Rates were already high coming into this week. As of last Friday, that meant an average 30yr fixed rate just under 7.5%. As of this Friday, we’re closer to 8%.

Certain lenders may be quoting lower rates, but that often involves the presence of discount points. The Freddie Mac survey (orange line above) doesn’t account for discount points. It’s also a weekly average and has not yet counted the rates seen on Thursday or Friday.

Friday brought a sharp rise to the highest levels in 23 years. The most obvious culprit was the big monthly jobs report which showed job creation (nonfarm payrolls) increasing far faster than economists predicted. It was one of only a handful of months in the past few years that came in higher than the 12 month trailing average.

Perhaps just as importantly, this is a level of job growth (336k) that falls at the upper edge of the pre-pandemic range.

Most economists thought we wouldn’t be breaking back above 300k after averaging less than 200k for the past 3 months. In a world where the Fed constantly reiterates “data dependence,” this was a blow for rates. 10yr Treasury yields–the most ubiquitous long-term rate benchmark–left no doubts as to the bond market’s response.

It’s easy enough to see the vertical line after the jobs data, but what’s up with the fairly big recovery later in the day? If bonds are freaked out about data, why would they erase a majority of the losses?

There are a few reasons. The best one is actually the most esoteric as it has to do with the tendency for traders to close out trading positions on Fridays and especially on the Fridays before 3-day weekends. If traders were betting on higher rates (and they were!), the closing of those positions would bring rates back down a bit.

Ultimately, that position closing doesn’t really change the bigger picture. In fact, the jobs report reaction barely sticks out on a longer term chart. What DOES stick out is the shift in momentum that began after the last Fed day–the one we’ve discussed a few times now as the market’s way of repricing toward a “higher for longer” rate trajectory.

It continues to be the case that economic data needs to be substantially more downbeat on a consistent basis (2-3 months) in order for the Fed to acknowledge that a true shift is taking place and that the end of their “higher for longer” policy stance is up for discussion. Only then would rates have a chance to meaningfully decline.

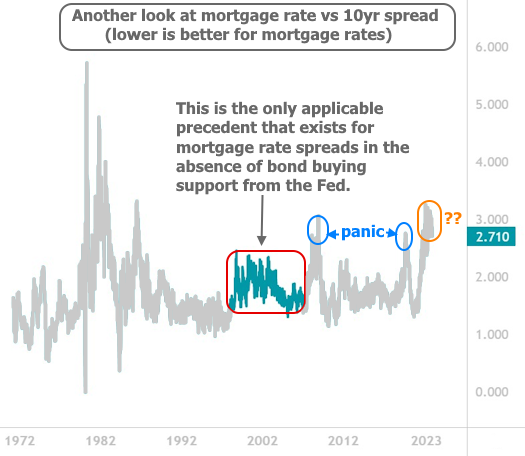

Still, there’s lots of hope out there that rates could/should decline for other reasons. One observation that’s become quite popular is the wide spread between mortgage rates and 10yr Treasury yields. For some reason, people think if spreads could only be a bit more narrow, mortgage rates could be more tolerable without the need for any major change in the broader bond market.

The following chart shows mortgage rates and 10yr yields on the same axis. It’s hard to track spreads with a chart like this, but it’s easy to see why the 10yr is used as a benchmark for mortgages!

The next chart makes the change in spreads easier to track. It is quite simply the value of the blue line above minus the value of the orange line. It shows that people might not be too crazy to hope for a return to a more normal spread range. After all, if we’re near 3% right now, a move down to 2% would put the average mortgage lender back in the high 6% range for a 30yr fixed.

A 2% spread is probably something that can be reasonably entertained, but some pundits are talking about spreads in the 1 to 1.5% range. A tightening of that magnitude is highly unlikely in the short term and possibly even “ever.” To talk about why, we first need a quick refresher on the Fed’s role in the mortgage market.

In order to prevent more catastrophic outcomes from the Great Financial Crisis, the Fed began buying large amounts of mortgage-backed securities (MBS) in 2009. In conjunction with the Fannie/Freddie conservatorship, this calmed investors and brought spreads down (mortgage buyers demand higher yields/rates when mortgage debt is perceived as more risky, thus inflating spreads).

Over the next decade, the Fed would not be able to stop buying MBS for long without spreads blowing out. Notably, there was only about a year of time before covid that the Fed was actually decreasing the amount of MBS it owned. That year coincided with broadly lower rates due to the trade war, and a lower rate trend helps spreads stay more narrow than they otherwise would be.

Why can’t we use the time before the financial crisis as a spread baseline? We can, to some extent, but nothing before the housing reforms of the mid 90s which expanded accessibility to mortgage financing and made the landscape riskier for investors. There is a very obvious bump in spreads at that time, and that marks the only real baseline that matters. Here’s the same chart, but with that time frame highlighted.

Since covid, we’ve had two instances of panic. The first was addressed with the most massive glut of Fed bond buying in the history of Fed bond buying. It crushed spreads and set us up for the world of pain we’re in now. As the Fed once again began shrinking its mortgage holdings in 2022, spreads blew out again. Combined with the surge higher in benchmark rates and the overall volatility (both things that hurt mortgage spreads) we saw even higher levels at the end of 2022.

But now, miraculously, without any Fed intervention, spreads have been grinding to slightly narrower levels. Sure, they’re still very wide, historically, but the Fed will definitely not be riding to the rescue this time around. Moreover, policymakers won’t likely be concerned enough to do anything about it until and unless a broader interest rate correction fails to help mortgage rate spreads come in a bit. Fortunately, a broader interest rate correction will almost certainly do just that. Just don’t expect it to restore the 1.0-1.5% spread level any time soon.

Think of it more like this: if 10yr yields find a scenario where they can rally down to 3.5% and spreads can return to 2.0%, that puts a 30yr fixed mortgage rate at 5.5%. At that level, the conversations about the weird things that need to happen to save the mortgage market would be very different, or altogether unnecessary.

Editorial Note: Blueprint may earn a commission from affiliate partner links featured here on our site. This commission does not influence our editors’ opinions or evaluations. Please view our full advertiser disclosure policy.

Getty Images

The average rate on a 30-year fixed mortgage is 7.65%, and on a 15-year fixed-rate mortgage, it’s 6.82%. The average rate on a 30-year jumbo mortgage is 7.44%.

*Data accurate as of September 7, 2023, the latest data available.

30-year fixed mortgage rates

The average mortgage rate for 30-year fixed loans rose today to 7.65% from 7.53% last week, according to data from Curinos. This is up from last month’s 7.47% and up from a year ago when it was 5.47%.

