Well now that the Super Bowl is over, it’s time to look forward toward spring and the rest of 2013.

The holidays have passed and now many individuals are determining what their financial goals are for the year.

Is this the year to finally sell a home, buy a home, or just continue to sit tight?

While all those questions may have different answers, depending upon your current position, it’s clear that it’s a seller’s market right now.

It’s not a traditional seller’s market, largely because most homeowners don’t have much home equity, but the current environment does favor sellers because inventory is just so tight.

There’s also voracious demand at the moment, thanks to the perception that the worst is now behind us, and that if you buy in now, you’ll get a cheap home with an even cheaper mortgage.

Unfortunately, this herd mentality often precedes a bubble, that is, an unwarranted surge in price before a sudden and dramatic correction.

Housing Bubble Part Deux?

So, are we in for more trouble, now that seemingly every pundit, analyst, government official, interested party, and American is in on the supposed recovery?

The few who believe we are in for another bubble basically think the Fed created artificial demand for housing by pushing mortgage rates to new record lows, via quantitative easing like QE3.

It’s hard to argue with that fact – mortgage rates did indeed fall to unprecedented levels, and with that seemed to come a newfound demand for housing.

But even though demand is up, home sales are still lower than they have been historically.

All the recent “killer numbers” are only good, or improved, relative to the preceding dismal years.

And one could argue that home prices are on the mend because they’re cheap, not because rates are low. After all, plenty of recent sales have gone to cash buyers who could care less about rates.

If you look at the historical relationship of home prices and mortgage rates, it’s not what you’d think.

There’s not much of a correlation, and higher mortgage rates could actually come with higher home prices as a result of an improving economy.

It’s not as if the moment rates rise home prices will plummet, though the current situation is a little unprecedented.

Additionally, home prices are only up from the “bottom,” and nowhere close to fully recovered, assuming they eventually match the prices seen during the previous bubble, which history tells us they will.

In other words, inventory shortages and low prices are the real driver of demand at the moment, not necessarily low rates.

The low rates are more a boon to those looking to refinance their now expensive mortgages, not reason alone to purchase a home.

Housing bears also believe unemployment will continue to hinder a real recovery, and that there just aren’t any real buyers, only speculators.

The reasoning here is that there aren’t any first-time homebuyers because the economy is in the dumps, and there aren’t any move-up buyers because existing owners don’t have equity.

I think this is a convenient way of summing things up, but doesn’t represent reality. There are plenty of individuals who “missed” the first bubble, and have been patiently waiting to get in this time around.

There are also millions of existing owners with plenty of equity that want to buy again, especially at much lower prices.

What About Mortgage Quality?

To further argue against another housing bubble, the quality of mortgages this time ‘round is night and day.

Can you really compare a 30-year fixed at 3.5% to an option arm with a 1% teaser rate, which after five years, will reset to a fully-indexed and variable rate of 6% or higher.

Or a more straightforward interest-only ARM that becomes fully amortizing (and fully indexed) after 10 years, pushing a homeowner to the brink of default?

Oh, and those types of loans were also taken out at the height of the market, making mortgage payments that much more unsustainable.

Today, borrowers are taking out mortgages they can truly afford, with more skin in the game and no surprise resets in the future. Surely that will make for a more bubble-resistant housing market going forward.

But don’t be surprised if there are some hiccups along the way, because there will always be ups and downs.

Inside: Are you looking for an affordable budgeting app that offers a range of features? YNAB may be the perfect choice for you! This guide will compare YNAB vs Mint, highlight their key features, and help you decide which is best for your needs.

Are you trying to make a choice between Mint and YNAB for managing your financials?

Here’s a comprehensive overview that would definitely point you in the right direction.

Both Mint and YNAB have proven to be efficient and reliable online budgeting tools, but their offering varies in some aspects.

While Mint shines with its free budgeting tools and comprehensive credit score and report management capabilities, YNAB stands distinguished with its robust features and specialist credit management options, making it worth its fee for some users.

Herein, we dive into the similarities, differences, and unique functionalities of both platforms to help you decide which one best aligns with your financial management needs and lifestyle.

As a finance expert, I’ve seen both YNAB and Mint apps work wonders for different people.

In my opinion, both have unique value. Novices may find Mint’s overview helpful, while more determined budgeters might prefer YNAB.

Remember, it’s perfectly fine to use both if it aids your long-term money management.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What is YNAB?

YNAB is a budgeting software I’ve utilized that provides detailed financial tracking and education for effective money management. Also, known as you need a budget app.

Adhering to its unique Four Simple Rules for Successful Budgeting, every dollar is assigned a specific task. YNAB operates via an online account or a mobile app, involving color codes and features like ‘The Inspector’ for efficient budget overview. However, it’s important to note that YNAB caters only to the zero budgeting style and charges a monthly subscription fee.

This is a great budgeting method as it gives you a cash flow budget plan for your money.

Overall, YNAB helped me gain control over my finances by setting realistic goals, getting one month ahead on bills, and focusing on each dollar’s purpose.

What is Mint?

Mint is a free, all-in-one finance platform owned by Intuit that can be used to easily manage my money.

It links all accounts in one place for easy tracking and includes features such as budgeting, credit score monitoring, and bill tracking.

For instance, Mint categorizes transactions, monitors changes in my credit score, and sets up budgetary limits.

With over 30 million users, Mint is a leading free tool in personal finance management.

A step up from Mint would be Intuit’s Quicken platform or Simplifi budget app.

Comparison of YNAB and Mint Apps

Mint is a comprehensive, free budgeting app, that provides an overall view of your finances. It links to your accounts, tracking and categorizing spending, while also offering savings tips. Conversely, YNAB, a paid app, focuses on giving users control over budgeting. It will link to your accounts and encourage a proactive role in handling finances.

These are two of the budget apps available on the market.

In my opinion, if you’re seeking an easy-to-use app offering a holistic view of your spending and savings, Mint is a perfect choice. However, if you’re looking for a stringent budget management system with more control, YNAB is worth the investment.

Kristy @ Money BLiss

1. YNAB vs Mint: Features

YNAB and Mint are both renowned budgeting apps, but they possess some notable differences.

While both support account linking, goal setting, and spending tracking, Mint pulls ahead with its investment and credit score tracking features.

YNAB distinguishes itself with a forward-thinking, zero-based budgeting strategy and benefits like manually adding transactions. Think budget by paycheck style.

From the ease of use standpoint, both are equally user-friendly.

2. YNAB vs Mint: Budgeting Snapshot

YNAB offers a rigorous, manually updated budgeting snapshot that employs a zero-based budgeting philosophy. This feature provides a detailed outlook, encouraging users to assign every dollar a job.

On the other hand, Mint has an automated tracking system that offers an all-in-one snapshot of all financial accounts and spending categories.

Mint integrates your accounts, offering useful tips and an overview of your finances. Conversely, YNAB requires a manual categorization of income and expenses but affords more budgeting control. Similar to using the ideal household budget percentages.

The budgeting snapshot in Mint is best suitable for individuals seeking a hands-off approach, while YNAB is ideal for those who prefer an in-depth, hands-on budget strategy.

A great way to move digital from your budget binder with envelopes.

3. YNAB vs Mint: Goal Setting

The Goal Tracking feature in YNAB allows users to set various budgeting goals such as saving targeted amounts of money or conversely working towards getting out of credit card debt. This in-built functionality provides a structured pathway for users to stick to and pursue their financial objectives effectively.

