Home prices continued to accelerate in August, rising a seasonally adjusted 0.68% from July and hitting another record high for the fourth consecutive month.

Prices in nearly half of the nation’s 50 largest markets climbed by 0.75% or more. Even on a non-adjusted basis, August’s gain of 0.24% was more than 60% larger than the 25-year average for the month, according to a mortgage monitor report from Intercontinental Exchange, Inc. (ICE).

“Either way you look at it, the increase was sufficient to push annual appreciation up to a stronger-than-expected 3.8%. This marks three months of clear acceleration in the rate of growth at the national level, with annual HPA up from 2.4% in July and just 0.25% back in May,” said ICE’s Vice President of Enterprise Research Andy Walden.

While home affordability recently hit a 38-year low due to spiking rates and home prices, Walden noted that it might yet get worse.

If adjusted home prices were to freeze where they are now, it would result in annual home price appreciation rising above 5% by the end of this year given the strong price increases seen earlier in 2023.

“On the other hand, if the 0.64% per month seasonally adjusted price increases we’ve seen on average in 2023 were to continue, we’d be looking at nearly 8% year-over-year growth by December,” Walden noted.

The high-interest rate environment continues to put downward pressure on mortgage origination activity.

Purchase loans comprised about 82% of overall mortgage lending in 2023 and ICE forecasts purchase lending to continue to dominate the market through next year.

There is modest opportunity in the refinance market although it is defying traditional analysis, according to ICE’s mortgage monitor report.

The profile of cash-out borrowers – who made up roughly 90% of all Q2 refinances – has shifted considerably in recent quarters.

While the average unpaid principal balance of borrowers entering a refinance has fallen from $319K in early 2020 to $183K in August 2023, it is even lower ($165K) among cash-outs specifically.

Alongside rising interest rates, the average equity withdrawal among cash-out refinances has also risen by nearly 90% from its low in 2020.

Today’s candidates are far more focused on tapping equity, and cash-outs may make sense for borrowers with lower balances looking to withdraw large amounts of equity at lower interest rates than what is available via a HELOC, ICE noted.

“With nine of 10 August 2023 refinances involving the borrower raising their interest rate – with an average rate increase of 2.34 percentage points – simple ‘in the money’ analytics are missing this market almost entirely. Granular insight into the before-and-after-refinance picture is key to understanding who is transacting in today’s rate environment – and more importantly, why, ” Walden said.

The average cash-out credit score of 715 is down more than 40 points in less than three years and is among the lowest in the post-Great Financial Crisis era.

Higher credit borrowers who can qualify in today’s market are more likely opting for HELOCs as a way of tapping equity, leaving a lower credit score residual among cash-out refis.

It’s with no great pleasure (none of any kind, for that matter) that we find ourselves in a position to report, yet again, that mortgage rates have sailed decisively to another new multi-decade high. Today’s installment is fairly unpleasant given that the average lender actually began the day in slightly stronger territory only to be forced to increase rates at least once over the course of the day.

As is the case any time rates start lower and are revised higher, the culprit is the underlying bond market. Specifically, bonds started the day in stronger territory but ended up weakening significantly between 10am and 2pm ET.

Underlying reasons for that weakness are a matter of debate and confusion. Some point to comments from Fed speakers or a delayed reaction to economic data, but there are good reasons to be skeptical of both explanations. One of the only things that can’t be disproven right now is the sense that the entire bond market has acquiesced to the notion of interest rates being “higher for longer” and simply can’t reach the “higher” destination all in one go.

In other words, the market believes the Fed and it sees the value in being cautious ahead of next week’s important economic data. Traders have apparently decided it’s less painful to err on the side of higher rates and be forced to buy more bonds in the future (buying = lower rates, all other things being equal) than to be caught on the wrong side of the “higher for longer” trade yet again.

Today’s mortgage rate adjustment is more painful than normal due to a phenomenon in the mortgage-backed securities market. It’s fairly complicated to understand, but this part is simple: if the bond market were to improve in the future by the same amount it deteriorated today, rates would be back in line with yesterday’s levels.

