Searching for a new apartment often takes a lot of time and research; in fact, it can be disheartening if you have a hard time finding an apartment you love. And that’s why winter is the best time to rent an apartment. You might be surprised at how easy it is to discover your next apartment, one that you can’t wait to turn into a home.

1. There often is lower demand in the winter

It’s no secret people love to move in the summer. The weather usually is great, the kids are out of school for families looking to relocate and there often is less demand on our time for other activities. In fact, 40 percent of all moves occur in the summer, with just 5% taking place in November and December. As a result, apartment shoppers can find some great apartments for rent, particularly new apartments that may be completed during the season.

2. You could find more options for apartment size, style

In tandem with lower demand, renters may find there is a wider variety of apartment sizes and styles available during the winter than in other seasons. Because demand is lower, it might be easier to find that two-bedroom apartment you wanted instead of having to settle for a one-bedroom unit. This also applies to those new apartments that are completed during the winter. That means you could land a great apartment with new appliances, updated finishes and special spaces such as a sunroom or screened porch.

3. There could be more availability with movers

Because people don’t move as often during the winter, you may be able to book your movers on your timetable instead of having to wait for one to become available. This is important so you can schedule the movers around your commitments and work schedule and don’t have to use valuable personal or vacation days for moving instead. Also, during this slower season, movers may not be as rushed, so might be less likely to damage your items.

4. You could have more time off to move

No one wants to spend their personal or vacation days moving instead of on a much-needed vacation. When moving in the winter, particularly around the holidays, you likely could have extra days off that won’t interfere with your PTO or vacation days. Although no one wants to spend their holidays moving, it could prove beneficial if you don’t have to take off extra time at work.

5. You could snag an apartment when a fall graduate vacates

Looking for an apartment near a college campus could be especially challenging because many, if not most, apartments are already booked from September through May. However, if you are moving to a college town during the winter, particularly in December or January, you could score an apartment when a fall graduate prepares to move out. After all, no landlord wants an apartment to sit empty until the new students arrive in August or September.

6. You could save money

While you may not be looking for a less expensive apartment, you could still score one during the winter. No landlord wants a vacant apartment, so it’s not uncommon for them to run rent specials during the winter when demand is low. This could range from waiving the security deposit to offering a free month of rent to reducing rent for the entire term of the rental agreement.

7. It’s a good time to negotiate preferred rental terms

Because landlords want to rent empty apartments during the winter, the tenant is in a good position to negotiate the rental agreement terms. This could include asking for a shorter- or longer-term lease, waiving fees such as those for pets or upgrading the appliances in the unit. If there’s something you want, now is the time to ask. The worst that could happen is the landlord says no.

Yes, winter is the best time to rent an apartment

As you can see, renting an apartment during the winter could provide many benefits, so don’t hesitate to start looking for a new apartment when the weather turns cold. You could end up scoring a hot deal on your next home.

Alicia Underlee Nelson is a freelance writer and photographer. Her work has appeared in Thomson Reuters, Food Network, USA Today, Delta Sky Magazine, AAA Living, Midwest Living, Beer Advocate, trivago Magazine, Matador Network, craftbeer.com and numerous other publications. She’s the author of North Dakota Beer: A Heady History, co-host of the Travel Tomorrow podcast and leads travel and creativity workshops across the Midwest.

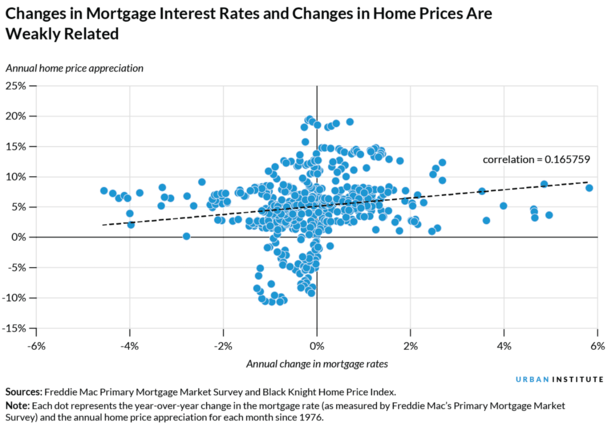

If you don’t believe mortgage rates and home prices can fall together, just look at what home prices have done in the face of 7% mortgage rates.

Despite the 30-year fixed surging from sub-3% levels to near-8% levels in less than two years, home prices hit fresh all-time highs.

So why is it so difficult to imagine the opposite scenario, where both interest rates and property values fall in tandem?

It seems the human mind wants there to be an inverse relationship between rates and prices when there often is not.

The good news is it’s possible that both rates and prices moderate from here, ushering in a better level of housing affordability.

Home Prices and Mortgage Rates Don’t Have Much of a Relationship

The Urban Institute wrote an article last year about the relationship between home prices and interest rates when mortgage rates were rapidly ascending.

They noted that since 1976, there has been “a positive but weak relationship” between the two.

In other words, higher mortgage rates are often accompanied by higher home price appreciation, though this tendency isn’t robust.

Still, it defies the logic many housing bears and everyday humans possess, where they assume higher mortgage rates must equate to lower home prices.

After all, if it becomes more expensive to purchase a home, the price must come down. That’s their argument at least.

But when you look at other necessary items (shelter also being a necessity), people don’t stop buying them because the cost goes up.

And one also needs to consider why mortgage interest rates are high to begin with. Often, interest rates are high because the economy is running hot.

This means there are more consumers out there making more money, which ostensibly means more of them can afford to buy expensive houses.

One other factor to consider is all-cash buyers – a large percentage of home buyers forgo mortgages to get the deal done, especially investors.

So while higher interest rates might affect the average home buyer, they don’t affect everyone.

Home Prices and Inflation Have a Strong Positive Relationship

While higher mortgage rates and home price appreciation have a weak, but still positive relationship, inflation and home price appreciation have a strong one.

That is to say that a higher rate of inflation is associated with higher home price appreciation.

And this association is significantly stronger than the relationship between mortgage rates and home prices.

Inflation has been front and center for the past couple years, and the Fed has been actively fighting it via 11 fed funds rate hikes since early 2022.

At the same time, home prices haven’t fallen, though the rate of appreciation has. Still, when you consider the 30-year fixed more than doubling in such a short time span, you’d expect housing market carnage.

Instead, we’ve seen home prices hit new all-time highs. Last week, the FHFA reported that home prices were up 0.8% in July from a month earlier, and up 4.6% year-over-year.

While that might sound too good to be true, consider that high interest rates are often correlated with periods of strong economic growth, low unemployment, rising wages, and high inflation.

Put another way, when the economy is hot, home prices tend to rise because more people have money and jobs to support mortgage payments, even if they grow larger.

This means housing demand can increase or at least remain steady, even if affordability erodes over time.

Housing Affordability at Its Worst Since 1984

Of course, affordability has worsened significantly of late because both rates and prices have continued to rise, pushing the national payment-to-income ratio to its highest level since 1984.

Per Black Knight, it takes a $2,423 principal and interest payment to purchase the median-priced home with 20% down and a 30-year fixed mortgage.

This is up 91% from $1,155 just two years ago, when the Fed ended Quantitative Easing (QE) and began their campaign known as Quantitative Tightening (QT).

Clearly this has slowed home price appreciation, which had been running at a double-digit clip. But as noted, prices keep on rising.

