Most airlines make it harder to earn elite status each year. Southwest Airlines is going the other way.

The airline is making it easier for members to qualify for its A-List elite status, and adding two free drink coupons to its list of benefits for top-tier elite status members.

In other changes to the Rapid Rewards program, Southwest is adding a “cash plus points” redemption option that will allow flyers to cover a portion of a flight’s cost with points (instead of “all or nothing”).

Here’s what to know about the changes for 2024.

Easier path to elite status

The most significant change Southwest Airlines is making to the Rapid Rewards program for 2024 involves elite status qualification.

Rapid Rewards members can earn A-List or A-List Preferred status by either flying a certain number of segments or accruing a certain number of “Tier Qualifying Points,” (TQP) which are earned through flying and spending on certain co-branded Southwest credit cards.

How do you get A-List on Southwest?

Starting on Jan. 1, 2024, Rapid Rewards members can qualify for elite status as follows:

20 one-way flights (down from 25) or 35,000 TQP (no change).

A-List Preferred

40 one-way flight (down from 50) or 70,000 TQP (no change).

Though Southwest is not reducing the number of TQP a member will need for A-List or A-List Preferred status, the airline is making it easier to earn points through credit card spending.

Cardholders will earn TQP more easily

Starting Jan. 1, 2024, members will earn 1,500 tier qualifying points toward A-List and A-List preferred for every $5,000 spent on the following credit cards:

Currently, those cards earn 1,500 TQP per $10,000 in spending, so Southwest has reduced the spending required in half.

Southwest to add cash + points option

Southwest is also making it easier for members to redeem points — particularly if they don’t have enough for an award flight — with a “cash plus points” redemption option.

Some loyalty programs, especially hotels, already offer this option. This will allow members to book a flight using a combination of Rapid Rewards points and cash. You’ll need at least 1,000 points in your account to use this option.

“Cash plus points” bookings can appeal to members short on points, but they’ll still want to be careful that they’re getting a good value for their Southwest points. The calculation should look like this: (Full cash price – cash price with points)/number of points.

Southwest is expected to roll out this change sometime in spring 2024.

A-List Preferred members get two free drinks

One additional change to the Rapid Rewards program will have top-tier Southwest Rapid Rewards elite status members saying an extra “Cheers!”

A-List Preferred members will receive two free inflight premium beverages (such as beer, wine or spirits) on eligible flights. The drink coupons will be loaded right onto the mobile boarding pass.

This will begin sooner than the other changes, effective Nov. 6, 2023.

What these changes mean for Southwest flyers in 2024

Southwest’s tweaks to its Rapid Rewards program for 2024 is generally good for frequent flyers, making it easier to earn A-List and A-List Preferred status through lowered benchmarks and more efficient TQP earnings for credit cardholders. The two free drinks for A-List Preferred members don’t hurt, either.

It’s also worth nothing, however, Southwest elite status comes with fewer tangible benefits since the airline already has free checked bags, open seating and no premium cabins. Still, since there’s open seating, A-List members’ ability to secure an earlier spot in the boarding process — arguably the best perk of Southwest elite status — certainly comes in handy for frequent flyers.

(Top photo courtesy of Southwest Airlines)

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are our picks for the best travel credit cards of 2023, including those best for:

Saving and investing both involve setting money aside for future expenses. However, there are key differences between the two.

Each has its own set of rewards and challenges. A balance of the two can lay the groundwork for financial prosperity and safeguard your wealth.

The Basics: Defining Saving and Investing

Saving: The Safety Net

What is a Savings Account?

A savings account represents the initial wealth-building step in most financial journeys. At its core, saving means putting money in a secure location, like a bank account. This ensures your money remains safe while also earning interest. High yield savings accounts, frequently found with online banks and credit unions, offer particularly appealing interest rates.

The Role of the FDIC

The safety of savings accounts, money market accounts, and CDs is often reinforced by the federal deposit insurance corporation (FDIC). This entity ensures that even if a financial institution faces challenges, your money remains protected up to the FDIC-defined limits.

Emergency Funds: Why Are They Important?

Life throws curveballs, making it essential to have an emergency fund—a financial buffer. This fund should ideally encompass three to six months’ worth of living expenses, ensuring you’re prepared for unexpected financial setbacks.

The Savings Trade-Off

While savings accounts offer peace of mind, they come with a compromise. The interest rates, especially in traditional savings accounts, often lag behind inflation. This dynamic means your diligently saved money might gradually lose purchasing power.

Investing: The Growth Engine

Dipping Into the Investment World

Investing means allocating money into assets with the hope of appreciating value. Whether it’s shares in the stock market, real estate properties, or units in mutual funds, the primary objective is growth.

Stock Market: A Historic Wealth Builder

The allure of the stock market lies in its historical track record. Over extended periods, it has typically provided returns surpassing those of standard or even high yield savings accounts. Diversifying investments, like putting money in mutual funds, can help harness these potential gains.

The Reality of Investment Risks

However, with potential reward comes inherent risk. Unlike the predictability of an FDIC-insured savings account, money put into the stock market or other investment vehicles isn’t guaranteed. It’s possible to see significant gains, but it’s equally possible to encounter losses.

When to Save vs. When to Invest: Making the Right Call

It’s vital to recognize that while both saving and investing are pillars of financial security, their roles vary according to your needs and circumstances. It’s important to know when to use each of these financial tools.

Immediate Needs and Short-Term Goals

Emergency fund: It’s always paramount to have savings set aside for unexpected expenses. Whether it’s a medical emergency, sudden job loss, or major car repair, an emergency fund acts as a financial buffer. Keeping this in an easily accessible savings account or money market account allows for quick withdrawal without penalties.

Upcoming purchases: If you’re planning major purchases within the next 1-3 years, such as a down payment for a house or a new car, the priority is preserving the principal. In such cases, a high yield savings account or a short-term CD might be more suitable than volatile investments.

Travel plans: Saving for a vacation in the next year? While it’s tempting to try to “grow” your vacation fund quickly through investments, the short timeframe means a higher risk of not having enough money when it’s time to book that trip. Opt for saving in this case.

Mid to Long-Term Objectives

Retirement: For goals that are more than a decade away, such as retirement, the potential returns from the stock market or mutual funds typically outweigh the risks. Even with market fluctuations, long-term investing often results in appreciable growth, especially if one starts investing early.

Children’s education: If you’re saving for your child’s college and they’re still in diapers, investing might offer the growth potential needed to meet rising education costs. 529 plans or other investment accounts might be apt choices.

Building wealth: If you’re aiming to increase your net worth over time and don’t have a specific goal in mind, investing is the route. It leverages the power of compound interest and potential market returns.

Debt Consideration

High-interest debts: If you’re carrying a significant credit card balance or other high-interest loans, focus on paying these down before considering investing. The interest on these debts often surpasses potential investment returns.

Personal Risk Tolerance

Emotional comfort: Your comfort with market fluctuations plays a role. If the thought of losing some of your investment keeps you up at night, even if it’s a generally recommended strategy, you might lean more towards saving or very conservative investments.

Strategies to Optimize Your Financial Balance

To establish and maintain an ideal equilibrium between saving and investing, it’s essential to employ strategic approaches that cater to evolving financial scenarios and goals. Here’s a deeper dive into methods that can help you optimize this balance.

Diversification: The Financial Safety Net

Spread your assets: Avoiding concentration in one type of investment can mitigate risks. By dividing your capital across varied assets, such as stocks, bonds, and real estate, you can potentially safeguard against significant losses in any single asset class.

Low cost index funds: These funds replicate the performance of a specific market index, like the S&P 500. Due to their broad exposure, they offer a balanced growth potential coupled with relatively lower risk. Plus, their typically lower fees mean more of your money stays invested.