At the current 30-year fixed rate, you’ll pay about $710 each month for every $100,000 you borrow — up from about $701 last week.

Ready to buy? Compare the best mortgage lenders

15-year fixed mortgage rates

The mortgage rates for 15-year fixed loans inched up today to 6.82% from 6.76% last week. Today’s rate is up from last month’s 6.78% and up from a year ago when it was 4.82%.

At the current 15-year fixed rate, you’ll pay about $889 each month for every $100,000 you borrow, up from about $885 last week.

30-year jumbo mortgage rates

The mortgage rates for 30-year jumbo loans rose today to 7.44% from 7.34% last week. This is up from last month’s 7.25% and up from 5.02% last year.

At the current 30-year jumbo rate, you’ll pay around $695 each month for every $100,000 you borrow, up from about $689 last week.

Methodology

To determine average mortgage rates, Curinos uses a standardized set of parameters. For conventional mortgages, the calculations are based on an owner-occupied, one-unit property with a loan amount of $350,000. For jumbo mortgages, the loan amount is $750,000. These calculations assume an 80% loan-to-value ratio, a credit score of 740 or higher and a 60-day lock period.

Frequently asked questions (FAQs)

Mortgage rates are determined by a variety of factors, including the overall economy, inflation and the actions of the Federal Reserve. Mortgage lenders then set their loan rates based on these economic elements.

The rate you’re offered on a mortgage will also depend not only on the lender but also on your credit score, income, debt-to-income (DTI) ratio and other parts of your financial profile.

If you opt for a rate lock, you can typically do so for 30 to 60 days, depending on the lender. In some cases, you might be able to lock in your rate for up to 120 days.

Keep in mind that while some lenders allow you to lock in a mortgage rate for free, you’ll likely have to pay a fee for a longer lock period. This fee generally ranges from 0.25% to 0.5% of your loan amount. You could also be charged a fee if you want to extend the lock period — usually 0.375% of the loan amount.

There are several strategies that could help you qualify for the best mortgage rate, such as:

Checking your credit: When you apply for a mortgage, the lender will review your credit to determine your creditworthiness as well as your interest rate. In general, the higher your credit score, the lower your rate will be. So before you apply, it’s a good idea to check your credit to see where you stand. If you find any errors in your credit report, dispute them with the appropriate credit bureau to potentially boost your score.

Comparing lenders: Taking the time to shop around and compare your options from as many lenders as possible can help you find the best deal. In addition to rates, make sure to also consider each lender’s terms, fees and eligibility requirements.

Improving your credit score: If you have less-than-perfect credit and can wait to apply for a mortgage, it could be worth working to improve your credit beforehand to qualify for better rates in the future. Some possible ways to boost your credit include paying all of your bills on time and aiming to keep your credit utilization (the amount of credit you’ve used compared to your credit limits) on credit cards and lines of credit at 30% or less.

Reducing debt: Paying down debt could help lower your DTI ratio, which is how much you owe in monthly debt payments compared to your income. Having a lower DTI ratio can make you look like less of a risk in the eyes of a lender, which can result in a lower rate.

Choosing a shorter repayment term: Lenders typically offer lower rates to borrowers who opt for shorter terms. For example, you’ll likely get a lower rate on a 15-year mortgage compared to a 30-year loan.

Blueprint is an independent publisher and comparison service, not an investment advisor. The information provided is for educational purposes only and we encourage you to seek personalized advice from qualified professionals regarding specific financial decisions. Past performance is not indicative of future results.

Blueprint has an advertiser disclosure policy. The opinions, analyses, reviews or recommendations expressed in this article are those of the Blueprint editorial staff alone. Blueprint adheres to strict editorial integrity standards. The information is accurate as of the publish date, but always check the provider’s website for the most current information.

Jamie Young is Lead Editor of loans and mortgages at USA TODAY Blueprint. She has been writing and editing professionally for 12 years. Previously, she worked for Forbes Advisor, Credible, LendingTree, Student Loan Hero, and GOBankingRates. Her work has also appeared on some of the best-known media outlets including Yahoo, Fox Business, Time, CBS News, AOL, MSN, and more. Jamie is passionate about finance, technology, and the Oxford comma. In her free time, she likes to game, play with her two crazy cats (Detective Snoop and his girl Friday), and try to keep up with her ever-growing plant collection.

Megan Horner is editorial director at USA TODAY Blueprint. She has over 10 years of experience in online publishing, mostly focused on credit cards and banking. Previously, she was the head of publishing at Finder.com where she led the team to publish personal finance content on credit cards, banking, loans, mortgages and more. Prior to that, she was an editor at Credit Karma. Megan has been featured in CreditCards.com, American Banker, Lifehacker and news broadcasts across the country. She has a bachelor’s degree in English and editing.

Ashley is a USA TODAY Blueprint loans and mortgages deputy editor who has worked in the online finance space since 2017. She’s passionate about creating helpful content that makes complicated financial topics easy to understand. She has previously worked at Forbes Advisor, Credible, LendingTree and and Student Loan Hero. Her work has appeared on Fox Business and Yahoo. Ashley is also an artist and massive horror fan who had her short story “The Box” produced by the award-winning NoSleep Podcast. In her free time, you can find her drawing, scaring herself with spooky stories, playing video games and chasing her black cat Salem.

Home loan borrowers, who were hoping to get some reprieve from high interest rate, are in for another disappointment. The Reserve Bank of India (RBI) has yet again decided to hold the repo rate, which has diminished the hope for any meaningful reduction in home loan interest rate in the near future. How long will the borrowers have to wait to see a fall in interest rate? What is the best way to manage a home loan in the current high interest rate regimen?

Home loan borrowers, especially the ones who took a home loan before May 2022, are going through one of the most difficult times. This is because the RBI raised the repo rate by 2.5% from May 2022 to February 2023. All floating rate home loans are now linked to an external benchmark and the repo rate is the benchmark for most such home loans. So, if the repo rate goes up, the interest rate of these home loans also go up by a similar quantum.

A 2.5% hike pushes EMIs up by 20% and total interest up by 44% Due to the steep rise in repo rate, these borrowers have seen an unprecedented increase in their home loan tenure or a steep hike in their home loan EMIs. For instance, on a Rs 50-lakh home loan taken for a tenure of 20 years, if you have to pay a higher interest rate of 9.5% instead of 7%, then your EMI goes up by 20% from Rs 23,259 to Rs 27,964. The impact on total interest payment during the tenure of the loan is overwhelmingly high as it goes up by 43.73% from Rs 25.82 lakh to Rs 37.11 lakh.