Nominal Home Prices Are Sticky and Rarely Fall

The Urban Institute noted that mortgage rates have mostly just declined since 1976.

There have only been a few periods when rates increased more than 1.5 percentage points year-over-year.

However, rates did rise rapidly from September 1979 to March 1982 (remember those 1980s mortgage rates) and from September 1994 to February 1995.

This caused the rate of home price appreciation to slow quickly, similar to what we saw lately.

During that 1979 to 1982 mortgage rate rise, home price appreciation decelerated from 12.9% to just 1.1%.

And from September 1994 to February 1995, it slowed from 3.2% to 2.6%.

During each of these time periods, real home price appreciation (adjusted for inflation) went negative, but nominal home prices only went negative once a recession was under way.

In other words, you need the economy to fall apart if you want home prices to come down. And guess what could also come down at the same time?

What About Falling Home Prices Combined with Lower Mortgage Rates?

So we’ve discussed how home prices and mortgage rates can rise together, though the relationship isn’t a strong one.

But that a robust economy tends to lift home prices higher, as has been the case over the past many years.

If that’s true, can’t the opposite also be correct? Can’t mortgage rates and home prices fall at the same time, perhaps because of disinflation and a cooling economy?

The answer is yes they can. If and when the economy takes a turn for the worse, the Fed could pivot and begin cutting its own policy rate.

At the same time, mortgage rates could retreat from recent highs and make their way lower as well.

And home prices could also begin to fall as a recession sets in, resulting in job losses, pay cuts, higher unemployment, and lower housing demand.

This counters the notion that mortgage rates back in the 4-5% would set off another housing market frenzy filled with bidding wars and rapidly appreciating prices.

Simply put, if home prices and mortgage rates can rise together, they can also fall together.

Ideally, we see moderation on both fronts, with home prices maybe pulling back from recent highs, at least on a real, inflation-adjusted basis, while mortgage rates also ease.

This could help to tackle the affordability issues currently plaguing the housing market.

Just remember though that the other big problem is supply. There simply aren’t enough homes for sale, and as we all know, scarcity leads to higher prices.

Interest rates can have a real impact on inflation. Learn how it works and what changing interest rates could mean for you.

October 3, 2023

When inflation is on the rise, everything from groceries to gas can get more expensive. And while a little inflation is normal, the Federal Reserve Board (also known as “the Fed”) tries to prevent steep increases in prices. Inflationary spikes can occur due to several factors, including supply chain issues, a booming labor market, and a low interest rate environment.

The Fed monitors inflation by tracking the average costs of goods and services. One of the most relied-upon measures of inflation is the Consumer Price Index (CPI), which looks at common expenses like food, energy, transportation, shelter, and health care.

When inflation is high, as it was in 2021 and 2022—with the headline number peaking in June 2022 at 9.1%, per a Bankrate article citing the Bureau of Labor Statistics (BLS)—consumers’ dollars don’t go as far because goods and services are more expensive. This not-so-fun reality tends to put a damper on economic growth, and people with a lower income are disproportionately burdened because they cannot afford higher prices. But it’s not a great situation for anyone.

So, how does raising interest rates affect inflation? Let’s start with why inflation can happen in the first place.

Why is inflation so high?

The pandemic sparked a chain of events—including supply chain disruptions, disruptions in production, and pandemic stimulus packages, per Bankrate—that helped lead to the inflationary spike between 2021 and 2022.

First, the global supply chain, which encompasses all stages of manufacturing, assembly, and logistics that make it possible for goods to be delivered around the globe in a timely fashion, was severely impacted by illness, business closures, and travel restrictions, per Bankrate. Simultaneously, demand for goods increased as people—many working from home—began ordering more things online to be shipped directly to their front doors.

It’s economics 101: When demand goes up and supply goes down, prices rise. And that causes inflation.

Then, as the pandemic started to ease, another event that would lead to price shocks occurred: Russia’s invasion of Ukraine. Russia is a major supplier of the world’s oil. As more countries placed war-related sanctions on Russia, oil prices rose—a lot. According to Bankrate, the price of a barrel of oil nearly doubled from February 2022 (when the war began) to July 2022.

Meanwhile, the upward trajectory of a robust job market and a roaring stock market in the U.S. meant that many consumers could afford to pay higher prices at the stores and the pumps. This combination of forces can propel prices even higher and keep economists and policymakers at the Fed up at night.

Luckily, the Fed has a tool to combat runaway inflation: interest rates.

What happens to inflation when interest rates rise?

The Federal Reserve’s job is to keep inflation manageable so that consumers are encouraged to spend and save. Interest rates—which represent the cost of borrowing money—are reflected in the annual percentage yields (APYs) of savings accounts and mortgage rates. (Learn more about how the Federal Reserve can affect mortgage rates.)

How does raising interest rates affect inflation?

When interest rates go up, borrowing money gets more expensive. How does this increase in interest rates affect you? Mortgages, car loans, and business loans aren’t as attractive. As a result, fewer consumers are willing to take out loans to buy or invest in things. Higher interest rates tamp down demand, which usually leads to a dip in prices as well.

Consumers are affected in other ways, too. Because interest rates on savings accounts, certificates of deposit (CDs), and money market accounts tend to increase, people move more of their money into these savings products to reap the benefits. Here’s how raised interest rates can affect those different accounts:

Savings Accounts

Banks’ interest rates typically track what the Federal Reserve is doing. So if you’re wondering when savings account interest rates will go up, it’s usually after a Fed rate hike. Money in a high-yield savings account during periods of higher interest rates will yield more returns as your funds compound over time.

CDs

CDs offer a guaranteed interest rate for the entire term of the CD, no matter what is happening in the stock market or if interest rates are rising (or falling). That said, these savings vehicles are especially beneficial when CD rates are high because you can lock in that rate over a set period—typically between three months and 10 years.

Choose your term, lock in your rate, and watch your CD grow

Discover Bank, Member FDIC

Money Market Accounts

Money market accounts also benefit from higher interest rates. They can feature an APY that’s competitive with savings accounts, but they can also include a debit card like a checking account for easy access to your money. To get the most out of a money market account, choose one with a high APY that doesn’t include fees.

When will inflation go down?

Inflation doesn’t last forever. In fact, after a series of interest rate hikes by the Fed, inflation had simmered down to 3% by June 2023, its lowest since March 2021, according to the BLS.

Economic experts predict, however, that inflation could continue through 2024, according to Bankrate. And the Federal Reserve may raise interest rates at least once or twice more, according to a Bankrate poll.

Keep saving through the ups and downs of inflation

Though no one knows for sure when inflation will go up or down, here’s one piece of advice that’s always wise during uncertain economic times: Stay the course. That means continuing to save for retirement and spend money wisely to make your financial goals a reality.

Looking for a safe place to keep your savings that also offers a high interest rate so your money can grow over time? Look no further than a high-yield online savings account.

Articles may contain information from third parties. The inclusion of such information does not imply an affiliation with the bank or bank sponsorship, endorsement, or verification regarding the third party or information.

Could a collapse in the U.S. housing market wreck the nation’s economy in 2023-2024, like it did in 2008? Financial experts are publishing their predictions amid a troubling backdrop of elevated home prices and high mortgage rates. Some of these forecasts are quite alarming, to say the least.

