In the age of Airbnb, listing your home, property or apartment for temporary and long-term renting is a unique way to generate income while stepping into property management shoes. Listing your property, which may initially sound simple, requires meticulous management, organization skills and a general understanding of landlord-tenant law. The worthy feat of generating income through property rental is gaining popularity, particularly in areas where housing is in high demand.

Explore the comprehensive guide below to understand the process of renting your house and assist in developing an efficient property management strategy. These step-by-step instructions are tailored to assist both novice and seasoned property owners in maximizing the benefits of the significant endeavor that is the rental game.

Renting out your house: a step-by-step guide

Follow these steps to ensure you and your potential renters gain the most from the renting experience. In addition to optimizing your earnings, acquire the know-how to increase your visibility, ensure compliance with legal regulations and cultivate essential management abilities.

1. Understand local laws and regulations

Before you embark on your property management journey, it’s imperative to research and familiarize yourself with local laws and regulations around renting. Here are some rules, regulations and definitions to understand concerning renting out your house while playing by the rules.

Fair Housing Act: This federal law prohibits discrimination against housing applicants on the basis of race, color, religion, national origin, disability, sex, age or familial status (e.g., women who are pregnant, families with small children or teenagers, etc.).

Fair Credit Reporting Act (FCRA): Credit and criminal background checks are subject to federal regulation known as the Fair Credit Reporting Act (FCRA). Its many provisions include the following requirements:

You must notify applicants in writing and get their written permission before running any check on them.

If you decide to reject an applicant based on the findings of a credit report or background check, you must notify the applicant of your intent in writing, furnish them a copy of the report and give them a reasonable amount of time (a week suffices) to respond with a correction or explanation of the report’s findings.

After that period, upon consideration of any response you get from the applicant, you may notify them in writing of your final decision.

“Fair chance” laws: This isn’t a federal law, but a growing number of states and cities have enacted these measures to prevent discrimination against persons with prison records. Specifics vary by jurisdiction, but most of these laws forbid asking about past criminal convictions or incarceration on housing applications.

Protect yourself by consulting your legal advisor to see whether any fair chance laws apply to you, and how they might affect your tenant-screening process. Avoid exposing yourself to legal liability as well by utilizing professional background-check companies or consulting legal advice further.

2. Prepare your property

Staging your property and making it suitable for renters is the next step. Ensure any broken appliances are fixed, messes tended to and any recommended enhancements are made. Completing some market research to see similar rental properties to yours (properties that have similar offerings like bedroom and bathroom numbers or properties in the same location) can be helpful in terms of improvements or enhancements to make to your rental property.

Secure landlord insurance as a part of your preparation step. Landlord insurance is a specialized policy that safeguards property owners from potential financial losses and liabilities when renting out their residential properties to tenants. It typically covers property damage, liability protection and loss of rental income due to covered events.

3. Set a competitive rental price with our rent estimator tool

Continue your market research in this step to determine the ideal price range for renting out your property to temporary tenants. Utilize this rent estimator tool to assist you in valuing your property for rent price.

4. Draw up a lease agreement

Draft a comprehensive lease agreement that clearly outlines the terms and conditions of the rental, including rent amount, security deposit, lease duration and any rules or policies for the property. Ensure that it complies with local and state laws.

5. Create your listing

Once you know what you’re charging for rent, you’re ready to get to the heart of marketing the property online: putting together a listing that will entice tenants into renting out your home.

The key to a great listing is communicating the unique advantages of your property in a way that attracts the right kind of tenant. Namely, a tenant who will be dependable and take care of your property as if it were their own.

A Rent. survey found that most seekers of single-family rental (SFR) properties are married or in domestic partnerships (62 percent), have children (61 percent) and have pets (54 percent).

Regardless of who you are renting out your home to, it’s important to highlight what’s most likely to resonate with your ideal tenant. Here are some potential features to consider when renting out your home.

Schools: Each Rent. listing automatically displays GreatSchools.org ratings for schools closest to each property. If nearby schools get high marks, consider highlighting them in your property description and noting if any are within walking distance.

Parks or playgrounds: If there are parks or playgrounds nearby, mention them and how long it takes to walk or bike to them. If you pique any rental seekers’ curiosity, they can use the map embedded in the Rent.com listing to explore via Google Street View.

Pet-friendliness: If you plan to allow pets on the property, make sure you include this in the listing, along with any breed restrictions info. Call out relevant details that will be of interest to pet owners (e.g., nearby pet-friendly parks, fenced-in yards, doggy doors, etc.).

Neighborhood highlights: Call out nearby landmarks, much-loved hangouts or transportation conveniences like a train or subway stop and include a picture. Don’t forget to call out the distance from your property.

6. Market your property

Share your listing across ILS networks to cover a lot of the heavy lifting, but you can also share links to your Facebook and Instagram accounts. Try using Facebook Marketplace to limit the post geographically (and to reach potential tenants you aren’t friends with on Facebook).

Once you’ve posted one and shared it across multiple ILS sites and social media, you’ll likely be moving on to the next phase of the rental process: choosing the best tenant from among the applicants who are interested in your rental listing.

7. Screen and collect

Develop a tenant screening process that includes background checks, credit checks and references. This will help you select reliable tenants who are more likely to pay rent on time and take care of your property. Once you find a suitable tenant, collect a security deposit and the first month’s rent from your tenants before they move in. Make sure you follow local laws regarding the handling of security deposits.

Once tenants are inhabiting your rental property, it’s imperative to stay responsive to maintenance requests from your tenants. Timely repairs and maintenance will help keep your property in good condition and your tenants satisfied.

8. Maintain your rental property

Regular maintenance tasks include keeping the property in good repair, addressing maintenance requests promptly and conducting routine inspections to identify and address issues before they become major problems. Timely maintenance is important because it minimizes the risk of costly repairs down the road. Make sure to stay up to date with local regulations and safety standards as well to ensure that your rental property remains compliant and safe for renting out.

Renting our your house made easy

Renting out your home, in the age of Airbnb and VRBO, is an exciting time and journey to embark on. Once you estimate your home using our rent calculator tool, draw up your lease and prepare your property, the rest of the process involves meeting and vetting potential tenants. Sharing your home, community and amenities is a unique job that just about anyone can do, using this article.

The information contained in this article is for educational purposes only and does not, and is not intended to, constitute legal or financial advice. Readers are encouraged to seek professional legal or financial advice as they may deem it necessary.

Wesley is a Charlotte-based writer with a degree in Mass Communication from the University of South Carolina. Her background includes 6 years in non-profit communication and 4 years in editorial writing. She’s passionate about traveling, volunteering, cooking and drinking her morning iced coffee. When she’s not writing, you can find her relaxing with family or exploring Charlotte with her friends.

There’s a lot to learn when you’re preparing to buy a home.

First, you’ll need to understand market values to avoid paying too much for your house. In addition, home inspections are vital to uncover any hidden issues before finalizing a purchase.

Furthermore, potential buyers must pay attention to closing costs, ensuring they have sufficient funds for the transaction. Lastly, perhaps the most critical aspect to keep in mind is being aware of current mortgage rates.

For those in the market for a house, even a minor adjustment in the interest rate can substantially change your financial picture and affect how much house you can afford.

This guide will shine a light on the intricacies of securing the best mortgage rate, which could translate into significant savings throughout the life of the loan. A lower rate may even allow you to afford a nicer home for your money.

Step 1: Boost Your Credit Score

A top-tier credit score be your VIP pass to securing the most enticing mortgage rates. But what factors make up your credit scores? And how can you boost yours in a hurry?

Timely bill payments: The bedrock of a solid credit score, timely bill payments account for 35% of your FICO credit score. Paying your credit card bills and monthly debt payments on time, consistently, boosts your credit scores. On the other hand, missed or late payments reduce your score, and can remain on your credit report for up to seven years, making it harder to get a good interest rate.

