay off the loan without missing payments on a set schedule, with a firm end date.

For this reason, a personal loan is known as closed-end credit. A credit card, on the other hand, is considered open-end credit, because it allows you to continue to charge debt (up to the credit limit) on a rolling basis, with no payoff date to work towards. 💡 Quick Tip: Before choosing a personal loan, ask about the lender’s fees: origination, prepayment, late fees, etc. SoFi personal loans come with no-fee options, and no surprises.

Transferring Balances

Essentially, a balance transfer is paying one credit card off with another. Most credit cards won’t let you use another card to make your payments, especially if it’s from the same lender. If your credit is in good shape, you can apply for a balance transfer credit card to pay down debt without high interest charges.

Many balance transfer credit cards offer an introductory 0% APR, but keep in mind that a sweet deal like that usually only lasts about six to 18 months. After that introductory rate expires, the interest rate can jump back to a scary level — and other terms, conditions, and balance transfer fees may also apply.

Credit Consumer Counseling Services

Credit consumer counseling services often take a more holistic approach to debt management. You’ll work with a trained credit counselor to develop a plan to manage your debt. Typically, the counselor doesn’t negotiate a reduction in debts owed. However, they may be able to have your loan terms increased or interest rates lowered, which would lower your monthly payments.

A credit counselor can also help you create a budget, offer guidance on your money and debts, provide workshops or educational materials, and more.

Many credit counseling agencies are nonprofit and offer counseling services for free or at a low cost. You can search this list of nonprofit agencies that have been certified by the Justice Department.

The Takeaway

When credit card debt starts to become unmanageable, negotiating a credit card debt settlement may be an option to consider. There are different types of settlement options to consider. Understanding what’s available to you — and what makes sense for your financial situation and needs — can help you make an informed decision. If a settlement isn’t right for you, there are other solutions, such as a personal loan or credit counseling services, that may be a better fit.

Think twice before turning to high-interest credit cards. Consider a SoFi personal loan instead. SoFi offers competitive fixed rates and same-day funding. Checking your rate takes just a minute.

SoFi’s Personal Loan was named NerdWallet’s 2023 winner for Best Online Personal Loan overall.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

The mere thought of filing for bankruptcy is enough to make anyone nervous. But in some cases, it really can be the best option for your financial situation. Even though it stays as a negative item on your credit report for up to ten years, bankruptcy often relieves the burden of overwhelming amounts of debt.

There are actually three different types of bankruptcy, and each one is designed to help people with specific needs. Read on to find out which type of bankruptcy you might be eligible for. We’ll also help you determine whether it really is the best option available.

What are the different types of bankruptcy?

In general, bankruptcy is the process of eliminating some or all of your debt, or in some cases, repaying it under different terms from your original agreements with your creditors.

It’s a very serious endeavor but can help alleviate your debt if you calculate that it’s unlikely to you’ll be able to repay everything throughout the coming years.

The two most common for individuals are Chapter 7 and Chapter 13. Chapter 11 is primarily used for businesses but can apply to individuals in some instances. Let’s take a look at some bankruptcy basics and the other details that set them apart from each other.

Chapter 7 Bankruptcy

Chapter 7 bankruptcy is designed for individuals meeting certain income guidelines who can’t afford to repay their creditors. You must pass a means test to qualify. Then, instead of making payments, a bankruptcy trustee can sell your personal property to help settle your debts, including both secured and unsecured loans.

There are certain exemptions you can apply for to keep some things from being taken away. It all depends on which debts are delinquent. If your mortgage is headed towards foreclosure, you might only be able to delay the process through a Chapter 7 delinquency.

If you’re only delinquent on unsecured debt, like credit card debt or personal loans, then you can file for an exemption on major items like your home and car. That way they won’t be repossessed and auctioned off.

Eligible exemptions vary by state. Usually, there is a value assigned to your assets that are eligible for exemption. You may keep them as long as they are within that maximum value. For example, if your state has a $3,000 auto exemption and your car is only valued at $2,000 then you get to keep it.

Most places also allow you to subtract any outstanding loan amount to put towards the exemption. So, in the situation above, if your car is valued at $6,000, but you have $3,000 left on your car loan, then you’re still within the exemption limit.