Today’s levels aren’t great. The average lender moved up from 7.50% yesterday to 7.65% by this afternoon. That’s for a top tier 30yr fixed scenario. Anyone with a less-than-perfect scenario is seeing even higher rates–many of then closer to 8.0%.

A new report released this week revealed that the majority of loan originators make $100,000 or more annually.

This was one of the major takeaways from Mortgage Daily’s 2012 Loan Originator Survey, which included 175 originators (120 who completed ALL questions).

Per the survey, nearly 60% of respondents indicated that they made at least $100,000, which is about double the median household income in the United States.

Additionally, many noted that they would have made even more if it weren’t for the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010.

However, a small share said they profited from the new requirements, perhaps because of fewer competitors in the space.

The biggest complaint from originators had to do with appraisal requirements, and the fact that many appraisals are coming in low these days (sign of the times).

Most of those surveyed do not work for banks, and more than a quarter are self-employed, meaning many could be mortgage brokers.

A study back in 2011 found that mortgage brokers generated average revenue of 2.25 mortgage points per loan, before the new compensation rules took effect, and predicted that number wouldn’t change.

On a $200,000 loan, we’re talking $4,500, less expense. So for the broker originating numerous loans monthly, you can see how it all adds up.

This figure probably used to be a lot higher during the boom, back when loan officers and brokers could get paid excessive amounts by both the lender and the borrower, not just one.

Is the Survey Skewed?

While this survey gives us a little insight into how much some originators are making these days, the number of participants is a bit limited.

Additionally, you have to wonder how many of the low-producing originators chose to take part in the questionnaire.

Those who aren’t having a banner year might not be keen on filling out a survey.

And salaries are always going to display an enormous range in the real estate business, mainly because there are those who work part-time, those who just entered the fray, and those who have been in business for decades that are well connected.

Just look at real estate agents, excuse me, Realtors, who made a median $34,100 in 2010.

The median salary for those in business for two years or less was just $8,900, while it was $47,100 for those in business 16 years or more, per NAR.

And 16% earned a six-figure income, revealing the major disparity among agents.

Fifth Third Providing Employment Solutions to Unemployed Mortgage Borrowers

Here’s a little something related, as it has to do with employment. Fifth Third Bank said it partnered with NextJob, a “nationwide reemployment solutions company,” to find jobs for its unemployed mortgage borrowers.

The program, which was piloted in 2012, targets bank customers who are at serious risk of default on their mortgages.

Of those who took part so far, 40% were fully employed after six months, making the program a novel way for both the bank and borrowers to avoid foreclosure.

NextJob helps borrowers create an effective resume and cover letter, carry out a targeted job search, and train and prepare for interviews.

Perhaps banks and lenders should consider hiring these at-risk borrowers in their own lending departments, seeing that they’re all having capacity constraints.

That could solve two problems in one, and by the sound of it, the compensation ain’t too shabby. But in all seriousness, if you’re a Fifth Third mortgage customer in need of assistance, check it out.

Pending home sales failed to add a third month onto the mini rally it staged in June and July. The National Association of Realtors® (NAR) said its Pending Home Sale Index (PHSI) declined 7.1 percent to 71.8 in August and is now down 18.7 percent from its August 2022 level.

The PHSI ended a three-month decline in June, rising 0.3 percent followed by a 0.9 percent increase in July.

The PHSI is based on contracts signed during the month to purchase existing single-family houses, condos, and cooperative apartments. It is a leading indicator of those sales which are expected to close over the following 30 to 60 days. NAR will report September’s existing sales on October 19.

“Mortgage rates have been rising above 7 percent since August, which has diminished the pool of home buyers,” said Lawrence Yun, NAR chief economist. “Some would-be home buyers are taking a pause and readjusting their expectations about the location and type of home to better fit their budgets.”

“It’s clear that increased housing inventory and better interest rates are essential to revive the housing market,” added Yun.

The index in all four of the nation’s major regions declined compared to both July and to the prior August. The Northeast PHSI was down 0.9 percent to 62.6 and was 18.2 percent lower on an annual basis. The index for the Midwest lost 7.0 percent and 19.1 percent compared to the two earlier periods to a reading of 71.3.

