Mortgage rates kept climbing for the fifth consecutive week, bringing average year-over-year rates 60 basis points higher.

Freddie Mac‘s Primary Mortgage Market Survey, which focuses on conventional and conforming loans with a 20% down payment, shows the 30-year, fixed-rate mortgage averaged 7.57% as of Oct. 12. That’s up 8 basis points from 7.49% the previous week.

By contrast, the 30-year, fixed-rate mortgage was at 6.92% a year ago at this time.

“For the fifth consecutive week, mortgage rates rose as ongoing market and geopolitical uncertainty continues to increase,” Sam Khater, Freddie Mac’s chief economist said in a press release. “The good news is that the economy and incomes continue to grow at a solid pace, but the housing market remains fraught with significant affordability constraints. As a result, purchase demand remains at a three-decade low.”

On Thursday, the Consumer Price Index report showed steady inflation in September, with increases in shelter costs.

Other indices showed significantly higher home loan rates this week.

HousingWire’s Mortgage Rates Center showed Optimal Blue’s average 30-year fixed rate for conventional loans at 7.52% on Wednesday, compared to 7.60% the previous week. At Mortgage News Daily on Wednesday, the 30-year fixed rate for conventional loans was 7.60%, up from 7.70% the previous week.

Last week’s stubbornly strong jobs report surprised investors, resulting in a surge in the 10-year Treasury yield and home loan rates, Hannah Jones, senior economic research analyst at Realtor.com, said in a news release.

On Thursday, the benchmark 10-year Treasury yield was at 4.6%, down from 4.8% earlier in October. Amid geopolitical uncertainty, investors took refuge in bonds, Jones noted.

Additionally, higher mortgage rates are also a result of the Federal Reserve‘s reduced holdings of mortgage-backed securities, Bright MLS Chief Economist Lisa Sturtevant said in a news statement. The Fed’s selloff of MBSs has increased the supply of mortgage bonds in the market, driving those bond yields higher.

It could be worth locking in a mortgage rate now, despite the elevated rate environment, some experts say.

Yuri Arcurs / Getty Images

Since 2022, the Federal Reserve has raised interest rates 11 times. During the most recent Fed meeting in September, however, the central bank did not issue another rate hike. Still, many predict the Fed will raise interest rates again when it meets next in November, and interest rates could remain elevated for a while after that.

And, while the Fed does not directly dictate mortgage rates, it generally influences the real estate market.

“The Fed is likely to increase rates by 25 basis points in November, which will likely keep upward pressure on mortgage rates,” says Eric Fox, chief economist at Veros.

From there, it could be a while until rates drop.

“I think our best chance of a rate drop is late 2024 or into 2025 — whenever the economy gets bad enough that the Fed needs to lower rates to energize it,” says Mason Whitehead, a home loan specialist at Churchill Mortgage.

Explore the mortgage rates you could qualify for here.

Should you lock in a mortgage rate now?

Amidst the strong possibility that interest rates will increase further, or at least remain elevated, many experts think that homebuyers are better off locking in rates now.

“If you’re a serious buyer and need to buy in the next month or two, it’s best to lock in the rate, as they aren’t coming down anytime soon,” says Lisa Simonsen, licensed associate real estate broker at Douglas Elliman Real Estate.

But even if rates don’t end up rising, you might be better off acting now.

“I always advise locking rates sooner rather than later. We make decisions based on the information in front of us and not speculating what may happen tomorrow or next week/month,” says Whitehead.

Learn more about the top mortgage rates you could qualify for here.

Marry the property but date the rate, experts say

Buying a home and taking out a mortgage now could also be helpful from a real estate cost perspective.

“Due to a continued constrained supply of homes on the market, it is unlikely that there will be any slowdown in the upward march of house prices. The best approach is to simply purchase what you can afford today and refinance down the road when mortgage rates tick down,” says Fox. “This will allow buyers to participate in home equity gains rather than sitting on the sidelines.”