Credit card balances: Having credit cards helps you build credit, which can increase your FICO score. But maintaining a balance lowers it. Aim to keep your utilization ratio, which is the balance in relation to your credit limit, below 30%. An even better practice is paying off the balance in full every month.

Avoid excessive inquiries: Every time you apply for credit, a ‘hard inquiry‘ is placed on your report. Multiple hard inquiries in a short period can indicate risk to potential mortgage lenders, slightly dropping your score with each one. There’s one caveat here: Inquiries for the same loan type (such as a mortgage or car loan) within a few weeks of each other are counted as one inquiry. The credit bureaus understand you are shopping around for the lowest rates.

Check your credit reports regularly: Make it a practice to review your credit report from all three bureaus annually. This can help you spot and rectify errors or discrepancies which, left unaddressed, could reduce your credit scores.

Remember, in the eyes of lenders, a higher credit score depicts financial responsibility. Achieving this can translate to potentially thousands saved in interest over the life of your mortgage loan.

Step 2: Increase Your Down Payment

The down payment is more than just the initial chunk of money you put toward your home; it’s a reflection of your commitment to the property. The amount you put down influences how mortgage lenders perceive your loan’s risk.

Take a look at some of the advantages of putting 20% or more down.

Less borrowing: The more you pay upfront, the less you’ll need to borrow. This reduces your loan-to-value ratio, which can make you a more attractive borrower to lenders.

Lower rates: Lenders often associate higher down payments with lower risk. A borrower who can afford a larger down payment is seen as more financially stable, thus possibly qualifying for a lower interest rate.

Avoid private mortgage insurance (PMI): Typically, if you put down less than 20% on a conventional loan, you’ll be required to pay PMI. This insurance protects the lender if you default on your loan. By increasing your down payment to 20% or more, you can bypass this additional cost.

Future financial flexibility: By paying more upfront, your monthly mortgage payments will be lower, offering you greater financial flexibility in the future. This can be particularly beneficial during unforeseen financial hardships.

While it may be tempting to jump into homeownership with a smaller down payment, putting at least 20% down can lead to substantial savings in the long run and a more favorable loan structure.

Step 3: Consider Buying Mortgage Points

The strategic purchase of mortgage points, also known as discount points, serves as an effective mechanism to lower your mortgage rate. Let’s explore how they work.

What are mortgage points?

A discount point is a form of prepaid interest. One point typically equates to 1% of your loan amount and can decrease your interest rate by a certain percentage, usually around 0.25%.

Should you buy points?

Points can be a costly upfront expense at closing time. It’s important to decide if the future benefits justify the investment. Ask yourself:

How long do you plan to live in the house?

How much will you save on your monthly payment?

How long will it take to break even on the cost of the points?

Your mortgage lender can help you calculate whether buying points makes sense for you. They can provide a breakdown of the costs and savings associated with purchasing points, offering a clearer picture of the potential benefits.

Step 4: Choose the Right Loan Term

Your loan term is more than just a deadline for repaying your mortgage; it determines your interest rate and monthly mortgage payment.

Generally, shorter-term loans, like a 15-year fixed rate mortgage, come with lower interest rates than longer-term ones, like a 30-year mortgage. The reason is simple: lenders face less risk when the borrowed amount is to be repaid over a shorter period.

However, with a shorter term, you’ll have higher monthly payments, since you’re dividing your total mortgage amount over fewer months. You’ll need to balance the allure of a lower rate against the practicality of larger monthly payments.

Before you choose a loan term, assess your current financial situation and your projected future income. Your comfort with the size of the monthly payment, your financial goals, and your age at the end of the term are all factors that should inform your decision.

By understanding these elements, you can select a loan term that best aligns with your financial plans, payment capability, and homeownership goals.

Step 5: Navigate Market Conditions

Understanding and responding to the broader economic landscape is pivotal in securing an affordable mortgage. The U.S. Federal Reserve sets the federal funds rate, which is the rate at which the central bank lends money. The funds rate determines the interest rate for credit cards, loans, and mortgages.

A flourishing economy often triggers an increase in interest rates. The U.S. Federal Reserve has raised rates in recent months to try to stem inflation. However, an economic downturn could cause the Fed to keep rates steady or even reduce rates to stimulate borrowing and spending.

Understanding these principles can offer insight into potential rate fluctuations as you decide whether you want to buy now or wait for rates to drop.

It’s important to research these factors to have an understanding of the market. But you can also seek the guidance of a financial advisor or a mortgage broker. They have expertise in market trends and can provide advice tailored to your circumstances.

Step 6: Leverage First-Time Homebuyer Programs

If you’re navigating the housing market for the first time, there are a plethora of programs tailored to assist you in securing a favorable interest rate. These programs, often government-supported or backed by financial institutions, are designed to make homeownership more accessible. They offer a variety of incentives such as competitive mortgage rates, lower down payment requirements, or even assistance with down payments.

To qualify, you usually need to meet certain criteria, including income limits, purchasing in a designated area, or completing a homebuyer education course. It’s crucial to investigate these opportunities, as eligibility can vary widely between programs and regions.

Tapping into these programs can significantly alleviate the financial strain of homeownership, reducing your mortgage rate, and making the dream of owning a home more achievable and affordable. Research and due diligence are key in identifying and securing these benefits.

Step 7: Compare Multiple Lenders

Actively seeking and comparing options from several lenders can help you secure the most favorable interest rate. Here are three steps to take in your search for the best mortgage rate.

Know what to compare: Each lender may have unique offerings in terms of mortgage loan options, closing costs, and interest rates. By getting quotes from a minimum of three lenders, you ensure that you have a broad spectrum for comparison, helping you make an informed decision.

Utilize financial tools: A mortgage calculator is an excellent tool for to evaluate lenders. By inputting the variables of different interest rates, loan terms, and down payment amounts, you can get a clearer understanding of the monthly payment and total cost associated with each loan option.

Take your time: Don’t rush this step. It’s important to thoroughly review and understand each offer. Remember, a mortgage is a long-term commitment, and the details matter. Choosing the right lender can save you thousands of dollars over the life of your loan.

Step 8: Negotiate Your Mortgage Rate

While it might seem daunting, negotiating your mortgage rate is entirely possible and could result in substantial financial savings. Lenders and mortgage brokers often have some flexibility in the rates and fees they can offer. This is where thorough research and understanding of your own financial health, including your credit scores, debt-to-income ratio, and loan options, can be advantageous.

The more you understand these factors, the more leverage you have during negotiations. A well-prepared negotiation strategy can give you a significant advantage in securing a mortgage rate that suits your financial situation best.

Remember, even a slight decrease in your mortgage rate can result in significant savings over the life of your loan. It’s worth the effort to negotiate terms; it could save you a considerable amount of money in the long run.

Conclusion

Securing the best mortgage interest rate can make your dream home more affordable and save you thousands over the life of the loan. By understanding how different factors like your credit scores, down payment, and loan term affect your rate, you can take steps to secure the best mortgage deal. Remember, a home loan is likely to be one of the biggest financial commitments you’ll ever make, so take the time to get it right.

Frequently Asked Questions

What is the ideal credit score for getting the best mortgage rate?

While credit requirements can vary by lender, a credit score of 740 or higher generally qualifies borrowers for the best mortgage rates. However, it’s still possible to secure a mortgage with a lower credit score, but the rates might be higher.

What’s the difference between a fixed-rate and an adjustable rate mortgage (ARM)?

A fixed-rate mortgage has a constant interest rate and monthly payments that never change. This offers stability and predictability over the life of the loan.