Pending sales in the South fell 9.1 percent to 86.5 in August, coming in 17.6 percent lower year-over-year. The West’s PHSI declined 7.7 percent to 56.3 and was 21.4 percent behind its August 2022 reading.

Yun concluded, “The Federal Reserve must consider the sharply decelerating rent growth in its consideration of future monetary policy. There is no need to raise interest rates. Moreover, the government shutdown will disrupt some home sales in the short run due to the lack of flood insurance or delays in government-backed mortgage issuance.”

The PHSI was benchmarked at 100 in 2001, a number equal to the average level of contract activity during that year.

Effective immediately, Indymac has halted all retail and wholesale forward loan production, according to a letter sent to shareholders on behalf of CEO Mike Perry, posted on the company’s blog.

Indymac will continue to process and ultimately fund locked loan applications, but will no longer accept rate locks or new loan submissions in forward mortgage lending channels, aside from its servicing retention channel.

As a result, Indymac plans to cut 3,800 jobs over the next couple months, with most sticking around in the company’s servicing department or reverse mortgage unit Freedom Financial.

Employees who have been with the company for five or more years will receive a minimum $20,000 severance pay package, which seems generous given the severity of the ongoing mortgage crisis.

However, most employees will receive just 30-days severance, as the company was forced to eliminate a program that provided one month of pay and one month of paid insurance coverage for each year of service with the company.

Perry explained that the struggling mortgage lender had been in need of some serious capital, but wasn’t able to raise it through traditional means, and chose not to pursue a firesale of assets, which could have depleted capital further.

Additionally, he noted that federal bank regulators have informed Indymac that it is no longer “well capitalized,” and as a result, is no longer permitted to accept new brokered deposits or renew existing ones unless it receives a waiver from the FDIC, which is currently pending.

That left the Pasadena, CA-based mortgage lender with little choice but to halt nearly all lending activity, which was a drain on the company’s balance sheet.

Going forward, the company will focus on reverse mortgage lending and loan servicing/retention efforts, which could generate roughly $5 billion to $10 billion of new GSE/FHA loans per year.

Perry expects Indymac to report a larger second quarter loss than the $184.2 million loss experienced in the first quarter of 2008, though he couldn’t provide an estimate given the number of uncertainties surrounding the company at the moment.

He has also made a request to Indymac’s Board of Directors that his base salary be reduced by 50 percent as a result of today’s news.

Shares of Indymac slid 21 cents, or 29.58%, to 50 cents in after hours trading.

Bonds Almost Hold Onto Gains Ahead of Shutdown Uncertainty

By:

Matthew Graham

Fri, Sep 29 2023, 3:51 PM

Bonds Almost Hold Onto Gains Ahead of Shutdown Uncertainty

Bonds improved moderately overnight, adding onto what was already a fairly substantial recovery yesterday. The morning’s PCE data was slightly lower than expected, but bonds didn’t seem unequivocally happy about that. There was a modest extension of the rally and then a slow give-back into the PM hours. Trading was very flat near unchanged levels after noon ET. Month/Quarter-end tradeflows are assumed to be underpinning some of the volatility of the past 3 days, as is the uncertainty surrounding the government shutdown. The most direct implication for bonds is that they must navigate the most important data week of the month without the most important data (no jobs report or JOLTS next week due to the shutdown).

Core PCE m/m

0.1 vs 0.2 f’cast, 0.2 prev

Core PCE y/y

3.9 vs 3.9 f’cast, 4.3 prev

08:46 AM

Moderately stronger overnight with some additional improvement after data. 10yr down 5+bps at 4.524. MBS up just over a quarter point.

11:11 AM

Giving up some gains. MBS off a quarter point from highs, but still up nearly an eighth on the day. 10yr still down 4bps on the day but up 3bps from lows.

03:13 PM

Weakest levels of the day for 10s, up 1bp at 4.588. Weakest liquid levels for MBS, down an eighth of a point in 6.0 coupons.

Download our mobile app to get alerts for MBS Commentary and streaming MBS and Treasury prices.

This statement from the Fed is classic Fed at work.