This kind of an adverse impact can jolt any borrower. The best remedy they can get against this hike is to see a similar rate reduction soon, but that is highly unlikely to happen. However, even a smaller reduction in interest rate can bring great relief. So what are the chances that the interest rate on these home loans will fall in the near future?

Will the interest rates fall any time soon?

The biggest relief home loan borrowers want is to see a significant fall in the interest rates so that their EMI burden comes down. So let us understand the likelihood of the interest rates coming down in the near future.Elevated inflation may not allow rates to fall soon The RBI has the primary responsibility to keep retail inflation in the range of 2-6%. If inflation remains above this range for a considerable period, the RBI is often compelled to go for a repo rate hike. So the direction of inflation is the most prominent factor that will determine the movement of the interest rate. Crude oil prices are one of the biggest drivers of inflation worldwide. From below $75 per barrel in June this year, Brent crude oil prices have gone up to over $90 per barrel. Therefore, a spike in inflation cannot be entirely ruled out. If inflation rises sharply, the central bank may have to go for a repo rate hike.

Upasna Bhardwaj, Chief Economist, Kotak Mahindra Bank, says the US dollar and bond yields have been on an uptrend. “Narrowing interest rate differentials to record low levels poses severe financial instability, thereby warranting a cautious approach by the RBI,” she says. Any action to reduce the rate will further reduce this differential and may put more pressure on the USD exchange rate, which the RBI would like to avoid.

However, the possibility of higher interest rates on short-term FDs cannot be ruled out. “We expect the RBI to prefer keeping the short-term rates elevated in the near term by using liquidity tools, given the pressure on INR and the underlying inflationary risks,” says Bhardwaj.

“We see cautious optimism in the governor’s speech. It suggests that things are difficult right now. But interest rates and inflation are on the right trajectory with limited upside risks, and the central bank will continue to manage growth expectations using all the tools of monetary policy,” says Adhil Shetty, CEO, Bankbazaar.com.

Another prominent indicator of the direction of the interest rates is the yield of the 10-year G-sec. Yield of the 10-year government bond, which had fallen below 7% in May, has risen above 7.2%. It indicates a rising trend in interest rate.

Another prominent factor that decides the interest rate’s direction is liquidity in the banking system. A tight liquidity situation pushes up the interest rates, especially on FDs with short tenures. “Liquidity conditions have tightened and borrowing costs have remained elevated since the last policy,” says a report published by CareEdge, a credit rating company. What it reaffirms is that the possibility of any reduction in interest rates is highly unlikely.

What should borrowers do? If you are a home loan borrower, there is hardly anything you can do about the interest rate movement, but you can at least ensure that you are getting the best possible deal on your home loan. If you are planning to buy a house and take a home loan then it will be a matter of relief that you would not need to pay higher interest rate.

“This steady repo rate is anticipated to foster stability in home loan lending rates, which is encouraging ahead of the festive season, where we expect the demand for homes to remain strong, especially in the luxury segment,” says Ashwin Chadha, CEO, India Sotheby’s International Realty.

As interest rates have peaked, most of the existing borrowers will be paying the highest interest rates seen in the last three years on their EMIs. If you are an old borrower, servicing a loan under previous regimes like the MCLR or base rate, then it may be a good time to shift to the new EBLR regime. This is because when there is a fall in interest rates, you will quickly benefit from it.

Compare your interest rate with those of other lenders. If you find that they are offering a much lower interest rate to a new borrower, you should consider transferring your loan after calculating the net benefit. However, if your lender is giving a much lower rate to new borrowers, then you may request your lender to reprice your loan at a lower rate. Lenders usually charge a repricing fee to restructure your loan at the new rate.

Regular partial prepayment is one of the best ways to pay off your home loan quickly. However, this option works only when you have adequate surplus to make the prepayments. If you have more money in hand after getting a salary raise, then you may consider increasing your EMI so that your total interest outgo can be brought down. If you get a bonus, incentive or any other form of windfall gain, consider going for partial prepayment so that your home loan outstanding comes down; this will help you reduce the tenure and total interest outgo on the loan.

As interest rates have reached very close to their peak home loan borrowers can expect things to get better from here as the chances of interest rate reduction appears to be higher. “Bond markets have already been discounting rate cuts, and 10-year G-Sec yields are down by 30 bps from this year’s peak levels. Home loan borrowers would do well to stick to their floating interest rate loans for now, even if fixed-rate loans are available at some discount,” says Anshul Gupta, Co-Founder and Chief Investment Office, Wint Wealth

This week has brought a series of fairly simple mornings with the initial reaction to economic reports playing out in a logical direction. Monday: stronger ISM pushed rates higher. Tuesday: stronger JOLTS caused heavy selling. Wednesday: weaker ADP helped bonds recover. Thursday: stronger claims led to initial selling pressure. Now today, the biggest report of the week is unsurprisingly producing the biggest result. Time to reset the clock on waiting for econ data to make a case for friendlier Fed policy and a better rate outlook.

The honey badger labor market woke up on Friday and chose violence, biting the legs of any job recession bear it could find. The first reaction from the bond market was to shoot up bond yields and mortgage rates went higher. However, as the day progressed, bond yields decreased from the peak.

What is going on with the U.S. labor market? The answer is that we are just working back to normal.

Jobs data

From BLS:Total nonfarm payroll employment rose by 336,000 in September, and the unemployment rate was unchanged at 3.8 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in leisure and hospitality; government; health care; professional, scientific, and technical services; and social assistance.

Nothing has changed from my long-term view on the labor market recovery premise I have written about for years. If COVID-19 had never happened, based on our population growth and job growth data pre-COVID-19, we should have between 157 million and 159million jobs today. Until we get into this ballpark range, it’s all make-up demand. Today, we stand at 156,874,000, so we are close to breaking into the makeup labor data pool.

Here is a breakdown of the jobs gained and jobs lost in today’s report

In this job report, the unemployment rate for education levels looks like this:

Less than a high school diploma: 5.5%

High school graduate and no college: 4.1%

Some college or associate degree: 3.0%

Bachelor’s degree or higher: 2.1%

From BLS: In September, average hourly earnings for all employees on private nonfarm payrolls rose by 7 cents, or 0.2 percent, to $33.88. Over the past 12 months, average hourly earnings have increased by 4.2 percent. In September, average hourly earnings of private-sector production and nonsupervisory employees rose by 6 cents, or 0.2 percent, to $29.06.

Wage growth data has been cooling down since January of 2022; we don’t see any data that would implicate a wage spiral. If the trend continues, we will be close to the Federal Reserve‘s target for wage growth next year with their goal of 2% inflation. To me, 3%-3.5% will make the Fed so happy, and If we get any productivity growth, that will be icing on the cake.