Your interaction with your YNAB account through the goal-tracking tool ties back to YNAB’s four Simple Rules for Successful Budgeting, aiding in fiscal responsibility.

This innovative feature assists individuals in staying focused on their planned budgets, ensuring they are empowered to make strides toward their unique financial goals.

Mint however doesn’t offer this feature.

4. YNAB vs Mint: Interface

While YNAB is ideal for meticulous budgeters prioritizing forward planning, Mint is perfect for those seeking an easy-to-use, comprehensive glimpse of their financial standing.

YNAB’s interface is focused on budgeting, featuring tools for expense tracking, goal setting, and manual transaction input.

In contrast, Mint offers a comprehensive overview of your financial health, automatically categorizing expenses, tracking investments, and offering set-up alerts.

5. YNAB vs Mint: Categorization

Mint offers automated categorization of transactions, which eases the process of budgeting for the user. However, it doesn’t allow the removal of default categories, and the addition of new ones might take time due to server communication.

On the other hand, YNAB allows a deeper level of categorization, with an option to visually nest categories, and more effortless editing of these categories.

In my opinion, Mint’s categorization feature suits a casual budgeter looking for automation, while YNAB would be ideal for those desiring granular control over their personal budget categories.

6. YNAB vs Mint: Mobile App & Cross Platforms

Both YNAB and Mint offer comprehensive personal finance management via mobile apps, compatible with iOS, Android, and desktops.

YNAB stands out with its Apple Watch integrations and a slightly better syncing experience based on user reviews on Trustpilot1.

YNAB also syncs across a desktop app as well.

7. YNAB vs Mint: Alerts

Mint provides a wide selection of alerts, including low balances, upcoming bill payments, over-budget warnings, ATM fees, and unusual expenditure notifications.

These comprehensive alerts from Mint give a more thorough financial pulse check but can be overwhelming for some.

On the other hand, YNAB recently added live push notifications based on your preferences.

8. YNAB vs Mint: Syncing

YNAB leads the game when it comes to synchronization, outshining Mint. While Mint supports numerous banks, issues with synchronization often lead to grievances among its users. YNAB, on the other hand, offers smoother syncing and fewer complaints, proving its superiority.

Many users find YNAB’s syncing consistent and reliable.

Personally, I believe that if you prioritize seamless syncing and don’t mind spending $14.99 a month, YNAB becomes a clear choice.

However, if you’re okay with potential sync issues and prefer free usage, Mint could be more suitable.

It’s crucial to pick according to your priorities and needs.

9. YNAB vs Mint: Savings Accounts

Mint offers automatic expenditure tracking and classifies my spending into categories, providing a comprehensive view of where my money is going.

YNAB, on the other hand, empowers me to manually budget my net income each month, ensuring I don’t overspend and promoting a proactive approach to saving.

10. YNAB vs Mint: Investment Tracker

Mint offers investment tracking features, allowing users to view their investment portfolio and monitor performance.

In contrast, YNAB lacks this feature, not providing any investment tracking at all.

As a user, if you highly prioritize tracking investments in one place, you may lean towards using Mint. Conversely, if investment tracking is less important to you than budgeting, YNAB’s strong budgeting emphasis, despite its lack of investment tracking, makes it a considerable option.

11. YNAB vs Mint: Learning Curve with your Finances

YNAB has a steeper learning curve, necessitating a proactive approach to money management by assigning every dollar a purpose. Thus, YNAB gives you a free 34-day free trial to understand how to use the app.

Mint, however, requires minimal user input post-account linkage and auto-categorizes your spending. For sheer ease of use, Mint might appeal to novices looking for automated budget tracking.

On the other hand, users wishing to take charge of their finances might appreciate YNAB’s proactive, behavior-altering approach. Despite having a steeper learning curve, YNAB offers an abundance of online tutorials and customer support, making the learning process manageable and rewarding.

The same is true when you are learning to use the biweekly budget template.

12. YNAB vs. Mint: Data Security

Data security is a paramount concern when utilizing online budgeting apps as they deal with sensitive financial information.

Apps like YNAB and Mint incorporate stringent security measures to protect user data.

For instance, YNAB uses a one-way salted and hashed password system and data encryption.

Mint, on the other hand, employs two-factor authentication and a Touch ID sensor for iOS for enhanced security.

Nonetheless, it’s important to note that while these apps provide bank-level security, Mint does anonymize and sell user data to advertisers.

13. YNAB vs Mint: Advertising

YNAB derives income primarily from subscription fees offering an ad-free experience, holding a straightforward revenue model. In contrast, Mint generates income through affiliate commissions by advertising financial products to users and selling anonymized user data!

Mint, contrastingly, is a free app reliant on ads and sells anonymized user data for third-party advertisements.

From my perspective, if avoiding ads and preserving data privacy matters to you, YNAB’s approach might be more appealing. However, if you prefer a free service and don’t mind the ads, Mint would be suitable.

14. YNAB vs Mint: Customer Support

When evaluating the customer support of Mint and YNAB, it’s evident that YNAB takes a more well-rounded approach.

With a commitment to respond to email queries within 24 hours, YNAB also provides educational resources such as the “get started” class, their blog, and user forums. This is in contrast to Mint, which, despite offering live chat support, has had reports of slow response times.

Both platforms offer online training materials, but YNAB seems more comprehensive and responsive in its support-providing role. Overall, YNAB appears to be the preferred choice when customer support is a primary consideration.

15. YNAB vs Mint: Cost

Mint is a free, ad-supported budgeting app while YNAB is a subscription-based model of $14.99 monthly or $99 annually.

However, for individuals seeking in-depth surgical budgeting capabilities without concerns for associated costs, YNAB’s price might represent a great investment.

Given the claimed average user saves $600 in two months and $6,000 in the first year.2

For those budgeting with minimal funds, the free price tag of Mint might be more attractive, but you are giving away your privacy.

Pros and Cons of YNAB vs Mint

Our Favorite

Key Features:

YNAB offers a comprehensive approach to budgeting, helping you plan monthly budgets based on your income. It also offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

YNAB’s superior synchronization skills make it the winner in this area. YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners

YNAB provides an option to manually add and upload transactions from accounts each month, a feature that Mint does not offer.

YNAB prioritizes user privacy, requires an opt-in to access budgeting data, and doesn’t sell user data.

Key Features:

Mint offers a centralized platform for monitoring all your financial accounts, including credit cards and bank accounts.

It provides a complete financial overview at a glance through the auto-population of data from linked accounts.

Mint’s features include detailed reporting in multiple categories, free credit score access, and exceptional compatibility with financial institutions.

The service is free, funded by ads and offers, and it best serves those who wish to categorize spending, budget their monthly expenses, and access all financial details from one place.

Lack of investment tracking feature

Customer service is only accessible via email, which might not be ideal for urgent queries

Steep learning curve which requires time and effort to navigate through.

Mint, which belongs to Intuit, automatically accesses all data and sells the data. Thus, an intrusion of privacy.

Budgeting feature doesn’t enable effective planning of future expenses.

Mint suffers from more technical glitches and synchronization issues.

Ads included in the free version of Mint can be obtrusive and may deter users.

$14.99 monthly or $99 annually

Free to Use, But Served Ads and They Sell your Data.

Offers a 100% money-back guarantee at any point of use.

Does not require credit card information to signup, a departure from the usual free trial model)

Our Favorite

Key Features:

YNAB offers a comprehensive approach to budgeting, helping you plan monthly budgets based on your income. It also offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

YNAB’s superior synchronization skills make it the winner in this area. YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners

YNAB provides an option to manually add and upload transactions from accounts each month, a feature that Mint does not offer.