The Fed has not helped its own cause here, as Austan Goolsbee, president and CEO of the Federal Reserve Bank of Chicago, said in a speech last week: “I’m still trying to process why long-end interest rates are increasing.”

My answer: “Stop talking about raising rate at this stage with a hawkish outlook!”

The Fed has expressed that real yields, meaning where inflation is currently and where rates are, are restrictive to the economy, so sounding hawkish on monetary policy at this stage can lead the bond market to go higher more than the Fed would like. Land the plane, folks, land the plane!

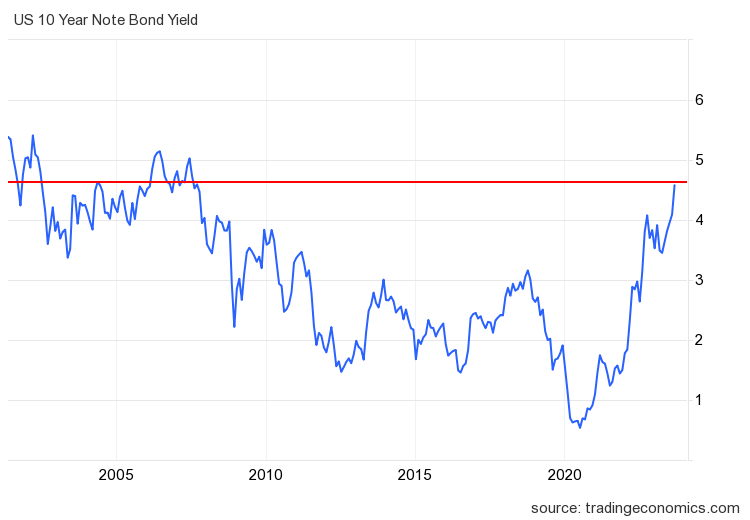

As you can see in the chart below, it was another wild week in the bond market. Mortgage rates went from 7.39% to a high of 7.65% and ended the week at 7.44%. Before last week the high for mortgage rates this year was 7.49%.

The bond market has been volatile, but after the 10-year yield broke the 4.34% level, I am watching for the 4.63% level. A close above that and follow-through bond market selling could lead to higher mortgage rates. Hopefully, the last two weeks caught the Fed’s attention. If they cared about a soft landing, which I have been skeptical about from the start, as I talked about here on CNBC, the Fed would be more mindful of what they say and do.

Weekly housing inventory data

One of the things I got wrong this year is that I believed if mortgage rates stayed higher for longer, active inventory would grow between 11,000 and 17,000 for at least some of the weeks; that hasn’t happened recently with higher rates — close but no cigar. T

Last week, the growth of active listings slowed to 6,808. Seasonality is kicking in now, but we should be able to continue growing housing inventory like we did last year, as higher rates slow sales down, keeping homes on the market longer.

Last year, the seasonal peak was Oct. 28. Last week, according to Altos Research:

Weekly inventory change (Sept.22-29): Inventory rose from 527,938 to 534,746

Same week last year (Sept. 23-30): Inventory rose from 556,865 to 561,229

The inventory bottom for 2022 was 240,194

The inventory peak for 2023 so far is 534,746

For context, active listings for this week in 2015 were 1,187,2000

After some volatile weeks with the new listings data, things look similar to earlier in the year when we had an orderly seasonal decline in new listings data, which has been trending at the lowest levels ever for over 13 months. Even with rates spiking, the new listing data hasn’t created another new leg lower. This is important, as I expect flat to slightly positive data soon due to a shallow bar.

Historically, one-third of all homes have price cuts every year. Last week’s price cuts were lower than last year at the same time by 4%. This is happening even with rates over 7% and part of the reason is that housing inventory has been negative year over year since mid-June. As mortgage rates move higher, the percentage of price cuts can grow but it’s trailing last year’s percentage as home sales aren’t crashing like they did last year.