It’s been straightforward with the Fed, bond yields and mortgage rates in 2022 and 2023. I don’t believe the Fed will pivot until jobless claims break over 323,000 on the four-week moving average. The one data line improving since July has been jobless claims, and bond yields have been trending higher. The four-week moving average is running at 208,750.

Bonds and mortgage rates

What does this mean for mortgage rates and the bond market after a crazy week? The bond market is oversold so that a rally could happen anytime, but can it get much lower with the jobless claims data being this strong? As we can see in today’s action, bond yields shot up, moved lower, but still ended higher than today’s lows.

I am currently looking at the 4.87% level on the 10-year yield as a line in the sand. The 10-year yield has just had a massive sell-off, and we need to find a stable level to bounce from, or this can keep going higher and higher. We had a weak attempt by a few Fed presidents and Treasury Secretary Janet Yellen this week to try to talk the bond market down, but bond traders didn’t care much. Actions speak louder than words, and when the Fed went with a hawkish future outlook, it gave traders the green light to sell bonds. And the jobless claims data is too low for the Fed to pivot off that hawkish tone.

All in all, the jobs report was a good one with good revisions. Wage growth is cooling and most likely, we will see some negative revisions to this report. However, this doesn’t change my mindset about the labor data; we are still in make-up mode for labor and working our way back to a normal job market.

Over the next 12 months, there will be new variables to test the economy, not only with higher rates, but now student loan debt payments will need to be made. We will take the economic data one day at a time, but I believe the story so far in 2023 is how well the jobless claims data is doing and we can’t have a job loss recession in America until that data line breaks over 323,000.

There have been plenty of reports about lower-income borrowers getting the short end of the stick during the latest housing downturn.

And a new National Housing Survey from mortgage financier Fannie Mae might reveal why.

Based on the second quarter data in the report, it appears as if those with annual incomes of less than $50,000 are more likely to take someone else’s “word for it,” as opposed to doing their own research.

In fact, 30% of respondents in the survey defined as being “lower income” borrowers indicated that a mortgage broker’s recommendation would be a major factor in choosing a lender.

That compares to 20% for those earning $50,000 – $100,000, and 17% for top earners in the $100,000+ group.

The numbers are similar for using a real estate agent’s referral, at 29%, 20%, and 14%, respectively.

Lower income borrowers were also more than three times more likely to rely on lender advertising than the wealthiest group.

Richest Borrowers Took the Best Offer

Conversely, the richest of borrowers were most likely to be influenced by the competitiveness of the offer received.

More than three-quarters (76%) of the $100,000+ crowd said the best offer was a major influence, compared to just 54% of low-income borrowers.

So basically just more than half of low-income borrowers seemed to care what their mortgage rate was.

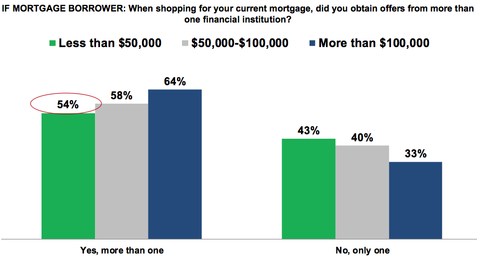

Wealthy borrowers also indicated that when shopping for a mortgage, they were more likely to obtain quotes from multiple banks and lenders.

I’ve said it many times before, and I’ll say it again, shop around! If you take the time to shop around for your big screen TV, surely you can shop for your mortgage.

Interestingly, lower-income borrowers were more likely to obtain mortgage quotes, or should I say their single quote, in person, whereas top earners did it by phone and seemed to get a better deal.

So much for that face-to-face trust perception…

[How many mortgage quotes should I get?]

The Rich Like Calculators

When it came time to decide how much one could afford, the richer borrowers were more likely to whip out a calculator.

Meanwhile, the majority of lower-income borrowers made calculations in their head or on a piece of paper.

They were also much less likely to use online tools or applications (mortgage calculators) to figure it out, despite these being readily available to anyone with an Internet connection.

And were more likely to let mortgage lenders, friends, family, co-workers, and real estate agents help them determine affordability.

[Mortgage vs. income]

Nobody Understands ARMs

Regardless of income, no one seems to understand how adjustable-rate mortgages work.

When respondents were asked to determine how much an ARM payment could rise, 37% of mortgage borrowers weren’t even able to offer up a guess.

On average, respondents estimated that mortgage payments on ARMs could only rise by about 10%, well below Fannie’s calculation of over 50%.

Clearly, ARM payments can reset a lot higher than 10%, though the mortgage caps in place limit those increases (and decreases) somewhat.

Fortunately, most borrowers these days are going with fixed-rate mortgages to avoid any misunderstanding.

The moral of this survey, like many before it, is that Americans continue to miss the mark when it comes to understanding how mortgages work.

This is unfortunate, given buying a home is often seen as the largest purchase an individual can make in their lifetime.

Perhaps poor financial education should be added to my lists of causes of the latest mortgage crisis.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

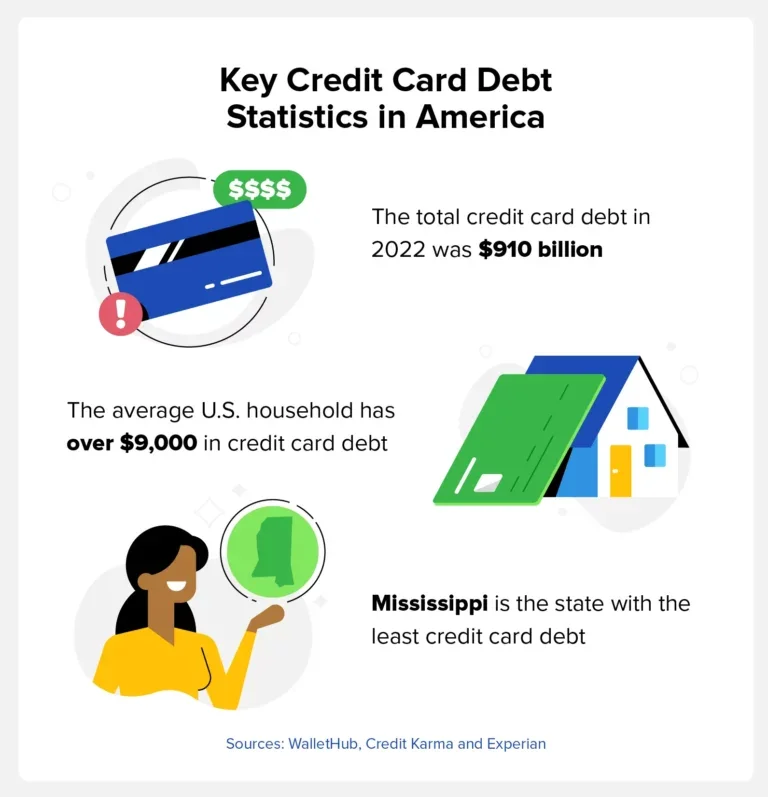

The average household credit card debt in America is $9,654, and the states with the largest amount of credit card debt are Alaska, Hawaii, and New Jersey.