By focusing on what you can afford now, you don’t have to worry as much if it takes a while for rates to come down. And, while rates can change, you might only have one opportunity to buy a particular home.

“I like to say you date the rate and marry the property,” says Simonsen. “You can always refinance but you can’t always find your dream home.”

Keep in mind, however, that rates might not get back to their pandemic lows. While rates might seem high now, they look more reasonable from a historical perspective.

“Buyers got used to perpetually — and artificially — low interest rates. For the time being, believe this to be the new normal. I do not think we will see those artificially historic low rates in the near future,” says Nikki Beauchamp, senior global real estate advisor, licensed associate real estate broker at Engel & Völkers.

That’s why it’s important to not overextend yourself when taking out a mortgage.

“You need to be comfortable with your payment as-is and not need the rate to drop and refinance in the future to comfortably afford the payment,” says Whitehead. “Plan and budget for what is real, not what you hope for in the future.”

Focus on what you can control

Homebuyers can’t control the Fed’s policy, and many experts think that homebuyers shouldn’t get overly caught up in which way the winds are blowing.

“Those borrowers who have been most successful don’t pay attention to short-term increases and decreases in mortgage interest rates. Rather, it is best to focus on the long-term, purchase what you can afford today, participate in home equity growth, and refinance whenever possible in the future,” says Fox.

You also might be able to get some relief via seller concessions.

Ask for concessions like rate buydowns, which involve paying money upfront to reduce mortgage rates, and “potentially check to see if there is the possibility of assuming a mortgage as well,” says Beauchamp.

That said, don’t assume you’ll get these types of concessions. It probably doesn’t hurt to ask, but the market conditions might not work in buyers’ favor.

“Due to the constrained supply of homes on the market today, extensive seller concessions are not going to be widely available to offset higher mortgage interest rates,” says Fox.

The bottom line

Overall, buyers need to focus on what they can control, experts say, like finding a home within their budgets. And, that’s true regardless of rates.

“If something suits your needs and one can comfortably make it work and build equity, it is worth considering,” says Beauchamp.

Nestled in the heart of Utah Valley, Provo has increasingly been a topic of discussion for those looking to relocate.

Known for its close proximity to natural wonders like Provo Canyon and Utah Lake, it’s a location that offers both city life and natural retreat. However, with such growing attention, the question arises: Is Provo, Utah, a good place to live?

Geographic overview

Provo, located in Utah County, sits about 45 miles south of Salt Lake City. As part of the larger Provo-Orem metro area, it’s surrounded by breathtaking views, notably the majestic Wasatch Front mountains. The city enjoys a beautiful position by the Provo River, leading many to the popular Provo River Parkway Trail for outdoor activities.

Educational excellence: BYU and beyond

Central to Provo’s identity is Brigham Young University (BYU). As one of the top institutions in the country, BYU has significantly influenced Provo’s status as a college town. The presence of BYU means Provo is bursting with educational opportunities, from lectures at the BYU Museum and Bean Life Science Museum to events at the BYU campus itself.

Quality of life in Provo

Economic, cultural and safety factors drive movers to Provo in droves.

Economic stability

Provo’s unemployment rate is below the national average. The presence of institutions like BYU and the Provo City Center Temple ensures steady employment in the education and service sectors. Additionally, with a tech boom happening in the broader Salt Lake Valley, many are finding new job opportunities within a commutable distance from Provo.

Cultural richness

Provo is home to a rich blend of cultures. While there is a significant presence of members of The Church of Jesus Christ of Latter-day Saints, Provo is diverse in thought and lifestyle. The city houses several art galleries, theaters, and the iconic Provo City Center Temple, a testament to its rich history and cultural significance.

Safety

One of the notable features of living in Provo is its low crime rates. Both violent crimes and property crimes are below the national average, making Provo a safe environment for young families and college students alike.

Cost of living: breaking down the numbers

Is Provo Utah expensive to live in? Compared to other cities along the Wasatch Front, Provo’s cost of living is slightly below average. However, with the city’s growth, housing costs have been on the rise.