Price cuts for last week over the years:

2021: 29%

2022: 42%

2023: 38%

Purchase application data

Purchase application data was 2% lower last week versus the previous week, making the year-to-date count 17 positive prints, 19 negative prints, and one flat week. If we start from Nov. 9, 2022, it’s been 24 positive prints versus 19 negative prints and one flat week. The week-to-week data has gotten softer since mortgage rates have been trending above 7%. However, it’s not crashing like last year because we are working from a lower bar.

The week ahead: It’s jobs week! (If the government is open)

If we don’t have a government shutdown, the week ahead will be jobs week again! The Fed was happy about labor data last month as job openings have been falling, and the job growth data is cooling down. However, jobless claims are still going strong, so they have more work to do in attacking the labor supply. In addition to jobless claims, this week we will also have job openings, the ADP jobs report, and the BLS Jobs Friday report, which could move the bond market this week.

Also, I will watch this week to see if more Fed members comment about rising long-term rates. The Fed would like to keep rates higher for longer, but if the bond market gets a whiff of any terrible recession data, it will take yields down. So far, jobless claims data hasn’t given them any reason to do so.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

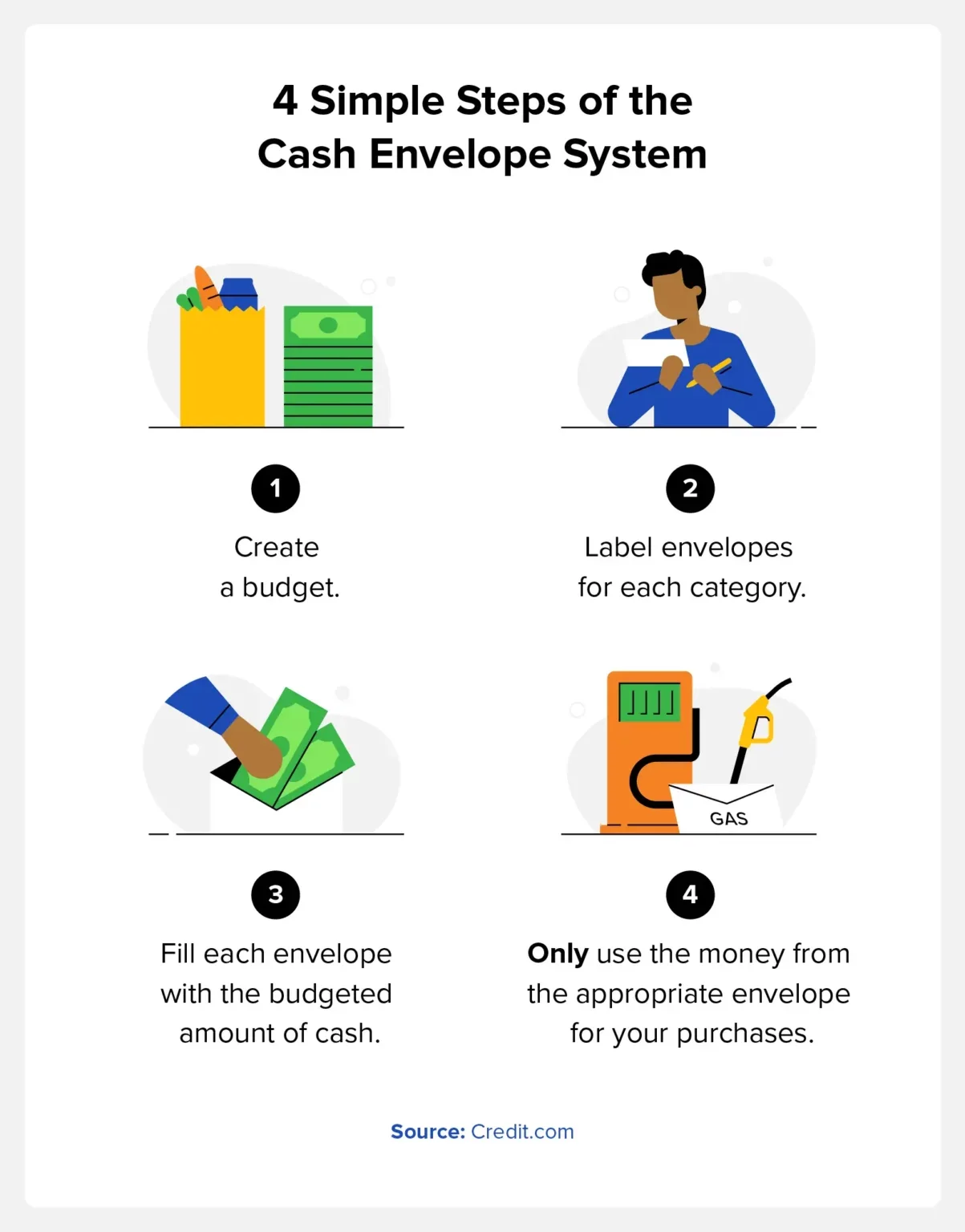

The cash envelope system is a budgeting tool that helps you develop self-discipline by only spending the allotted amount of cash from labeled envelopes each month. It can help reduce overspending and impulsive purchases.

Budgeting is one of the best ways to keep track of your spending, pay down debt, and build wealth. Unfortunately, many Americans don’t take advantage of preparing a monthly budget. Our team at Credit.com surveyed over 1,000 Americans, and 27 percent said they don’t think a budget is necessary.

We also found that 15 percent of people don’t want to feel restricted by a budget, and 24 percent simply don’t think they will stick to it. Fortunately, with the cash envelope system, it’s easy to do both.

Today, you will learn about this simple budgeting method that can help you save money, lower your debt, and potentially help raise your credit score.

Key takeaways:

You can use cash envelopes as a monthly budget by putting cash in different envelopes for spending categories.

The system is ideal for people who have a habit of impulsive spending or overspending.

It allows you to monitor your money rather than guessing how much you’re spending.

The cash envelope system is often called “cash stuffing” on social media apps like TikTok.

What Is the Cash Envelope System?