Seek Professional Guidance: Navigate with Expertise

Why advisory services?: The financial landscape is vast and often intricate. For those unfamiliar or even those looking for a second opinion, brokerage services or financial advisors provide valuable insights. They help decode the complexities, ensuring your strategies align with your objectives.

Certified financial planners: CFPs undergo rigorous training and certification processes. They can offer comprehensive financial planning advice, ensuring your saving and investing strategies are cohesive and well-aligned with your broader financial goals.

Automate to Accumulate: Consistency is Key

The power of direct deposits: By automating transfers from your checking account to investment or savings vehicles, you ensure consistent contributions. Over time, this approach can substantially amplify your savings and investments.

Harness dollar-cost averaging: This strategy involves investing fixed amounts regularly, irrespective of market conditions. It can potentially reduce the impact of market volatility on your investment.

Review, Reflect, and Refine: Adaptability Matters

Changing tides: Life isn’t static, and neither is the financial world. Personal milestones, market shifts, or alterations in financial objectives can necessitate a change in strategy.

Scheduled check-ins: Dedicate time periodically (annually or semi-annually) to review your portfolios. Rebalancing, which involves realigning the proportions of your investments, can be essential to ensure they continue to match your risk tolerance and goals.

Common Myths and Pitfalls: Separating Fact from Fiction

While financial literacy has grown over the years, myths still abound. These misconceptions can hinder sound financial decision-making. Let’s demystify some of the most common myths and pitfalls in the realm of saving and investing.

Investing Equals Gambling: A Risky Misconception

Understanding the difference: Yes, both investing and gambling involve risk. However, investing is about making informed decisions based on research, market trends, and historical data. Gambling is more reliant on chance and often lacks a strategic foundation.

Strategic approach: Investors often utilize various tools, analyses, and professional advisory or brokerage services to make informed decisions. Over time, while there are market fluctuations, historically, the stock market has trended upwards.

Age Constraints: The Timeless Truth

Power of compound interest: Starting young has its perks. Even small investments can grow exponentially over time, thanks to compound interest. But it’s essential to note, it’s not just for the young.

Every moment counts: Older individuals can still benefit from investing, especially with more substantial amounts and a well-thought-out investment strategy. No matter your age, it’s about finding the right investment portfolio that aligns with your financial goals and risk tolerance.

Minimums and Barriers: Breaking the Monetary Myth

Modern investing landscape: The financial markets have become increasingly accessible. With advancements in technology and the emergence of online banks and brokerage platforms, the barriers to entry have significantly lowered.

Fractional shares & micro-Investing: Some platforms today allow individuals to invest with as little as a few dollars, purchasing fractional shares of stocks or ETFs. This democratization means that virtually anyone can participate in the financial markets, regardless of their initial investment size.

Avoiding paralysis: One of the pitfalls here is waiting for the “right amount” to start investing. This can lead to missed opportunities. Consistently investing, even smaller amounts, can be beneficial in the long run.

Safety Nets, Backups, and Financial Security: A Three-Pronged Approach

Achieving true financial security is akin to constructing a sturdy building. It’s not just about the facade or height but ensuring a robust foundation and safety mechanisms in place. Here’s an expanded view on establishing a comprehensive financial safety framework.

Building a Strong Foundation: The Indispensable Emergency Fund

Significance of the fund: Think of an emergency fund as your financial cushion. When unexpected expenses – like medical emergencies or sudden job losses – arise, this fund ensures you don’t have to dip into long-term investments or accrue high-interest debt.

FDIC insured banks and credit unions: Parking your emergency savings in institutions insured by the Federal Deposit Insurance Corporation or similar protections in credit unions offers an added layer of security. Such institutions guarantee the safety of your deposits up to a certain limit, ensuring your money is shielded against unforeseen institutional failures.

Insurance: Your Financial Umbrella

Different types, singular purpose: The world of insurance is vast: health, life, disability, homeowners, renters, and more. Each type serves a unique purpose but shares a common goal: safeguarding you and your loved ones against financially detrimental events.

Preventive approach: Paying insurance premiums might feel like an added expense. However, in the face of adversities, insurance policies can prevent significant out-of-pocket expenses, ensuring financial stability.

Tax-Savvy Approaches: Maximize Your Returns

Taxable vs. tax-advantaged accounts: Recognizing the difference between these two is crucial. A standard brokerage account will have its earnings subject to taxes annually. In contrast, retirement accounts, like IRAs or 401(k)s, offer tax advantages, either deferring tax payments until withdrawal or eliminating them altogether, depending on the account type.

Compound and save: Over time, the money you save on taxes can compound, potentially leading to significantly larger returns. Being tax-smart is a key component of holistic financial planning.

Stay Liquid: Balancing Accessibility and Growth

Importance of liquidity: Investments tied up for the long term can offer excellent growth potential. However, it’s equally vital to have assets that can be quickly converted to cash for immediate needs, without penalties or a significant loss in value.

Ideal liquid venues: Savings accounts and money market accounts are perfect contenders for such liquid assets. They offer a blend of easy accessibility and modest growth, ensuring you’re not caught off-guard by short-term financial needs.

Bottom Line

Balancing saving vs. investing is an ongoing journey, not a one-time decision. As you navigate life’s ups and downs, your strategy will need tweaks and adjustments. However, with a solid foundation, informed choices, and a commitment to both saving and investing, you can optimize both risk and security, paving the way for a bright financial future.

Frequently Asked Questions

How much should I aim to save before I begin investing?

While it varies for each individual, many financial experts recommend building an emergency fund covering 3-6 months’ worth of living expenses before starting to invest aggressively.

Can I lose all my money if the stock market crashes?

While stock market downturns can lead to significant losses, diversified portfolios can mitigate this risk. It’s rare to lose all money unless invested in single, high-risk stocks.

Do I need a financial advisor, or can I start investing on my own?

You can certainly start on your own, especially with numerous online platforms and resources available. However, a financial advisor can offer personalized advice tailored to your goals and risk tolerance.

Is real estate a safer investment than the stock market?

Both real estate and stocks come with their risks and rewards. While real estate is tangible and can provide rental income, it requires more capital upfront and may not be as liquid as stocks. Diversifying investments across asset classes can help balance risk.

What’s the difference between a Roth IRA and a traditional IRA?

Both are retirement accounts, but they differ in tax treatments. With a Roth IRA, you contribute post-tax money, and withdrawals during retirement are tax-free. With a traditional IRA, contributions may be tax-deductible, but withdrawals during retirement are taxed.

How frequently should I review and adjust my investment portfolio?

While there’s no one-size-fits-all answer, many experts suggest reviewing your portfolio at least annually or whenever there are significant changes to your financial situation or goals.

Can I invest in stocks without going through a brokerage?

Yes, some companies offer Direct Stock Purchase Plans (DSPPs) that allow investors to purchase shares directly without a broker. However, using a brokerage can offer more options and tools for managing investments.

How can I protect myself against inflation eroding my savings?

Investing a portion of your savings can help. Stocks, bonds, and real estate have historically outpaced inflation over the long term. Additionally, consider high yield savings accounts or inflation-protected securities.

Whether you’re bringing in $140,000 on your own or that’s your combined household income, you probably feel pretty confident about your homebuying journey. You’re making about double the national median household income, which is $70,784 per the latest Census data, so getting approved for a mortgage and finding homes that fit your budget shouldn’t be too tricky.

Be smart as you shop, though. Earning more makes it easy to spend more — experts call this lifestyle inflation — and if you’re not careful, a hefty monthly mortgage payment could mean your spending outpaces your monthly earnings. Let’s crunch the numbers on how much house you can afford with a $140K salary.