Adjustable rate mortgages have an interest rate that may change periodically, affecting your monthly payments. The rate adjustments are tied to market conditions and specified in the mortgage agreement.

The main difference is that a fixed-rate mortgage offers long-term stability in payments, while an ARM carries the risk of the payments increasing or decreasing over time.

How much can I save by improving my credit score?

The difference in mortgage rates between different credit score ranges can be substantial. For instance, improving your credit score from ‘fair’ (580-669) to ‘very good’ (740-799) could potentially lower your interest rate by a full percentage point or more. Over the life of a 30-year mortgage, this could translate to tens of thousands of dollars in savings.

How much should I save for a down payment?

The amount you should save for a down payment can depend on the type of loan you’re getting and your financial situation. Traditionally, a 20% down payment is recommended for conventional loans, as this allows you to avoid paying for private mortgage insurance (PMI). However, some loan types, such as Federal Housing Administration (FHA) loans, allow for lower down payments.

How do I choose between a 15-year and a 30-year loan term?

The choice between a 15-year and a 30-year loan term depends on your financial circumstances and goals. A 15-year loan typically has a lower interest rate but a higher monthly payment, making it a good choice if you can comfortably afford the payments and want to pay off your mortgage faster. On the other hand, a 30-year loan has lower a monthly payment but a higher interest rate, making it a more affordable option for many buyers.

Is it worth buying discount points to lower my interest rate?

Whether it’s worth buying discount points depends on your particular situation. If you have the cash and plan to stay in your home a long time, buying points can be beneficial. The savings over time from a lower rate can exceed the points’ upfront cost.

What are some examples of first-time homebuyer programs?

First-time homebuyer programs can vary by state and by lender, but some examples include FHA loans, USDA loans, and VA loans, as well as specific state-sponsored programs that offer down payment assistance or tax credits. It’s worth checking with your local government and potential lenders to see what programs might be available to you.

How do market conditions impact mortgage rates?

Mortgage rates are influenced by a variety of market conditions, including inflation rates, economic growth indicators, and monetary policy decisions by central banks. Generally, when the economy is strong, mortgage rates tend to rise to keep inflation in check. Conversely, during economic downturns, rates often fall to stimulate borrowing and investment.

Many people are lured into the world of real estate investing by stories of millionaires who started their journey with no money down or no steady employment. But the reality is that making money in real estate isn’t easy; a good credit score, investment capital and steady income can help in the beginning.

You’ll also need to grasp the nuances of the local real estate market and learn how to manage financial aspects such as cash flow and property taxes. While real estate buying, selling, and renting may not be much like a game of Monopoly, it is possible to earn steady side income, supplement your retirement, or even build a full-time real estate investment business with the right tools, knowledge, and patience.

Unlike mutual funds, the stock market, cryptocurrency or many other investments, real estate is tangible. Real estate is a concrete asset—one can see, touch, and even reside in. That gives investors a sense of security. However, it also creates unique challenges.

Managed well, the stability and passive income from rental properties can be a safety net against more volatile investments.

This guide is here to clarify the process for beginners. It aims to empower you to make informed decisions, reduce risks, and lay a strong foundation for your real estate investing journey.

Benefits of Investing in Real Estate

The allure of real estate goes beyond the mere ownership of tangible assets. It presents a robust suite of financial benefits that have the potential to amplify wealth and provide stability in uncertain times. As we navigate the advantages, it becomes evident why many seasoned investors prioritize real estate in their portfolios.

Steady and Passive Income

Real estate investing, especially in rental properties, stands out for its potential to provide a consistent revenue stream. When you own a rental property, the monthly or quarterly distributions from tenants contribute to steady income, which can safeguard your finances against unexpected events or economic downturns.

This consistency contrasts with the often erratic nature of the stock market, which can fluctuate daily based on global events, company performances, and other factors. Additionally, for those aiming to attain financial freedom, the passive income generated from real estate can be a step closer to achieving that goal. Over time, as the mortgage payment decreases or remains static, rental rates may rise, increasing your monthly cash flow.

Appreciation Potential

Every investor dreams of their assets appreciating, and real estate often doesn’t disappoint. While there can be periodic downturns in the real estate market, historical trends suggest that properties generally gain value over the long run.

This means that not only can investors benefit from rental income, but they can also potentially see substantial gains when they choose to sell the property.

Tax Benefits

Navigating the world of taxes can be intricate, but real estate investors often find several advantages here. The ability to deduct mortgage interest and property taxes from taxable income can be a significant financial boon.

Furthermore, strategies like depreciation allow real estate investors to offset rental income, reducing their tax burden. Consulting with a financial advisor can help investors maximize these benefits and understand other potential tax advantages, such as 1031 exchanges or deductions related to property management.

Diversification

The saying “don’t put all your eggs in one basket” is sound investment advice. Diversification is a fundamental strategy to mitigate risks. By adding real estate to an investment portfolio, investors introduce a separate asset class that doesn’t directly correlate with the stock market or mutual funds. This can provide a buffer, ensuring that a downturn in one sector doesn’t wholly derail an investor’s financial trajectory.

Leverage

Leverage, in the context of real estate investing, refers to the ability to use borrowed capital to increase the potential return on an investment. When you purchase property with a mortgage loan, you’re often putting down only a fraction of the property’s total cost, while still reaping the benefits of its entire value in terms of appreciation and rental income.

This magnifies the return on investment, as the gains and income generated are based on the property’s total value, not just the down payment. It’s a powerful tool but should be used wisely. Over-leveraging or not accounting for potential rental vacancies can turn leverage into a double-edged sword.

Types of Real Estate Investments

As one dives deeper into the world of real estate, it becomes evident that this asset class is multifaceted, with various avenues to explore and invest in. The right choice often depends on an investor’s goals, risk tolerance, budget, and expertise. Here’s a closer look at some prominent types of real estate investments:

Residential Properties

Residential properties cater to individuals or families. They range from single-family homes to duplexes, triplexes, high-rise buildings with apartments, and other multi-unit properties. You may encounter the term “MDU” or “MUD,” which stand for multi-dwelling unit or multi-unit dwelling, to describe anything more than a single family home, or SFR (single family real estate).

Investing in residential real estate, especially the SFR market, is often a beginner’s first step due to its familiarity and the perpetual demand for housing. While these properties can be a reliable source of rental income, investors should be prepared for the challenges tied to property management, tenant turnover, and ongoing maintenance.

Commercial Real Estate

When one thinks of skyscrapers lining city horizons or sprawling office parks in suburban locales, that’s commercial real estate. These properties are tailored to businesses, and can include complete corporate headquarters or individual offices.

Commercial leases often run longer than residential ones, offering the potential for stable, long-term rental income. However, the entry point can be higher, with larger down payments and a more extensive due diligence process. Additionally, commercial real estate values can be closely tied to the business environment of the locality.

Industrial

Industrial real estate encompasses properties like warehouses, distribution centers, and manufacturing facilities. They’re integral to business operations, ensuring products move efficiently from manufacturers to consumers.

Investing in this sector can offer substantial rental yields, especially if the property is strategically located near transportation hubs. However, the nuances of industrial real estate, such as zoning laws and environmental concerns, necessitate a more in-depth understanding than residential or commercial sectors.

Retail

This sector includes shopping malls, strip malls, and standalone stores. What’s unique about retail real estate is that leases sometimes include a provision where the landlord gets a percentage of the store’s profits, termed as “percentage rent.”

In a thriving commercial area, retail properties can be quite profitable, with long-term leases and the potential for appreciating property values. However, investors should be mindful of shifts in consumer behavior and the evolving retail landscape, especially with the rise of e-commerce.