YNAB prioritizes user privacy, requires an opt-in to access budgeting data, and doesn’t sell user data.

Lack of investment tracking feature

Customer service is only accessible via email, which might not be ideal for urgent queries

Steep learning curve which requires time and effort to navigate through.

$14.99 monthly or $99 annually

Offers a 100% money-back guarantee at any point of use.

Does not require credit card information to signup, a departure from the usual free trial model)

Key Features:

Mint offers a centralized platform for monitoring all your financial accounts, including credit cards and bank accounts.

It provides a complete financial overview at a glance through the auto-population of data from linked accounts.

Mint’s features include detailed reporting in multiple categories, free credit score access, and exceptional compatibility with financial institutions.

The service is free, funded by ads and offers, and it best serves those who wish to categorize spending, budget their monthly expenses, and access all financial details from one place.

Mint, which belongs to Intuit, automatically accesses all data and sells the data. Thus, an intrusion of privacy.

Budgeting feature doesn’t enable effective planning of future expenses.

Mint suffers from more technical glitches and synchronization issues.

Ads included in the free version of Mint can be obtrusive and may deter users.

Free to Use, But Served Ads and They Sell your Data.

Who should use YNAB?

From my experience, YNAB works best for those who are ready to seriously manage their money and spend some time learning a new budgeting approach. Its use of the zero-based budgeting system not only makes you more intentional with your money but also demands active participation in decision-making.

YNAB’s ability to link to your accounts and its multitude of educational resources available are admirable features I’ve used.

YNAB offers detailed financial tracking and built-in education, but its monthly subscription fee and suitability for a specific budgeting style may be limiting for some.

However, it comes with a monthly or annual cost – a worthy investment for those searching for a robust, hands-on, and future-focused budgeting tool. Most YNAB budgets agree they save multiples of the subscription cost.

However, it can be less suitable for those not ready for a hands-on approach or those sensitive to subscription pricing.

Who should use Mint?

On the other hand, Mint is an all-in-one app that automatically tracks and categorizes your spending.

Based on my experience, Mint is an excellent tool for novice-level budgeters seeking to track their expenses, set budgets, and manage their finances with ease. This budgeting app allows a comprehensive view of all your financial accounts, which differentiates it from YNAB.

If you’re comfortable seeing ads and not needing investing features, Mint could be a perfect fit. However, if you require the ability to assign multiple savings goals to one account or a bill pay feature, YNAB may be more suitable for you.

Therefore, Mint is most applicable for beginners seeking a free and user-friendly budgeting platform.

YNAB vs. Mint: Which is better for you?

As a content writer and budgeting app user, I find Mint and YNAB are unique in their offerings.

Mint automatically tracks and categorizes your spending, providing an intuitive picture of where your money goes, ideal for beginners in budgeting.

In contrast, YNAB promotes a proactive approach, helping to set and monitor budgets, hence perfect for those with specific financial goals. To sum up, Mint offers a simplified, passive overview, while YNAB is excellent for a detailed, forward-thinking approach to managing finances.

Personal preferences and needs really influence the choice here. Do you need intricate control and don’t mind paying a fee? YNAB might be your fit. Prefer automation and want a free option? Mint could work for you.

YNAB vs Mint: Verdict

As an expert in personal finance tools, I’ve explored both YNAB and Mint.

In my experience, there are distinct differences between YNAB and Mint. For my readers, I recommend YNAB.

YNAB, with its laser-focused approach towards budgeting, is a boon for individuals needing extensive assistance in the budgeting arena. You learn to assign every dollar with intention, thereby gaining a higher degree of control over your finances.

This proactive approach will help you to be financially independent faster.

To sum up, if detailed budgeting is your priority, choose YNAB.

YNAB

Enjoy guilt-free spending and effortless saving with a friendly, flexible method for managing your finances.

Pros:

Comprehensive approach to budgeting, helping you plan monthly budgets based on your income.

Offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

Superior synchronization skills make it the winner in this area.

YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners.

Option to manually add and upload transactions from accounts each month.

YNAB prioritizes user privacy.

Start 34 Day Free Trial

However, for a more holistic financial insight with less emphasis on budgeting, Mint might be the better choice.

Now, make sure to check out our Quicken Review.

Source

TrustPilot. “YNAB Review.” https://www.trustpilot.com/review/ynab.com. Accessed on September 27, 2023.

YNAB. “YNAB Pricing.” https://www.ynab.com/pricing/. Accessed on September 27, 2023.

Know someone else that needs this, too? Then, please share!!

Though FICO® and VantageScore® ranges start at 300, most new credit users don’t start this low. In fact, if you’ve never taken out credit or applied for a loan, you might not have a credit score at all.

When applying for credit cards and loans, you begin to build credit, but you may be wondering—what does your credit score start at? Most people’s initial credit scores are between 500 and 700 points, depending on the steps taken when establishing credit. However, you won’t have a credit score to report if you’ve never opened a credit account.

Read on to learn more about your starting credit score and how to build your credit over time.

What Credit Score Does an 18-year-old Start with?

Contrary to popular belief, you don’t automatically receive a credit score the day you turn 18 years old. However, you need to be at least 18 years of age to apply for credit and start building your score. Remember that if you haven’t used credit yet, you likely won’t have a score at all.

Once you start using credit, you will get a score roughly three to six months after opening your first credit account. Your credit score will be calculated based on a variety of factors outlined in the next section.

How Are Credit Scores Calculated?

So, how are credit scores determined if everyone doesn’t receive the same default credit score? According to FICO, they use the following five factors to calculate your credit score:

Payment history: The most important factor to determine your credit score is your history of paying credit accounts on time.

Accounts owed: While owing money on credit accounts isn’t necessarily bad, using a majority of your available credit can lead to lenders viewing you as higher-risk.

Length of credit history: Generally, the longer your credit history, the better it is for your score since lenders have a more accurate assessment of your risk.

Credit mix: The different types of credit you have, such as credit cards, installment loans, and finance company accounts, are your credit mix.

New credit: Opening too many credit cards in a short period of time can hurt your score since doing so signals to lenders that you’re a greater risk.

How to build credit

If you’re new to credit, you may be wondering how to start building your credit in the first place. Receiving a loan without a credit score might be difficult, so FICO suggests the following ways to start building credit:

Become an authorized user on a family member’s credit card. You can be added to a card owner’s account, which allows you to make purchases with their credit card. Keep in mind that this method doesn’t have a large effect on your score but can be a good stepping stone to building credit.

Apply for a secured credit card. As a person with no credit, your risk to lenders is considered very high. A secured credit card requires you to pay a refundable security deposit to mitigate risk.

Report rent and other service providers. Credit and loans aren’t the only factors that affect credit. While landlords and utility companies typically don’t report to the credit bureaus, you can request that they do so to start building your credit.

How long does it take to build a 700 credit score?

According to FICO, a credit score of 700 or above is considered good. And since the national average credit score is 716 as of April 2022, it certainly is achievable, although it will take time. If you’re starting with no credit, you can expect building a 700 credit score to take at least six months of practicing positive credit habits.

Keep in mind that there are steps you can take to increase your initial credit score and reach your credit score goal of 700 or higher credit.

How to improve your initial credit score

So, how can you help make sure that you start out with a good credit score? Follow the tips below to improve your credit score.

Review your credit report. Once you open a credit account, be sure to view your credit report and look for any inaccuracies.

Be on time with your payments. Since payment history is the most important factor that influences your credit score, be sure to pay your bill on time and avoid missing payments.