Chapter 7 bankruptcy is the fastest option to go through, lasting just between three and six months. It’s also usually the cheapest option in terms of legal fees. However, keep in mind that you’ll likely have to pay your attorney’s fees upfront if you choose this option.

Chapter 13 Bankruptcy

A chapter 13 bankruptcy is the standard option when you make too much money to qualify for a Chapter 7 bankruptcy. The benefit is that you get to keep your property but instead repay your creditors over a three- to five-year period. Your repayment plan depends on several variables.

All administrative fees, priority debts (like back taxes, alimony, and child support), and secured debts must be paid back in full over the repayment period. These must be paid back if you want to keep the property, such as your house or car.

The amount you’ll have to repay on your unsecured debts can vary drastically. It depends on the amount of disposable income you have, the value of any nonexempt property, and the length of your repayment plan.

How long your plan lasts is actually determined by the amount of money you earn and is based on income standards for your state. For example, if you make more than the median monthly income, you must repay your debts for a full five years.

If you make less than that amount, you may be able to reduce your repayment period to as little as three years. You can enter your financial information into a Chapter 13 bankruptcy calculator for an estimate of what your monthly payments might look like in this situation.

To qualify for Chapter 13, your debts must be under predetermined maximums. For unsecured debt, your total may not surpass $1,149,525 and your secured debt may not surpass $383,175. However, unlike Chapter 7 bankruptcy, you may include overdue mortgage payments to avoid foreclosure.

Chapter 11 Bankruptcy

Chapter 11 bankruptcy is usually associated with companies. However, it can also be an option for individuals, especially if their debt levels exceed the Chapter 13 limits. A lot of the characteristics of Chapter 11 and Chapter 13 are the same, such as saving secured property from being repossessed.

Having to pay back priority debts in full and having a higher income bracket than a Chapter 7 bankruptcy are also common characteristics. However, unlike Chapter 13, you must make repayment for the entire five years with a Chapter 11. There is no option to pay for just three years, no matter where you live or how much you make.

Another reason to pick Chapter 11 is if you are a small business owner or own real estate properties. Rather than losing your business or your income properties, you get to restructure your debt and catch up on payments while still operating your business, whether it’s as a CEO or as a landlord.

One downside to be aware of with a Chapter 11 bankruptcy is that it’s usually the most expensive option. However, you can pay your legal fees over time so you don’t have to worry about spiraling back into debt.

What are the long term effects of bankruptcy?

It should come as no surprise that going through bankruptcy causes your credit score to plummet. Depending on what else is on your report, your score could drop anywhere between 160 and 220 points.

Those effects linger. A Chapter 13 bankruptcy stays on your credit report for seven years. And a Chapter 7 bankruptcy remains there for as many as ten years. Their effects on your credit score do, however, begin to diminish as time goes by.

You’ll probably have trouble getting access to credit immediately following your bankruptcy. Eventually, you’ll start getting approved for loans and credit cards, but your interest rates are likely to be extremely high.

A new mortgage will probably be out of reach for at least five to seven years from the time you file for bankruptcy. Additionally, any employer performing a credit check can see all of these items on your credit report.

Government agencies can’t legally discriminate against you because of your bankruptcy, but there is no specific rule for privately-owned companies. It could be particularly damaging if the job you’re applying for deals with money or any type of financials. No matter where you work, though, you can’t be fired from a current employer because of a bankruptcy.

Should I file bankruptcy?

There’s no correct answer to this question. It’s ultimately something you’ll need to decide on your own. However, there are a few things you can do to make sure you’re making the best decision possible. Start by finding a licensed credit counselor to help analyze your individual situation. They’ll help you review the guidelines for each type of bankruptcy and determine if you’re even eligible.

At first glance, filing for bankruptcy may seem like a great way to settle your debts and move on with your life. Unfortunately, the process isn’t as simple as filling out a form. The effects of bankruptcy will stick with you for years.

As you begin the evaluation process of whether bankruptcy is right for you, there are several considerations to consider. This overview will get you thinking about your situation. It will also point you in the right direction for more in-depth resources when you need them.

Is your current status temporary or permanent?

You should also look at your expected future and compare your potential earnings to your amounts of debt. If you don’t see how you’ll ever pay off that debt, then bankruptcy may be a wise option. Also, understand the types of debt you owe. Tax payments, student loan debt, and liens on your mortgage or car will not be discharged even when you file for bankruptcy.