Between the first quarters of 2022 and 2023, The Federal Reserve Bank of New York reported that the credit card debt in America rose by $145 billion. As of June 2023, we saw a 12-month inflation increase of 3%, the smallest year-over-year increase since March 2021.

By understanding American credit card debt statistics, you’ll better understand where you stand and what you can do to potentially lower your debt. Credit card debt increases your credit utilization ratio, which can hurt your credit and ultimately cost you more money in interest.

We surveyed over 1,100 Americans to learn more about credit card debt statistics in the United States. This data covers the average debt by state, average interest rates, and more. While many of the statistics from our other sources look at the situation as a whole, our data helps us see what’s happening on an individual level.

Despite the national average of Americans having over $9,000 in credit card debt per household, only 14% say they’re “very worried” about their debt.

67% of respondents said they have less than $2,000 in debt, which may indicate that only a concentrated number of people have high amounts of credit card debt.

20% of respondents don’t know how long they’ve been in debt.

The majority of respondents (56%) say their credit card debt is due to unexpected expenses.

74% of respondents said at least one collection agency has contacted them about a past due debt.

In this article, we’ll also provide tips on how to get out of debt and work toward better credit.

Table of contents:

Key Credit Card Debt Statistics

Many factors play into credit card debt, such as the average interest rates, which cards have the best offers, and the balance people carry on their card. These statistics will help you compare your own credit card balance to the national average and see if you’re getting a good deal with your current cards.

Here are the standout findings of various debt statistics:

The average American household has over $9,000 in credit card debt. (WalletHub)

Mississippi has the least credit card debt at $5,259 per person. (Credit Karma)

Alaska has the most credit card debt on average at $8,139. (Credit Karma)

Credit cards 90 days or more past due rose to 4.57% in 2023. (FRBNY)

Individuals making $184,000 or more per year have the most credit card debt at an average of $12,600. (Federal Reserve)

The total credit card debt in America as of Q3 2022 was $910 billion. (Experian®)

How Many Credit Cards Carry a Balance

The American Bankers Association releases a quarterly report for consumer credit conditions, and the most recent data comes from the third quarter of 2022.

In America, approximately 43% of credit cards carried a balance, 23% were dormant, and 34% were used but paid off each month. Those who pay off their credit card balance are able to keep a low credit utilization ratio and prevent the accumulation of debt.

Tip: Use our credit card payoff calculator to estimate when you’ll be debt free.

Average Interest Rates for New Credit Card Offers

LendingTree analyzed the terms and conditions of 200 credit cards from upwards of 50 different credit card companies, banks, and credit unions. With this data, they were able to gather an assortment of information involving annual percentage rates (APR).

The APR is the amount of interest consumers pay for their purchases, and the following table is broken down by credit card type.

The following table is based on data from July 2023.

Average Credit Card Debt by State

In February 2023, Credit Karma gathered data from 74 million of their members to see which states had the most and least amount of credit card debt. Below, we’ve compiled a complete list based on Credit Karma’s data that contains the average credit card debt for each of the 50 states alphabetically.

Top 10 States With the Most Credit Card Debt

The following states had the most credit card debt, with Alaska having the highest average credit card debt in America at $8,139 per person.

State

Average credit card debt

1.

Alaska

$8,139

2.

Hawaii

$7,444

3.

New Jersey

$7,306

4.

Maryland

$7,248

5.

Virginia

$7,174

6.

Connecticut

$7,032

7.

New York

$7,029

8.

California

$6,952

9.

Washington

$6,869

10.

Florida

$6,783

Top 10 States With the Least Credit Card Debt

The major credit bureau, Experian, tracks credit card debt data as well and found that between 2021 and 2022, overall credit card debt in the U.S. increased from $785 billion to $910 billion—a 16% increase. The average debt also increased in many states, according to Credit Karma’s report.

State

Average credit card debt

1.

Mississippi

$5,259

2.

Kentucky

$5,455

3.

Wisconsin

$5,593

4.

Arkansas

$5,600

5.

Indiana

$5,601

6.

Alabama

$5,647

7.

West Virginia

$5,674

8.

Iowa

$5,732

9.

Idaho

$5,737

10.

Maine

$5,788

Average Credit Card Debt by Age

Credit Karma’s report with the state-by-state data also broke down credit card debt by age group. Currently, Generation X carries the most credit card debt, while Generation Z carries the least.

Age group

Average credit card debt

11-26 (Generation Z)

$2,781

27-42 (Millennials)

$5,898

41-58 (Generation X)

$8,266

59-77 (Baby Boomers)

$7,464

78-95 (Silent Generation)

$5,649

Average Credit Card Debt by Income

The following data comes from the Federal Reserve’s Survey of Consumer Finances (SCF) and was most recently updated in 2019. The Federal Reserve completed a new survey at the end of 2022 and will have updated data later in 2023.

As you’ll see, higher-income individuals have much more credit card debt than those who make less. This makes sense because high-income individuals are able to get much larger credit lines. But when you look at the debt-to-income ratio, lower-income households have much more consumer debt compared to the amount of money they make.

Percentile of Income

Average credit card debt

Less than 20%

$3,800

20%-39%

$4,700

40%-59%

$4,900

60%-79%

$7,000

80%-89%

$9,800

90%-100%

$12,600

Average Household Credit Card Debt

A recent study from WalletHub found that while total credit card debt in the United States rose 14.1% between 2022 and 2023, household credit card debt only rose by 8.39%.

Their data shows that the average household credit card debt at the end of the first quarter in 2023 was $9,654 adjusted for inflation, which is $738 higher than the same time the previous year. WalletHub’s chart goes back to 1986, and the highest household credit card debt was in 2007 when it was $12,221 on average per household.

Average Credit Card Debt by Race or Ethnicity

Research from Annuity.org shows that Black and Hispanic Americans are less likely to feel financially stable and less likely to have a bank account. This information can help us better understand what’s happening in the financial lives of different communities.

This data comes from the Federal Reserve’s 2019 SCF.