Limit applying for multiple lines of credit in a short period of time. Applying for credit results in a hard inquiry, which may slightly lower your credit score. Too many of these hard inquiries in a short period of time can cause your credit score to drop.

Keep your credit utilization ratio under 30 percent. Credit utilization refers to the amount of credit you’re using divided by the amount that is available to you. For example, if your monthly credit limit is $1,500, aim to use under $450 each month.

Be patient. Again, the length of credit history is an important factor that contributes to your credit score. The more time that passes since you opened your account, the better for your score.

FAQs

Below, we’ve answered some common questions regarding your first-time credit score.

Does your credit score start at 0?

Your credit score doesn’t start at zero. In fact, the lowest credit score possible is 300. However, you likely won’t start at this score unless you’ve made actions that have damaged your credit score.

Does everyone start with the same credit score?

Everybody doesn’t start with the same credit score. As mentioned above, your individual credit score is based on a number of factors.

Is no credit worse than bad credit?

No credit means you lack a credit history, whereas bad credit means you’ve made credit-damaging mistakes, such as multiple late payments. While both scenarios can cause limitations, building credit from scratch is generally easier than rebuilding a bad credit score. As a result, it’s worse to have bad credit than no credit.

What’s a good credit score for young adults?

A good credit score is 670 and up. According to Experian®, the average credit score for young adults ages 18-25 is 679, so any score above that is considered above average for the age group.

How to check your credit score for free

Once you begin building credit, it’s crucial to follow responsible financial practices that will help you raise your credit score over time. And don’t forget to regularly monitor your credit to make sure you’re on the right track.

ExtraCredit by Credit.com gives you tools to manage your credit at an affordable monthly price so you have information you need to help you achieve your financial goals. Get started today.

Is your poor credit history preventing you from obtaining your financial goals, such as getting a credit card, buying a car, or purchasing a home? If so, there are steps you can take right now to improve your credit score in as little as three months.

This article provides actionable steps you can take today to start on the path to rebuilding your credit.

In This Piece

How Quickly Can You Improve Your Credit?

The exact amount of time it can take to repair your credit score depends on several factors, such as your current credit score, the amount of debt you owe, your ability to repay your debt, and your overall credit history.

Despite this, you can start making improvements in as little as three months. Below is a look at five things you can do to improve your credit score, along with tips to keep in mind.

1. Pay Off the Debt You Can

Start by paying off as much debt as possible. There are several strategies you can use to pay down your debt, including the debt avalanche method, the snowball method, and a debt consolidation loan. No matter which method you use, the faster you can pay down some of your debt, the sooner your credit can start to improve.

Keep in mind that it could take your creditors up to 30 days to report payments to the credit bureaus and another 30 days for the credit bureaus to post these payments to your account.

2. Minimize Your Credit Utilization

Your credit utilization ratio accounts for up to 30% of your overall credit score. This ratio compares the amount of credit you have available with the amount of credit you’ve used. It’s recommended to keep this ratio below 30%. If you’re having trouble hitting this number, here are some things you can do.

Ask for a Higher Credit Limit

If your credit utilization ratio is above 30%, you can ask your credit card company to increase your credit card limit. This strategy will increase the amount of credit you have available, which can help lower your credit utilization ratio.

Use as Little Credit as Possible

Instead of using your credit card to make multiple or large purchases, consider using another method to pay. The less you have charged to your credit card, the better your credit utilization ratio will be.

Taking these steps to decrease your credit utilization rate could start to improve your credit in as little as 60 days.

3. Keep an Eye on Your Credit Report

According to a recent study, 34% of Americans found at least one mistake on their credit report. Just one credit card error could damage your credit score. This is why it’s so important to keep an eye on your credit report.

You can request a free credit report from all three major credit reporting agencies, Experian, Equifax, and TransUnion, at annualcreditreport.com. Obtaining your credit report is just the first step; you also want to perform the following tasks.

Check Your Report for Errors

Carefully review your credit report to make sure all the information listed is correct, including your personal information and account details. Make a list of any incorrect information and any accounts or personal information that’s missing.

Dispute Inaccurate Information

The best way to remove incorrect information on your credit report is to file a dispute with the credit reporting agency. Write a dispute letter that clearly explains what inaccurate information is listed on your credit report and why it’s incorrect. Submit this letter, along with any supporting documents, to the credit bureaus listing the error.

Typically, the credit reporting agencies have up to 30 days to investigate your dispute and another 5 days to let you know their decision.

Ask if Lenders Will Remove Paid-Off Items From Your Report

Many lenders report past-due accounts to credit reporting agencies to entice customers to pay their debts. Once you pay your debt off, the lender may be willing to remove this debt from your credit report. Contact your lender directly to make this request.

It could take days, weeks, or months to receive a clear answer from your lender. If they do agree to remove this debt, it could take up to 60 days to reflect on your credit report.

How to Add Your Utility Bills to Your Credit Report

Typically, utility companies don’t report on-time payments to the credit bureaus. You can, however, work with a reporting service company, such as Credit.com’s ExtraCredit service, to make sure these payments along with your rent payments are listed on your credit report. This step can help prove you have a strong payment history.

Once you sign up for a credit reporting service, you can expect to see these payments on your credit report within 60 days.

4. Consider Applying for a New Line of Credit

Having a mix of different types of credit accounts, such as revolving credit accounts and fixed-payment accounts, makes up to 10% of your credit score. If you want to boost your credit score, it’s important to have a nice mix of different accounts. Below is a look at some types of credit accounts you may qualify for even if you don’t have good credit.

Are Credit Builder Loans Right for You?

As the name suggests, credit builder loans are designed to help you build credit. This type of loan is different from traditional loans, as you don’t have access to the money until you make all your payments. Obtaining a credit builder loan can be a great way to save money while building your credit because these lenders often report loan payments to the credit bureaus.

Types of Credit to Consider

If you can’t obtain a traditional credit card, there are other options, such as:

Secured credit card. With a secured credit card, you’ll be required to put down a cash security deposit prior to obtaining your card. Otherwise, these credit cards work just like traditional cards and can help you build your credit.

Authorized user. If you can’t obtain your own credit card, you can ask a friend or family member to add you as an authorized user to their account. If the credit card company reports your authorized user status, it can help build your credit.

Tips for Applying for New Credit

While maintaining a mix of credit accounts can help you build your credit, you want to make sure you don’t open too many new accounts too quickly. This action could damage your credit score due to excessive credit inquiries. Instead, take it slow and gradually open a mix of accounts.

Opening just two different types of credit accounts, such as a car loan and a credit card, can impact your credit as soon as they’re reported on your credit report.

5. Keep on Top of Your Finances

Keeping on top of your finances is a very important building block in your credit foundation. Start by building a budget and sticking to it. This step can make sure you don’t overspend, help you start to save money, and learn to be more conscious of how you’re spending your money on credit.

What to Do if You Don’t Have Credit

If you currently have little to no credit, you may be wondering how you can build credit in just a few months. Taking some of the steps above, such as working with a reporting service company, obtaining a secured credit card, or becoming an authorized user, can help you build credit as soon as they are reported.

Knowing how to raise a credit score in three months is just the first step. Now, it’s time to take action.

Has a close friend or loved one asked you to cosign a loan or credit card? You may be tempted to help them out. But does cosigning hurt your credit? Becoming a cosigner may not immediately affect your credit. However, there are many circumstances when this type of financial agreement could impact your credit negatively.