Once you figure out which specific options are available to you, it’s time to contact a bankruptcy attorney. You’re certainly able to represent yourself, but the process is complicated. It’s usually best to have a professional work on the case on your behalf. Just be sure to interview a few different lawyers to get multiple opinions and prices to compare.

Evaluate Your Situation

Even when your bankruptcy is underway, it’s smart to spend some time evaluating how you got there. Was it due to a one-time financial hardship, like a long bout of unemployment? If that’s the case, then you know that you have a brighter future ahead of you with the promise of work and steady income to pay your bills.

However, if you’re on the path to bankruptcy because of reckless spending, you really need to look inward and address your overspending habits. Otherwise, it becomes too easy to put yourself in the same situation a few years down the road. Use your bankruptcy as a second chance to start fresh with a clean financial slate.

Why Consider Bankruptcy?

If you’re considering bankruptcy, then you’re most likely feeling overburdened with debt and other financial obligations. You probably have a tough time paying your bills each month and may even worry about how you’ll ever pay off some of your outstanding balances.

If you’ve already exhausted your other options, like working overtime and cutting back on your non-necessities, it might be time to seriously think about potentially declaring bankruptcy. Some signs that you might be ready include:

Increased interest rates because of late payments or bad credit

Using credit cards for daily purchases without paying off the balance each month

Already downsized things like house, car, and other assets

Working multiple shifts or jobs

Paying off debt with retirement funds

Wages are being garnished

If one or more of these situations apply to you, then you should probably continue your research into bankruptcy. If not, try finding other ways to improve your financial situation. For example, you could rework your budget if there are easy places to cut back on.

You can also try negotiating with your lenders, particularly if you’re experiencing just a short-term setback. Most lenders are willing to work with you. They would much rather set up a new payment plan than have the debt discharged or settled through bankruptcy.

Bankruptcy Alternatives

If you want to file for bankruptcy it takes careful planning. Due to the long-term legal and financial consequences of bankruptcy, there are many rules that must be followed before you’re eligible.

For example, it’s necessary to show the bankruptcy court that you have obtained credit counseling and considered debt relief options like debt settlement or debt consolidation. Bankruptcy is controlled exclusively by the federal judicial system, which strongly recommends hiring an attorney before attempting to file.

If you need help finding a bankruptcy lawyer, contact the American Bar Association. They offer free legal advice, and you may qualify for free legal services if you are unable to afford an attorney.

Creating a Checklist to Avoid Dismissal

Before you file for bankruptcy, there are several important questions you should ask yourself. There are also several key steps that you need to take. First, it’s necessary to ask yourself if you really need to file for bankruptcy.

If you don’t, you probably won’t be approved anyway. You also need to calculate income, expenses, and assets, find a trustworthy attorney, and select a credit counseling program.

It’s helpful to be methodical and to use a checklist. Failure to take the right steps and find the right credit counseling could result in more wasted money and a bankruptcy dismissal where they throw out the case.

Reasons to Delay Bankruptcy

Even if bankruptcy is the best choice for you, there may be some situations where it’s smart to delay the process so you can maximize your benefits. First, if you had a high income within the last six months that no longer applies to your situation, then you might want to wait.

That’s because the bankruptcy court weighs your last six months of income to determine your eligibility for Chapter 7 bankruptcy. If you had a nice monthly salary a few months ago but have been laid off since then, that means test isn’t going to reflect your current situation accurately.

Another reason to delay bankruptcy is if you are anticipating an upcoming major debt. New debt isn’t allowed to be discharged once you file for bankruptcy.

So, for example, if you’re about to have a major medical surgery, you might consider waiting until it’s over to include the medical bills as part of your bankruptcy plan. Talk to a professional to see the eligibility requirements. Luxury items charged right before a bankruptcy filing, for example, likely won’t be included as part of your debt discharge.

Changes in Bankruptcy Law

Before getting started, it’s important to note the changes that went into effect in 2005 under the Bankruptcy Abuse Prevention and Consumer Protection Act (BAPCPA). While the changes don’t affect some people applying for bankruptcy, they may affect others.

Federal bankruptcy laws require mandatory credit counseling to make sure you fully understand the consequences of declaring bankruptcy. It also created stricter eligibility requirements for Chapter 7 bankruptcies. For Chapter 13 bankruptcy filings, the law requires tax returns and proof of income.