The cash envelope system, also known as “cash stuffing,” is an easy-to-use budgeting tool that helps track how much money you have to spend. You’ll put the cash in labeled envelopes and check each envelope throughout the budgeting period to see how much money you have left to spend.

Different budgeting systems work for different people. For some, having a monthly budget template on their computer is the best option. Others may benefit more from being able to physically see how much money they have left for purchases like groceries, gas, and entertainment.

How the Cash Envelope System Works

Before cash stuffing, you will need to organize your money envelopes into different categories. If it helps, you can start with a spreadsheet budget template, or you can write down the categories in a notebook. Some of the top budget categories to consider include:

Utilities

Fuel or transportation costs

Groceries

Healthcare and medications

Savings

Debt

It’s also beneficial to ensure you have cash envelopes for areas where you typically overspend. This may be eating out, buying clothes, or online shopping. You can allocate money toward these areas, but the goal is to ensure you don’t overspend.

During the month, whenever you spend money in one of these categories, you only use the money from the appropriate envelope. For example, if you enjoy buying a $5 cup of coffee on your way to work and allocate $100 to that envelope, take $5 out of it each morning.

The cash envelope system is a way to hold yourself accountable for your spending. This means that once the money is gone from an envelope, it’s gone. If you miscalculated how much you need in a certain category, revisit your budget the following month and tweak the amounts.

You can refill your envelopes at the start of each budgeting period or after each paycheck.

The Benefits of the Cash Envelope System

There are pros and cons that come along with every budgeting strategy, so it’s helpful to know the benefits and drawbacks and find the one that’s right for you. The cash-stuffing envelope system is great for people who don’t check their bank account daily or are better with their money when using cash.

Additional benefits include:

Avoiding overdraft fees

Minimizing overspending

Increasing accountability

Helping with disciplined spending

By sticking to cash, the system also helps reduce the frequency with which you use your credit card, minimizing interest fees.

The Downsides of the Cash Envelope System

The cash envelope system isn’t for everyone, and it may create some additional challenges. The primary downside of this budgeting system is that you need to go to your bank or an ATM whenever you need to refill your envelopes. It’s also beneficial to consider that carrying large amounts of cash has the risk of losing it for the money being stolen.

Some of the other downsides include:

It’s time-consuming.

You get no credit card rewards.

You can only spend the amount contained within each envelope.