Multi-Purpose Commercial

A new breed of commercial real estate has emerged to compete with the growth of e-commerce. Multi-purpose commercial spaces blend housing units with office space and retail, often adding hospitality and entertainment venues.

Typically, these spaces are the domain of large real estate investment and property management firms. But if you invest in commercial office space or retail, you will be competing with these multi-purpose properties for tenants, so they are worth acknowledging.

Real Estate Investment Trusts (REITs)

For those not keen on direct property ownership, REITs present an attractive alternative. These are companies that own, operate, or finance income-producing real estate across various sectors. What makes REITs distinctive is that they’re traded on stock exchanges, similar to stocks.

By investing in a REIT, you’re buying shares of a company that manages a portfolio of properties, thus gaining exposure to real estate without the hassles of property management. Moreover, by law, REITs are required to distribute at least 90% of their taxable income to shareholders, leading to potentially attractive dividend yields. However, it’s essential to remember that like all publicly traded entities, REITs can be subject to market volatility.

9 Ways to Invest in Real Estate

Investing in real estate can seem tricky for beginners. But, with time and patience, anyone can master it. Focus on simple investment methods first to get to know your local property scene, meet experienced investors, and learn how to handle money wisely. As you learn and grow, you can dive into more complex investment options.

Here are some great ways for beginners to start in real estate:

1. Wholesaling

Acting as the bridge between property sellers and eager buyers, this method primarily focuses on securing properties at a rate below the prevailing market value. The secured contract is then transferred to an interested buyer, ensuring a margin for the wholesaler.

2. Prehabbing

Unlike intensive property renovations, prehabbing is about amplifying a property’s appeal through minimalistic enhancements. These properties, once given their facelift, usually attract investors with a keen eye for larger renovation projects.

3. Purchasing Rental Properties

An avenue promising consistent returns, this involves acquiring properties to lease them out. For those not inclined towards the intricacies of landlord duties, there’s always the option of hiring seasoned property management professionals.

4. House Flipping

A strategy that has garnered significant attention, house flipping involves a cycle of purchasing, upgrading, and promptly reselling properties, aiming for a profit. The emphasis is on swift transactions and keen market acumen.

5. Real Estate Syndication

Envision a collective where like-minded investors come together, pooling both resources and expertise. Such collectives venture into large-scale property acquisitions, and the ensuing profits or rental incomes are distributed among the participants.

6. Real Estate Investment Groups (REIG)

Primarily, these are conglomerates that steer their operations around real estate investments. By amassing capital from a plethora of investors, they dive into acquisitions of sizeable multi-unit residences or commercial holdings.

7. Investing in REITs

Real Estate Investment Trusts (REITs) revolve around the ownership and meticulous management of properties that yield income. However, investors don’t have to handle the management themselves. Instead, participants can relish the benefits of the real estate sector without the responsibilities of direct property ownership.

8. Online Real Estate Platforms

A fusion of technology with real estate, these platforms seamlessly connect potential investors with vetted property developers. This synergy enables backers to finance promising property ventures and, in exchange, enjoy periodic returns that encompass interest.

9. House Hacking

A blend of homeownership and investment, house hacking is about maximizing the potential of a multi-unit property or a single-family home. Investors live in one segment while leasing out the remaining portions. This dual approach can significantly reduce or even negate monthly housing expenses, serving as an excellent introduction to the world of property management for novice investors.

6 Steps to Get Started in Real Estate Investing

Starting on the path of real estate investing requires careful planning, due diligence, and a methodical approach to ensure that your investments are sound and have the potential for fruitful returns. Whether you’re dreaming of becoming a millionaire real estate investor or merely looking to diversify your investment portfolio, following a structured process can be the key to success. Here’s a step-by-step breakdown:

1. Assess Your Financial Health

Every investment journey should begin with introspection. As an aspiring real estate investor, it’s essential to have a clear understanding of your current financial standing. Ask yourself questions like:

How much capital am I willing to invest?

What are my short-term and long-term financial goals?

Do I have an emergency fund set aside?

Evaluating your risk tolerance is equally crucial. Some might be comfortable flipping houses, while others might prefer the steadiness of rental properties. Consulting a financial advisor at this stage can provide insights tailored to your financial health, enabling you to make informed decisions as you proceed.

2. Dive Deep into Market Research

Knowledge is power in the world of real estate. The local market can be significantly different from national or even statewide trends. Delve deep into understanding:

The demand for rental properties in your target area.

The average property values and rental rates.

The historical appreciation rates.

Any upcoming infrastructure projects or urban development initiatives.

Furthermore, familiarize yourself with real estate terminology. Phrases like “cap rate,” “loan-to-value,” and “operating expenses” will become a regular part of your vocabulary. The better informed you are, the more confidently you can navigate your investments.

3. Assemble Your Real Estate Team

No investor is an island. Success in the real estate business often hinges on the strength and expertise of your team. Look for professionals with a proven track record and positive reviews. Your team might include:

Real estate agents who understand the investor’s perspective.

Property managers to streamline tenant interactions and maintenance.

Lawyers specializing in real estate transactions.

Accountants familiar with the tax implications of real estate investments.

4. Explore Financing Options

The path to acquiring a property is paved with various financing methods. Traditional mortgages are common, but the real estate industry offers other mechanisms like:

Hard money loans.

Private money loans.

Real estate syndication where multiple investors pool resources.

Seller financing.

Each of these has different pros and cons, interest rates, and repayment terms. Understand each deeply to determine which aligns best with your financial strategy.

5. Analyze Potential Properties

The crux of real estate investing is ensuring that the numbers make sense. Before purchasing, assess the property’s potential for generating rental income. Break down:

Monthly mortgage payments

Property taxes

Maintenance costs

Potential vacancy rates

Your goal should be a positive cash flow, where the monthly income from the property (rent) exceeds all these expenses.

6. Negotiate and Close the Deal

Once you’ve zeroed in on a property, the negotiation phase begins. Here, understanding the property’s market value, any existing damages or repair needs, and the local real estate market dynamics can give you an edge.

When it comes to closing, be aware of all associated costs. These might include inspection fees, title insurance, and escrow fees. Being well-informed can help you negotiate these fees and ensure that you’re not overpaying.

Risks and How to Mitigate Them

Like any investment, real estate comes with its set of challenges and uncertainties. The difference between successful real estate investors and those who falter is often the ability to anticipate risks and prepare for them. Here’s an exploration of some prevalent risks in real estate and actionable steps to manage them:

1. Market Fluctuations

Real estate markets can be volatile, with property values rising and falling based on a myriad of factors.

Mitigation: To protect against market downturns, it’s essential to buy properties below their market value. Conducting comprehensive research and seeking expert investment advice can help investors make informed decisions. Remember, real estate is often a long-term game, so a short-term dip can be offset by long-term appreciation.

2. Unexpected Repairs and Maintenance

Properties can often come with surprises, from plumbing issues to roof repairs.

Mitigation: Regular property inspections can catch potential problems before they become major expenses. Setting aside a buffer fund specifically for maintenance can also cushion the financial blow of unforeseen repairs.

3. Vacancy Periods

There might be periods where your property remains unoccupied, leading to loss of rental income.

Mitigation: Properly vetting and building a good relationship with tenants can lead to longer lease periods. Diversifying your investment properties across different areas can also help, as vacancy rates might vary from one location to another.

4. Legal and Tax Implications

Real estate investors can sometimes find themselves entangled in legal disputes or facing unexpected tax bills.

Mitigation: Regular consultations with a tax professional or attorney familiar with the real estate industry can keep investors informed and protected.