Before you agree to cosign on a credit card, student loan, car loan, home mortgage, or any other credit account, it’s important to understand the advantages and disadvantages of becoming a cosigner and what impact it could have on your credit score.

What Is a Cosigner?

A cosigner is someone who guarantees that they will be legally responsible for paying back a debt if the borrower cannot pay. Some of the best people to cosign are trusted friends or family members with a good credit history and a solid income history.

How a Cosigner Helps

A loved one might ask you to cosign to help them qualify for a loan if they:

Don’t meet the minimum income requirements for a loan

Have no established credit

Have bad credit

Meet the minimum income requirements, but their debt-to-income ratio is too high

Are self-employed

Changed jobs recently or their income is variable

Getting a cosigner only helps, though, if they pay their cosigned loan as agreed. Doing so will help them to build a good payment history, which will also give their credit score a lift.

If they manage their cosigned loan payments responsibly, they can reap the benefits and watch their credit score climb over time.

Get matched with a personal

loan that’s right for you today.

Learn

more

How Cosigning Affects Your Credit

When you cosign a loan, credit card, or other credit account, you’re agreeing to be financially responsible for that loan. This means that if the primary borrower fails to make payments on the account, you’re legally liable for paying the remainder of the debt in full.

Although you’re the cosigner, lenders treat the loan as if it’s yours. Depending on the type of credit account or loan, it could impact your credit utilization ratio, which accounts for up to 30% of your credit score.

Does cosigning on a car loan for a family member affect your credit? Yes, lenders view this new loan as if it were your loan, affecting your credit utilization ratio. Depending on your specific situation, the new loan could lower your credit score almost immediately.

However, if the primary borrower continuously makes on-time payments, being a cosigner could positively impact your credit in the long run.

Does Cosigning Show up on Your Credit Report?

Once you cosign a loan or credit card, it’s likely to show up on your credit report. In fact, the only way the new credit wouldn’t show up on your credit report is if the lender fails to report it.

It’s important to note that most lenders report loans and credit accounts to the credit bureaus. Even if the new account doesn’t immediately show up on your credit report, the lender could report late or missing payments at a later date. If the loan goes into default or collections, this too could be reported on your credit report.

Not only is the new account likely to appear on your credit report, but it’ll show as if it’s your personal loan. Lenders don’t distinguish between your personal loans and those that you cosign.

Does a Cosigner Need to Have Good Credit?

The answer is yes. Lenders treat cosigners just as they do the primary account holder. They want to know that you can financially afford to pay for the loan and have a good credit history. Once you submit the application as a cosigner, the creditor will conduct a hard inquiry on your credit.

Before you agree to be a cosigner, you may want to check your credit score with Credit.com’s Credit Report Card. While each lender has its own credit requirements, most expect a cosigner to have good credit with at least a 670 credit score.

What Are the Disadvantages of Cosigning?

There are numerous risks involved in becoming a cosigner. The most crucial disadvantage is the impact cosigning can have on your credit. Not only can becoming a cosigner increase your credit utilization ratio, but late or missed payments, repossessions, and loan defaults can be detrimental to your credit.

If your credit score drops, you could have trouble securing new credit in the future. For example, you cosign a personal loan for a friend, and this friend stops making payments and defaults on the loan. This could damage your payment history and credit utilization ratio as well as lower your credit score. Depending on the impact on your credit score, it could affect your ability to secure a loan in the future, such as a car loan.

Most importantly, if the primary account holder fails to make on-time payments, it could destroy your relationship.

What Are the Advantages of Cosigning?

The biggest advantage of cosigning a loan is that it gives you the opportunity to help a loved one build their credit. You can also help a loved one reach their personal and financial goals. For example, cosigning a student loan for your child can help them obtain the degree they need for their career.

If all goes well, cosigning a loan may also boost your credit score. First of all, having a mix of credit accounts makes up about 10% of your credit score. If this is a new type of loan, it could help you improve that rating.

Secondly, if the primary account holder continues to make on-time payments, it can help boost your payment history.

Disadvantage of cosigning

Advantages of cosigning

You’re responsible for repaying the loan if the primary account holder stops paying.

You can help a friend or family member build their credit and reach their personal or financial goals.

Late payments, repossessions, loan defaults, and increased credit utilization can negatively impact your overall credit score.

Adding new credit could increase your credit mix, which accounts for up to 10% of your credit score.

Cosigning a loan could impact your ability to secure future credit for yourself, such as a car loan.

If the primary account holder continues to make on-time payments, it could boost your credit score.

Issues with the loan and payments could destroy the relationship between the cosigner and the primary account holder.

How to Remove Yourself as a Cosigner

Once you agree to be a cosigner, removing yourself from the account can be difficult, but not impossible. In almost all cases, you’ll need the primary account holder’s permission to remove yourself as a cosigner.

Some student loans and auto loans offer a cosigner release process. While this can make it easier, securing approval can still be very difficult. However, if the primary account holder has established good credit during the duration of the loan, it may be possible.

If the loan doesn’t offer a cosigner release option, it’ll likely require a new agreement with the lender to remove yourself as a cosigner. If the lender doesn’t agree to this arrangement, the primary account holder can consider refinancing the loan without a cosigner or taking out a consolidation loan. Since these would be new loans, both options will remove you from the cosigned loan.

Does Removing a Cosigner Affect Your Credit?

Removing yourself as a cosigner of a loan will also remove all the data related to that loan. So, if the primary cardholder made consistent on-time payments, removing yourself could actually lower your credit score.

If, on the other hand, that account has several missed or late payments, removing yourself from the loan could help repair your credit.

Questions to Think About

Before you agree to become a cosigner, there are several things you should consider, such as:

Do you have good credit?

Can you afford to take over the payments if necessary?

Do you trust the primary account holder?

Can the primary account holder afford the payments?

Does the primary account holder have a steady employment history?

Why does your loved one need a cosigner?

Are there other options to help your loved one build credit?

Knowing the answer to these questions can help determine if being a cosigner is the right option for you.

What Is Financial Infidelity and Why Does It Matter?

In a survey about how money matters in relationships, we asked both men and women if they’d ever broken up with someone over money. Around a quarter of respondents said they had, while around a fifth said someone had broken up with them over financial matters.

Clearly, financial factors can create friction in relationships—and that’s true whether or not someone breaks up over these issues. According to a poll conducted by the Association of International Certified Professional Accountants, almost 70% of Americans who were married or living with a partner said they’d fought about money with their significant other within the past 12 months.

With money a stressor in relationships, it’s not surprising that financial infidelity sometimes occurs. Find out more about financial infidelity and the role finances play in relationships below.

In This Piece

How Are Finances Important to Relationships?

People often shy away from the importance of finances in a marriage or other relationship because they don’t want to seem materialistic or as if they’re putting money and things before their significant other. In reality, though, finances are critically important because they can provide stability—or take it away, as the case may be. Being honest with each other about finances and working together transparently for future financial goals builds trust and helps the entire marriage or relationship succeed.

Some things that might be important to financial fidelity in a relationship include:

Being honest about income. Even if you don’t put all your money in a joint account together, being honest about your incomes can be important. Hiding that you make substantially more, so you can keep money to yourself is a form of financial infidelity in marriage. Instead, consider coming clean about the income and working together to come up with a fair way to treat the budget if you don’t want a complete “what’s mine is theirs” relationship.

Working together on budgeting. Create a shared budget and stick to it. This is especially important if you put all your funds together and treat them as the same. If you don’t do that, decide what expenses you’ll cover together, and always honor your part of that agreement before you spend on or save for yourself.