An informed decision begins with understanding bankruptcy laws, the bankruptcy process, and what has changed. It’s essential to better understand these changes before you make any final decisions.

Filing Under Chapter 7 or Chapter 13

Understanding how bankruptcy works means understanding the process and laws related to Chapters 7 and 13 of the Bankruptcy Code. Depending on the details of your situation, you might be eligible to file under Chapter 7 or Chapter 13. Which route you choose has a lot to do with your income and what assets you want to keep.

Your debts can either be resolved quickly or over a several-year period. It’s helpful to read up on in-depth frequently asked questions related to each route.

Calculating Chapter 7 Means

To have all your unsecured debts eliminated under Chapter 7 bankruptcy, you must qualify under the Chapter 7 means test. Using your personal information, or a basic estimate, an online calculator can help determine this for you. When filing bankruptcy, you must also fill out an appropriate form in which you enter your income, expense information, and data from the Census Bureau and IRS.

If you don’t meet the income level requirements to file for Chapter 7 bankruptcy, you can still file for Chapter 13. A Chapter 13 will settle many of your debts after you successfully complete a three to five-year repayment program.

Qualifying and Qualifying Debts

Your debts qualify for bankruptcy relief when you can prove you are unable to pay them, but a great deal depends on your situation and which chapter you are filing bankruptcy under. Debts can be either unsecured or secured. Secured debts include mortgages, cars, and debts related to a property you’re still paying for.

Unsecured debts include credit card debt, bills, collections, judgments, and unsecured loans. It’s important to know which debts qualify for bankruptcy. But, it’s even more important to know whether your situation makes you eligible for this major step. To determine this, a full financial assessment is necessary. You can start by reading more about debts that qualify.

Defaulting on a Student Loan

If you have defaulted on a student loan, there are several options open to you. Bankruptcy is one of them, but if your goal is to have a student loan discharged under Chapter 7, this can be very difficult.

Nevertheless, taking certain steps as soon as possible can help prevent wage garnishment. Knowing your options can help you make the best choice before matters become more difficult. Under Chapter 13, your defaulted loan can be consolidated with your other bills. This will give you a better payment plan or a temporary reprieve from making payments.

If you have a federal student loan, check out your repayment options, especially if you are facing financial hardship. Otherwise, read more to figure out how to pull yourself out of student loan default.

What Assets You Can Keep During Bankruptcy

Depending on how you file for bankruptcy, there are certain assets you can keep. Different states have different exemptions, and in certain states, you can choose between state and federal bankruptcy exemptions.

If you need to have debts discharged, are out of work, and cannot afford a repayment plan, some assets might be lost. In most cases, however, people who declare bankruptcy can keep their homes and cars and much of what they own while they repay their debts under a modified plan. It all depends on your unique circumstances and how you file.

Get a FREE Credit Evaluation Before You File Bankruptcy

A bankruptcy can affect your credit for 7 to 10 years and should be considered a last resort option when all other options have failed. Many times, people file bankruptcy when it is completely unnecessary. A credit professional can help you fix your credit and deal with your creditors so you can avoid filing for bankruptcy.

Before filing bankruptcy, talk to a credit specialist:

Visit the website and fill out the form for a free credit consultation with a professional credit repair company.

Model/actress Nicole Nagel, best known for her roles in ER and Suddenly Susan has just listed her Brentwood home for $11.995 million. And it’s far from your ordinary celebrity home.

Dubbed Constellation 167, the house is an architectural marvel that features a stellar design, standing out like a huge piece of artwork compared to the traditional homes that line the family-friendly neighborhood.

The dome-shaped structure marks the first residence designed by famed architect Eric Owen Moss, who is known for daring and unconventional works.

Photo credit: Wayne Ford courtesy of Compass

Its striking design has attracted several big names in both screen and publication. The house has appeared in TV shows like Curb Your Enthusiasm and Star Trek. It has also been featured in The New York Times and included in the book 100 of the World’s Best Houses.

Nagel won a precedent-setting case against the original homeowners

In 2013, the house garnered attention when Nagel successfully won a legal dispute against its initial owners, who had concealed well-known structural flaws during the property’s sale.