Surely, you’ll recall the Federal Reserve hinting at a “higher for longer” interest rate policy at last month’s Federal Open Market Committee (FOMC) meeting. The upward pressure on mortgage interest rates has been unmistakable. This begs the question of what’s in store for the housing market and how stock investors can prepare for what’s coming.

Housing Market Alert: Expect Home Prices and Mortgage Rates to Rise in 2024

As we embark on the final quarter of 2023, all eyes are turning to 2024. Understandably, people want to know what to expect in the housing market. Suffice it to say home prices and mortgage rates are very likely to increase.

They’re already elevated, to put it mildly. Believe it or not, the median sale price of an existing home in the U.S. reached $406,700 in July. That figure is only $7,000 less than the all-time high.

Furthermore, the average annual interest rate for a 30-year mortgage reached 7.36% in late August. And with few signs that the “higher for longer” interest rate policy will end soon, housing could become even less affordable.

So, what are the experts predicting? National Association of Realtors (NAR) Chief Economist Lawrence Yun expects home prices to increase by around 3% to 4% in 2024. Meanwhile, the supply of houses is “likely to remain below what we would deem a balanced market,” according to Chen Zhao, who leads the economics team at Redfin.

Experts with Zillow see home values increasing by 3.4% in 2024. Moreover, the National Association of Home Builders anticipates that America’s housing shortage will persist through the end of this decade.

On the other hand, Moody’s Analytics and Morgan Stanley both expect that U.S. home prices will decline slightly in 2024. This just goes to show that consensus is, as always, hard to find on Wall Street.

What You Can Do About It

Should you prepare for a housing market collapse in 2024? Not necessarily, though real estate buyers and sellers need to factor in elevated home prices and mortgage rates.

This might involve altering your budget for the next year. At the same time, it’s not a bad idea to cut back on real estate stocks. Two clear-cut examples would be Realty Income (NYSE:O) and Rocket Companies (NYSE:RKT). Finally, always keep an eye on the Federal Reserve for hints about future interest rate policy changes.

On the date of publication, David Moadel did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

David Moadel has provided compelling content – and crossed the occasional line – on behalf of Motley Fool, Crush the Street, Market Realist, TalkMarkets, TipRanks, Benzinga, and (of course) InvestorPlace.com. He also serves as the chief analyst and market researcher for Portfolio Wealth Global and hosts the popular financial YouTube channel Looking at the Markets.

Editor’s Note: For the latest developments regarding federal student loan debt repayment, check out our student debt guide.

What happens if I miss a student loan payment? That’s the question on many borrowers’ minds as federal student loan payments resume after more than three years of emergency forbearance.

Missing payments on student loans can have a variety of negative consequences, including damage to your credit score and wage garnishment. However, the Biden administration is offering a temporary “on-ramp” to ease the transition back into repayment. Until the end of September 2024, borrowers will not have to worry about their student loans falling into default or damage to their credit score if they miss payments.

Interest will continue to accrue during this time, though, and any missed student loan payments will be due eventually. Rather than ignoring your student loan bills, take some time to review your options for making them more affordable. The Department of Education offers various plans to help struggling borrowers get back on track.

What Happens if I Miss a Federal Student Loan Payment?

Missing federal student loan payments typically leads to delinquency and default, but from October 2023 through September 2024, borrowers who miss a payment will avoid these consequences. Here’s a closer look at what this student loan on-ramp entails, followed by what typically happens when you miss payments.

Understanding the Student Loan On-Ramp

Federal student loan borrowers have been exempt from student loan payments and interest since March of 2020. With the end of this emergency forbearance, the Biden administration is offering a one-year on-ramp for borrowers to adjust to the new reality. Until Sep. 30, 2024, borrowers won’t face the usual consequences if they miss payments.

For example, your loans won’t fall into delinquency or default, and missed payments won’t be reported to the credit bureaus. Your loans won’t go into collections, and you won’t have to worry about garnishment of your wages, tax refund, or Social Security benefits.

What’s more, the interest that accrues during this year won’t be capitalized, or added onto, your principal balance when the on-ramp expires. This on-ramp gives borrowers time to start making payments again after the lengthy pause.

However, interest will still accrue during this time, and you’ll still have to pay back your loan eventually. Instead of skipping payments over the next year, you may be better off applying for an income-driven repayment plan for more affordable monthly bills.

What Normally Happens When You Miss a Student Loan Payment

Normally, your student loan is considered delinquent the day after you miss a payment. Even if you start making the next payments, your account will remain delinquent until you make up for the missed payment or receive deferment or forbearance.

Once 90 days pass, your loan servicer will let the major credit reporting agencies know that your loan is delinquent. Your credit score will take a hit, making it more difficult to qualify for good terms on loans or credit cards or to rent an apartment.

If you continue not paying, your loan will go into default. For federal loans, the government will wait 270 days. Defaulting on your student loan has serious consequences. The entire amount you owe on your loan, including interest, becomes due immediately.

You won’t be able to take out any other student loans, and you’ll no longer qualify for deferment or forbearance or be able to choose your own mortgage, car loan, or other forms of credit. The government may take your tax refund or federal benefits to pay off your loan. You may also have your wages garnished, meaning your employer will take part of your paycheck and send it to the government to be applied toward the loan.

It’s rare, but the government can also sue you at any time — there’s no statute of limitations. You may also be responsible for collection fees, attorney’s fees, and other costs. In other words, you do not want to default on your student loans. (If you do, options exist for getting out of default, such as the Fresh Start program.) 💡 Quick Tip: Get flexible terms and competitive rates when you refinance your student loan with SoFi.

What Happens if I Miss a Private Student Loan Payment?

Private lenders usually give you much less leeway than the federal government. Exactly what happens if you miss a payment depends on the company’s policies and your loan terms. A private lender can tack on late fees and transfer your loan to a debt collection agency.

Also, private lenders can sue you if you stop paying your student loans. If they win, a court can sign a judgment allowing them to garnish your wages. States set the statute of limitations for lawsuits about payment of private loans; the time period usually ranges from three years to a decade. But the lender can continue trying to collect the debt for as long as they want. Plus, certain actions can reset the statute of limitations, such as making a payment or even acknowledging that the debt belongs to you.

Will My Loans Eventually Go Away if I Can’t Pay?

If you stop paying your student loans, they will not go away. However, it may be possible to discharge student loans in bankruptcy or qualify for student loan forgiveness or discharge.

For example, federal student loans can be discharged if you suffer from a total permanent disability or your school closes while you’re attending or soon after you leave. You can also pursue student loan forgiveness programs, such as Public Service Loan Forgiveness or Teacher Loan Forgiveness.

Student loan cancellation from an income-driven repayment plan may also be an option. Income-driven plans will discharge your remaining student loan balance at the end of your term. While the term is 20 or 25 years for some plans, the new SAVE plan will offer forgiveness after 10 years if your original principal balance was $12,000 or less. On all the income-driven plans, it’s possible that your monthly payment could be $0, depending on your discretionary income.

For instance, borrowers who earn less than $32,800 as individuals or $67,500 as a family of four in most states could have $0 monthly payments on the SAVE plan. If this describes you, you could essentially stop paying your student loans and see them go away after anywhere from 10 to 25 years on the plan, depending on how much you borrowed and whether you took out the loans for undergraduate or graduate school.

However, you’ll have to apply for income-driven repayment and recertify your income annually to stay on the plan and keep making progress toward loan cancellation. If you give the Department of Education permission to access your tax information, it can recertify your plan automatically each year.