Maintaining transparency about spending. Be honest about what you spend and how, especially if you’re sharing accounts. Don’t hide packages or things you bought from each other or downplay what something costs because you know the other person might be upset about it. When making big purchases, talk to each other beforehand.

Deciding together on frivolous expenditures. Make a budget for frivolous spending or a no-questions-asked cash budget. For example, maybe you each get $50 a week in cash to do whatever you want with. If you like expensive coffees or want to eat out and your spouse doesn’t see the value in that, you can use your fun money for it without feeling like you have to hide it.

Agreeing to debt and other major decisions together. Don’t incur debt the other person doesn’t know about, and make large financial decisions together whenever possible.

What Is Financial Infidelity?

Financial infidelity occurs when you lie about money matters to each other in a relationship where there’s an expectation that you won’t. Usually this is possible when a couple shares finances, but it’s also possible even if you keep your finances separate and are dishonest about things.

A few examples of financial infidelity include:

Incurring debt and hiding it from the other person

Not paying a bill but telling the other person you did

Buying something in secret you know the other person wouldn’t approve of, especially if it’s expensive

Hiding money from the other person, such as opening a savings account in your name only to funnel money into

Signs of Financial Infidelity

If you’re worried that financial infidelity is at play in your relationship, consider the following common signs:

The other person gets anxious or angry, seemingly for no reason, when the subject of money comes up

There are larger-than-normal cash withdrawals on any of your accounts

You haven’t seen a credit card or bank statement in a while and the other person makes excuses whenever that comes up

The other person makes it difficult or impossible for you to log into online credit card or bank accounts

The other person always tries to get to the mail before you and doesn’t show you all the mail

You find potentially expensive items in your home, and you’re not sure where they came from or when they were purchased

You or your spouse is denied credit based on high debt-to-income ratios or credit utilization, but you weren’t aware that you had a lot of debt

Does Financial Infidelity Signal the End of Your Relationship?

Whether you should break up with someone or ask for a divorce based on financial infidelity is a personal choice, and one that probably should take into account many other factors. According to our survey, men are slightly more likely to initiate a breakup over financial issues, with almost 30% saying they had, compared to close to 23% of females.

Age also seems to play a role. Almost 30% of those aged 25 to 34 say they’ve broken up with someone over finances, and just over 30% of those aged 35 to 49 said the same. For people aged 50 to 64 and 18 to 24, the number drops to less than 15%, and for those over age 65, only around 6% said they had broken up with someone for these reasons.

Avoid Financial Infidelity

Couples know they have to work on issues like communication and intimacy. But they often don’t realize they should put the same effort into working on finances together. Start today by being open and honest about money. Consider signing up for your free credit scores together at Credit.com, so you can see where you both stand.

Methodology

This survey was conducted for Credit.com using Suzy. The sample consisted of a total of 1,019 responses per question and is not statistically representative of the general population. This survey was conducted in September 2022.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

The amount of money you need for a down payment depends on the overall cost of the house as well as the type of loan you’re approved for. VA and USDA loans can be as low as 0% while conventional and FHA loans range between 3%and 10%. Jumbo loans typically require a 10%down payment or more.

Buying a home is a goal for many Americans. The consumer and market data experts at Statista expect over 6 million homes will sell in 2023, which is a great sign for the housing market. If you’re one of the millions of Americans planning on buying a home, the first question you may have is, “How much do I need to put down on a house?”

Today, you’ll learn about how much you’ll need to put down before buying a home, and it may not be as much as you think. We’ll also go over how your down payment affects your offer as well as the pros and cons of making a larger down payment to help you make the right decisions before purchasing your dream home.

What Is a Down Payment?

A down payment is a certain percentage of the purchase price that you pay up front to secure a property, and the rest is paid in installments as part of a loan. Buying a home is a major purchase that can be hundreds of thousands or even millions of dollars, and if you’re like most people, you don’t have that much cash lying around. A down payment is much more realistic amount to pay up front, and it also lessens the risk of the lender by showing you’re more likely to have the ability to make your mortgage payments on time.

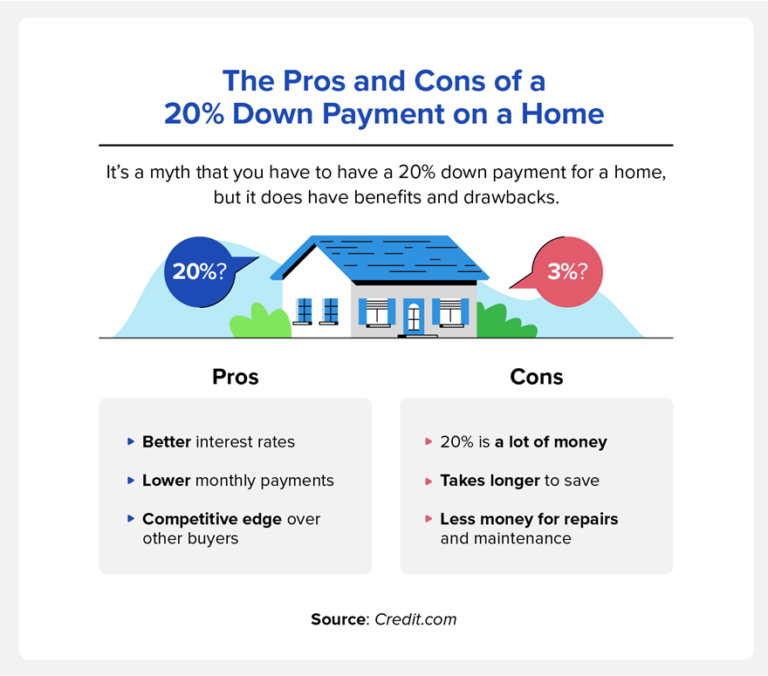

Do You Need to Put a 20% Down Payment on a House?

It’s a myth that you have to put down 20% when buying a home. A 2022 National Association of Realtors study found that 35% of people believe you need a 16-20% down payment to buy a home, but that’s not the case at all.

Get matched with a personal

loan that’s right for you today.

Learn

more

The data collected was from 1989 to 2021, and it shows that the typical down payment was 7% for first-time homebuyers and 3.5% for those getting an FHA loan.

The study also showed that repeat buyers put down an average of 17%, and this is because, based on their experience, they know the benefits of a larger down payment.

Although buyers don’t have to put down 20%, there are a few pros and cons to doing so:

Pros:

Better interest rates: A larger down payment means less risk for the lender and a smaller loan amount, so they charge less interest.

Lower monthly mortgage payments: The overall loan amount is lower, which also lowers the individual monthly payments.

The offer may be more competitive than other potential buyers: A larger down payment makes sellers feel more confident in the sale because it shows you can access more money and make the payments.

Cons:

It’s a lot of money you’ll no longer have access to: It’s always good to have a financial cushion in an emergency, so depleting your savings for a larger down payment may be a risk.

It may take longer to save for a home: The difference between a 5% and 10% down payment on a house can be tens of thousands of dollars, which can take additional years of saving.

You have less money for maintenance, repairs, furnishing, and appliances: Houses have many additional costs aside from the actual home.

You will have to take out Private Mortgage Insurance (PMI) insurance.

Minimum Down Payment Requirements Based on Type of Loan

The minimum down payment for a house can vary depending on which type of loan you’re approved for.

VA and USDA loans: If you’re a veteran or currently active in the military or qualify for a USDA loan, your down payment may be as low as 0%. The USDA loans are for suburban and rural home buyers and have an application process where you must meet certain requirements for the program.