Race

Average credit card debt

White (non-Hispanic)

$6,940

Black or African American (non-Hispanic)

$3,940

Hispanic or Latino

$5,510

Other or multiple races

$6,320

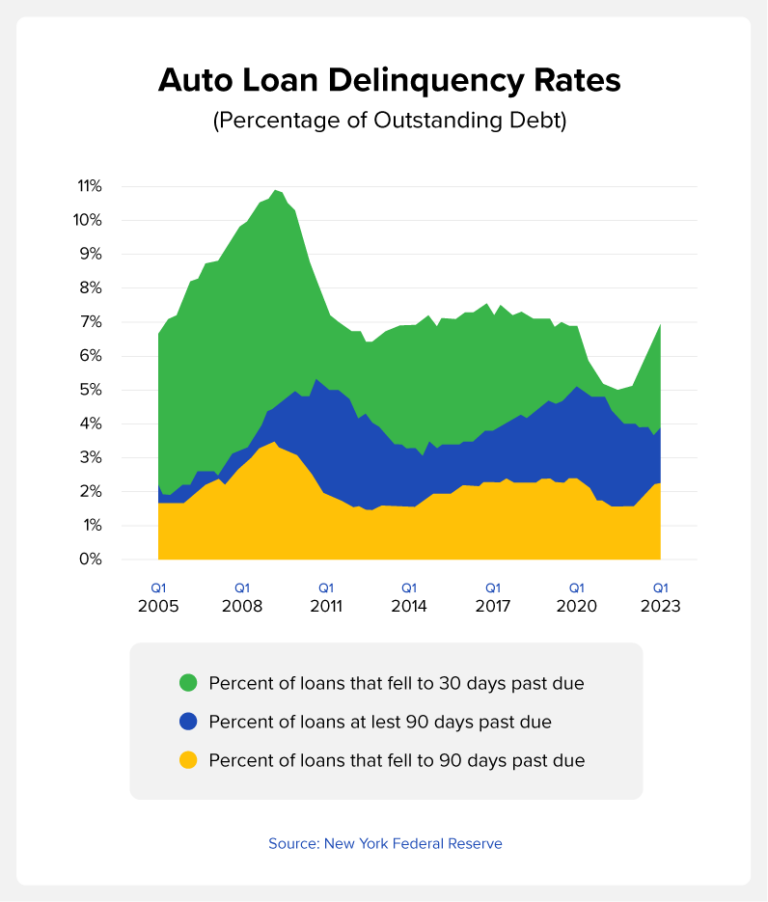

Credit Card Delinquency Rates in America

When someone is at least 30 days past due on their credit card payment, their status becomes delinquent. The number of delinquencies in the United States can be a measure of people’s ability to pay down their credit card debt.

To track this data, Experian conducted a study between 2021 and 2022:

Accounts 30 to 59 days past due increased from 1.04% of total accounts to 1.67%.

The delinquency rate of accounts 60 to 89 days past due increased to 1.01%.

Accounts 90 to 180 days past due rose to 0.63%.

How to Get Out of Credit Card Debt and Improve Your Credit

Credit card debt in America is something many individuals struggle with, and when your debt isn’t under control, it can affect your credit. A lower credit score leads to higher interest rates, which means you’re paying more for your purchases. It can also lead to being denied new credit lines.

Here are some simple steps you can take to start getting out of debt sooner rather than later:

Reduce additional credit card spending: You don’t want to add to your current debt if you don’t have to.

Create a budget: Cutting your spending can help you save additional funds to pay down your debt.

Use the snowball method: Each month, pay off your smallest debt in full. This can help you build momentum as you chip away at your overall debt.

Try debt consolidation: Consolidating your debt may help reduce the interest rate and keep your debt in one place rather than with different creditors.

Get a balance transfer card: Balance transfer cards allow you to transfer credit card debt to a different account, which may have a lower interest rate and will also help you consolidate your debt.

If you need help getting your debt under control and improving your credit, Credit.com has resources to help you learn to better manage your finances. To begin managing your credit, sign up for a free credit report card and check out ExtraCredit®. Our services can help you learn how to work on your credit and educate you about managing your finances so you know how to work toward the life you want.

Methodology for Credit.com data: This survey was conducted for Credit.com using Suzy. The sample consisted of a total of 1,154 responses per question and is statistically representative of the general population. This survey was conducted in December 2022.

The amount you need to borrow to buy a new or used car is higher than normal due to the COVID-19 pandemic. Although the world appears to be back to normal, during the height of the pandemic, there were many supply chain shortages and factory shutdowns. Due to supply and demand, this made the price of vehicles higher than normal. Although people are still trying to get their finances back on track post-COVID, we’re still experiencing the effects as the world recovers.

Credit Score

New vehicles

Used vehicles

All

$40,068

$25,041

781 to 850

$36,663

$27,303

661 to 780

$42,438

$28,402

601 to 660

$43,807

$26,527

501 to 600

$40,746

$23,065

300 to 500

$36,690

$19,912

Total Auto Loan Debt in America

During the first quarter of 2011, the total auto loan debt in America was close to $700 billion. Since then, it’s more than doubled and was over $1.5 trillion by 2023. Not only are vehicle prices continuing to rise over the years, but part of the overall debt may be due to more people having access to auto financing as well.

Auto Loans as Percentage of Consumer Debt

As mentioned earlier, buying a vehicle is one of the largest purchases you’ll ever make. Millions of Americans are in debt, and a lot of this comes from auto loans. The average American credit card debt is only 5.8% of consumer debt, but auto loans are the third largest portion at 9.2% of consumer debt. The two largest amounts of debt come from mortgages and student loans.

How Much Do Americans Borrow for Car Loans?

Each quarter, Americans borrow money to purchase new and used vehicles. In 2011, Americans borrowed a little over $72 billion during the first quarter. As you can see in the chart below, the number rises and falls over the years, but as of the first quarter of 2023, the quarterly total is close to $159 billion. This is lower than the third quarter of 2022, when it was over $181 billion.

Average Car Loans by Age Group

The age group that takes out the largest auto loans is those between the ages of 30 and 49. During the first quarter of 2023, Americans between 30 and 39 took out about $37 billion in auto loans, and those 40 to 49 took out $36.5 billion. The lowest borrowers are younger people ages 18 to 29 as well as the older age group of 50 to 59.

Average Car Loan Term by Credit Score

The loan term of your car is the length of the loan if you’re making minimum monthly payments. The loan term is shorter when you make extra payments or larger payments. Based on the recent data from Experian, people with credit scores of 601 to 660 have the longest loan terms for new vehicles. When you have a longer loan term, you’re also paying more in interest fees, which you can see by using a simple loan calculator.