What if I’m Experiencing Financial Hardship?

If you are having a tough time with your finances or are putting off making a late student loan payment, don’t just ignore your loans; instead, approach your lender or loan servicer to discuss your options.

For federal loans, an income-driven repayment plan could help. Income-driven plans, which include SAVE, PAYE, Income-Based Repayment, and Income-Contingent Repayment, adjust your monthly payments based on a percentage of your discretionary income. Most also extend your loan terms and offer loan forgiveness if you still owe a balance at the end. The new SAVE plan particularly has the most generous terms for borrowers.

You might also be able to qualify for a deferment or student loan forbearance, allowing you to temporarily stop or reduce payments. If you’re in deferment, depending on the type of loan you have, you may not be responsible for paying the interest that accrues during the deferment period. Among other reasons, you can apply for deferment if you’re in school, in the military, unemployed, or not working full-time.

You can apply for forbearance if your student loan payments represent 20% or more of your gross monthly income, if you’ve lost your job or seen your pay reduced, if you can’t pay because of medical bills, or if you’re facing another financial hardship, among other things. Private lenders are not required to offer relief if you’re facing hardship, but some, including SoFi, do.

Will I Be Sent to Collections if I Do Not Pay My Student Loans?

It is possible that if your student loan is in default it may be sent to a collections agency. Federal student loans in default are managed by the Department of Education’s Default Resolution Group. The Default Resolution Group oversees collections for all federal student loans that are in default, so they are not sent to a private collections agency.

The Department of Education is temporarily offering a Fresh Start program for student loans in default. By calling your loan servicer or logging into myeddebt.ed.gov, you can get your loans back into active repayment, enroll in a new repayment plan, and have the record of default removed from your credit report. You’ll also regain access to federal financial aid.

Private student loans may be sent to a collection agency as soon as the loan enters default, which is generally after 90 days of non-payment.

What if I Don’t Expect My Situation to Change Anytime Soon?

Deferment, forbearance, and relief offered by private lenders are temporary solutions. If your financial hardship looks like a long-term issue, you’ll need a permanent fix.

With federal loans, you may be eligible for an income-driven repayment plan. The government currently offers four plans that aim to make payments affordable by tying them to your monthly income.

On most plans, the payments range between 10% and 20% of your discretionary income, and if you make them on time, the balance is eligible to be forgiven in 20 or 25 years.. As mentioned, though, the new SAVE plan may offer loan forgiveness after just 10 years, depending on your original loan balance. Plus, starting in July 2024 it will cut monthly payments on undergraduate loans in half. For most borrowers, the SAVE plan will likely offer the most affordable monthly payments. However, parent loans are not eligible for SAVE. If you’re a parent borrower, your only option for an income-driven plan is Income-Contingent Repayment.

Private student loans are also not eligible for income-driven repayment, and most private lenders don’t offer this option. If you’re struggling to afford your private student loan bills, though, it’s worth explaining your situation to the lender and seeing if they can work with you on a feasible repayment plan. It’s in their interest to continue collecting even partial payments from you, rather than seeing payments stop altogether and having to go through the trouble of lawsuits or referrals to collection agencies.

Why You May Want to Consider Refinancing

Another potential long-term solution to unaffordable payments is student loan refinancing. With a private lender like SoFi, you can refinance federal student loans, private loans, or both. Refinancing involves obtaining a new loan to pay off all of your old ones and committing to the new terms and interest rate.

Refinancing your student loans can make sense if you qualify for a lower interest rate, which, depending on the term you choose, may be able to cut down the money you spend in interest over the life of your loan. Or, if you choose a longer term than you originally had when refinancing, you could lower your monthly payments, which can make the loan more affordable for you now. You may pay more interest over the life of the loan if you refinance with an extended term.

When you refinance with SoFi, you won’t pay any origination fees to refinance, and if your financial situation improves down the line and you want to pay off your loan faster, you won’t face prepayment penalties. It takes just two minutes online to figure out whether you qualify and the potential rates you can obtain.

The Takeaway

Missing student loan payments can have serious consequences, including entering default and damaging your credit score. Fortunately, borrowers have some leeway through September 2024 as they adjust to making payments on their federal loans again. However, private student loans offer no such benefit.

Refinancing could be an option to consider for borrowers looking to secure a lower interest rate. Consider SoFi — where there are zero fees for refinancing student loans and qualifying borrowers can secure a competitive interest rate.

Hoping to get a handle on your student debt? Look into whether refinancing your student loans with SoFi could help you lower your payments or save money in the long term.

FAQ

What happens if I’m late on a student loan payment?

If you are late on a student loan payment, the loan may be considered delinquent. The loan will remain delinquent until a payment is made, or other arrangements — such as deferment or forbearance — are made. Through Sep. 30, 2024, missing payments on your federal loan payments won’t cause them to go into delinquency or default thanks to the student loan on-ramp.

Does a late payment on a student loan affect credit?

A late payment may have a negative impact on your credit score. With the exception of the student loan on-ramp through the fall of 2024, federal loans are normally reported to the credit bureau if they remain delinquent for 90 days. Private student lenders may report a late payment to credit bureaus after 30 days.

What happens if you miss a student loan payment by 270 days?

If you fail to make payments on your federal student loan for 270 days, the student loan will enter default (again, with the exception of the temporary student loan on-ramp). Consequences of default can be serious, such as the total balance of the loan becoming due immediately.

Private student loans may be considered in default after 90 days.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Student Loan Refinancing If you are a federal student loan borrower you should take time now to prepare for your payments to restart, including the opportunity to refinance your student loan debt at a lower APR or to extend your term to achieve a lower monthly payment. (You may pay more interest over the life of the loan if you refinance with an extended term.) Please note that once you refinance federal student loans, you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as the SAVE Plan, or extended repayment plans.

SoFi Private Student Loans Please borrow responsibly. SoFi Private Student Loans are not a substitute for federal loans, grants, and work-study programs. You should exhaust all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

SoFi Private Student Loans are subject to program terms and restrictions, and applicants must meet SoFi’s eligibility and underwriting requirements. See SoFi.com/eligibility-criteria for more information. To view payment examples, click here. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Gross Domestic Product, or GDP, is an economic measure representing the total value of all goods and services that a country or region produces in a specific time period, usually a quarter or a year.

The GDP of the United States was $26.49 trillion at the end of Q1, 2023, an increase of 1.3% over the previous quarter, according to the Department of Commerce’s Bureau of Economic Analysis (BEA).

GDP can serve as a quick, numeric shorthand for explaining a country’s economy’s trajectory, and investors can use it as a factor, along with market trends and other analysis, in making their investing decisions. It’s important for investors to know more than just the definition of GDP in order to have context about what the number truly means.

Calculating GDP

When calculating the GDP of a country, economists look at a wide range of factors, including: Public and private consumption, government spending, investments, growth in private inventories, construction spending, as well as the balance of foreign trade (exports minus imports).

The GDP formula can be complicated, so to enable comparisons, countries typically follow a set of internationally accepted guidelines, known as the 1993 System of National Accounts, created by the International Monetary Fund, the European Commission, the Organization for Economic Cooperation and Development, the United Nations, and the World Bank.

In the United States, the BEA uses data collected by other federal agencies, including the Census Bureau, the Bureau of Labor Statistics, and the Treasury. It also gathers information directly from private industry, including trade groups and companies that specialize in sales data for a wide range of products, from prescription drugs to cars.