The 28/36 rule

Many financial experts use a fairly simple set of calculations called the 28/36 rule to assess affordability. This guideline breaks down how much of your income should go toward your mortgage and other debts: Per the rule, no more than 28 percent of your gross income should go to your housing payments each month. And no more than 36 percent should be allocated to your total debt, including housing — such as car payments, student loans and credit card bills.

Let’s apply the 28/36 rule to your $140K salary to see how much you should be spending on housing costs:

Calculator

$140,000 / 12 = $11,667 (gross monthly income)

$11,667 x 0.28 = $3,267 (the most you should spend on housing costs each month)

$11,667 x 0.36 = $4,200 (the most you should spend on total debt each month)

How much house can you afford?

But wait, you might be thinking. I want to know a purchase price, not just how much I should spend on my mortgage payments. Bankrate’s mortgage calculator can help: It shows that if you were to buy a $500,000 home, with a 20 percent down payment and a 30-year loan at 7.5 percent interest, your monthly principal and interest payments would be $2,796. That leaves you a few hundred dollars to cover home insurance premiums and property taxes, which will vary widely depending on your location, before you hit that $3,267 cap.

So hypothetically, you can afford a $500K home. Don’t forget, though, that this does not include your upfront expenditures: a 20 percent down payment on a home of that price is a significant $100,000, plus closing costs.

And these aren’t the only factors to consider before you start house shopping. Here are some other metrics mortgage lenders look at to make sure you’re not overextending yourself:

Credit score: The higher your credit score is, the better the interest rate you can get — which means you’ll pay less in interest. This translates to big savings over the life of the loan, so it’s worth getting your score in the best shape possible before your house-hunt begins.

Debt-to-income ratio: Often called DTI, this metric is similar to the 28/36 rule in that it measures how your debt obligations stack up against your income. If you stay below 36, you should be in good shape, although some lenders allow for a higher DTI.

Down payment: You might have heard that you need to put 20 percent down, but that’s not necessarily true. Some loans require as little as 3 percent for a down payment. However, paying less upfront means borrowing more, and thus bigger monthly payments. And putting down the full 20 percent lets you avoid paying private mortgage insurance on top of your mortgage payment. With your $140K salary, shelling out a bigger down payment just makes sense.

Desired location: In most parts of the country, a $500,000 housing budget will probably get you a spacious single-family home. But in particularly pricey markets, like New York City or the San Francisco Bay Area, it might buy a lot less. Consider general cost of living prices, too, from groceries to transportation to entertainment. Make sure you can afford not just the house, but the lifestyle you want to live.

Home financing options

Even if you’re comfortable spending half a million dollars on a home, you probably don’t have that kind of cash just lying around. That’s where home financing comes in.

Get preapproved for a mortgage

Before you even start house-hunting, it’s smart to get preapproved for a mortgage. Preapproval isn’t final approval, but it tells you the size of the loan you’re likely to get, which helps ensure you don’t waste time looking at homes that don’t fit within your budget. It can also be crucial in competitive markets, where there may be more than one offer on a home — your preapproval lets sellers know you are a serious, qualified buyer.

Different types of loans

There are many different types of mortgages that can help you make that half-million home yours. Most have specific credit-score requirements, and you may not be eligible for some due to your high salary. If you are a military service member or veteran, it’s well worth looking into VA loans, and FHA loans are often popular with first-time buyers and borrowers with poor credit. But with a $140K salary, you’ll probably be looking at a conventional loan. A knowledgeable loan officer or mortgage broker will be able to explore your options with you.

First-time homebuyer programs

Are you transitioning from renter to homeowner for the first time? If so, you might be able to take advantage of first-time homebuyer programs, which can range from grants to low-interest or forgivable loans offering closing cost and down payment assistance. However, many such programs come with a maximum salary cap, so your $140,000 income might make you ineligible.

Getting started

When you’re ready to jump into the homebuying market, working with an experienced real estate pro in your desired area is your best first step. Local agents know their markets well and will be able to show you home options that match your needs and your budget. Ask for recommendations from friends and family, look at yard signs in the neighborhoods you like and research online to find some good candidates. Then, interview a few people before you choose the right one for you.

Netflix has come a long way from its 1998 start of mailing rental DVDs to consumers. There’s no doubt that today it reigns as one of the most popular streaming services out there, gaining the No. 1 spot in U.S. News & World Report’s list of best on-demand streaming services for its expansive library and award-winning original content.

In fact, according to a recent Netflix earnings report, more than 238 million people have monthly subscriptions as of 2023. But is Netflix the right streaming service for you? Explore how much Netflix costs and how the cost per month could fit into your overall budget.

Netflix costs $6.99 to $19.99 per month, depending on your subscription plan. It offers three plans: Standard With Ads, Standard and Premium. A former popular choice was the Basic plan at $9.99, but Netflix recently eliminated this option for new or rejoining members. If you’re currently on the Basic plan, you can keep your account as-is until you decide to change plans or cancel.

Users can cancel anytime. They can watch for the rest of the current billing period, and service ends when the next billing cycle starts. Customers who pay with credit or debit card also have the option to pause service for a month at a time rather than canceling, for up to three months.

Netflix subscription cost

Netflix only offers monthly subscriptions; there’s no option to pay yearly for a discount.

Standard with ads: $6.99 per month

With the Standard with ads plan, subscribers can access the majority of Netflix’s library in full high-definition and watch ad-supported film and television on two supported devices at a time. Supported devices include your smartphone or tablet, smart TV, laptop, or a streaming device such as Roku or Google Chromecast.

Downloading content onto a device to watch offline is not available with this plan.

Standard: $15.49 per month

The Standard plan is similar to the Standard with ads plan in that users can watch Netflix on two devices at a time, but have the added benefit of downloading content onto two devices and watching unlimited ad-free movies and shows. The Standard plan also includes full HD.

In previous Netflix offerings, users could share passwords with friends and family not living in the same household. But in late May, Netflix cracked down on password sharing, telling U.S. customers that their Netflix account “is for you and the people you live with — your household.” Customers now must pay $7.99 per month to share their account with people outside their household. Under the standard plan, users can add only one “extra member” outside their household.

Premium: $19.99 per month

Premium subscribers have unlimited ad-free viewing and can use up to four devices simultaneously, with the capability to download content onto six devices. Enhanced viewing features, like Ultra HD and Netflix spatial audio, set Premium subscriptions apart from the other options. Premium users also have the opportunity to add to the account two extra members not within the same household for shared access, at $7.99 each per month.

Regardless of which tier seems the most suitable today, price increases are on the horizon. The price of major ad-free streaming services has escalated by 25% in the past 12 months, according to The Wall Street Journal. While Netflix has been one of the few that has not increased prices since 2022, it is reported to be planning a pricing change once the Hollywood actors’ strike is over.

How do streaming services fit into your budget?

When deciding whether to add a new streaming subscription or adjust your current ones, it’s a good idea to reevaluate your budget. The 50/30/20 framework can be helpful; it means you allocate up to 50% of your income for needs, 30% for wants, and 20% for savings and debt repayment.

Streaming services fall into the category of wants, or the 30% available from your take-home pay. There’re a few ways to approach fitting streaming services like Netflix into your budget.

First, consider all the expenditures in your wants category — are there ways to save elsewhere, like reducing online shopping or cutting back on restaurant visits? Freeing up funds from other wants can make room in a budget for costlier streaming options.

Likewise, reviewing the number of monthly subscriptions you have and reassessing whether you still use and want them all can help keep a budget on track. Ask yourself: How much do I use each service? If I have to choose one, would I rather have subscription A or B?