Credit score

New vehicle loans (in months)

New leased vehicles (in months)

Used vehicle loans (in months)

Overall average

70.5

35.88

66.11

781 to 850

61.6

35

64.7

661 to 780

70.15

35.91

68.41

601 to 660

74.20

36.30

68.34

501 to 600

73.80

36.31

66.27

300 to 500

72.79

N/A

62.85

Car Loans by Lender Type

When purchasing a new or used vehicle, you have a variety of options for lenders. For new vehicles, most people use dealer financing, which is 54% of new car loans. Used vehicles have more of a mix with people using banks, credit unions and other options. “Buy here, pay here” lenders typically have the highest interest rates and market toward people with poor credit.

4 Tips to Lower Your Car Payments

If you’re in the market for a new car, there are ways that you can lower your car monthly car payments. Knowing these tips before walking into the dealership can help you create a plan. Below, we list four ways to lower your monthly payments:

Put down a larger down payment: Your monthly payments are based on your overall loan amount. When you make a larger down payment, you have lower monthly payments.

Trade in your old vehicle: If you don’t have the money for a larger down payment, your old vehicle has a value the dealer applies to lower the loan amount. You can also trade in your vehicle and make a larger down payment.

Extend the loan term: By opting for a longer loan term, your monthly payments will be less.

Improve your credit: Improving your credit score is one of the best ways to lower your monthly payments because you’ll likely get a better interest rate, which also decreases the total amount of a vehicle.

When buying a vehicle, keep in mind that although lower monthly payments are helpful, the more important factor is the overall cost of the car. A longer loan term may lead to lower monthly payments, but you may pay thousands more for the car due to interest fees.

How Your Credit Score Affects Your Car Payments

Your credit score is a determining factor when getting a car loan, so it’s beneficial to improve your score before getting an auto loan. The average car loan interest rate for those with low credit scores can be 2% to over 13% more than someone with a good credit score.

If you’re unsure of your credit score, get a copy of your free credit report card to find out. You can also sign up for ExtraCredit® and receive additional credit reporting, which may help you know where you need to work on your credit.

Many or all of the products featured here are from our partners, who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

On average, homeowners insurance in the United States is $1,424 annually and about $118 per month. This price varies based on the state you live in, along with other factors like previous home insurance claims, credit score, and the age of your home.

If you’re buying a home, there are a lot of cost considerations, from the monthly closing costs to the mortgage payments and interest rate. One factor many people often overlook is the additional cost of home insurance. To properly budget for your new dream home, it’s helpful to know the average cost of home insurance in your state.

Today, we’ll go over the average insurance cost for each state, which companies have the best rates, and what factors can affect your rates. By learning more about home insurance, you can find the best deals to save money and enjoy the experience of moving into your new home. If you’re considering moving to a new state, this information may also help influence your decision.

Table of contents:

Homeowners Insurance Facts

The cost of your homeowners insurance is affected by various factors. The cost of homeowners insurance can vary by state because some states are more prone to natural disasters than others. For example, Florida is more prone to hurricanes than other states, so the average cost is higher than in a state like Nevada.

As you’ll learn, homeowners insurance can range from less than $1,000 to over $3,000 per year. Here are some key facts about homeowners insurance in the United States:

The average annual cost of homeowner’s insurance in the United States is $1,424.

The state with the cheapest homeowners insurance at $382 per year is Hawaii.

Oklahoma has the highest homeowners insurance rates, averaging $3,659 annually.

Portland, Oregon, is the most populous city with the lowest average annual insurance rate at $686 per year.

People with a credit score of 740 or higher have the lowest average insurance rates at roughly $1,207 per year.

Average Cost of Home Insurance by State

The overall average cost of home insurance in the United States is $1,424 annually or $118 per month.

The following chart and table show the average cost of home insurance for each state and includes Washington, D.C. These prices are based on $250,000 for dwelling coverage.

Top 5 States With the Cheapest Homeowners Insurance Rates

Hawaii has the lowest annual rate of $382 per year, which is 73% lower than the national average. Vermont, Delaware, Utah, and Oregon are also in the top five states with the lowest homeowners insurance rates, and each is close to 50% lower or more than the national average.

Hawaii: $382 per year

Vermont: $658 per year

Delaware: $679 per year

Utah: $696 per year

Oregon: $723 per year

Top 5 states With the Most Expensive Homeowners Insurance Rates

The states with the most expensive homeowners insurance rates in the country are Oklahoma and Kansas at $3,659 per year and $3,083 per year respectively. Some of the other states with the highest rates include Nebraska, Colorado, and Arkansas.

According to Insurance.com, these states have high rates because they’re more likely to experience tornadoes, hurricanes, hailstorms, and other natural disasters.

Oklahoma: $3,659 per year

Kansas: $3,083 per year

Nebraska: $2,951 per year

Colorado: $2,152 per year

Arkansas: $2,123 per year

Average Cost of Homeowners Insurance by City

The city you live in may also determine the cost of your homeowners insurance rates. In addition to the possibility of natural disasters, population, crime statistics, and local materials and labor costs are also factors.

The following cities are the 25 largest cities in the United States, organized alphabetically. The table includes their average annual and monthly rates.

How Much Does Homeowners Insurance Cost by Company?

As with all forms of insurance, it’s typically a good idea to shop around for the best rates. Your rates may change depending on the provider based on the size of your home, claim history, and additional factors. And keep in mind that the level of coverage will also change the cost of your insurance premiums.

The following table shows 11 of the country’s most popular homeowners insurance providers sorted by annual rates.

4 Factors That Can Affect Homeowners Insurance Rates

Outside of your home’s location, some other factors can determine the cost of homeowners insurance. We’ve listed four of the most common factors that could affect your insurance rates.

1. Credit Score

Some states may look at your credit score to help determine your rates. Your credit score may be a factor because a low credit score or bad credit history can be considered a risk factor.

There are some exceptions. According to Experian®, states like California, Hawaii, Maryland, and Massachusetts prohibit using credit scores as a determining factor for insurance rates.

Credit Score:

Poor (300-579)

Fair (580-669)

Good (670-739)

Excellent (740-850)

Average Annual Rate:

$3,274

$1,571

$1,428

$1,207

2. Claims History

Similar to automotive insurance rates, if you have an extensive history of home insurance claims, this can raise the price of your rates. Although you have less control over the damage that may happen to your home, insurance companies require higher premiums to help cover the costs of damages or injuries.

This table shows what types of claims may raise your rate based on the average amount paid out for the claim. The average payouts are taken from the Insurance Information Institute’s research for dwellings with $250,000 in coverage.