💡 Quick Tip: Did you know that opening a brokerage account typically doesn’t come with any setup costs? Often, the only requirement to open a brokerage account — aside from providing personal details — is making an initial deposit.

Multiple Measures of GDP

There are several ways to measure GDP.

Real GDP

Real GDP is an inflation-adjusted measure of the value of the amount of goods and services produced by a given economy. This is the number typically released by the United States.

Nominal GDP

Nominal GDP uses current market prices to compare countries’ GDP. It does not adjust values based on inflation. If a country’s output remains steady, but the value of what they produce changes, then its nominal GDP would change. That makes it much harder to compare GDP in two different time periods.

Purchasing Power Parity GDP

Purchasing Power Parity (PPP) measures GDP as adjusted for the differences in both local prices and local living costs. This metric allows economists to make more meaningful correlations from country to country about the impact of GDP on the people who live there.

Per Capita GDP

This breaks down the GDP by the number of people in a country’s population. As such, it shows the average output or income of each person in that country, and is often used to paint a picture of the relative wealth or poverty in a given country.

Recommended: 101 Investing Guide

What GDP Means for Investors

When the GDP makes the financial news, the number in the headline is usually a percentage, namely how much the GDP rose or fell in the most recent quarter. The standard definition of a recession is two quarters of consecutive declines in the GDP.

During a period of rising GDP, employment tends to increase because companies staff up for expansion. This means that more people have more income to spend. That creates more business, which keeps the growth cycle spinning. But when GDP is in decline, the opposite tends to occur, with fewer people working, and wages depressed, leading to a downward cycle.

While there is not a direct cause-effect relationship between the GDP and stock or bond prices, some investors use a strategy known as business-cycle investing to determine how to allocate their portfolio.

Recommended: Asset Allocation by Age

Equity Investors

Many stock investors prefer an economy where the GDP is steadily rising, since it often means a healthy economy and higher company earnings, which can boost the stock market. In contrast, a falling or stagnant GDP can be bad news for stock prices.

Bond Investors

Fixed-income investors may have a different view of GDP. That’s because GDP growth often comes with more borrowing by both consumers and businesses, which can create inflation. Inflation often leads to higher interest rates, which have the effect of driving down bond prices. With sinking GDP, the opposite tends to happen, resulting in higher bond prices.

The Takeaway

GDP is essentially an economic scorecard for a country. By understanding how a country’s GDP is changing over time, and how it compares to other countries, you can get a sense of its overall economic health. Investors can consider GDP trends when planning their investing strategy.

Ready to invest in your goals? It’s easy to get started when you open an investment account with SoFi Invest. You can invest in stocks, exchange-traded funds (ETFs), and more. SoFi doesn’t charge commissions, but other fees apply (full fee disclosure here).

For a limited time, opening and funding an Active Invest account gives you the opportunity to get up to $1,000 in the stock of your choice.

Photo credit: iStock

SoFi Invest® The information provided is not meant to provide investment or financial advice. Also, past performance is no guarantee of future results. Investment decisions should be based on an individual’s specific financial needs, goals, and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below. 1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC registered investment advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or prequalification for any loan product offered by SoFi Bank, N.A.

Claw Promotion: Customer must fund their Active Invest account with at least $10 within 30 days of opening the account. Probability of customer receiving $1,000 is 0.028%. See full terms and conditions.

When you are an experienced real estate agent looking for a new brokerage, you are thorough about interviewing companies that will be the right fit. You analyze change not only in terms of commission splits, culture, marketing, and support, but also in terms of what feels good for your business. You look for companies that fit your goals and will be good for growth. You have learned to interview brokers and not the other way around. You know the ins-and-outs of the business and feel confident that you will bring value to a company but the value needs to be reciprocal. Going through the trouble of changing companies without benefit for you and your business, would make absolutely no sense.

Oh the headache!! New business cards, property signs, branding! Going through all platforms changing brokerage names. Making announcements and making sure business is uninterrupted! Change and adjustment must come with a nice price tag and added value.

The easy way is not always the best way

No wonder so many agents remain in their good ‘ol boring companies for years. If it ain’t broke, don’t fix it! How lame is that!! And how can you really scale your business with your current status quo. Well…maybe you are happy with status quo, and that’s really ok – but what if a broker knocked on your door and promised you more money? (I’m not mentioning any names or the known company offering nice bonuses!!) <<pure sweetness, may as well take a nice vacay and continue your good ol’ business once you return.

But I’m not talking about magic pills here. I’m talking about not scaling your business because of lack of motivation, fear of technology, fear of hiring help, or worse: fear of change. So if a broker can guarantee efficiency so you have time to focus on real estate, would that catch your attention?

I know what you are thinking … you are an independent contractor. Shouldn’t you be responsible for improving your own business? That is NOT your broker’s responsibility. << sorry to say but although much of that is true, it’s also a good way for you to BS yourself. A good broker will go out of their way to continuously improve their tech and systems to make you productive and efficient. A great broker will do that and also make sure your needs are taken care of instead of forgetting you in the background and focusing on their new hires.

Is the value promised real?

The truth is that brokerages need money to make money – so if they claim they will provide value, they better give proof, not just tease you with the latest shiny object.

Let’s break down what’s important to you as an agent:

tools (in one place, not having to jump around all over the web, and having the latest tech)

name recognition (is this really about the broker or your own brand and value?)

efficiency (cut down hours doing useless things that don’t make you money)

support (cut down hours doing useless things that don’t make you money)

leads (do you want a broker that gives you hand-me-downs or one that will provide A.I. and predictive analytics?)

Your current broker could be holding you back

The point of this article is to make you think of the unthinkable, change. Mediocrity is not an option, and although change is sometimes the answer for making great things happen, your decision should ultimately be about aligning yourself with powerful and smart people that will not just compliment your business but help it soar to new levels.

I challenge you to look back at your business and analyze how it has improved (or not) in the last year. Can you hear “change” calling your name? shhhhh…..if you listen, it will be clear as day.

Imagine making $1,000 for every $100 you spend on real estate leads. Today’s guest, Joe Herrera of the Joe Taylor Group, does exactly that with a smart, simple Facebook advertising strategy. Listen and learn how to create viral property ads and how to consistently convert the leads that they generate. Plus, you’ll hear how to hold a team of Realtors accountable, what works best for buyer leads in 2023, and why you should not advertise a property’s price.

Listen to today’s show and learn:

About Joe Herrera [0:41]

Why Joe focuses on Facebook for real estate leads [4:43]

How to stop playing Zillow’s game [7:50]

An argument for not listing a property’s price [9:24]

Determining lead spend based on agents’ needs [12:55]

What to expect when you start running ads on Facebook [15:13]

How soon you’ll know whether or not a real estate ad is working [19:29]

How leads come in when running Facebook ads [21:34]

Why Zillow isn’t the right fit for Joe’s real estate business [24:49]

Focusing on the why instead of the what when working buyer leads [27:59]

Building the right relationship with potential clients [29:23]

What the 9-6-6 follow-up schedule looks like [31:50]

Joe’s coaching and lead-gen program for busy real estate agents [33:16]

Common conversion mistakes [36:45]

The difference between customer service and sales [39:51]

How to hold real estate agents accountable [41:40]

Joe’s real estate goals for the next few years [45:41]

The most relevant voice in real estate [49:16]

Joe Herrera

Joe Herrera is a multifaceted individual who seamlessly blends passion and responsibility into his various roles. As a keynote speaker, coach, mentor, lead generator, podcast host, and associate broker of Real Broker, Herrera’s enthusiasm for his work is contagious.