According to reports, the original owners knew that the house was suffering from mold and structural damage caused by water but still sold the property without informing Nagel.

In the arbitration, Nagel was granted $4.5 million in compensation, along with attorney’s fees. Nagel’s case became a precedent and led to additional protections for home buyers and creditors in the state.

Following this, Nagel restored the property thoughtfully, making sure to preserve the home’s unique qualities. The reconstruction took four long years to finish but paid off big time, as it increased the house’s value by millions more.

Why Constellation 167 is a “love letter to geometry”

Photo credit: Wayne Ford courtesy of Compass

The first-ever residential project by world-renowned and widely published architect Eric Owen Moss, known for his experimental and daring commercial architectural endeavors, the futuristic-looking abode is said to be a “5,476-square-foot love letter to geometry.”

From the outside, the house looks more like a contemporary art sculpture than a family home.

Its exteriors showcase edgy details, a stucco finish, tilted windows, and a curved, asymmetrical roofline.

Photo credit: Wayne Ford courtesy of Compass

But looks can be deceiving and while its exteriors are avant-garde, the inside offers a lot of coziness.

The interiors boast vast living spaces, with expansive white walls and lots of natural light coming in from its large windows and many skylights. The inside also showcases unique details, with unconventional staircase layouts spread over its levels, uneven pathways, and a jagged steel fireplace.

Throughout the generous 5,476 square feet of living space, we find four bedrooms, five bathrooms, a large dining room, a well-equipped kitchen, and a dramatic 2.5-storey living room.

Photo credit: Wayne Ford courtesy of CompassPhoto credit: Wayne Ford courtesy of CompassPhoto credit: Wayne Ford courtesy of CompassPhoto credit: Wayne Ford courtesy of CompassPhoto credit: Wayne Ford courtesy of CompassPhoto credit: Wayne Ford courtesy of Compass

One of its most notable upgrades is the backyard, which has been improved with a lagoon-like swimming pool and a lush forest garden featuring lime, lemon, peach, plum, nectarine, orange, fig, avocado, mango, and pomegranate trees that fill the side yard.

Nagel commissioned Moss to design this special area and the whole thing cost over half a million dollars. The lagoon-style pool also has a jacuzzi and is finished with underwater speakers and drought-tolerant greenery.

Photo credit: Wayne Ford courtesy of Compass

Nagel has described the home as a “meeting of geometrics, many shapes, forms and materials that come together in an extraordinary way. It is truly one of a kind, like a painting. I’ve seen people walking or driving by pause for a few minutes to take in the architecture and design and try to understand the geometry.”

Photo credit: Wayne Ford courtesy of Compass

The unique property is listed with Sally Forster Jones and Tamara Bakir with Sally Forster Jones Group at Compass; and Marc de Longeville with Vista Sotheby’s.

More stories

Jim Carrey’s house in Brentwood gets $2.4M price cut, now listed for $26.5 million

Why Brentwood is one of Los Angeles’ most glamorous neighborhoods

Inside Travis Scott’s Houses: a $23.5M Ultra-Modern Brentwood Mansion & Hip Houston Pad

UK mortgage war ‘under way’ as lender offers 4.99% fixed rate

Brokers say borrower confidence likely to lift after the first below 5% deal surfaces since June with more offers likely soon

A fixed-rate mortgage priced at below 5% has gone on sale for the first time since June as leading lenders announced a fresh wave of home loan reductions.

Brokers said a mortgage rate war was “well and truly under way” and that the lower pricing should provide a boost to borrowers worried about the imminent end of their current deal, as well as would-be homebuyers who have been sitting on the sidelines.

UK lenders have been reducing their rates for several weeks, and the last few days have seen a flurry of reductions, with further cuts due to take effect on Friday courtesy of banks including the Halifax.

On Thursday, a five-year fixed-rate deal priced at 4.99% was launched by The Mortgage Works, a division of Nationwide building society, which brokers said was the first sub-5% fixed deal they had seen for several months. It is thought it is the first fixed-rate product priced at below that level since late June.

The 4.99% product is a buy-to-let deal rather than a standard residential mortgage and is available to people borrowing up to 55% of the property’s value. Ranald Mitchell, a director at the broker firm Charwin Private Clients, said: “Seeing rates starting with a 4 is a sight for sore eyes and could provide a stimulus to the market and borrower confidence.”