Long-term Strategy and Growth

Real estate investing is not just about making a quick buck; it’s about building lasting wealth. Adopting a long-term perspective and continuously refining your strategy can pave the way for consistent growth in the real estate industry. Here’s how:

1. Define Your Real Estate Identity

Are you more comfortable with a buy-and-hold strategy, where properties are retained for long-term growth and steady rental income? Or do you thrive on the excitement of flipping houses, where properties are bought, renovated, and sold for profit? Understanding your preference can help tailor your investment strategy.

2. Reinvestment is Key

For those adopting a buy-and-hold strategy, reinvesting the rental income can substantially grow your real estate portfolio. By channeling profits into purchasing additional properties, investors can benefit from compounded growth.

3. Diversify Your Portfolio

As you gain experience, consider diversifying across various real estate sectors. Branching out into commercial real estate or exploring real estate investment trusts (REITs) can provide additional avenues for income and growth.

4. Continue Your Education

The real estate industry is continually evolving. By staying updated on market trends, attending seminars, and networking with other real estate professionals, you can adapt your strategy and seize new opportunities as they arise.

5. Scale Strategically

A real estate empire begins with just one property. With time, dedication, and a sound strategy, it’s possible to grow your holdings into a substantial full-time income. As you scale, ensure you’re not overextending; always prioritize the quality of investments over quantity.

Key Tips for Beginners

Embarking on a journey into real estate investing can be thrilling, yet the complexities of the industry can sometimes overwhelm beginners. Simplifying the learning curve is essential for novice investors to make informed decisions and find success. Here are some pivotal tips to guide those just starting out:

1. Start Small and Scale Gradually

Many millionaire real estate investors began their journey with a modest property. Purchasing a smaller, more manageable property as your first investment can help you navigate the nuances of the real estate business without being overwhelmed. As you gain confidence and experience, you can then venture into bigger and more diverse properties to scale your portfolio.

2. Prioritize Education

The world of real estate is vast and ever-evolving. Leverage online real estate platforms to learn about market trends, investment strategies, and financing options. Additionally, joining real estate investment groups can be invaluable. These groups not only provide mentorship but also offer opportunities to share resources, insights, and deals with other investors.

3. Location is Crucial

In the real estate realm, location often takes precedence over the type or condition of a property. A mediocre house in a prime location can fetch better returns than a grand mansion in a less desirable area. Research local market dynamics, neighborhood amenities, future development plans, and other location-specific factors before making an investment decision.

4. Networking is Key

Surrounding yourself with knowledgeable people can fast-track your learning process. By connecting with seasoned real estate investors, you can gain insights from their experiences, avoid common pitfalls, and even discover potential partnership opportunities. Attend local real estate seminars, join investor forums online, and participate actively in real estate conferences to grow your network.

5. Stay Updated and Adapt

The real estate industry is not static. Market conditions, property values, and investment strategies can change. Being adaptable and staying updated on industry trends will ensure you remain ahead of the curve and can capitalize on new opportunities.

6. Always Conduct Due Diligence

Before diving into any real estate transaction, thorough due diligence is imperative. From understanding property taxes and zoning laws to estimating potential repair costs and evaluating tenant profiles, leaving no stone unturned will protect you from potential setbacks.

8 Terms Beginner Real Estate Investors Should Know

Venturing into real estate can feel like you’ve entered a world with its own language. Don’t worry; everyone feels this way at the start. Knowing basic real estate terms can help you communicate confidently and make informed decisions.

Dive into these essential terms every beginner should grasp:

Appreciation: Appreciation is the increase in the value of a property over time. It’s one of the primary ways real estate investors make money, especially in growing markets. Appreciation can result from factors like inflation, increased demand, or improvements made to the property.

Capitalization rate (cap rate): Think of the cap rate as a tool to gauge the potential return on a property. It’s a percentage derived from comparing a property’s net operating income to its current market price.

Cash flow: This term captures the money dance – what’s coming in and what’s going out. In the context of rental properties, it means the rental earnings minus all the costs. Positive cash flow indicates you’re earning more than you’re spending.

Equity: Equity represents the value of ownership in a property. It’s calculated by taking the market value of the property and subtracting any outstanding mortgage or loans against it. As an investor pays down their mortgage or if the property appreciates in value, their equity in the property increases. This equity can be tapped into for various financial needs or reinvested.

Leverage: This term refers to the concept of using borrowed money, often in the form of a mortgage, to invest in real estate. It allows investors to purchase properties with a small down payment and finance the remainder. When used correctly, leverage can amplify returns, but it can also increase the risk if property values decline.

Net operating income (NOI): Simplified, NOI is the profit made from a property after deducting all operational costs. It’s your rental income minus all the expenses, showing the true earning potential of a property.

Real estate owned (REO): An REO property is one that didn’t sell at a foreclosure auction and is now owned by the bank. These properties are often sold at a lower price because banks aim to sell them quickly, making them attractive to investors.

Return on investment (ROI): In simple terms, ROI measures the bang you get for your buck. It’s calculated by comparing the profit you made to the amount you invested. The higher the ROI, the better your investment performed.

Conclusion

Real estate investing offers an avenue to diversify your portfolio, generate steady income, and potentially achieve long-term growth. With due diligence, a clear strategy, and the right team, beginners can successfully navigate the complexities of the real estate industry and lay the foundation for a prosperous investment journey. Remember, every millionaire real estate investor started with their first property. Your journey is just beginning.

In May 2021, the median price for a home was $350,300. That reflected a 23% increase year-over-year, demonstrating that the housing marketing was bustling after the impact of the COVID-19 pandemic. But it’s not just a rise out of the pandemic that has created a competitive housing market in 2021 and beyond. The record high in May 2021 followed 111 months of year-over-year gains, starting in March 2012.

In 2021 and 2022, the housing marketing has been awash in demand. But there aren’t enough homes to go around, leading to bidding wars and other challenges for buyers. Looking at this landscape, you may wonder, can you buy a house with bad credit?

The Challenges of Buying a Home with Bad Credit

Mortgage lenders look at a lot of factors to determine if you qualify for a home loan. Of course, your annual income and debts are crucial, but your credit score is also a significant factor. Applicants with great credit scores—750 or higher—tend to have an easier time getting approved for a mortgage and getting the most competitive interest rates available. Applicants with credit scores below 650 may have a more difficult time getting approved for a mortgage or securing low interest rates.

For a mortgage lender, all applicants present some sort of calculated risk. Lenders perceive those with higher credit scores as being at lower risk of foreclosure or defaulting on their home loans. As a result, people with high scores can get a lower interest rate and more favorable terms on a loan. Unfortunately, those with bad credit scores are automatically perceived to be a higher risk and—if they can get a loan—may end up paying higher interest rates and having to agree to less appealing terms that come with a bad credit mortgage.

COVID-19’s Impact on Buying a Home

The pandemic had some impact on the mortgage-buying process. That’s true for individual buyers as well as the entire process.

Get matched with a personal

loan that’s right for you today.

Learn

more

Homebuyers may have faced financial struggles during the pandemic, for example. Job or income loss could have led to difficulties paying bills or the need to take out loans to cover living expenses short-term. Those situations can impact credit and your ability to get a home loan.

At the same time, the Federal Reserve dropped interest rates in 2020 to help support the struggling pandemic economy. One result was that buying a house became very attractive, in part due to the lower overall cost of the loans.

Bad Credit in a Competitive Market

But now rates are increasing again—and may continue to rise throughout the year. Increasing rates may decrease competition between buyers, but they can make it more difficult for someone with less-than-great credit to buy a home for a number of reasons, including:

You may not be able to outbid others. Lenders may be willing to take a risk on someone with poor credit, but that risk is usually fairly limited. That means you may not be able to get approved over a certain amount, limiting how much you can pay for any home.

Your loan options may limit you. Buying a house with bad credit often means leveraging a government-backed loan, such as FHA or USDA loans. These loans must follow certain requirements about loan-to-value ratios, inspections and other steps to buying a home. In today’s housing market, having to stick to strict requirements can put you at a disadvantage.