If you’re a credit card user, check your rewards categories and see if you earn cash back or bonus points for subscription services. While it may not be worth opening a new card for these perks alone, it can be a nice complement to an existing budgeting strategy.

Selling a house amid a divorce can make an already-complicated situation even more complex. The need to manage a real estate transaction while also managing your interpersonal conflict is stressful, but sometimes financially necessary. Every couple’s situation will be a little bit different, of course, but if you need to sell the marital house due to a divorce, here are answers to some common questions and other things to consider during this difficult process.

Should I sell the house before getting divorced?

You can sell a property before, after or during a divorce, and the best option may be different for each couple. A number of factors can impact the best timing, including housing market conditions, how amicable your split is and the financial needs of each spouse.

One thing that can be useful is to work with a real estate agent who has experience in divorce transactions. “The common denominator for a divorce sale is that the divorcing parties must mutually agree to sell the marital property,” says Lou Rodriguez, an agent with United Realty Consultants in South Florida and author of “Selling Your Home During Divorce: How Everyone Can Win.”

An additional consideration for the timeline of your home sale is the potential profit you stand to make. If the value of the property has gone up significantly since you purchased it, you may have to pay capital gains tax, and the amount is very different depending on whether your taxes are filed jointly or as single individuals. For single tax filing status, you must pay taxes on anything over $250,000 in capital gains. That number doubles to anything over $500,000 if you file jointly as a married couple.

If you sell before the divorce is finalized, be sure you have a plan for what will happen with the earnings. “You’ll want to be careful how you handle the proceeds of the sale so that those proceeds are divided fairly during the divorce process,” says Randi Dukes, an agent with Repeat Realty in Dallas–Fort Worth and a divorce real estate specialist who has earned the RCS-D (Real Estate Collaboration Specialist–Divorce) designation. “It’s often recommended that those proceeds go into a separate account that can be divided upon divorce, rather than mixing the proceeds into other joint accounts.”

What are the options?

When you are going through a divorce, there are several different ways you could decide to sell the family home. Here are some common options.

Sell the house outright

“Often, selling the house makes the most sense because it provides both parties with a lump sum of money to establish a new home and a fresh start,” says Dukes. Selling the property outright means the proceeds can be more easily divided between two people. It also gives both partners the opportunity to establish the next phase of their lives.

Sell it to your spouse

Sometimes it makes more sense for one partner to continue owning the house. This can happen when one partner will have primary custody of the children, for example, as it eliminates the need for the children to move out of their home and be uprooted.

However, this option only works if the partner buying the home can make it work financially. “The spouse keeping the house needs to do their due diligence to make sure keeping it is a sound decision,” Dukes says. “A real estate agent can look at the title to see if there are any liens or second mortgages that one spouse may not know about, and the spouse can talk to a lender or financial advisor to see if they can actually afford to keep the house.”

If this is your plan, make sure you get all your legal ducks in a row. The partner selling the house will likely need to sign a quitclaim deed giving up their rights to the property and transferring them to the other partner — have a real estate attorney manage this process.

Co-own it

You could decide to hang on to the property and continue to own it together. Co-owning might allow you to rent out the property and both gain rental income, for example. Or, you could make the property work for both of you to live there with a renovation that divides it into two units. This can be a viable option for parents who both want to stay near the children.

Give it to your kids or family members

If you’d rather keep the home in the family than sell it, you could consider gifting the property to your adult children or another relative. This option eliminates the need to prepare the property for a sale and could be a way for both partners to put the property in the hands of someone they love. Again, be sure to have a real estate attorney handle the deal for you to ensure that ownership is properly transferred — and it’s a good idea to talk to a tax professional as well, to understand any tax or estate planning implications.

Community property states vs. equitable distribution states

There are two main legal approaches to how property is divided after a divorce. It all depends on whether you’re in a community property state or an equitable distribution state.

The majority of states fall into the category of equitable distribution, which means if one party earns or purchases certain assets, those assets are considered theirs individually. The assets don’t become shared property unless both parties agree to share them. “I live and work in Florida, an equitable distribution state, which simply means Florida courts will divide marital property in a manner which it considers fair, but not necessarily equal,” says Rodriguez.

Community property states, on the other hand, consider all assets acquired during a marriage to be jointly owned by both parties, and they are divided equally in the event of a divorce. Only nine of the 50 states are community property states, according to the IRS: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin.

How to sell a house during a divorce

Selling a house can be stressful and time-intensive no matter what. Follow these steps if you decide to sell your house during your divorce proceedings.

1. Hire an experienced real estate agent and lawyer

Not every real estate agent or attorney knows how to navigate the conflict and tension that can come with selling a house during a divorce. It’s important to work with someone who has experience in sales like this, or even specializes in them.

“I would recommend that you work with someone who knows how to work in high-conflict situations and has experience in getting people moving in one direction to accomplish shared goals,” says Rodriguez. “Because whatever happens during the sale — accepting an offer, countering an offer, all the way to signing closing documents — requires that both parties agree each step of the way. It makes a difference having a transactionally experienced listing agent who has worked with other divorcing clients.”

2. Get a home estimate and agree on a sale price

It’s important that both parties come together on pricing. There are various ways to determine how much your home is worth, from online estimators to a thorough analysis of your local market prepared by a real estate agent. But a professional home appraisal, which will cost several hundred dollars, is probably the most accurate assessment of a home’s market value.

3. Sell the home and split up the net proceeds

Once you agree on the terms and price for selling the home, your agent will guide you through the home-selling process. This will involve preparing the home for the market, taking professional photos for the listing, listing and marketing the property, coordinating showings, reviewing offers and preparing all the closing paperwork. Once the sale is closed and complete, the proceeds will be shared as required by your state and established by your attorney.

Next steps

Ready to sell? It’s important to find a local real estate agent both of you feel you can trust. “Look for someone with additional training in divorce real estate, and ask them about their experience,” says Dukes. This type of agent will be skilled in handling not only the home sale but also any interpersonal conflict that may arise.

FAQs

The best time to sell a house will be different for different couples. “If both spouses agree, then selling your house before filing for divorce is an option — if you’re trying to take advantage of a strong seller’s market, this might be a good idea,” says Randi Dukes, a Dallas–Fort Worth Realtor who specializes in divorce real estate. However, selling the house after the divorce may be the right choice for other couples. Whichever timeline you choose, it’s important that both partners agree on the process.

In some cases, if both parties can’t come to an agreement on how to sell the property, yes, a court may intervene to force the sale. The laws will differ depending on your state and your specific circumstances, so be sure to consult both your divorce lawyer and a real estate attorney in your area.

Due to the financial challenges created by the COVID-19 pandemic, federal student loan payments were automatically paused from March 2020 to September 2023. During that time, interest didn’t accrue and collections activities were also paused. But now that payments are due again, many borrowers are looking for ways to make their loans more manageable, especially those who are facing ongoing financial hardships.

One option is student loan deferment, which allows you to temporarily pause your student loan payments. As with most financial decisions, there are pros and cons to deferring your student loans. Here’s more information about student loan deferment and what it could mean for your financial future.

What Is Student Loan Deferment?

Deferment is a program that allows you to temporarily stop making payments on your federal student loans or to temporarily reduce your monthly payments for a specified time period.