The other challenge with the cash envelope system is making online payments or automatic payments. Automatic payments are a great way to avoid forgetting about a payment and accruing late fees. You can still use the cash envelope system, but you will need to keep track by writing on the back of the envelope, similar to balancing a checkbook.

Should You Use the Cash Envelope System?

This budgeting system is ideal for people who are quick to pull out their debit or credit card and have trouble with overspending. It can be difficult to track your money electronically, but using physical cash can help many people stick with a budget.

The system is also a great way to budget for beginners. It’s a simple system, and you can start with just a few categories. If you know you have a problem with overspending on ordering food or going out, use this system to allocate a specific amount of cash for these activities.

FAQ

Although the cash stuffing system is a simple method, there are some common questions people have when getting started.

Can the Cash Envelope System Work If You Make Online Payments?

The most common method is to create a physical envelope while keeping the money in your bank account for online payments. You can keep track by writing on the back of the envelope each month.

What If an Envelope Runs Out of Cash?

If you run out of cash from the envelope, stay disciplined and avoid borrowing money from other envelopes. Revisit your budget and find ways to save in different categories, earn extra money, or reduce your spending.

How Do You Use the System When Emergency Expenses Happen?

Emergencies happen, and in these cases, you can shift money around from your envelopes and budget accordingly the following month. It’s also helpful to build an emergency fund for these situations, and you can also keep a credit card for emergency funds.

What Do You Do If There’s Money Left Over in Your Cash Envelope?

Money left over in cash envelopes means you’re doing a great job with your budget. You can use this to treat yourself or add to your personal spending money envelope the next month. You may also want to use this extra money to make extra debt payments or put it in your savings account.

How the Cash Envelope Budget System Can Help Improve Your Credit

Creating a budget is a great way to get your finances under control and create quality spending habits. The cash envelope system is also helpful for reducing your debt and improving your credit. One of the key factors of your credit score is credit utilization, so allocating an envelope toward paying down your debt and using leftover money for additional payments can help increase your score.

For additional credit resources, you can sign up for Credit.com’s free credit report card or our ExtraCredit service.

As home affordability decreased, sellers reduced asking prices more frequentlythis September, with the pace coming in above typical seasonal patterns.

Approximately 6.5% of homes on the market saw asking prices reduced during the four-week period ending Sept. 27, according to new research from Redfin. The rate corresponds to approximately one in 15 properties on the market and represents an increase from 5.8% a month earlier. That is a sharp rise from what has been reported in past years over the same time frame, the real estate brokerage said.

The uptick in price cuts comes as low inventory and rising interest rates take a bite out of affordability, according to several recent reports. Conditions contributing to the current state of the market appear set to continue leaving their mark on affordability over the next several months, leading analysts said at this week’s Digital Mortgage conference in Las Vegas.

Redfin found the median sales price rose 3.1% year-over-year, coming in at $372,500, even with “relatively low” demand. A recent rise in the volume of new listings, also atypical for the time of year, is giving home shoppers more leverage.

“Buyers are using things like inspection negotiations and high insurance premiums to back out of deals,” said Heather Kruayai, a Redfin agent in Jacksonville, Florida, in a press release. “They’re holding a lot of the cards; today’s sellers need to concede on some details to close the deal.”

The latest affordability data from the Mortgage Bankers Association offers few signs of improvement for aspiring homeowners. In its monthly purchase-applications payment index released this week, the trade group reported the average monthly amount applied for by new home buyers increasing by a fraction to $2,170 in August, from $2,162 in both June and July. The current figure is higher by 18% compared to the mean level of a year ago — $1,839.

“Prospective homebuyers’ budgets continue to be impacted by the combination of high home prices and mortgage rates that remain higher than 7%,” said Edward Seiler, MBA’s associate vice president, housing economics, and executive director, Research Institute for Housing America.

The latest PAPI report does not factor in September’s surge in mortgage rates, with the 30-year conforming average landing at 7.41% at the end of last week among MBA members — the highest point since late 2000. Similarly, Freddie Mac reported a consistent rise in the 30-year rate throughout September after a pullback in August.