Sellers may not choose your offer. Even if your offer is competitive, if you’re bidding with an FHA loan or other such financing, sellers may opt for a cash offer or one backed by a traditional commercial loan. Right or wrong, there’s some perception that cash or traditional loan offers are more likely to go through.

How to Buy a House with Bad Credit

It’s not all a lost cause, though. There are options for buying a home with poor or bad credit, such as Federal Housing Administration (FHA) loans. That’s true even in a competitive market.

FHA Loans

FHA loans have some of the most lenient qualification requirements. And they’re available to any homebuyer, not just first-time buyers.

To be eligible for an FHA loan, you need a credit score of at least 500. You’ll also have to meet other requirements, including appropriate debt-to-income ratios and not having certain types of open collection accounts in your credit history. Overall, you need to demonstrate to the lender that you’re reasonably able to pay the mortgage associated with the loan.

If you have a credit score between 500 and 579, the loan-to-value ratio is limited to a maximum of 90% on any FHA loan you might be approved for. That means you’ll need to come up with at least 10% of the purchase price as a down payment. For example, if you buy a home for $200,000, you’ll need at least $20,000 for the down payment.

If you have a credit score of 580 or above, you could be eligible for maximum financing. That means you may be able to get a loan with as little as 3.5% down.

VA Loans

Veterans Administration loans are available to military veterans and qualified spouses. The VA doesn’t set a specific credit score requirement for its programs, though it does state that borrowers will need to meet creditworthiness requirements. At the very least, the lender must determine that you have the means to pay the mortgage.

Some benefits of VA loans include:

They don’t necessarily require a down payment

No requirement for PMI, even if you don’t put down 20%

Competitive interest rates you might not be able to access elsewhere

USDA Loans

The United States Department of Agriculture offers mortgages to home buyers in eligible rural areas whose incomes fall in the low-to-average income range for their areas. The USDA doesn’t publish a minimum credit score requirement. It simply states that borrowers must have the willingness and ability to repay the loan, as demonstrated in part by their credit history. USDA lenders must look at three years of credit history.

Other Options

There are ways to increase your chances of getting approved for a mortgage with bad credit, even if you don’t want to go with one of the above government-backed options. Consider saving up for a larger down payment. A larger down payment reduces the amount you need to borrow and increases your likelihood of getting approved for a mortgage.

You may also be able to avoid the need for Private Mortgage Insurance with a higher down payment. Bypassing the need for PMI can easily save you $1,000 per year or more. It also frees up more money so you can pay down other debts, which can improve your credit.

Know Your Credit Score

If you’re thinking about trying to buy a home in the near future, the first step you should take is finding out where your credit stands. Begin by looking at your current credit reports and carefully reviewing them. Specifically, be on the lookout for any mistakes or errors on your report.

If you notice something incorrect on your report, you can file a dispute—most credit bureaus let you file a dispute online. You should also take the time to calculate how much of a mortgage you can reasonably afford before applying for one.

If you’re not sure what your credit score is, you can see your credit score for free on Credit.com. You also get a free credit report card that shows you ways to improve your credit score in each of the five areas that factor into how your score is calculated.

For even more information about where your credit stands, consider signing up for ExtraCredit®. You’ll get access to 28 of your FICO® scores, including the type of scores used by lenders to evaluate you as a mortgage borrower.

Once you know where you stand with your credit score and have done what you can to improve it, you can start shopping for mortgage rates and loans.

An FHA loan is a mortgage loan that’s provided under a program from the Federal Housing Agency (FHA), which is a part of the U.S. Department of Housing and Urban Development (HUD). These loans offer prospective homebuyers with lower credit scores and down payments the change to purchase a home. These loans are insured by the FHA, but they are not made by the FHA. Find out more about FHA loan limits, credit requirements, and other factors related to these mortgage loans below.

In This Piece

What Is an FHA Loan?

An FHA loan is a loan insured by the Federal Housing Administration. That doesn’t mean the FHA gives you the loan. You have to go through an approved FHA lender for this type of mortgage. The fact that FHA loans are insured by the federal government reduces some of the risk for lenders. That can make it easier, in some ways, for borrowers to get approved.

Difference Between an FHA Loan and Conventional Mortgage

The most popular—and perhaps most widely known—types of mortgages include conventional home loans, called conventional fixed-rate mortgages, and FHA loans.

Conventional home loans are not insured by a government agency, such as the FHA or the US Department of Veterans Affairs (VA loans). Conventional loans require credit scores of at least 620. In exchange for higher interest rates, you can put down as little as 3% for a conventional home loan. With a lower down payment, you’ll have to pay personal mortgage insurance (PMI) either upfront or monthly for a conventional home loan. And, a conventional loan has a higher interest rate and requires a lower debt-to-income ratio than an FHA loan.

An FHA loan, on the other hand, is insured by the FHA. People with credit scores as low as 580 can qualify, but down payments need to be 3.5% or higher. FHA loans require a mortgage insurance premium be paid upfront and as part of the monthly payment. Interest rates for FHA loans are lower than with a conventional loan. And borrowers can have higher debt-to-income ratios compared to borrowers using a conventional loan.

Get matched with a personal

loan that’s right for you today.

Learn

more

FHA Mortgage Loan

Conventional Mortgage Loan

Required Credit Score

500+ credit score

640+ credit score

Credit History Impact on Qualification

Shorter wait times after negative credit events, such as foreclosure, short sale, bankruptcy and divorce

Longer wait times after negative credit events, though some lenders may be flexible depending on circumstances

Typical Down Payment

As low as 3.5%

As low as 3%, with advantages for a larger down payment

Mortgage Insurance

Requires both a 1.75% upfront premium and 0.45%-1.05% annual premium

Unless you make a 20% down payment, you must buy private mortgage insurance. Usually this is included in the cost of the loan and can be canceled when you have 20% equity or more

Typical Interest Rate

Lower interest rates than a conventional loan for many borrowers

Potentially higher interest rates than an FHA loan, unless you have stellar credit and a large down payment

Required Debt-to-Income Ratio

Higher debt-to-income ratio acceptable

Lower debt-to-income ratio than an FHA loan

Types of FHA Loans

The FHA offers a number of loan programs you might be able to take advantage of:

FHA Loan Limits

How much you can finance with an FHA loan is limited. The exact figures depend on the location of the property and what type of property it is. You can use the US Department of Housing and Urban Development’s FHA mortgage limits tool to find out the numbers for your location.

The FHA mortgage limit floor in 2022 is $420,680, and the ceiling is $970,800.

Individual FHA loans are also limited by the value of the home being purchased. At most, you can get an FHA loan for the total value of the property in question. However, people with lower credit scores may not be able to borrow that much.

FHA Loan Credit Requirements

The minimum credit score requirement for an FHA loan is 500. If your score is less than 500, you can’t be approved for an FHA mortgage loan.

If your score is between 500 and 579, you can get an FHA loan, but you can’t be approved for maximum value. At most, lenders can approve you for up to 90% of the value of the home. That means you’ll need at least 10% as a down payment. It could be more depending on other factors, including your credit history, income, and current expenses.

If you’re buying a home for $200,000 with a low qualifying credit score, then, you might need to pay $20,000 or more as a down payment.

For borrowers with a score of 580 and higher, maximum financing is possible. Typically, that means a down payment of 3.5%. In the case of a $200,000 home, that would equal $7,000.

FHA Loan Documentation Requirements

When you apply for an FHA loan, plan on providing the lender with the following documentation:

Driver’s license

Social Security number

Last paycheck

W-2s for the past two years

Valid tax returns for two years

Bank, investment, and credit card account statements for three months

Signed and dated letters detailing any gift funds used to purchase the home, that must explicitly state that you don’t need to pay back the money.