Housing market insights

The median home price in Provo has seen an upward trend over the past few years, though it remains competitive compared to Salt Lake City. Average rent for apartments is also reasonable, particularly given the high student population from BYU and Provo College. However, the demand for affordable homes has been steadily increasing.

Everyday expenses

When comparing Provo’s cost for groceries, transportation, and healthcare to the national average, residents find it reasonable and often below average. However, as with any city, certain luxuries or non-essentials can drive up living costs.

The heart of Provo: its people

With a population density of around 2,500 people per square mile, Provo is lively without feeling overcrowded. The median age skews younger, thanks in part to the influx of college students. Provo residents are generally known for their hospitality, community spirit and active lifestyles, taking advantage of nearby attractions like Provo Beach and Rock Canyon.

Before you pack: Moving to Provo insights

What do I need to know before moving to Provo Utah? Here are some considerations:

Outdoor Activities: With Provo River, Provo Canyon, and myriad trails, there’s always something to do outdoors. Whether you’re into hiking, fishing, or just picnicking, Provo has you covered.

Community Feel: Provo, often dubbed “Happy Valley”, has a tight-knit community. Neighbors often become lifelong friends, and community events are frequent.

Religious Considerations: As mentioned, Provo has a substantial Mormon population. While this brings a unique cultural flavor, it’s essential to be respectful and understanding of religious practices and holidays.

Public Transportation: The bus system in Provo is reliable, but having a car might be convenient for broader exploration and commuting.

Final verdict

Living in Provo offers a harmonious blend of city life and nature, academia and culture, community and individuality. With its reasonable cost of living, low crime rates and opportunities for both personal and professional growth, Provo stands out as one of the best cities in North Central Utah. Whether you’re a student at Brigham Young University, a young family looking to settle or anyone in between, Provo provides a backdrop for memories, experiences and growth.

In the balance of life’s considerations, the essence of Provo UT seems to be this: it’s more than just a city — it’s a community, an experience, and, for many, it’s home.

So, to the question, “Is Provo Utah a good place to live?” the answer resounds as a confident “Yes!” Search our Provo apartments for rent.

A charming 672-square-foot home set along Florida’s scenic 30A highway recently changed hands. And set a new local real estate record in the process.

The property is located in Seaside, Florida, an area best known for its iconic role in The Truman Show and recognized as the birthplace of the new urbanism architectural movement along the 30A, which passes through a collection of small, unique, beautiful beach towns nestled quietly between busier areas like Destin and Panama City.

Despite its modest size, the 1-bedroom, 1-bath home sold for $2,900,000, setting a new record of $4,135 per square foot — the highest ever recorded in Seaside, Fla.

The record sale was brokered by Jonathan Spears and Lyndon Jackson with Spears Group at Compass, who shared with us that the previous record for price per square foot in Seaside, Florida was $3,935.

Beyond its picture-perfect location, the 672-square-foot home is one of only 12 exclusive new urban honeymoon cottages that line Seaside’s idyllic beaches.

Photo credit: Array Photography courtesy of the Spears Group

“What makes this property truly captivating is its enchanting fusion of two remarkable attributes: the unparalleled views, and its coveted proximity to the charming Seaside Square,” says listing agent Jonathan Spears, the founder of the Spears Group, which was named the #16 medium-sized real estate team in North America by The Wall Street Journal. “Seaside Square serves as the heart of 30A, putting the area firmly on the map with its delightful array of local shops and restaurants.“

High real estate prices are not uncommon for the area.

The small resort community in northwest Florida is known for its late-20th-century New Urbanist design, as well as its pastel-colored houses featuring porches and white picket fences.

Widely seen as a coastal haven with a very high quality of life, Seaside is a sought-after location for buyers looking for a relaxed lifestyle.

Talking about the Seaside real estate market and its allure among wealthy buyers, Spears explains the appeal: “It’s the grandfather of new urbanism and the lifestyle aspect of being able to park your car and walk or bike to world class restaurants, shopping and local entertainment is a staple that continues driving value.“

But the $2.9 million sale of the 1-bedroom cottage stands out, even for the highly competitive market which tends to command impressive prices.