This is similar to another option known as forbearance. However, unlike forbearance, you may not be charged interest while your loan is in deferment. According to the Department of Education, if you hold one of the following types of loans, you will not be responsible for paying interest on your loan while it is in deferment:

• Direct Subsidized Loan

• Subsidized Federal Stafford Loan

• Federal Perkins Loan

• The subsidized portion of a Direct Consolidation Loan

• The subsidized portion of a Federal Family Education Loan (FFEL) Consolidation Loan

If you have one of the following types of loans, you will be responsible for paying the accrued interest on your loan while it is in deferment:

• Direct Unsubsidized Loan

• Unsubsidized Federal Stafford Loan

• Direct PLUS Loan

• FFEL PLUS Loan

• The unsubsidized portion of a Direct Consolidation Loan

• The unsubsidized portion of a FFEL Consolidation Loan

If you are responsible for paying interest on your student loans while they are in grad school deferment, you have two options: 1) you can make interest-only payments on the loans while they are in deferment; 2) if you choose not to make these interest-only payments, the accrued interest will capitalize (be added to the loan principal) when the deferment period is over. 💡 Quick Tip: Ready to refinance your student loan? With SoFi’s no-fee loans, you could save thousands.

How Do You Qualify for Student Loan Deferment?

In order to qualify for student loan deferment, you must meet one of the following requirements:

• You’re enrolled at least part-time at a qualifying university

• You’re unemployed or unable to find employment (for up to three years)

• You’re experiencing an economic hardship

• You’re currently volunteering in the Peace Corps

• You’re on active-duty military service (or are in the 13 months following that service)

• You’re in an approved graduate fellowship program

• You’re in an approved rehabilitation program (for disabled students)

Requesting a Deferment

If you’re interested in deferring student loans to go back to school, you’ll need to apply for an in-school deferment. Most likely, you will request the deferment directly through your loan servicer—there is usually a form for you to fill out. When you request a deferment, you’ll also need to provide some sort of documentation to prove that you qualify for a deferment.

If you are enrolled in an eligible college or career school at least half-time, may be placed in deferment automatically . If it is, your loan servicer will notify you that deferment has been granted. If you enroll at least half-time and do not automatically receive a deferment, you will need to contact the school in which you are enrolled. The school will then send the appropriate paperwork to your loan servicer, so that your loan can be placed in deferment.

Pros and Cons of Student Loan Deferment

The biggest benefit of student loan deferment is the ability to temporarily postpone student loan repayment. As of the first quarter of 2023, 2.8 million loans were in deferment.

If you are deferring for extreme financial hardship, deferment allows you to free up money to pay off bills that require immediate attention like rent or electricity.

For students who have qualified for deferment through community service, like a stint in the Peace Corps, deferment gives them the opportunity to serve their community without any added stress from student loan payments.

While temporarily pausing loan repayment may seem like a blessing, it can come at a cost, especially if your student loans are not subsidized by the government. When in deferment, interest continues to accrue on your loan. And at the end of your deferment period, that interest will be capitalized on the loan. (This means that the accrued interest will be added to the principal balance of the loan. So ultimately, you’ll be paying interest on top of interest.)

This can mean you end up paying even more money over the life of the loan. To see how much deferring your student loans could cost, you can use an online calculator to get an estimate of how much interest will accrue while the loan is in deferment.

The Pros and Cons to Student Loan Refinancing

If you have private loans that aren’t eligible for federal student loan deferment, refinancing your student loans is another option to consider. You may also want to think about refinancing when you’re done with your graduate degree to pay off your loans at a potentially lower interest rate.

When you refinance, your existing student loans are paid off with a new loan from a private lender. If you are refinancing private loans before going back to graduate school, you may be after a lower monthly payment, which you could potentially qualify for when refinancing your loans and extending the loan term. (You may pay more interest over the life of the loan if you refinance with an extended term.)

Alternatively, if you’re looking to refinance after graduate school, you could potentially qualify for a lower interest rate, which could reduce the amount of money you spend over the life of the loan. The lender will use your credit score and earning potential to determine what interest rate you’ll qualify for. And thanks to your new graduate degree, you could have significantly increased your earnings.

Another big benefit of student loan refinancing? You’re able to combine all of your student loan payments – for both federal and private loans – into one easy-to-manage payment.

If you hold only federal student loans, however, you could look into a Direct Consolidation Loan , which allows you to consolidate federal loans into one loan with a single monthly payment. The new interest rate will be the weighted average of your current interest rates (rounded to the nearest one-eighth of 1%), so unlike refinancing, when you consolidate your student loans, you won’t necessarily qualify for a lower interest rate.

If you are taking advantage of your federal loans’ flexible repayment plans or student loan forgiveness programs (or if you are planning to do so), refinancing might not be the best option for you. A major con of student loan refinancing is that you’ll lose access to federal loan benefits when refinancing with a private lender—including deferment and income-driven repayment plans.

Refinancing Your Loans with SoFi

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

With SoFi, refinancing is fast, easy, and all online. We offer competitive fixed and variable rates.

Student Loan Refinancing If you are a federal student loan borrower you should take time now to prepare for your payments to restart, including the opportunity to refinance your student loan debt at a lower APR or to extend your term to achieve a lower monthly payment. (You may pay more interest over the life of the loan if you refinance with an extended term.) Please note that once you refinance federal student loans, you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as the SAVE Plan, or extended repayment plans.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

The difference between the two travel cards mostly comes down to basic math: As a mid-tier travel card, the Sapphire Preferred has a$95 annual fee, but the Venture X is considered a premium travel card — and has the hefty price tag to match. The Venture X certainly delivers when it comes to luxury perks, but the card won’t be the right choice if you won’t make use of any of those benefits, or aren’t willing to pay for them.

Here’s how to decide between the Chase Sapphire Preferred® Card and Capital One Venture X Rewards Credit Card.

At a glance

How the cards compare

Capital One Venture X Rewards Credit Card

Chase Sapphire Preferred® Card

on Chase’s website

Annual fee

Welcome bonus

Earn 75,000 bonus miles when you spend $4,000 on purchases in the first 3 months from account opening, equal to $750 in travel.

Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That’s $750 toward travel when you redeem through Chase Ultimate Rewards®.

Rewards

10X miles on hotels and rental cars booked through Capital One Travel.

5X miles on flights booked through Capital One Travel.

2X miles on all other purchases.

Earn 5X points on travel purchased through Chase Ultimate Rewards®, excluding hotel purchases that qualify for the $50 annual Ultimate Rewards® hotel credit.

Earn 3X points on dining, including eligible delivery services, takeout and dining out.

Earn 3X points on online grocery purchases (excluding Target, Walmart and wholesale clubs).

Earn 3X points on select streaming services.

Earn 2X on travel purchases not booked through Chase Ultimate Rewards® .

Earn 1X per dollar spent on all other purchases.

Extra benefits

$300 annual credit for bookings through Capital One Travel.

$100 credit for Global Entry or TSA PreCheck.

Get 10,000 bonus miles (equal to $100 toward travel) every year, starting on your first anniversary.

Every year, earn bonus points equal to 10% of your total purchases made the previous year.

Up to $50 in statement credits each account anniversary year for hotel stays purchased through Chase Ultimate Rewards.

Still not sure?

Why Chase Sapphire Preferred® Card is better for most people

Lower annual fee

Annual fees for credit cards aren’t inherently bad, and in most cases the more you pay, the more you get. Still, forking over a large fee for a travel card can be a tough pill to swallow. The annual fee for the Chase Sapphire Preferred® Card is several hundred dollars less than the Venture X’s. And when you consider how much value you get for the Chase Sapphire Preferred® Card and its $95 annual fee, many people will find it hard to justify paying hundreds more for another travel credit card.

Better transfer partners

Transfering points to a partner airline or hotel is one of the best ways to squeeze more value out of them. While Chase has fewer transfer partners than Capital One, most travelers will find Chase’s to be more attractive. For example, only Chase partners with United and Hyatt, and Hyatt boasts perhaps the best transfer value at 2.3 cents per point, according to NerdWallet’s analysis.