There are no minimum or maximum salary requirements to qualify for an FHA loan. If your lender requires any additional documentation, they can walk you through the requirements to ensure you have everything in order.

FHA Loan Property Requirements

In addition to your required documentation, there are property requirements as well.

FHA loans can only be used for the primary residence of the borrower.

They cannot be used for second homes.

They cannot be used to buy investment property.

One of the homebuyers must occupy the home within 60 days of closing.

You can only use an FHA loan to buy a multifamily home (up to four units) if you plan to live in one of the units.

An FHA appraisal and inspection are required to determine the fair market value of the home.

They cannot be used to flip a home.

Benefits of FHA Loans

There are many potential benefits for FHA loans:

Lower credit score requirements than conventional mortgages

Fairly competitive interest rates

Lower down payment requirements than many other options

Shorter wait times after negative credit events, such as foreclosure, short sale, and bankruptcy

Certain fees may be lower on an FHA loan, too, particularly when it comes time to closing. The FHA loan program allows for coverage of some of those costs by the seller or another applicable third party.

Disadvantages of an FHA Loan

If your down payment is lower than 20%, the disadvantage you’ll face with an FHA loan is the MIP. Costs for MIP are typically higher than the private mortgage insurance (PMI) borrowers have to pay on conventional loans—especially when you account for the upfront MIP you’ll pay on an FHA loan.

The upfront MIP (UFMIP) fee is 1.75% of the base loan amount, which gets applied regardless of your loan term or LTV ratio. The annual MIP fee, paid in 12 monthly installments, depends on the terms of your loan and your loan-to-value ratio. Annual MIPs range from 0.45% to 1.05% of the amount you’re borrowing and your loan term.

MIP is harder to cancel than PMI on a conventional loan. Conventional mortgage lenders let you out of PMI once you pay your mortgage down to 78% of the home’s value at the time of purchase. Plus, you can ask your lender to cancel your PMI on a conventional loan early if you’ve paid your mortgage down to 80% of that original value ahead of schedule.

And, if you put a smaller down payment on an FHA loan, your mortgage payment will be higher than a conventional loan with a higher down payment.

COVID-19 and FHA Loans

The COVID-19 pandemic did have an impact on FHA loans. For example, HUD notes that while processing for FHA loans continued during the pandemic, changing remote worker situations could lead to delays. FHA loans, which are federally backed, also qualified for forbearance options during the pandemic. This provided some relief to homeowners struggling to pay their mortgages due to income loss. These specific relief measures have expired, but federally backed loans may see other benefits like this that conventional mortgages don’t qualify for.

For future buyers in the years after the COVID-19 pandemic, the biggest impact may be buying power. FHA loans require inspections and have rules about appraisals and prices that conventional loans don’t have. When bidding for homes in a competitive market—where cash buyers and those backed by conventional mortgages are bidding well above asking price—FHA buyers may find it harder to compete.

Should I Consider an FHA Loan?

The FHA loan program is great for borrowers who don’t have a lot of cash on hand for a down payment or need some flexibility when it comes to underwriting. That’s true for first-time home buyers and people buying their second or third homes too. It is also an ideal option for people with lower credit score—lower than the 620 minimum for a conventional loan.

If you do have the resources to make a large down payment and your credit score is in good shape, you may be better off going with a conventional home loan—given that you can skip the PMI.

Of course, regardless of type, you should only get a mortgage you can repay. Learn how much house you can afford as a starting point.

Prepare for Your House Hunt

The best way to arm yourself for house shopping—in any market—is to do your homework. Start by getting a look at your credit report and scores to avoid any surprises. Take time to build or repair your credit where possible before you apply for a mortgage. Then, look at your budget to figure out how much house you can afford.

Then browse options for mortgages to find competitive rates and a short list of lenders you want to work with. FHA loans are great tools, and they can be especially helpful for those with lackluster credit. But make sure you consider all your options before you settle on a loan.

While mortgage rates above 7% aren’t preferable, there are a few benefits to consider for borrowers.

Westend61/Getty Images

There’s no question that today’s housing market isn’t ideal for homebuyers. With numerous Federal Reserve rate hikes over the last 18 months, mortgage rates have skyrocketed.

The average 30-year fixed mortgage rate is now well above 7% — despite rates recently hitting a 3-week low. That’s well above the 2% to 3% rates that many homebuyers were getting in 2020 and 2021.

But while higher mortgage rates aren’t preferable, as they can dramatically increase the cost of buying a home, there are some upsides to the elevated rate environment. While you may think it’s best to wait for rates to drop, today’s elevated rate environment can actually offer some surprising benefits to homebuyers.

Explore the mortgage loan rates you may qualify for here.

4 ways today’s mortgage rates can benefit homebuyers

Here’s how today’s high mortgage rates can work in favor of those looking to purchase their dream home.

There may be less competition for available inventory

One of the main advantages of high mortgage rates is the reduced competition for homes. When rates are high, many potential buyers may choose to delay their home-buying plans, thinking they can secure a better deal later when rates potentially decrease. This means less competition in the market, which can be a golden opportunity for you — especially considering that home inventory remains low in many markets across the nation.

With fewer buyers vying for the same properties, you won’t have to worry as much about losing out on your dream home due to a bidding war. And, sellers may also be more open to negotiation. In turn, you could have a better chance of closing the deal at a price that suits your budget.

Learn more about today’s top mortgage rates here.

There may be more options for buyers

High mortgage rates can also lead to more choices for buyers. Not only are many people choosing to wait out the high rates in hopes that mortgage rates will decline, but it’s also harder to qualify for a loan when interest rates are elevated. In turn, homes are staying on the market longer in many markets, giving you more options — and more time to make a decision.

While some markets still remain hot, not all of them are. And, if homes are sitting for longer than they were in recent years, you’ll have a wider selection to choose from. With more options on the market, you’re more likely to find a home that ticks all the boxes on your wishlist — which may not have been possible during the buying frenzy when rates were in the 2% to 3% range.

The risk may be lower for buyers

In a competitive real estate market with low mortgage rates, buyers often face pressure to waive contingencies, like inspections and appraisals, in order to get their offer accepted by a seller. This heightened risk can be stressful and financially burdensome — and could lead to disaster in some cases.

However, when mortgage rates are high and competition is lower, buyers may have the upper hand. Sellers may be more willing to accommodate your requests, including allowing necessary contingencies. This reduces your risk and ensures you can make an informed decision about the property you’re purchasing.

Buyers still have the option to lower their rate over time

While today’s high mortgage rates may not be ideal for initial home financing, they come with the opportunity to lower your interest rate before closing — or over time. For example, you can explore options like buying down the rate on your home. Buying down the rate involves paying extra upfront to your lender to reduce your interest rate, which can save you money over the life of your mortgage.

You also have the option of refinancing when rates become more favorable. Rates are high right now, but it’s unlikely that they’ll stay that way forever. As economic conditions change, mortgage rates may decrease, allowing you to refinance your mortgage at a more attractive rate, potentially reducing your monthly payments.

The bottom line

High mortgage rates may seem like a disadvantage if you’re looking for a home to purchase right now, but they can actually offer numerous benefits to buyers. With less competition, a broader range of choices, reduced buyer risk and the potential to improve your mortgage terms later, today’s high rates can work in your favor. So, if you’re in the market for a new home, don’t be discouraged by the numbers. Embrace the advantages they bring and make the most of this unique opportunity.

Building your own place can be immensely fulfilling. And you should end up with exactly the home you wanted. But you often need a flexible timeline and deep pockets.

How can you finance a land purchase and construction project? Should you even try? Read on to see what your best options could be.