Conventional loans: These loans include loans like HomeReady and Home Possible and can be as low as 3%. These aren’t backed by the government, but they have similar guidelines and sometimes require a minimum credit score of 620.

FHA loans: Federal Housing Administration loans are as low as 3.5%, but for those with bad credit, it may be 10%. To qualify for the lower down payment amount, you’ll need a credit score of 580 or higher.

Jumbo loans: For these larger loans that exceed FHA limits, the down payment may be as low as 10%, but lenders often require more to lessen their risk.

Five Benefits of Making a Larger Down Payment

If you know how much house you can afford and are in a good financial situation, a larger down payment is typically a better option. While 20% may not be achievable, there are still benefits to making a down payment that’s higher than the minimum.

The following are some of the benefits to a larger down payment:

Lower monthly payments: Your monthly payments are divided by what you owe on a home, so a larger down payment will reduce how much you spend each month.

Better interest rates: Interest rates are often higher when a lender is taking on more risk, so they’re lower when the lender is lending less money due to the larger down payment.

Lower closing costs: Lenders charge closing costs as a percentage of the total loan amount, which is less based on the big down payment.

Better equity: Your home’s equity comes from how much of the home you own, and you own more of a percentage of the home with a larger down payment.

Better chance of closing the deal: Sellers feel more confident selling to someone who can put down more cash up front.

How Much Should You Put Down on a House?

How much you put down on a home is going to be different for everybody. Not only will it depend on your personal situation and financial goals, but it will also depend on how competitive you want to be with your offer. When buying a home, there may be multiple offers, and a larger down payment can signal to sellers that you’re able to follow through with closing the deal.

A larger down payment also means less money for other financial goals. In that same study from the National Association of Realtors, they found the second most common source of down payments comes from loans. If you’re already in debt when looking to buy a house, you may want to put down a lower down payment.

Here are some other considerations that may help you decide how much to put down on a house:

How much you should keep in savings: Life is unpredictable, which is why it’s always good to have an emergency savings fund. When deciding on a down payment, it’s helpful to ensure you still have some savings to fall back on in case of emergencies.

Other costs as a homeowner: Some first-time home buyers forget that they’ll have more expenses when owning a home than renting. You’ll be responsible for all of the maintenance and repairs.

Closing costs: The closing costs of a home are a percentage of the loan, so when planning out the down payment, keep this fee in mind.

Down payment assistance options: There are various programs and incentives for home buyers, so you may be able to find down payment assistance options. Also, remember that different lenders may have different rates, so shopping around may help you find a better deal.

FAQ

There are additional nuances to down payments on a home, so we’ve answered some common questions below.

Is It Worth Putting 20% Down on a House?

If you’re in a good financial position and can afford a 20% down payment, there are many benefits to putting that amount down. It can help lower your interest rates and monthly payments and may even help you close the deal with the seller.

Is $10,000 Enough to Put Down on a House?

A $10,000 down payment might be enough for a home. According to the National Association of Realtors, down payments are based on a percentage of a home with an average down payment of 7-17%.

What Is the Normal Amount to Put Down on a House?

The normal down payment amount for a house varies depending on the house’s price and loan type.

How Much Do You Need to Put Down on a 400K House?

The most common type of loan is a conventional loan, and you may put 5% down for a 30-year fixed-rate mortgage. For a $400,000 home, the down payment would be $20,000.

Can You Buy a House Without a Down Payment?

Yes. There are government-backed loans like VA loans or USDA loans that don’t require a down payment if you qualify.

How Your Credit Affects Your Ability to Buy a House

In addition to the down payment for a home, your credit score plays a big role in the overall cost of a home as well as the type of loan you can qualify for. For example, the FHA has credit requirements, and you need a score of 580 to qualify for a 3.5% down payment.

If you’re unsure where you stand with your credit, you can sign up and get your free credit report card right at Credit.com. We also provide additional services through our ExtraCredit® program that can help you monitor your credit score in addition to other features as you get ready to buy a home.

Yes, you can refinance student loans with a private lender more than once in the quest for a lower interest rate and different repayment term.

How Many Times Can You Refinance Student Loans?

If you’re a graduate who has the credit score and income to qualify, you can refinance your student loans as many times as you’d like. In fact, some folks refinance multiple times.

But before you get too refi-happy, it’s important to know the advantages and disadvantages of this strategy.

What Are Some Advantages of Refinancing Multiple Times?

One of the biggest advantages of refinancing your student loans is that you may be able to qualify for a lower interest rate, whether you refinance once or several times. A reduced rate can help you save money in the long run.

For example, let’s say you’ve been paying down an older federal Grad PLUS loan that currently has a balance of $40,000 and an interest rate of 7.90%. You have 10 years of payments left, which are currently $483.20 per month.

You have good credit and qualify for a seven-year, fixed refinance rate of 6%. If you were to go through with the refinance, you’d actually increase your monthly payment by about $100. However, you’d save about $8,900 in total interest.

Later on, you might qualify for a lower fixed rate or an even lower variable rate, and so on.

Or you might find it helpful to refinance to a longer term, with lower monthly payments. That will likely mean paying more in interest over the life of the loan, but lower monthly payments may put you in a better position to accomplish your short-term financial goals.

Reputable lenders charge no application or origination fees, so refinancing each time will not cost you anything.

💡 Quick Tip: Get flexible terms and competitive rates when you refinance your student loan with SoFi.

What Are Some Disadvantages of Refinancing Multiple Times?

One disadvantage of refinancing your student loans is that your credit score could temporarily drop by a few points. Whenever you apply for a loan, the lender performs a hard credit inquiry. One or two inquiries usually have a small and temporary impact on your score. However, too many hard inquiries within a short time frame could cause some damage. The good news is that many student loan refinancing lenders allow you to shop for rates and get quotes online using a soft credit pull, which has no impact on your score.

Another factor to consider is your time. Though you can refinance as many times as you want, it helps to make sure it’s worth the effort. That means researching reputable lenders and the rates and terms they offer.

It’s important to point out that refinancing federal student loans even once will cause you to permanently forfeit government-backed protections and benefits, such as federal student loan forgiveness programs, deferment, and forbearance.

How Is Student Loan Refinancing Different Than Consolidation?

It’s important to make a distinction between refinancing and consolidation. When you refinance your student loans with a private lender, you are borrowing one new loan with new terms, such as a lower interest rate or different repayment term, and using the proceeds to pay off your existing loans.

When you consolidate federal student loans into a Direct Consolidation Loan, you combine your existing loans into one. The term may be drawn out to up to 30 years, and the interest rate will be the weighted average of the original loans’ rates, rounded up to the nearest eighth of a percentage point. For this reason, your new rate may actually be higher than the rate of your previous lowest-interest loan.

Things to Look for When Refinancing

Whether you refinance your student loans for the first or sixth time, it would be smart to check that your new rate and term make sense for you.

You’ll encounter fixed-rate and variable-rate loans. Fixed-rate loans have one set interest rate that does not change over the life of the loan. The rates on fixed-rate student loans are typically higher than the initial rates of variable-rate loans. However, because the rate never changes, it can make budgeting easier.

Variable-rate loans have interest rates that start off lower, but can fluctuate based on the prime rate or another index. Rates can climb if the rate or index they are tied to goes up (and vice versa).

Variable-rate loans might be a good choice for shorter-term loans. The longer the loan term, the bigger the chance of a rate hike.