Photo credit: Array Photography courtesy of the Spears GroupPhoto credit: Array Photography courtesy of the Spears GroupPhoto credit: Array Photography courtesy of the Spears Group

“In Seaside, Florida, the median sales price per square foot stands at an impressive $2,621, reflecting the exquisite nature of this coastal haven,” Jonathan Spears says in an exclusive comment for FancyPantsHomes.com. “Typically, other properties in this area tend to sell for a median price of $3,323,500, further emphasizing the desirability of Seaside’s real estate market.”

More stories

An EXCLUSIVE Before-and-After look at the former Vera Bradley Inn in Santa Rosa Beach, now a glam $6.5M residence

Mar-a-Lago neighboring mansion undergoing a massive renovation eyes $40 million sale

Grant Cardone’s Houses: A $40M ‘Castle on the Sand’ and a Wildly Colorful Main Residence in Florida

AI and data-led fintech company Pagaya Technologies named Sanjiv Das as president. Das, a former CEO of Caliber Home Loans, will begin his new role on Oct. 16.

His responsibilities include overseeing the strategy and growth of Pagaya’s commercial business – including its single-family rental business and its subsidiary Darwin Homes – as it continues to enhance its tech-enabled product offering and expand its new and existing lending partnerships, the firm said in a news release.

“We’re excited to welcome Sanjiv as President of Pagaya. His global perspective and extensive entrepreneurial experience in the financial sector and capital markets, as well as his proven track record of building and growing global businesses at scale, uniquely positions him to guide Pagaya’s lending network and innovative product offerings in this next stage of growth,” Gal Krubiner, Pagaya’s co-founder and CEO, said.

Das spent six years as CEO of Caliber Home Loans — a NewRez-owned residential mortgage lending company — until January 2022.

Das’ career also includes positions as CEO, president and chairman of the board of directors for Citigroup‘s mortgage division. He has also held senior roles at Morgan Stanley, American Express and Bank of America.

The executive replaces Ashok Vaswani, who served as Pagaya’s president since June 2022. Vaswani will serve as an advisor to Pagaya for a smooth transition for Das.

“Under Vaswani’s leadership, Pagaya has successfully onboarded new, large partners and expanded its AI-driven lending network, enabling access to more financial opportunities for their customers,” the firm said.

Pagaya, founded in 2016, provides comprehensive consumer credit and residential real estate solutions for its partners, their customers and investors, according to the firm’s website. The fintech has more than 600 employees across two offices in New York and Tel Aviv, Israel.

The firm has been in the real estate business since 2020. Pagaya also offers personal loans, auto loans, credit cards and point-of-sale (POS) financing.

In January 2023, Pagaya acquired proptech Darwin Homes to capitalize on the rental market.

Targeting the single-family rental market, Pagaya shared plans to combine its AI tech and data network with Darwin’s software, operations and mobile app to create a “tech-forward” real estate platform that benefits residents, investors and service operators, the firm said at the time of acquisition.

Bonds have seen only a few examples of a solid 2-day rally over the past few months. While the present example is the largest in terms of the ground covered, it also began from the highest starting point and from the most sharply oversold technical levels. That’s the backdrop for a discussion on why bonds are still rallying. The brushstrokes involve geopolitical turmoil, global economic uncertainty, and an increasingly unanimous opinion among Fed speakers regarding a shift in the rate outlook and in the economy itself. All of the above was enough for the bond market to largely ignore hotter PPI data this morning and a softer 10yr Treasury auction this afternoon. We suspect Thursday’s CPI will get more attention if it’s very far off the median forecast.

Core PPI m/m

0.3 vs 0.3 f’cast, 0.2 prev

Core PPI y/y

2.7 vs 2.3 f’cast, 2.2 prev

Headline PPI m/m

0.5 vs 0.3 f’cast, 0.7 prev

09:05 AM

Stronger overnight. Briefly weaker after data, but selling is over. 10yr down 7.4bps at 4.583. MBS up just over an eighth of a point.