With more than a decade of experience as a lead conversion coach, Herrera has an impressive track record of generating more than 10,000 leads annually. His exceptional team, the Joe Taylor Group, closes an outstanding 1,000 units each year, expanding its presence to seven locations across North America. Notably, Herrera has graced the stage as a featured keynote speaker at prestigious real estate events across the U.S. and Mexico, sharing his expertise and insights.

In addition to his accomplishments in real estate industry, Herrera’s entrepreneurial spirit shines as he owns and operates several businesses specializing in investment and lead generation. His commitment to helping others extends further through his dedicated Velocity coaching business, where he pays it forward by guiding and supporting aspiring professionals.

As a Las Vegas area REALTOR®, Herrera understands the significance of buying or selling a home as a major life event for his clients. Beyond being a salesperson, he embraces his role as a trusted guide, providing unparalleled support and expertise throughout the process.

Outside of his professional pursuits, Herrera remains deeply connected to his community and family. He devotes his time to various acts of service, always ready to give back to those in need. An avid golfer, Herrera enjoys spending quality time with his kids, hitting the links at his favorite golf courses across the country.

Joe Herrera’s story is one of dedication, ambition, and genuine care for others – a testament to his remarkable character and the positive impact he brings to both the real estate industry and his community.

Related Links and Resources:

It might go without saying, but I’m going to say it anyway: We really value listeners like you. We’re constantly working to improve the show, so why not leave us a review? If you love the content and can’t stand the thought of missing the nuggets our Rockstar guests share every week, please subscribe; it’ll get you instant access to our latest episodes and is the best way to support your favorite real estate podcast. Have questions? Suggestions? Want to say hi? Shoot me a message via Twitter, Instagram, Facebook, or Email.

Inside: Are you looking for an affordable budgeting app that offers a range of features? YNAB may be the perfect choice for you! This guide will compare YNAB vs Mint, highlight their key features, and help you decide which is best for your needs.

Are you trying to make a choice between Mint and YNAB for managing your financials?

Here’s a comprehensive overview that would definitely point you in the right direction.

Both Mint and YNAB have proven to be efficient and reliable online budgeting tools, but their offering varies in some aspects.

While Mint shines with its free budgeting tools and comprehensive credit score and report management capabilities, YNAB stands distinguished with its robust features and specialist credit management options, making it worth its fee for some users.

Herein, we dive into the similarities, differences, and unique functionalities of both platforms to help you decide which one best aligns with your financial management needs and lifestyle.

As a finance expert, I’ve seen both YNAB and Mint apps work wonders for different people.

In my opinion, both have unique value. Novices may find Mint’s overview helpful, while more determined budgeters might prefer YNAB.

Remember, it’s perfectly fine to use both if it aids your long-term money management.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What is YNAB?

YNAB is a budgeting software I’ve utilized that provides detailed financial tracking and education for effective money management. Also, known as you need a budget app.

Adhering to its unique Four Simple Rules for Successful Budgeting, every dollar is assigned a specific task. YNAB operates via an online account or a mobile app, involving color codes and features like ‘The Inspector’ for efficient budget overview. However, it’s important to note that YNAB caters only to the zero budgeting style and charges a monthly subscription fee.

This is a great budgeting method as it gives you a cash flow budget plan for your money.

Overall, YNAB helped me gain control over my finances by setting realistic goals, getting one month ahead on bills, and focusing on each dollar’s purpose.

What is Mint?

Mint is a free, all-in-one finance platform owned by Intuit that can be used to easily manage my money.

It links all accounts in one place for easy tracking and includes features such as budgeting, credit score monitoring, and bill tracking.

For instance, Mint categorizes transactions, monitors changes in my credit score, and sets up budgetary limits.

With over 30 million users, Mint is a leading free tool in personal finance management.

A step up from Mint would be Intuit’s Quicken platform or Simplifi budget app.

Comparison of YNAB and Mint Apps

Mint is a comprehensive, free budgeting app, that provides an overall view of your finances. It links to your accounts, tracking and categorizing spending, while also offering savings tips. Conversely, YNAB, a paid app, focuses on giving users control over budgeting. It will link to your accounts and encourage a proactive role in handling finances.

These are two of the budget apps available on the market.

In my opinion, if you’re seeking an easy-to-use app offering a holistic view of your spending and savings, Mint is a perfect choice. However, if you’re looking for a stringent budget management system with more control, YNAB is worth the investment.

Kristy @ Money BLiss

1. YNAB vs Mint: Features

YNAB and Mint are both renowned budgeting apps, but they possess some notable differences.

While both support account linking, goal setting, and spending tracking, Mint pulls ahead with its investment and credit score tracking features.

YNAB distinguishes itself with a forward-thinking, zero-based budgeting strategy and benefits like manually adding transactions. Think budget by paycheck style.

From the ease of use standpoint, both are equally user-friendly.

2. YNAB vs Mint: Budgeting Snapshot

YNAB offers a rigorous, manually updated budgeting snapshot that employs a zero-based budgeting philosophy. This feature provides a detailed outlook, encouraging users to assign every dollar a job.

On the other hand, Mint has an automated tracking system that offers an all-in-one snapshot of all financial accounts and spending categories.

Mint integrates your accounts, offering useful tips and an overview of your finances. Conversely, YNAB requires a manual categorization of income and expenses but affords more budgeting control. Similar to using the ideal household budget percentages.

The budgeting snapshot in Mint is best suitable for individuals seeking a hands-off approach, while YNAB is ideal for those who prefer an in-depth, hands-on budget strategy.

A great way to move digital from your budget binder with envelopes.

3. YNAB vs Mint: Goal Setting

The Goal Tracking feature in YNAB allows users to set various budgeting goals such as saving targeted amounts of money or conversely working towards getting out of credit card debt. This in-built functionality provides a structured pathway for users to stick to and pursue their financial objectives effectively.

Your interaction with your YNAB account through the goal-tracking tool ties back to YNAB’s four Simple Rules for Successful Budgeting, aiding in fiscal responsibility.

This innovative feature assists individuals in staying focused on their planned budgets, ensuring they are empowered to make strides toward their unique financial goals.

Mint however doesn’t offer this feature.

4. YNAB vs Mint: Interface

While YNAB is ideal for meticulous budgeters prioritizing forward planning, Mint is perfect for those seeking an easy-to-use, comprehensive glimpse of their financial standing.

YNAB’s interface is focused on budgeting, featuring tools for expense tracking, goal setting, and manual transaction input.

In contrast, Mint offers a comprehensive overview of your financial health, automatically categorizing expenses, tracking investments, and offering set-up alerts.

5. YNAB vs Mint: Categorization

Mint offers automated categorization of transactions, which eases the process of budgeting for the user. However, it doesn’t allow the removal of default categories, and the addition of new ones might take time due to server communication.

On the other hand, YNAB allows a deeper level of categorization, with an option to visually nest categories, and more effortless editing of these categories.

In my opinion, Mint’s categorization feature suits a casual budgeter looking for automation, while YNAB would be ideal for those desiring granular control over their personal budget categories.