Capital One also boasts an array of airline and hotel transfer partners, but they are largely foreign brands. Savvy travelers can find outsize value from Capital One’s partners, but many travelers will find Chase’s options more accessible.

Full list of Chase transfer partners

Aer Lingus (1:1 ratio).

Air Canada (1:1 ratio).

Air France-KLM (1:1 ratio).

British Airways (1:1 ratio).

Emirates (1:1 ratio).

Iberia (1:1 ratio).

JetBlue (1:1 ratio).

Singapore (1:1 ratio).

Southwest (1:1 ratio).

United (1:1 ratio).

Virgin Atlantic (1:1 ratio).

Hyatt (1:1 ratio).

InterContinental Hotels Group (1:1 ratio).

Marriott (1:1 ratio).

Full list of Capital One transfer partners

Aeromexico (1:1 ratio).

Air Canada (1:1 ratio).

Air France-KLM (1:1 ratio).

Avianca (1:1 ratio).

British Airways (1:1 ratio).

Cathay Pacific (1:1 ratio).

Emirates (1:1 ratio).

Etihad (1:1 ratio).

EVA (2:1.5 ratio).

Finnair (1:1 ratio).

Qantas (1:1 ratio).

Singapore Airlines (1:1 ratio).

TAP Air Portugal (1:1 ratio).

Turkish Airlines (1:1 ratio).

Accor (2:1 ratio).

Choice Privileges Hotels (1:1 ratio).

Wyndham Rewards (1:1 ratio).

Broader rewards structure

The rewards structure on the Chase Sapphire Preferred® Card makes the card more suited for everyday spending than the Venture X. The latter has the potential to earn up to an eye-popping 10x on travel, but you’ll have to book that travel through the Capital One portal. The card earns a respectable 2x on everything.

With the Chase Sapphire Preferred® Card you’ll earn 3x points on dining, including delivery services and takeout; streaming services; and online grocery purchases. If your spending habits sync with the Sapphire Preferred’s rewards structure, you’ll be able to effortlessly rack up points to pay for your next vacation.

🤓Nerdy Tip

By adding another no-fee card or two to your wallet, you can create a Chase Trifecta and supercharge your Ultimate Rewards® earnings. The Chase Freedom Flex℠ earns 5x up to $1,500 per quarter in rotating bonus categories when you activate (1x on everything else), plus 3x at drugstores.

Points worth 25% more

As major card issuers, both Chase and Capital One have their own travel portals through which cardholders can book flights, hotels and car rentals. However, Chase’s Ultimate Rewards® travel portal offers slightly better value. Points are worth 1.25 cents each when used to book through Chase while one Capital One mile is worth 1 cent.

Who might prefer the Capital One Venture X Rewards Credit Card

You want lounge access

True to its classification as a premium travel card, the Venture X grants its cardholders and two guests unlimited access to more than 1,000 airport lounges including Priority Pass lounges and Capital One lounges.

If you want lounge access but prefer Chase’s lineup of credit cards, your only option is the $550-annual-fee Chase Sapphire Reserve®.

You like Capital One’s travel portal

Booking travel through Capital One’s portal is the best way to offset most of the Venture X’s annual fee. Cardholders will receive a $300 annual credit toward travel expenses, which can be used in a single transaction or across multiple purchases. If you don’t mind booking through the portal, the $300 credit plus the 10,000 anniversary points you’ll get each year you renew (worth $100) will cover the entire annual fee of the card.

The Chase Sapphire Preferred® Card offers an annual credit, too, but it’s $50 and only good for hotel bookings through the Ultimate Rewards® portal.

You want trusted traveler program credit

Skipping the line in a crowded airport can be a huge perk, and Capital One Venture X Rewards Credit Card cardholders get a $100 credit for Global Entry or TSA PreCheck. The Chase Sapphire Preferred® Card offers no such reimbursement. Note, though, that you must pay for the Global Entry or TSA PreCheck fee with the Venture X card, and the $100 credit renews every four years, not annually.

Which card should you get?

The Chase Sapphire Preferred® Card, with its reasonable annual fee, top-tier travel partners and access to Chase’s travel portal, is the perfect entree into the world of travel credit cards. Plus, the $95 annual fee can be partly recouped by redeeming the hotel travel credit. Only if you’re after luxury perks and are comfortable paying a triple-digit annual fee should you commit to the Capital One Venture X Rewards Credit Card.

Are you wanting to invest in the stock market but don’t know where to start? You’re not alone. Buying stocks online is a simple process. But doing the research can be a bit overwhelming if it’s your first rodeo. But don’t fret. Read on for a step-by-step guide on how to buy stocks.

Mastering the Basics: A 4-Step Guide to Buying Stocks for Beginners

Embarking on your stock trading journey can be both exciting and overwhelming. With this concise 4-step guide, we’ll help you navigate the essentials of stock trading, from setting up a brokerage account to making informed decisions on stock purchases.

Step 1: Set Up a Brokerage Account

To buy stocks, you’ll need to apply for a brokerage account. With an online brokerage account, you can transfer funds into your account electronically from a linked bank account to fund any future investment orders. And upon making a purchase the stocks will remain in the account until you trade them.

Types of Brokerage Accounts

The basic types of brokerage accounts are:

Discount Broker

Common amongst online brokers

Similar to a do-it-yourself option with limited support

Minimal fees and commissions

Some don’t have a minimum deposit requirement

Full-Service Broker

Designed to help investors from start to finish with planning and execution of trading goals

Offers extensive support from financial advisers at brokerage firm

Commission or fee-based structure

When analyzing brokerage firms, you want to consider the following:

Minimum deposit requirement: if you’re just starting out, you may only want to invest a small amount to get your feet wet. Once you’re acclimated with buying and selling stocks online, you’ll beef up your stock portfolio. But until you reach that point, a discount brokerage with minimal fees and little to no deposit requirement may be best.

Short term goals: do you plan to hit the ground running? Do you need all the support you can get to maximize your investment in the shortest amount of time possible? If so, a full-service brokerage may be the better choice.

Some of the most popular online brokers include Ameritrade, Charles Schwab, E*Trade, Fidelity, Merrill Edge, Robinhood, and Vanguard.

Direct Stock Purchase Plan

Some publicly-traded companies also offer a direct stock purchase plan (DSPP), which allows you to buy stock from them. This is another way to buy stocks that require using online brokers. Instead, the company’s transfer agent manages the transaction.

Check Out Our Top Picks for 2023:

Best Online Stock Brokers for Beginners

Step 2: Evaluate Your Options

There are tons of individual stocks to choose from. So how do you narrow down your options and select the best fit for your financial situation? You can sift through mountains of financial data inundated with jargon you’ve never seen a day in your life.

A better idea: think about industries or businesses you have a keen interest in. Are there a few that you’d like to own a piece of? If so, start there. Otherwise, you can always ask your financial adviser for data on up-and-coming companies or pay attention to market trends in the media.

Get a Copy of the Annual Report

Once you have a list of top prospects, head on over to the company’s website and download a copy of the annual report. It’s an extensive document that provides an overview of how the company performed in the last year, along with detailed financial reports.

The U.S. Securities and Exchange Commission (SEC) mandates that public companies provide this report to shareholders on an annual basis.

But it’s usually available through the company’s website as well for the public to see. If you’re unfamiliar with any of the terms listed, the broker’s website should have information and resources that can assist.

Monitor the Company’s Performance

You may also want to consider monitoring the company’s performance before making a purchase decision. Steep fluctuations or signs of declining revenues could indicate that it may not be the right time to invest.