Type of Claim

Average Dollar Amount of Claim Paid Out

Average Annual Rate After a Claim

Wind

$11,650

$1,570

Liability

$30,324

$1,749

Theft

$4,415

$1,763

Fire

$77,340

$1,773

3. Deductible Amount

Your deductible is another factor to consider. Some people opt for a higher deductible because it lowers their rate. Should something happen to your home, you’ll have a higher out-of-pocket expense due to that higher deductible. This is helpful to remember as you budget around your home insurance costs.

Another consideration is that while you may save money while paying for your homeowners insurance, you may face financial hardships should you need to file a claim.

Deductible Amount

Average Annual Rate

$1,500

$1,368

$2,000

$1,273

$5,000

$1,111

4. Age of Home

If you own an older home, it may be more expensive to repair the home if it’s damaged. Older homes typically have higher rates due to these higher costs for repairs. The repairs are often more expensive, and the contractors may need to bring the home up to the most current building and safety codes. The first year of recorded data was in 1959.

What Does Homeowners Insurance Cover?

Knowing what your homeowners insurance policy covers can help you better prepare for situations when you might need to use it. With a better understanding of what is and isn’t covered, you can protect yourself from the potential of financial losses if you need to file a claim.

Depending on which insurance provider you choose, they may offer some or all of the following coverages.

Dwelling coverage: The averages listed throughout this post are based on the dwelling coverage of $250,000, which means the insurance will cover up to $250,000 in repairs. Should you get a policy with a higher dwelling coverage amount, more repairs will be covered.

Additional structures: Basic dwelling coverage covers damages to your home, but if you have other structures like a guest house, shed, or detached garage, you’ll need this extra coverage. This coverage is often 10–20% of the dwelling coverage’s limit.

Medical payments: If someone who doesn’t live in your home gets injured on your property, you can get coverage for their medical payments. Medical payment coverage usually ranges from $1,000 to $5,000 of coverage.

Personal liability: Personal liability coverage can be between $100,000 and $500,000, which is for property damage to someone else’s property or if you’re legally liable for injuries on your property. Personal liability coverage may also cover legal fees if someone were to sue you after being injured.

Loss of use: If your home gets damaged to the point where you cannot live there until the repairs are done, this coverage will help cover living expenses. Loss of use coverage can range from 10% to 30% of dwelling coverage.

Personal property: Ranging from 50% to 75% of your dwelling coverage, this provides coverage for the personal property in your home, like clothing, furniture, and electronics. If you have this coverage, be sure to read the details because it may have a max limit of coverage on certain types of items.

What Characteristics Affect Homeowners Insurance?

Earlier, we went over different factors that can affect your homeowners insurance, like your credit score and history of claims. Home and location characteristics may also give you lower or higher rates.

Home Characteristics

Various characteristics of your home and how it’s built may make it more at risk for damage. As with other forms of insurance, if there are higher risks, they can increase your rates.

One of the common characteristics affecting your rates is the condition of your roof. Your roof is a primary part of your home that protects the inside of your home. If you have an older roof that may not withstand harsh weather or is made from poor materials, you may have to pay a higher insurance rate.

Some insurance providers may also have higher rates for special features. Some of these include having a pool, hot tub, sauna, or any other feature that may cause an injury.

Location characteristics

Earlier, you learned how the average home insurance cost varies from state to state, and much of this has to do with the area’s characteristics. In addition to weather risks, home insurance rates are often higher in areas prone to wildfires. Some insurance providers calculate risk based on how close the home is to fire stations and fire hydrants.

Another location characteristic that home insurance providers look at is crime rates. Home insurance policies may have theft coverage, but in higher crime areas, the rates will be higher due to a higher likelihood of break-ins. Sometimes, you can lower your insurance rates by installing security measures like cameras and alarms.

8 Ways to Lower the Cost of Your Homeowners Insurance

Your mortgage is the primary expense for your home, and it’s important to factor in the cost of your homeowners insurance as well for budgeting purposes. Fortunately, there are ways to lower your homeowners insurance through different methods. Here, we’ve listed different ways you can get better rates for your home insurance.

Improve your credit score: Many states allow insurance providers to use your credit score as a factor. By improving your score, you can likely lower your rates.

Bundle your policies: You may be able to bundle your home and car insurance for a better price on both.

Do some renovations: An old roof or out-of-date parts of your home may increase your rate, so it might be worth it to do some renovations.

Opt for the higher deductible: Although you’ll have to pay more when you file a claim, a higher-deductible policy can save you on your annual rate.

Compare insurance quotes: There are many different homeowners insurance providers, so it may be helpful to shop around to find the best price.

Try an independent agent: You don’t have to work with an insurance company directly. Some independent agents are licensed insurance professionals who can offer you a good deal.

Get the right coverage: Educate yourself about what coverages you need and which you don’t. Some people may pay for coverage they won’t need to use.

Check for discounts: There are a variety of discounts you could get in addition to bundling your policies. Your provider may offer a loyalty discount, an alarm system discount, or a claims-free discount.

Methodology

The primary source of this data comes from Bankrate. To conduct their analysis, Bankrate uses the data provided by Quadrant Information Services. The data comes from various insurance providers across all 50 states as well as Washington, D.C., for 2023.

The average rates use the following base insurance profile:

Homeowner: Male, 40 years of age

Dwelling coverage: $250,000

Personal property coverage: $125,000

Liability coverage: $300,000

Loss of use coverage: $50,000

Medical payments coverage: $1,000

Repair Your Credit Before Getting Homeowners Insurance

Depending on your state, your credit score may play a significant role in your homeowners insurance rates. By improving your credit score, not only can you potentially save on your home insurance rates, but your credit score can also help you when purchasing or refinancing your home.

Credit.com offers a free credit report card that provides you with an analysis of your credit health. You can also utilize our ExtraCredit® subscription for additional credit reporting and other services.

Trusted, up-to-date local Detroit and Michigan-wide breaking news.

Accurate, fact-based journalism without an agenda, so you get the information you need to make informed decisions.

Complete coverage and commentary on Michigan politics from Chad Livengood, Beth LeBlanc and Craig Mauger.

Sports coverage for locals, by locals: led by journalists Bob Wojnowski, John Niyo, Angelique Chengelis and Matt Charboneau.

Columns that cover the things that matter to our community, from reporters Daniel Howes, Nolan Finley, Maureen Feighan and Bankole Thompson.

Newsletters on the topics that interest you most, like the Detroit Dinner Bell, Red Wings Report, Auto Insider and so many more, are delivered in your inbox each morning.