12:22 PM

Additional gains heading into PM hours. 10yr down 7.8 bps at 4.579. MBS up just over a quarter point.

01:10 PM

Some selling after auction. 10yr still down 4.1bps at 4.616. MBS still up 5 ticks (.16), but down more than an eighth from highs.

02:19 PM

Effectively no reaction to Fed minutes. 10yr down 5.1bps at 4.606. MBS up an eighth.

04:42 PM

Best levels of the day after hours. 10yr down 9.5bps at 4.562. MBS up 3/8ths.

Download our mobile app to get alerts for MBS Commentary and streaming MBS and Treasury prices.

MCLEAN, Va., Oct. 12, 2023 (GLOBE NEWSWIRE) — Freddie Mac FMCC today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 7.57 percent.

“For the fifth consecutive week, mortgage rates rose as ongoing market and geopolitical uncertainty continues to increase,” said Sam Khater, Freddie Mac’s Chief Economist. “The good news is that the economy and incomes continue to grow at a solid pace, but the housing market remains fraught with significant affordability constraints. As a result, purchase demand remains at a three-decade low.”

News Facts

30-year fixed-rate mortgage averaged 7.57 percent as of October 12, 2023, up from last week when it averaged 7.49 percent. A year ago at this time, the 30-year FRM averaged 6.92 percent.

15-year fixed-rate mortgage averaged 6.89 percent, up from last week when it averaged 6.78 percent. A year ago at this time, the 15-year FRM averaged 6.09 percent.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit. For more information, view our Frequently Asked Questions.

Freddie Mac’s mission is to make home possible for families across the nation. We promote liquidity, stability, affordability and equity in the housing market throughout all economic cycles. Since 1970, we have helped tens of millions of families buy, rent or keep their home. Learn More: Website | Consumers | Twitter | LinkedIn | Facebook | Instagram | YouTube

Countrywide CEO Angelo Mozilo reportedly originated home loans at a discount for preferred customers known internally as “friends of Angelo,” according to the Wall Street Journal.

These “FoA’s” included high-profile clients such as James A. Johnson and Franklin Raines, former CEOs of government-sponsored mortgage financier Fannie Mae.

While it’s not illegal for mortgage lenders to provide certain clients with special rates and terms, Fannie has a code of conduct that prohibits the acceptance of loans with preferred terms from potential business partners without prior review and approval.

The loans in question include a $1,300,000 five-year adjustable-rate mortgage extended to Johnson at a rate of 5.25 percent when the going rate was 6.0 percent and a $986,340 10-year ARM at a rate of 4.125 percent to Raines when the market average was 5.1 percent.

The pair also received similar, favorable mortgage rates on prior home loans dating back as far as 1998, although the disparity was less significant.

Per the article, a Countrywide spokesperson said Mozilo sometimes provided “moderate” concessions to special borrowers, but not all his requests were met.

While the rates extended to these borrowers clearly seem preferential, it’s pretty common for anyone in the know to receive a “below-market” rate as long as they have some knowledge of the process and a friend in the business.

Couple that with the fact that these borrowers were surely able to document income and assets and provide a large down payment, and these rates may not seem that far from those extended to the most creditworthy of borrowers.

To that end, it’s unclear to what extent these borrowers were favored, but it’s abundantly clear Countrywide will continue to be firmly positioned under the media spotlight until the brand is swallowed up by Bank of America next quarter.

Update: James Johnson announced his retirement from the Obama campaign, citing the increasing distraction as a result of this discovery.

If you want to snag a foreclosure property on the cheap, take a look at the new improved Zillow.

The real estate listing company announced the launch of its so-called “Foreclosure Center” today, which includes tutorials, buyer and seller guides, and most importantly, free foreclosure listings!

You can now access pre-foreclosures, foreclosure auctions, bank-owned properties, and more, alongside their standard listings.