Moneyfacts, the financial data provider, said the average rate on a new fixed-rate deal lasting for five years was now 6.14%, though there are best-buy deals available that are considerably cheaper than that: for residential mortgages, the cheapest five-year fix on Thursday was priced at 5.12%.

Halifax has announced reductions of up to 0.5 percentage points on selected fixed deals, taking effect from Friday. It means it will have five-year fixed deals priced at 5.15%.

The Mortgage Works has also cut rates by up to 0.5 percentage points, with effect from Thursday, while brokers say Coventry building society is also reducing some rates on Friday.

These moves come hard on the heels of cuts by other high street players. On Wednesday, Nationwide reduced some of its fixed rates by up to 0.29 percentage points, while on the same day Santander trimmed selected new fixes by up to 0.14 percentage points.

Mortgage costs had been rising for months, but UK lenders have been reducing their rates since the second half of July after it emerged that UK inflation fell further than expected in June.

skip past newsletter promotion

after newsletter promotion

However, another Bank of England rate rise next week – a decision will be announced on 21 September – could put the brakes on further reductions. The Bank’s base rate is now at 5.25%, and many commentators anticipate a rise to 5.5%.

Amit Patel, an adviser at the broker Trinity Finance, said: “After a summer of doom and gloom, it feels that as we head into the autumn months, we may have turned the corner.”

Diarmuid Phoenix, an adviser at Mint Mortgages & Protection, said: “Seeing the return of rates under the 5% bracket in line with falling swap rates should hopefully give a boost of confidence to borrowers who have been living in fear of the end of their current fixed-rate deals, as well as those who have been sitting on the fence waiting for rates to come down before purchasing.”

Investing in tech to save costs and get business in the door has become ever more important in an origination market facing extended headwinds.

Recognizing the opportunities in the mortgage space, Grant Moon, former CEO and founder of fintech platform Home Captain, is gearing up to launch his new firm – BlueForceX.

As a mortgage technology optimization platform, BlueForceX would provide data solutions, cut inflated tech solutions costs, and advise market positioning strategies.

“Given the current environment, a lot of lenders out there are looking to save money. A lot of the technologies in the tech stack that mortgage companies are pretty embedded with have high switching costs, and they have little to no flexibility with other technologies to give an integrated stack that’s best for the particular lender. Each lender’s needs are different,” Moon said in an interview with HousingWire.

“Some lenders have a stake in the ground to improve their loan execution; they’re finding it’s faltering with their POS system. Some are having top-of-funnel issues as it relates to their POS [and] some are having call center issues,” Moon noted of the challenges lenders face.

With BlueForceX’s three business lines, the platform aims to increase lenders’ leads and pull-through rates on their funnel conversions, as well as grow their funded loan volume.

Home Data Solutions – a 50-state MLS data aggregation company – will provide data solutions and a stack for lenders to have 100% MLS coverage.

With the official launch set for the first quarter of 2024, Home Data Solutions secured 50 state licenses and has relationships with 700+ MLSs.

“Home Data Solutions is a pure-play tech company. We are already in negotiations with one of the largest providers of tech to the overall industry about serving them,” Moon said.

BlueForceX’s second line of business involves working with some of the top tech solution providers.

With BlueForceX having intelligence on what other providers are charging lenders for their solutions, it can offer different vendor options (depending on the lenders’ needs) without an excessive user fee.

“Being on the vendor side of the house [previously at Home Captain], I know their job as a vendor is to charge the lender as much as you can possibly get. We work with tech vendors that we believe are the top three in any respective category,” Moon said.

He added, “If we can get competition amongst the three other providers to drive that price down, we can create additional margin for the lender.”

In return, BlueForceX will get compensated on a percentage of the money lenders are saving.

The last line of business for BlueForceX is consulting services, which range from brand market positioning and strategy to even acting as a small team to fill any gaps for lenders that downsized.

“We like to think of ourselves as entrepreneurs who care about the overall business. We are augmented as part of their team attachments, where we come in and roll up our sleeves and accomplish what the lender is looking to accomplish, which a lot of that is, helping with their margin compression issues,” Moon said.

The platform has four clients under its consulting business. For example, its current consulting service involves helping a lender build out its conversion optimization platform and serving as an M&A advisor for another lender.