6. YNAB vs Mint: Mobile App & Cross Platforms

Both YNAB and Mint offer comprehensive personal finance management via mobile apps, compatible with iOS, Android, and desktops.

YNAB stands out with its Apple Watch integrations and a slightly better syncing experience based on user reviews on Trustpilot1.

YNAB also syncs across a desktop app as well.

7. YNAB vs Mint: Alerts

Mint provides a wide selection of alerts, including low balances, upcoming bill payments, over-budget warnings, ATM fees, and unusual expenditure notifications.

These comprehensive alerts from Mint give a more thorough financial pulse check but can be overwhelming for some.

On the other hand, YNAB recently added live push notifications based on your preferences.

8. YNAB vs Mint: Syncing

YNAB leads the game when it comes to synchronization, outshining Mint. While Mint supports numerous banks, issues with synchronization often lead to grievances among its users. YNAB, on the other hand, offers smoother syncing and fewer complaints, proving its superiority.

Many users find YNAB’s syncing consistent and reliable.

Personally, I believe that if you prioritize seamless syncing and don’t mind spending $14.99 a month, YNAB becomes a clear choice.

However, if you’re okay with potential sync issues and prefer free usage, Mint could be more suitable.

It’s crucial to pick according to your priorities and needs.

9. YNAB vs Mint: Savings Accounts

Mint offers automatic expenditure tracking and classifies my spending into categories, providing a comprehensive view of where my money is going.

YNAB, on the other hand, empowers me to manually budget my net income each month, ensuring I don’t overspend and promoting a proactive approach to saving.

10. YNAB vs Mint: Investment Tracker

Mint offers investment tracking features, allowing users to view their investment portfolio and monitor performance.

In contrast, YNAB lacks this feature, not providing any investment tracking at all.

As a user, if you highly prioritize tracking investments in one place, you may lean towards using Mint. Conversely, if investment tracking is less important to you than budgeting, YNAB’s strong budgeting emphasis, despite its lack of investment tracking, makes it a considerable option.

11. YNAB vs Mint: Learning Curve with your Finances

YNAB has a steeper learning curve, necessitating a proactive approach to money management by assigning every dollar a purpose. Thus, YNAB gives you a free 34-day free trial to understand how to use the app.

Mint, however, requires minimal user input post-account linkage and auto-categorizes your spending. For sheer ease of use, Mint might appeal to novices looking for automated budget tracking.

On the other hand, users wishing to take charge of their finances might appreciate YNAB’s proactive, behavior-altering approach. Despite having a steeper learning curve, YNAB offers an abundance of online tutorials and customer support, making the learning process manageable and rewarding.

The same is true when you are learning to use the biweekly budget template.

12. YNAB vs. Mint: Data Security

Data security is a paramount concern when utilizing online budgeting apps as they deal with sensitive financial information.

Apps like YNAB and Mint incorporate stringent security measures to protect user data.

For instance, YNAB uses a one-way salted and hashed password system and data encryption.

Mint, on the other hand, employs two-factor authentication and a Touch ID sensor for iOS for enhanced security.

Nonetheless, it’s important to note that while these apps provide bank-level security, Mint does anonymize and sell user data to advertisers.

13. YNAB vs Mint: Advertising

YNAB derives income primarily from subscription fees offering an ad-free experience, holding a straightforward revenue model. In contrast, Mint generates income through affiliate commissions by advertising financial products to users and selling anonymized user data!

Mint, contrastingly, is a free app reliant on ads and sells anonymized user data for third-party advertisements.

From my perspective, if avoiding ads and preserving data privacy matters to you, YNAB’s approach might be more appealing. However, if you prefer a free service and don’t mind the ads, Mint would be suitable.

14. YNAB vs Mint: Customer Support

When evaluating the customer support of Mint and YNAB, it’s evident that YNAB takes a more well-rounded approach.

With a commitment to respond to email queries within 24 hours, YNAB also provides educational resources such as the “get started” class, their blog, and user forums. This is in contrast to Mint, which, despite offering live chat support, has had reports of slow response times.

Both platforms offer online training materials, but YNAB seems more comprehensive and responsive in its support-providing role. Overall, YNAB appears to be the preferred choice when customer support is a primary consideration.

15. YNAB vs Mint: Cost

Mint is a free, ad-supported budgeting app while YNAB is a subscription-based model of $14.99 monthly or $99 annually.

However, for individuals seeking in-depth surgical budgeting capabilities without concerns for associated costs, YNAB’s price might represent a great investment.

Given the claimed average user saves $600 in two months and $6,000 in the first year.2

For those budgeting with minimal funds, the free price tag of Mint might be more attractive, but you are giving away your privacy.

Pros and Cons of YNAB vs Mint

Our Favorite

Key Features:

YNAB offers a comprehensive approach to budgeting, helping you plan monthly budgets based on your income. It also offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

YNAB’s superior synchronization skills make it the winner in this area. YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners

YNAB provides an option to manually add and upload transactions from accounts each month, a feature that Mint does not offer.

YNAB prioritizes user privacy, requires an opt-in to access budgeting data, and doesn’t sell user data.

Key Features:

Mint offers a centralized platform for monitoring all your financial accounts, including credit cards and bank accounts.

It provides a complete financial overview at a glance through the auto-population of data from linked accounts.

Mint’s features include detailed reporting in multiple categories, free credit score access, and exceptional compatibility with financial institutions.

The service is free, funded by ads and offers, and it best serves those who wish to categorize spending, budget their monthly expenses, and access all financial details from one place.

Lack of investment tracking feature

Customer service is only accessible via email, which might not be ideal for urgent queries

Steep learning curve which requires time and effort to navigate through.

Mint, which belongs to Intuit, automatically accesses all data and sells the data. Thus, an intrusion of privacy.

Budgeting feature doesn’t enable effective planning of future expenses.

Mint suffers from more technical glitches and synchronization issues.

Ads included in the free version of Mint can be obtrusive and may deter users.

$14.99 monthly or $99 annually

Free to Use, But Served Ads and They Sell your Data.

Offers a 100% money-back guarantee at any point of use.

Does not require credit card information to signup, a departure from the usual free trial model)

Our Favorite

Key Features:

YNAB offers a comprehensive approach to budgeting, helping you plan monthly budgets based on your income. It also offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

YNAB’s superior synchronization skills make it the winner in this area. YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners

YNAB provides an option to manually add and upload transactions from accounts each month, a feature that Mint does not offer.

YNAB prioritizes user privacy, requires an opt-in to access budgeting data, and doesn’t sell user data.

Lack of investment tracking feature

Customer service is only accessible via email, which might not be ideal for urgent queries

Steep learning curve which requires time and effort to navigate through.

$14.99 monthly or $99 annually

Offers a 100% money-back guarantee at any point of use.

Does not require credit card information to signup, a departure from the usual free trial model)

Key Features:

Mint offers a centralized platform for monitoring all your financial accounts, including credit cards and bank accounts.

It provides a complete financial overview at a glance through the auto-population of data from linked accounts.

Mint’s features include detailed reporting in multiple categories, free credit score access, and exceptional compatibility with financial institutions.

The service is free, funded by ads and offers, and it best serves those who wish to categorize spending, budget their monthly expenses, and access all financial details from one place.

Mint, which belongs to Intuit, automatically accesses all data and sells the data. Thus, an intrusion of privacy.

Budgeting feature doesn’t enable effective planning of future expenses.

Mint suffers from more technical glitches and synchronization issues.