Zillow estimates their pre-market inventory to total more than 1.5 million properties nationwide, along with another 250,000 properties that have already been foreclosed on.

They are also “surfacing” 67,000 foreclosure listings in their for-sale search category (I guess merging them?).

Now if only they could display all that shadow inventory as well…like the people about to walk away, or just behind on the mortgage.

Zillow’s Foreclosure Listings Include Pictures

For better or worse

You can actually get a lot of detail on these foreclosed properties

Including both interior and exterior photos

Which may reveal the condition some of these homes are in

This is what a foreclosed kitchen looks like after being ransacked and left for dead. At least they did some decorating.

So if you ever wanted to see what a gutted, foreclosed home looked like, wonder no longer.

Pictures aside, there are also details galore. Take a look at this screen grab from one property listed as a pre-foreclosure in auction status.

Check Out the Foreclosure Status in Great Detail

Instead of simply marking a property as “foreclosed”

Zillow provides the history of the foreclosure

Including the previous sale, when the NOD was filed

And when the foreclosure auction is scheduled to take place

It actually shows you when and where the auction is scheduled to be held.

The new improved listings also provide more background on the property, including when the owner was served a Notice of Default, the first step in the foreclosure process.

Additionally, there’s mortgage lender information so you can see which bank is involved in the sale, what the unpaid loan balance is, and if and when they acquire the property from the delinquent homeowner.

Finally, there’s trustee and/or attorney information as well

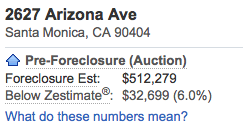

Introducing Foreclosure Estimates

They also provide foreclosure estimates

Which sadly aren’t known as Festimates (I wish!)

It’s basically what Zillow expects the property to sell for

Taking into account that it’s a foreclosed property

Zillow has also come up with so-called “Foreclosure Estimates,” which flank their flagship Zestimates and Rent Zestimates. Why they aren’t called “Festimates” is beyond me.

This figure is essentially what Zillow thinks the property will sell for, and is represented as a dollar amount and percentage relative to the Zestimate.

They tend to be estimated to sell below the Zestimate, which makes sense given that they are foreclosures.

Still, some of the properties will sell above their listing price and below the Zestimate.

Hopefully Zillow will include data about what foreclosed properties sell for versus traditional sales in the future.

Timing Is Everything Though…

Zillow always seems to be a bit behind

When it comes to providing fresh data

So while it’s nice to have access to a wealth of foreclosure information

It needs to be up-to-date to be of any use to a potential home buyer or investor

I hate to break up this party, but Zillow still faces some challenges with its new foreclosure listings.

While they may be winning on the information front, their timing is still a little off.

I browsed a few of their foreclosure listings and noticed that their info was outdated in many cases.

For example, one property listing was chock full of foreclosure information, but didn’t contain any new data since July.

Meanwhile, over on Redfin it was listed as a pending sale as of October 19th.

Redfin actually addressed this issue earlier this month, when it claimed to have much better data than its peers.

For example, it noted that it has 100% of agent-listed homes available, versus only 81% for Trulia and 79% for Zillow.

Additionally, the company said nearly two out of every five listings on Zillow and Trulia are no longer for sale, compared to just one out of 1,000 at Redfin.

The median day to publish a new listing was zero days for Redfin, seven days for Zillow, and nine days for Trulia.

Of course, they only looked at 11 metros in the U.S., though they were major ones like Los Angeles and Chicago.

However, I did come across foreclosure listings in Zillow that didn’t appear on Redfin.

So at the end of the day, you really still need to scour all of these sites simultaneously to ensure you don’t miss a thing.

The bank then complained that Ginnie Mae reversed its course after a few weeks and left TCB empty-handed. It said that Ginnie Mae had nullified the bank’s priority lien after TCB had already loaned millions of dollars for the sake of RMF, affecting retirees and the Home Equity Conversion Mortgage (HECM) program. The HECM program … [Read more…]