In the current environment where mortgage lenders are in a big contraction given the lack of inventory, rising interest rates and affordability challenges, lenders need support, Moon noted.

“Lenders need someone on their side that can do trench warfare. There is no silver bullet. But there are five things that they can implement in the course of three months that will save the business a tremendous amount of money. That’s where we’ve been able to focus,” said Moon.

Home builder confidence took a hit in September as average mortgage rates for a 30-year fixed-rate loan stayed above 7%.

Builder confidence in the market for newly built single-family homes in September fell five points to 45, according to the National Association of Home Builders / Wells Fargo Housing Market Index released Monday. This follows a six-point drop in August.

The monthly index looks at current sales, buyer traffic and the outlook for sales of new-construction homes over the next six months. September’s reading is the first time in five months that overall builder sentiment levels dropped below the break-even measure of 50.

“The two-month decline in builder sentiment coincides with when mortgage rates jumped above 7% and significantly eroded buyer purchasing power,” said Alicia Huey of the NAHB.

Home builder sentiment had been rising earlier this year, riding the wave of demand caused by lack of inventory in the existing home market. But confidence dropped for the first time this year in August, as rates climbed.

In addition, builders continue to grapple with a shortage of construction workers and buildable lots, which is further adding to housing affordability challenges, said Huey.

All three dimensions of the new housing market evaluated saw declines in September: The index gauging current sales conditions fell six points to 51. The component charting sales expectations in the next six months also declined six points to 49. And the gauge measuring traffic of prospective buyers dropped five points to 30.

“High mortgage rates are clearly taking a toll on builder confidence and consumer demand, as a growing number of buyers are electing to defer a home purchase until long-term rates move lower,” said Robert Dietz, NAHB Chief Economist. “Putting into place policies that will allow builders to increase the housing supply is the best remedy to ease the nation’s housing affordability crisis and curb shelter inflation. Shelter inflation posted a 7.3% year-over-year gain in August, compared to an overall 3.7% consumer inflation reading.”

New homes have become an attractive alternative for buyers frustrated by extraordinarily low inventory of existing homes as homeowners hunker down with their ultra-low mortgage rates of 2%, 3%, 4% rather than selling and becoming a buyer at a 7% rate.

As mortgage rates stayed above 7% over the last month, more builders cut prices to boost sales, according to NAHB.

In September, 32% of builders reported dropping home prices, compared to 25% in August. That’s the largest share of builders cutting prices since last December. The average price discount is 6%.

Meanwhile, 59% of builders provided sales incentives of all forms in September, more than any month since April.

This available inventory and price flexibility has gotten the attention of first-time homebuyers.

According to the NAHB, 42% of new single family home buyers were first time buyers so far this year. That’s significantly higher than the 27% of first time buyers purchasing new construction homes during the same time period in 2018, when the market was more typical.

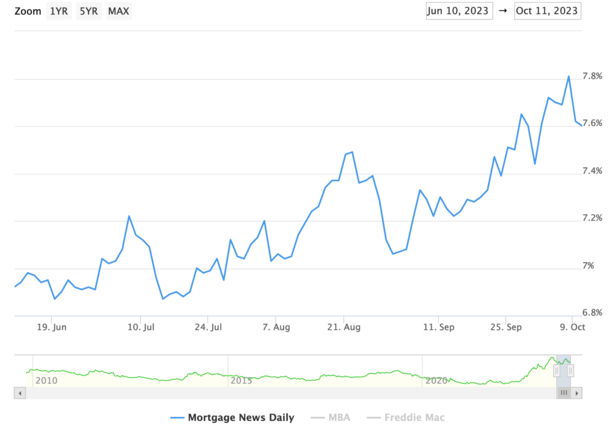

If you’ve been keeping track lately, you might be wondering why mortgage rates plunged this week.

Last week was a totally different story, with a hotter-than-expected jobs report almost enough to push the 30-year fixed across the daunting 8% threshold.

But then the unexpected happened over the weekend, as is often the case with geopolitical events.

In times of uncertainty, bonds are typically a safe haven, and when demand for them rises, their associated yields (or interest rates) fall.

This, coupled with some more dovish talk from Fed speakers, might explain the recent pullback in rates.

How Much Have Mortgage Rates Plunged?

First off, the word “plunge” might be a strong one given how much mortgage rates have climbed over the past 18 months.