(Most brokerage firms will also offer tools and resources to help you stay on top of what’s going on with the companies you’re considering).

Step 3: Get a Quote

You’ll want to pay close attention to the information presented in the quote. Stock quotes, which are represented by ticker symbols that are abbreviations of the company, include:

Bid: highest price per share a buyer wants to pay per share

Offer or Ask Price: lowest price per share a seller will accept per share

Historical information on trading volume

Interactive resources to help gauge projected performance

Contact your online broker to learn more or visit Nasdaq.com to retrieve a real-time quote.

Step 4: Place an Order

Now that you’ve gotten all the technical/admin duties out of the way, it’s time to buy stock. But before you get too excited, it’s important to familiarize yourself with order types.

Market Order

A market order ensures you get the amount of shares requested, even if the asking price is a bit higher than your bid. This is usually the case when your primary concern is the share volume and not stock price.

This type of order is best for investors who are in it for the long haul. Why so? Well, a slight spread, or the difference between the asking price and bid, shouldn’t make that much of a difference over time.

Let’s say you want to buy 75 shares at $150 and the quote states:

Bid: $149 (75)

Ask: $150 (60)

Last: $151 (100)

If the seller agrees to issue 75 more shares at $153, your market order will be for 60 shares at $150 and 15 at $153.

Limit Order

A limit order ensures the broker purchases shares at the desired price point. So there’s a possibility you may not receive the number of shares you want until the price point decreases.

Let’s say you want to buy 80 shares at $160 and the seller is only offering 45 at that price point. If you decide to execute a limit order, you would get 45 shares and wait for sellers offering at least 35 or more shares at $160 to reach 80 shares.

No Guarantees

When you place a limit order, understand that there are no guarantees your order will be filled since market orders are executed first.

If it takes several rounds of trading to get the desired volume of shares, expect a hefty amount of broker fees because commissions are tacked on after each transaction.

In this case, it may be in your best interest to execute a market order and pay a bit more per share since the cost of commissions may wipe out the cost-savings per share of stock.

AON Limit Orders

You should also be mindful of all-or-none (AON) limit orders, which indicate to the seller that you’ll only purchase if the price is at or below the amount of your bid. Furthermore, the requested amount of shares must be offered during that specific bid.

If you want to leave the order on the table for an extended period of time, it can be coded as good till canceled (GTC). The timeframe can span from a few to several months.

Stop Orders

Stop orders are driven by price and are only filled when the requested amount of shares reaches the stop price. There are two types of stop orders you should be aware of:

Stop-limit order: functions like a limit order because it’s only executed at the “stop-price”. However, you may not get the number of shares you want.

Stop-loss order: functions like a market order, but the primary difference is the entire order will only be filled when the price is at or below the “stop level”.

How many shares will you be purchasing?

Before you can execute a market or limit order, you’ll need to decide on the number of shares you wish to purchase. There’s no right or wrong amount, and some newbies prefer to start small and scale up once they’re a bit more comfortable with how stock trading works.

The Next Steps

Kudos to you on your first stock purchase. It’s a great first step toward building wealth and helping secure your financial future.

And even if your first round doesn’t turn out as planned or your experience steep market downturns, don’t throw in the towel right away. Remember why you started and focus on the light at the end of the tunnel, or your future earning potential.

If you are unsure of which stocks to pick, you might want to consider buying mutual funds or ETFs.

Best Online Brokers and Trading Platforms for Buying Stocks

The best online brokers offer low commissions and fees, and great research tools, such as charts and stock screeners. You will also want to choose a brokerage platform that is easy to use and intuitive.

Good customer service is also essential when considering an online brokerage account. Check to see if the broker offers phone and email support, as well as live chat. Here are some of the most popular brokers to look into:

Robinhood is a good choice for buying stocks with zero commissions. It offers a simple mobile app with a limited selection of commission-free ETFs and no-transaction-fee mutual funds.

Charles Schwab offers a comprehensive trading platform with powerful research capabilities. You also get access to a wide variety of financial products, and Schwab offers 24/7 customer service.

Fidelity offers comprehensive research and market analysis tools, low trading fees and commissions, and a dedicated customer service team.

With E-Trade, you can easily invest in stocks and other financial instruments online or on your mobile device. They also offer advanced trading tools and charting.

How to Buy and Sell Stocks FAQ

How do I buy and sell stocks?

You can buy and sell stocks through a stockbroker or online trading platform. A stockbroker can help you with the purchase and sale of stocks and provide advice on the best investments for your portfolio. If you decide to use an online trading platform, you’ll need to research and choose one that best meets your needs.

What is the best way to buy stocks?

The best way to buy stocks is to do your research and learn about the different stocks and companies you’re interested in. Then, choose the ones that best fit your investment goals and risk tolerance.

You should also consider the fees associated with trading and the terms of the broker you plan to use when making your purchase. Additionally, it is important to practice patience and discipline to avoid making rash decisions.

How do I choose which stocks to buy?

When choosing which stocks to buy, you want to consider a variety of factors. You should look into the company’s financial health, its competitive advantage in the market, its management team, the industry it operates in, and its earnings potential.

Additionally, you should consider your own financial goals, risk tolerance, and investing timeline. Before you start buying stocks, it is important to do your own research. You may even want to consult a financial advisor to ensure that the stocks you are considering are appropriate for your individual financial situation.

What is the risk associated with investing in stocks?

Investing in stocks carries a certain level of risk, as the stock market can be volatile and movements in stock prices can be unpredictable. It’s critical to understand that stocks have the potential to both increase and decrease in value.

What are the costs associated with buying and selling stocks?

The costs associated with buying and selling stocks include commission fees, taxes, and any other applicable fees. Depending on the broker, commissions can range from a flat fee to a percentage of the total trade value.

Taxes, such as capital gains taxes, may also be applicable when selling stocks. Other fees such as account maintenance fees, custody fees, and margin interest may also be applicable.

How old do you have to be to trade stocks?

You must be at least 18 years old to open a brokerage account and trade stocks in the United States. However, some brokers, and in certain states, you need to be at least 21 years old to trade stocks.

How much money do I need to start investing in stocks?

The amount of money needed to start investing in stocks will depend on the types of stocks you plan to buy and the amount of money you are comfortable investing. Generally, you should expect to start with at least $1,000. However, some online platforms require a minimum of $500 or less.

How much money can I make from investing in stocks?

The amount of money you can make from investing in stocks depends on the types of stocks you invest in, the amount of money you invest, and the success of your investments. It’s important to remember that stock investing can also result in losses as well as gains.

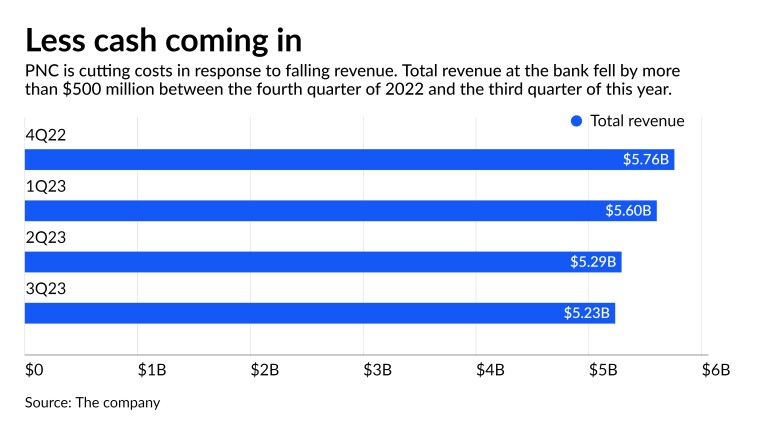

Amid falling revenue, PNC Financial Services Group said it will trim 4% of its workforce to curtail costs by $325 million and prop up its profitability in 2024.