Find your lowest mortgage rate. Start here

In this article (Skip to…)

The cost to build a house

In 2022, a new home in the U.S. cost $392,241 to build on average, according to the National Association of Home Builders (NAHB). However, that excludes the cost of buying and financing the land on which you wish to build. With that added in, you may well be looking at something north of $500,000.

Of course, those costs can vary significantly depending on where you live. Some states and areas have vastly more or less expensive land prices and labor costs. Even the costs of materials can differ across the country.

Check your home buying options. Start here

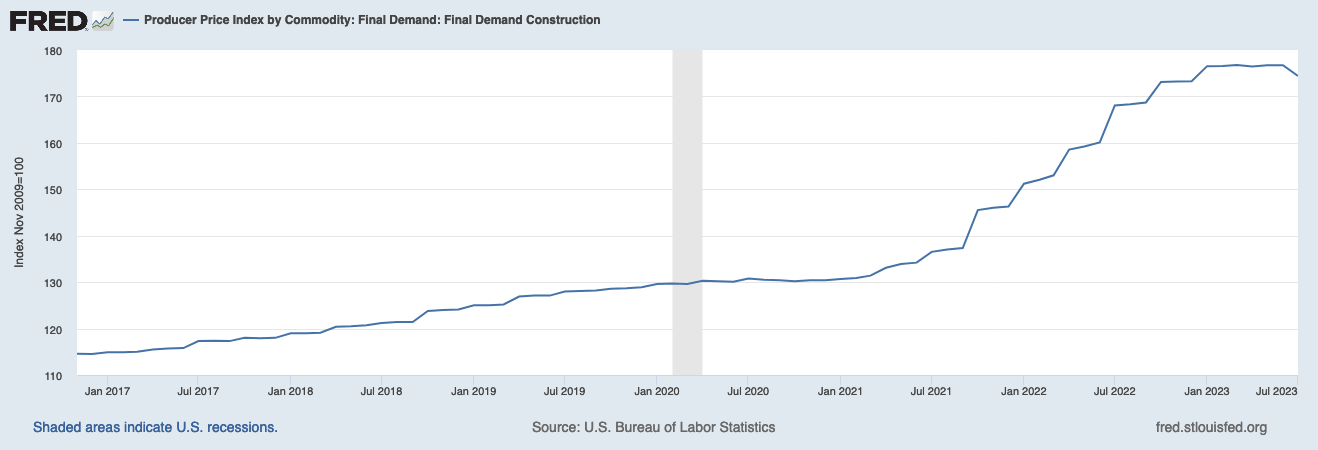

Inflation weighed heavily on construction materials in recent years. The following graph from the Federal Reserve Bank of St. Louis suggests price pressures were easing by July 2023. So comparing a friend’s new build from a few years ago may not be a good barometer for new construction now.

Many (probably most) of the homes in the NAHB study were likely built as part of large developments comprising dozens or hundreds of homes. We excluded developers’ costs, such as financing, marketing, sales commissions and profits from the numbers we cited. Large developers also may enjoy economies of scale on labor and materials costs that won’t be open to you on a single project. So, use the NAHB’s figures only as a very rough guide when calculating your own cost to build a house.

Breakouts of the costs associated with each building stage

The NAHB breaks down those average 2022 costs by different elements in the process:

Find your lowest mortgage rate. Start here

Site work (fees for permits, impact, inspections, architects and engineers): $29,193

Major systems (plumbing, electrical, HVAC and other): $70,149

Interior finishes (everything to bare-wall finish, including kitchen, bathrooms and appliances): $94,300

Final steps (landscaping, outdoor structures, driveway, clean up …): $23,065

Unspecified others: $6,059

Remember, those are only the elements that make up the average cost to build a house of $392,241. Read on for why your costs could be much higher or lower.

Factors that can change the cost to build a house

An endless list of things can make your home-building project’s costs vary from the average. Some of the biggest include:

Find your lowest mortgage rate. Start here

Location — Labor costs and land prices aren’t consistent across the country, with some states and areas significantly more or less expensive than others. Urban settings generally have higher costs than rural ones

Isolation — You may dream of living far from the general public or off the grid entirely, but you’ll likely pay more for materials and labor to travel there

Site conditions — If your construction site isn’t easily accessible for heavy machinery and deliveries, you’ll have to pay for it to be made so. If it’s steeply sloping or hard to excavate, that, too, will add to your costs

Square footage — A sprawling McMansion can cost 10 or 20 times as much to build as a tiny house. The NAHB study says the average home comprised 2,561 sq. ft. in 2022. So, scale up or down from that

Finishes — Will you be importing slabs of Italian marble and several antique fireplaces and fountains from Europe? Or will you rely on Home Depot and your contractor’s trade accounts for your finishes? The price difference could run from the thousands into millions

Amenities — Do you want a pool, firepit, hot tub, home theater, gym, games room, indoor basketball court, and a dedicated gift-wrapping room? Those luxuries will cost extra

It’s good to have an average homebuilding budget as a starting point. But you’re going to have to make a lot of adjustments as your plans evolve.

Ways to finance a newly constructed home

Unless you have serious funds squirreled away, you’ll likely have to borrow to finance the purchase of your land and to pay for your construction project.

Check your home loan options. Start here

You have a dizzying array of options, including:

Land loans (aka lot loans) — Especially useful if you want to hold the land for a while before developing it

Home equity loans — Borrow a lump sum secured by the equity (the amount by which the value of your home currently exceeds your mortgage balance) in your existing home. You repay in equal installments over a period that you largely set

Home equity lines of credit (HELOCs) — Again, you’ll need plenty of equity in your existing home. You get a line of credit, meaning you receive a credit limit and can draw up to that amount. You pay interest only on your balance so these can be good for short-term borrowing or longer-term projects where costs arise over time

Personal loans — No collateral required. But you’ll typically need an uber-high credit score and very sound finances to get a competitive rate

Construction loans — These short-term loans can be combined with land loans to finance the whole process of getting you into your custom home. You can then refinance both into a new mortgage. Or you can opt for a “construction-to-permanent loan,” which lets you pay for everything with a single closing on your mortgage

For many homebuyers, a construction-to-permanent loan is the obvious choice. Popular ones of these are government-backed, by the FHA, VA or USDA. And that means you need only a small (3.5%) or no down payment. You also don’t need a stellar credit score to get approved.

Who offers these loan types?

There’s no shortage of lenders of home equity loans, HELOCs or personal loans. Nearly all mortgage lenders offer the first two, and plenty of banks and specialist lenders offer the third.

However, land loans and construction-to-permanent loans are a different matter. They’re specialist loans that many lenders — with otherwise wide portfolios of mortgage products — won’t touch them.

But don’t despair! They’re out there. You just have to track them down.

Is building a home right for you?

Building your own home isn’t for everyone. But the advantages of doing so are immense.

Most importantly, you get to choose everything: from the building style and layout, to every detail of the finishes. That means you get a sense of complete ownership that evades many who buy an pre-designed home from a developer.

Check to see what mortgage rate you qualify for. Start here

But there are disadvantages. First, the cost to build a house is often higher than buying an existing home. Then there’s the hassle. Even if you employ a project manager, there will be endless details that only you can decide upon. And, of course, you could face frustrating delays and cost overruns. If you’re impatient or on a tight budget, you could save a lot of headaches by opting for an existing home.

The bottom line: Cost to build a house

Don’t underestimate the challenges and costs of building a house. But also don’t underestimate the sheer joy of living in a home that’s been custom-built to meet your needs.

It’s like commissioning a tailor-made suit or gown that fits you precisely. You look great and feel comfortable. Of course, this tends to come at a higher price — both the dollar costs and the probability of unexpected budget and timeline changes.