While mortgage rates have indeed fallen all week, they remain well above recent lows. And even much higher than levels seen this summer.

If we want to use MND’s widely cited daily rate survey as the measure, the 30-year fixed now stands at 7.60%.

That’s down from 7.81% on Friday October 6th. So basically mortgage rates have improved by about 20 basis points, or perhaps .25% depending on the lender.

It also reduced the year-over-year change in rates from 0.77% to 0.46%, providing a glimmer of hope that the worst could be behind us.

And better yet, perhaps mortgage rates have peaked. While that remains to be seen, it’s been hard to get any meaningful relief lately.

Typically, any pullback or improvement in rates has been met with further increases. And the wins are generally short-lived.

Will that be the case again this time or is there finally light at the end of the tunnel?

Mortgage Rates Helped by New Geopolitical Risks

As for why mortgage rates improved this week, one would be quick to point to the events that took place in Israel (and continue to unfold).

Generally, mortgage rates tend to go down if there is the threat of war or similar tension in the air.

The reason is uncertainty, which is a friend to bonds because of their relative certainty.

In short, investors will flee riskier markets like equities and pile into bonds, which is known as the flight to safety.

If more investors are buying bonds, the price goes up and the yield drops. Since Friday, the 10-year bond yield has fallen from 4.84 to about 4.61 today.

Of course, this could prove to be a short-term reaction to what has been a clear move higher for bond yields lately.

So it’s entirely possible that the 10-year yield marches on back to those recent levels (and beyond) depending on what transpires.

And the conflict in the Middle East could actually exacerbate inflation if oil prices (and gas prices) rise.

No More Fed Rate Hikes Could Take Pressure Off Mortgage Rates

Another factor related to the recent mortgage rate plunge has been some dovish talk from Fed officials.

Atlanta Fed President Raphael Bostic came out this week and basically said no more interest rate hikes were needed.

The Fed has already raised its key policy rate 11 times since early 2022, pushing mortgage rates up along with it.

But Bostic “told the American Bankers Association that Fed policy is sufficiently restrictive.”

Additionally, he said rate cuts could even be in the cards “if things get ugly in the Middle East.”

“You can pretty much count on the Fed taking that into its world view and that’s only going to be lower rates.”

Earlier in the week, Dallas Fed President Lorie Logan said higher bond yields could do the heavy lifting for the Fed, requiring no additional tightening on their part.

And Fed Vice Chair Jefferson made comments that suggested he was in favor of pausing the fed rate hikes.

Interest rate traders have taken that to mean that the Fed rate hikes could be over, and the next move might be lower.

Per the CME FedWatch Tool, that cut could come by the June meeting, based on the current odds.

Though if the situation worsens in the Middle East, cuts could materialize even earlier in 2024.

As it stands now, another rate hike looks exceedingly unlikely, while a rate cut appears to be coming sooner-than-expected.

Now it’s important to note that the Fed doesn’t control mortgage rates, but their long-term outlook can have an effect on mortgage rates.

Fed Clarity Can Lower Bond Yields and Narrow the Spread

Additionally, more clarity from the Fed could go a long way in fixing the spread between 10-year bond yields and mortgage rates.

It’s currently about double its usual amount, at around 300 bps vs. 170. Knowing the Fed’s position on monetary policy could normalize spreads.

If we assume the 10-year bond yield settles in at current levels of say 4.50%, adding a more typical spread of 200 bps puts the 30-year fixed back to 6.50%.

That would spell relief for many prospective home buyers, who might be facing mortgage rates as high as 8% depending on their individual loan attributes.

Factor in paying mortgage points at closing, and it’s possible home buyers could obtain mortgage rates back in the high-5% range.

That would likely be good enough for now to get transactions flowing again, and potentially unlock some existing homeowners trapped by so-called mortgage rate lock-in.

Just beware that the trend has not been friendly to mortgage rates for a long time, and things can easily reverse course again depending on what transpires.

While it might signal a turning point, mortgage rates can also remain stubborn at these levels without significant economic data pointing to lower inflation.

And tomorrow’s CPI report alone could completely reverse the big move lower over the past couple days.

So while we’ve gotten some relief over the past few days, this so-called mortgage rate plunge may easily unwind if more hot economic data comes in. Or if global tensions ease.