The $557 billion-asset bank’s executives said during a third-quarter earnings call Friday that PNC initiated the staff cuts earlier this month in response to lower lending activity and declining interest income. Total revenue of $5.3 billion was down $60 million from the prior quarter and down $316 million from a year earlier.

The Pittsburgh-based bank had acknowledged earlier this week that it was cutting jobs. But it left many of the details of the plan, which will span PNC’s geographic footprint and business lines, for its earnings presentation and call on Friday.

“What’s new is basically dropping the run rate related to personnel and just tightening the ship in what is a tougher revenue environment,” CEO Bill Demchak told analysts on the call.

The projected savings, which amount to about 2% of PNC’s expected 2023 expenses, are projected to drop to the bottom line next year. They will come on top of $400 million-$450 million of savings from an annual “continuous improvement program” that was already underway, PNC said.

In July, the bank initiated a round of layoffs in its mortgage and home equity divisions. Home lending is under heavy pressure across the industry after mortgage rates more than doubled over the past two years.

In total, PNC is targeting $725 million of 2024 expense cuts, though the layoffs will necessitate a $150 million one-time charge in the fourth quarter.

The cuts will likely boost PNC’s bottom line next year, but its fourth-quarter earnings will be adversely impacted by the staff reduction charge, Autonomous Research analyst John McDonald wrote in a note to clients.

Meanwhile, Raymond James analyst Michael Rose lowered his 2024 earnings per share projection for PNC. He cited a belief that the bank’s net interest income and fee income will be lower than previously expected, and that its credit costs will be higher than previously projected, as factors offsetting the bank’s cost savings.

Rose estimated operating earnings per share of $13.45 for this year and $12.65 for 2024. Still, he maintained his “market perform” rating on PNC’s shares.

PNC Chief Financial Officer Robert Reilly explained the expense reductions by saying that 11 Federal Reserve interest rate hikes since early 2022 have taken a toll on bread-and-butter interest income and pushed up funding costs.

The trends crimped PNC’s net interest margin, which declined by eight basis points from the second quarter to 2.71%. The bank’s net interest income declined by $92 million, or 3%, from the prior quarter.

Third-quarter loans were down 2% from the prior quarter and averaged $320 billion, as more commercial borrowers moved to the sidelines amid the lofty rates.

Deposits were down 1% to $423 billion, even as PNC paid up for funding. The rate the bank paid on interest-bearing deposits increased to 2.26%, up from 1.96% for the prior quarter. That trend more than offset gains on loan yields of 18 basis points in the quarter to 5.75%.

PNC started 2023 with about 61,500 employees. It said the layoffs would be nearly completed by the end of this year.

“While decisions involving personnel are never easy, we believe they will help us more effectively and efficiently deliver for our customers and stakeholders, and we’ll continue to be diligent in our expense management going forward,” Demchak said.

Reilly emphasized that, following the July cuts, every expense category in the third quarter remained stable or declined from the second quarter. Overall noninterest expense of $3.2 billion was down 4%. Still, with no end in sight to high rates, more actions were needed to keep costs in check next year, he said.

“The current environment poses meaningful pressures,” Reilly said. “As a result, we took a hard look at our organizational structure and identified opportunities to operate more efficiently through staff reductions.”

PNC reported third quarter net income of $1.57 billion, or $3.60 per share. That was up from $1.5 billion, or $3.36, for the prior quarter but down from $1.64 billion, or $3.78, a year earlier. Analysts polled by FactSet Research Systems were expecting third quarter earnings of $3.10 per share.

Inside: Looking for a job that pays at least $25 per hour? This list has the best jobs that fit that description. Each job offers unique benefits and opportunities, so take a look and see if any of them match your interests and skills.

Making $25 an hour is not a pipe dream; it’s a viable reality for thousands of people worldwide.

Earning such an income not only instills a sense of financial well-being but also provides a robust platform to plan for the future.

Today, we dive into elucidating the different opportunities potential jobs offer, aligning your skills and experience with an hourly rate that feels just right for your wallet.

Hence, securing such a job is not a function of luck but more a strategic alignment of skills, passion, and industry demands. But if you’re not entirely sure about where to begin or how to hone your skills for these high-paying jobs, don’t worry.

Imagine earning smooth entry-level jobs 25 an hour, all from the comfort of your workspace. Sounds enticing, right?

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

Best Jobs That Pay $25 an Hour

This section will highlight various professions across distinct fields that provide such a desirable pay rate.

Looking for jobs that pay $25 per hour? We’ve got you covered.

Whether you’re transitioning careers or just starting, this list could help you discover a role that fits your skills and experience.

1. Paralegal

A paralegal role is an excellent job choice due to the vast knowledge gained in the field of law and legal procedures.

Being a paralegal involves a variety of interesting tasks, such as helping lawyers prepare for hearings, trials, and corporate meetings.

This position is not solely monetarily advantageous, it also presents opportunities for growth and professional development in the legal sector.

Earning Potential: It offers rewarding prospects with an average pay of $25 per hour, with the potential to earn up to $40 an hour depending on experience and expertise.

2. Landscaper

Why toil in a stuffy office when the great outdoors can be your workspace? Relish the satisfaction of planting, pruning, and mowing yourself into a healthier, happier lifestyle.

Ideal for nature enthusiasts and people persons out there, landscaping combines green-thumbed work with personnel management. A knack for the outdoors and previous work experience will be your stepping stones, while a certificate in grounds maintenance can make your application stand out.

Start by volunteering in your local community gardens or offering your services to neighbors. Through this, not only will your skills blossom, but your resume will flourish, too.

Earning Potential: You can expand your lucrative landscaping journey by owning your own company and training others to be laborers.

3. Truck Driver

Why is it a top-tier job, you ask? Consider this: truck drivers are the beating heart of global commerce, pivotal figures in ensuring warehouses stay stocked and goods reach their desired destinations. Plus, you’re free of the traditional office environment.

This job is perfect for those who prefer to work alone as well as those who prefer delivery routes that often stretch into the night.

You must be over the age of 21 years old and able to pass a CDL exam. Many truck drivers to a training course to get a jumpstart in the industry.

Earning Potential: Many truck drivers start their own company and will employ a couple of rigs to make passive income.

4. Social Media Marketing

Do you have a knack for creating engaging captions or a Sherlockian eye for data? Then Social Media Marketing could be your calling.

This position, hot in demand and rewarding, calls for creativity and analytical prowess.

Why is it a top job? Well, it’s not for the adrenaline rush of its fast pace. It’s the fact that you get to put your tech-savviness to great use. Social media marketers nurture and grow brands through smart strategies and engaging content.

Earning Potential: Many people start working for someone else as a Social Media Coordinator and then go on to open up their own business.

5. Event Planners

As an event planner, you are the unseen forces behind flawless galas, memorable weddings, and standout corporate functions. If you thrive on creativity, organization, and people skills, you will ensure that each event is meticulously executed.

This role allows you to blend creativity with pragmatic decision-making: from the captivating process of selecting venues, and coordinating with caterers

It’s a dream job for you if you love putting smiles on people’s faces and making their day unforgettable.

Earning Potential: An enticing reason is its attractive pay rate: on average, $24-28 per hour, peaking up to $40, with the potential of a quick pay raise. Plus those lucrative tips!

6. Mechanical Technician

If you’re seeking a rewarding, high-paying role that gets you hands-on with varied machinery, then a Mechanical Technician career.