Ads included in the free version of Mint can be obtrusive and may deter users.

Free to Use, But Served Ads and They Sell your Data.

Who should use YNAB?

From my experience, YNAB works best for those who are ready to seriously manage their money and spend some time learning a new budgeting approach. Its use of the zero-based budgeting system not only makes you more intentional with your money but also demands active participation in decision-making.

YNAB’s ability to link to your accounts and its multitude of educational resources available are admirable features I’ve used.

YNAB offers detailed financial tracking and built-in education, but its monthly subscription fee and suitability for a specific budgeting style may be limiting for some.

However, it comes with a monthly or annual cost – a worthy investment for those searching for a robust, hands-on, and future-focused budgeting tool. Most YNAB budgets agree they save multiples of the subscription cost.

However, it can be less suitable for those not ready for a hands-on approach or those sensitive to subscription pricing.

Who should use Mint?

On the other hand, Mint is an all-in-one app that automatically tracks and categorizes your spending.

Based on my experience, Mint is an excellent tool for novice-level budgeters seeking to track their expenses, set budgets, and manage their finances with ease. This budgeting app allows a comprehensive view of all your financial accounts, which differentiates it from YNAB.

If you’re comfortable seeing ads and not needing investing features, Mint could be a perfect fit. However, if you require the ability to assign multiple savings goals to one account or a bill pay feature, YNAB may be more suitable for you.

Therefore, Mint is most applicable for beginners seeking a free and user-friendly budgeting platform.

YNAB vs. Mint: Which is better for you?

As a content writer and budgeting app user, I find Mint and YNAB are unique in their offerings.

Mint automatically tracks and categorizes your spending, providing an intuitive picture of where your money goes, ideal for beginners in budgeting.

In contrast, YNAB promotes a proactive approach, helping to set and monitor budgets, hence perfect for those with specific financial goals. To sum up, Mint offers a simplified, passive overview, while YNAB is excellent for a detailed, forward-thinking approach to managing finances.

Personal preferences and needs really influence the choice here. Do you need intricate control and don’t mind paying a fee? YNAB might be your fit. Prefer automation and want a free option? Mint could work for you.

YNAB vs Mint: Verdict

As an expert in personal finance tools, I’ve explored both YNAB and Mint.

In my experience, there are distinct differences between YNAB and Mint. For my readers, I recommend YNAB.

YNAB, with its laser-focused approach towards budgeting, is a boon for individuals needing extensive assistance in the budgeting arena. You learn to assign every dollar with intention, thereby gaining a higher degree of control over your finances.

This proactive approach will help you to be financially independent faster.

To sum up, if detailed budgeting is your priority, choose YNAB.

YNAB

Enjoy guilt-free spending and effortless saving with a friendly, flexible method for managing your finances.

Pros:

Comprehensive approach to budgeting, helping you plan monthly budgets based on your income.

Offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

Superior synchronization skills make it the winner in this area.

YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners.

Option to manually add and upload transactions from accounts each month.

YNAB prioritizes user privacy.

Start 34 Day Free Trial

However, for a more holistic financial insight with less emphasis on budgeting, Mint might be the better choice.

Now, make sure to check out our Quicken Review.

Source

TrustPilot. “YNAB Review.” https://www.trustpilot.com/review/ynab.com. Accessed on September 27, 2023.

YNAB. “YNAB Pricing.” https://www.ynab.com/pricing/. Accessed on September 27, 2023.

Know someone else that needs this, too? Then, please share!!

Hate cold calling? Hear how to ditch it entirely on this podcast with organic-lead-gen expert Charlie Cameron. Charlie generated an incredible amount of real estate business incredibly fast, and it was very inexpensive. Today, he shares the low-cost tech tools and proven strategies that helped make it happen. Discover how he built a booming Facebook group, how he consistently ranks above competitors on Google, and more on this Real Estate Rockstars!

Listen to today’s show and learn:

About Charlie Cameron [0:54]

“Easy money” [2:20]

Getting clients from a Facebook group [3:25]

You don’t have to cold call [4:54]

How NOT to fail at Facebook groups [6:37]

Ways to help your Facebook group grow [8:46]

Charlie’s follow-up process for Facebook leads [12:44]

How much business Charlie gets from his Facebook group [19:22]

Attracting clients and agents with blogging and SEO [20:43]

How to ensure potential clients find you online [27:42]

Ways to get ahead with organic lead gen now [30:14]

Charlie’s content-machine goal [36:44]

Advice on picking a platform for your content [38:11]

Charlie Cameron’s advice for real estate agents [44:56]

Charlie Cameron

Real estate super nerd, family man and veteran! I’m passionate about real estate and obsessed with helping others win and with continuous growth.

Charlie Cameron is a Dad, military spouse, and Air Force veteran (turned reservist) who found a passion for real estate while serving. Thanks to real estate—largely eXp Realty and investing—he was able to transition out of Active Duty military service to focus on real estate! People and real estate are his passions, and helping other succeed is what he finds most rewarding.

Charlie enjoys mentoring growth-minded agents the most. At this time, he is growing an international real estate team, building a local military-focused real estate team along the Florida Panhandle, and scaling an as-passive-as-possible real estate portfolio of short term rentals, residential assisted living, and more! He is also an Air Force Reservist in a part time capacity (2 weeks a year) as a weapon program manager.

By leveraging teams, systems, automation, and intentional task prioritization, Charlie is able to prioritize his most important thing: living in the moment with family & friends!

Current lines of effort:

Grow international real estate team: help other real estate agents become successful, grow their leads and business, create multiple income streams, and achieve financial freedom. Team growth achieved through blog and content creation.

Lead a local military-first real estate team: though long term low effort client attraction efforts, Charlie provides clients to his local military focused team to work and close!

Scale a real estate investment portfolio: real estate investing is best investing!

Charlie has a bachelors in Mechanical Engineering from the University of Virginia and a Masters in Industrial Engineering from New Mexico State. He starting investing in real estate while serving in 2017 by STARTING with 8 apartments which he self managed. After scaling a small multifamily portfolio he transitioned and 1031 exchanged into a self managed short term rental portfolio, all of which he managed from afar. Recently he has pivoted again into the residential assisted living niche. Charlie partners on just about every investment deal he does.

Charlie spent 11 years on Active Duty, as an engineer and officer developing, testing, and managing cutting edge weapons systems programs to ensure the Air Force stays undefeatable! He led hundreds of tests and ran hundreds of million dollar a year programs and contracts developing, acquiring, and testing new weapons for the warfighter. During that time, he also served as a USAA Advisory Panel Member, providing direct feedback on bank and insurance products as a military member to the board of directors. In a past life, he has also been a Firefighter, EMT, and lifeguard.

Charlie is a nerd who loves to tinker and find new ways to grow and implement things in his businesses. While he wishes he was able to focus on only one business, he knows now that resistance is futile and he must find ways to grow multiple lines of effort without consuming more time!

Related Links and Resources:

It might go without saying, but I’m going to say it anyway: We really value listeners like you. We’re constantly working to improve the show, so why not leave us a review? If you love the content and can’t stand the thought of missing the nuggets our Rockstar guests share every week, please subscribe; it’ll get you instant access to our latest episodes and is the best way to support your favorite real estate podcast. Have questions? Suggestions? Want to say hi? Shoot me a message via Twitter, Instagram, Facebook, or Email.