Also, beware of qualifying for a low interest rate that’s attached to a longer-term loan. Though monthly payments might be low, a longer term might mean you’ll end up paying much more in interest over the life of the loan. If you can afford the higher monthly payment, loans with shorter terms can be a good cost-saving option.

Consider looking for a refinance lender that offers competitive rates and flexibility in choosing the repayment term. And if you want to refinance both federal and private student loans into one new loan, look for a lender that does that.

Serious savings. You could save thousands of dollars. We offer flexible terms and low fixed or variable rates.

Refinancing Your Student Loans More Than Once

It’s all about the great rate chase.

Having a low debt-to-income ratio can help you qualify for a lower interest rate. So if you have a higher salary, get a big bonus, or pay off other debts, your debt-to-income ratio might improve.

Similarly, if your credit score increases, you typically become more attractive to lenders. This could happen if you are using a small amount of your available credit, or if you find and correct a mistake on one of your credit reports. (Do student loans affect your credit score? Continuous on-time payments may have a positive effect.)

Married couples may want to consider refinancing student loans together to put the power of two earners to use. A solid cosigner could also be brought aboard.

If you’re thinking about a refinance, it could help to keep an eye on the federal funds rate, which is the rate banks charge one another for overnight loans. When the Federal Reserve raises or lowers short-term interest rates, private lenders respond in turn. (This does not apply to federal student loans, whose interest rates have been set by Congress once a year since 2006.)

Even if interest rates rise now, they could still be considered low by historical standards.

Refinancing Your Student Loans With SoFi

Is it bad to refinance multiple times? If it saves you money, that’s nothing but a good thing. Refinancing won’t be the right move for all people, but everyone should know the rates they’re paying, their total student debt load, and their repayment strategy.

SoFi is a leader in refinancing student loans, with low fixed or variable rates and flexible loan terms.

Looking to lower your monthly student loan payment? Refinancing may be one way to do it — by extending your loan term, getting a lower interest rate than what you currently have, or both. (Please note that refinancing federal loans makes them ineligible for federal forgiveness and protections. Also, lengthening your loan term may mean paying more in interest over the life of the loan.) SoFi student loan refinancing offers flexible terms that fit your budget.

With SoFi, refinancing is fast, easy, and all online. We offer competitive fixed and variable rates.

FAQ

Can I consolidate student loans more than once?

You can consolidate federal student loans into a Direct Consolidation Loan more than once only if you have federal loans that were not included in a previous consolidation, or if you previously consolidated loans under the Federal Family Education Loan (FFEL) consolidation program. Remember that consolidation does not lower your loan rate.

How many times can you refinance a loan?

As many times as you qualify to do so.

How many times can you take out student loans?

When it comes to federal student loans, there is no time limit on how long a borrower can receive Direct Unsubsidized Loans or Direct PLUS loans, but annual and aggregate limits for Direct Unsubsidized Loans apply.

Private student loans, for which you must qualify or have a cosigner, usually have an annual limit equal to an institution’s cost of attendance minus other financial aid. Most have aggregate loan limits for undergraduate and graduate students.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Student Loan Refinancing If you are a federal student loan borrower you should take time now to prepare for your payments to restart, including the opportunity to refinance your student loan debt at a lower APR or to extend your term to achieve a lower monthly payment. (You may pay more interest over the life of the loan if you refinance with an extended term.) Please note that once you refinance federal student loans, you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as the SAVE Plan, or extended repayment plans.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

This article originally appeared on Radical FIRE and has been republished here with permission.

When you’re planning on moving in with your partner, there are important money conversations you need to have before moving in with your partner.

I’m planning to move in with my partner after we complete our four-month mini-retirement, where we travel to Central America together. I assume that after we’ve spent so much time together abroad, we should be fine with moving in together. Just one thing that should be discussed is our finances.

Money Conversations with Partner

Moving in with someone requires some financial logistics to be arranged. You need to discuss who is paying which bills, who is responsible for what, and more.

You know I love having money conversations, with my friends or with my family. I love to talk about money, that’s why I write on the blog. When no one wants to hear me talk about money for the gazillionth time, I’m just writing a blog post about my money thoughts.

Now onto the money conversations that you need to have before moving in with your partner. I’ve had all these conversations over the past weekend just to know we’re on the same page. I recommend you also have them when you’re planning to move in with your partner!

Money Conversation #1: Do We Share Our Stuff?

I mean, is everything that was once mine now ours? Is everything that was once yours now ours? It’s about the tangible things that are in the house, not including money. This is something to think about before moving in together.

If you have things that your partner also has, should you bring it? Or can you use one and get rid of the other one? If there are things that you don’t have yet but you know you need? Will you buy it together or will one of you buy it?

In relation to that, we get to the next point.

Money Conversation #2: What Will We Do If … ?

You don’t go living together with your partner unless things are serious between you. You need to consider the possibility of the relationship ending sometime very far in the future (OMG!). Breakups and divorces are a possibility that needs to be considered.

If you’re sharing things, what will happen after you stop being together? This is important for things like furniture and electronics, following the previous point. Will you share everything together, yes or no?

Related read: 10 Ways Divorce can Affect your Credit

Money Conversation #3: Is The Money Going to Be Ours, Too?

It’s important to think about if you’re going to join finances or not. It’s a very personal thing to think about and it will differ for everyone depending on their situation. If your partner makes a lot less, you can decide to pay more towards the fixed monthly payments. Or vice versa.

Just keep in mind that you should do something that makes you comfortable!

For me and my partner, we will not join finances. We’re having separate financial goals at the moment. I’m working towards my goal of financial independence and keeping a savings rate of over 80% consistently until we go on our travels. Meaning we’re not on the same page concerning money goals.

That’s okay for now. He will look for a job after we return and we will decide how we will go from there.

For our expenses, we will be splitting everything equally. I currently make more than my partner. The rent will be low enough for him to comfortably be covering half. If in any given month he cannot pay his portion of the rent or there are any other difficulties that won’t allow him to pay half of the rent, I will of course help him.

Related read: How Renting Can Impact Your Credit

Money Conversation #4: How Will You Deal with Changes?

What if I lose my job? Or my partner can’t find a job after graduation? What if we need to move for work or someone can get a promotion abroad? All scenarios can happen. It’s extremely difficult to think about what you want to do when you’re not yet in the situation. It’s a good thing to discuss these matters a little in advance.

If you don’t know now how you will deal with these kinds of changes, think about how you’re both dealing with changes until now? When you’re both quite relaxed under changes, it’s unlikely that those changes will put stress on your relationship. If you’re both sensitive to changes, it might lead to stressful situations and it might be good to address those things at this moment.

Money Conversation #5: What Do You Value Spending Your Money On?

Before you’re moving in with your partner, it’s important to talk about what you value spending money on? It can significantly differ among people. One person loves to go on big holidays, the other likes to drive their dream car, wants to have a big space to live in, or likes to have the latest tech gadgets. It’s good to know what they value.

Before you’re moving in together, it’s important to understand what they value and what is important to them. The habits they have around the things they value may have an impact on your joint life together.

My partner loves playing games and spends a great deal of time playing games both online and offline. He used to spend a good amount of money on getting new games, getting new consoles, or updating his computer. Currently, he doesn’t spend too much money on those types of things, but it’s still something to keep in mind when you’re going to live together.

I used to buy a lot of clothes, but since getting on my clothing ban I haven’t bought any clothes. On the contrary, I’ve sold a lot of stuff around the house when I decided decluttering was the way I wanted to go. I won’t say I’m exactly a minimalist, but I’ve gotten rid of certain habits and I’m starting with a clean slate when I’m moving in with my partner.