Within individual segments, borrowers of Federal Housing Administration-backed mortgages saw their average payment hit a record of $1,901, jumping 2.5% from $1,854 in July and 29.4% from $1,469 in August 2022.

But even with the overall PAPI increase, conventional-loan borrowers saw a fall in the mean to $2,187 from $2,197 between July and August. But the number was still well above $1,901 a year ago.

The MBA’s national payments index for new purchase applications inched up 0.4% to a reading of 175.4 in August compared to 174.7 a month earlier. An increase in the number reflects declining affordability. Strong income earnings of over 4% over the past 12 months helped offset the steep climb upward in payment amounts.

The states showing the smallest degree of affordability were concentrated in the Western U.S., according to the MBA. Idaho led the country with a PAPI score of 269.6, followed by Nevada and Arizona at 265.7 and 238.6.

Inside: Are you looking for an affordable budgeting app that offers a range of features? YNAB may be the perfect choice for you! This guide will compare YNAB vs Mint, highlight their key features, and help you decide which is best for your needs.

Are you trying to make a choice between Mint and YNAB for managing your financials?

Here’s a comprehensive overview that would definitely point you in the right direction.

Both Mint and YNAB have proven to be efficient and reliable online budgeting tools, but their offering varies in some aspects.

While Mint shines with its free budgeting tools and comprehensive credit score and report management capabilities, YNAB stands distinguished with its robust features and specialist credit management options, making it worth its fee for some users.

Herein, we dive into the similarities, differences, and unique functionalities of both platforms to help you decide which one best aligns with your financial management needs and lifestyle.

As a finance expert, I’ve seen both YNAB and Mint apps work wonders for different people.

In my opinion, both have unique value. Novices may find Mint’s overview helpful, while more determined budgeters might prefer YNAB.

Remember, it’s perfectly fine to use both if it aids your long-term money management.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What is YNAB?

YNAB is a budgeting software I’ve utilized that provides detailed financial tracking and education for effective money management. Also, known as you need a budget app.

Adhering to its unique Four Simple Rules for Successful Budgeting, every dollar is assigned a specific task. YNAB operates via an online account or a mobile app, involving color codes and features like ‘The Inspector’ for efficient budget overview. However, it’s important to note that YNAB caters only to the zero budgeting style and charges a monthly subscription fee.

This is a great budgeting method as it gives you a cash flow budget plan for your money.

Overall, YNAB helped me gain control over my finances by setting realistic goals, getting one month ahead on bills, and focusing on each dollar’s purpose.

What is Mint?

Mint is a free, all-in-one finance platform owned by Intuit that can be used to easily manage my money.

It links all accounts in one place for easy tracking and includes features such as budgeting, credit score monitoring, and bill tracking.

For instance, Mint categorizes transactions, monitors changes in my credit score, and sets up budgetary limits.

With over 30 million users, Mint is a leading free tool in personal finance management.

A step up from Mint would be Intuit’s Quicken platform or Simplifi budget app.

Comparison of YNAB and Mint Apps

Mint is a comprehensive, free budgeting app, that provides an overall view of your finances. It links to your accounts, tracking and categorizing spending, while also offering savings tips. Conversely, YNAB, a paid app, focuses on giving users control over budgeting. It will link to your accounts and encourage a proactive role in handling finances.

These are two of the budget apps available on the market.

In my opinion, if you’re seeking an easy-to-use app offering a holistic view of your spending and savings, Mint is a perfect choice. However, if you’re looking for a stringent budget management system with more control, YNAB is worth the investment.

Kristy @ Money BLiss

1. YNAB vs Mint: Features

YNAB and Mint are both renowned budgeting apps, but they possess some notable differences.

While both support account linking, goal setting, and spending tracking, Mint pulls ahead with its investment and credit score tracking features.

YNAB distinguishes itself with a forward-thinking, zero-based budgeting strategy and benefits like manually adding transactions. Think budget by paycheck style.

From the ease of use standpoint, both are equally user-friendly.

2. YNAB vs Mint: Budgeting Snapshot

YNAB offers a rigorous, manually updated budgeting snapshot that employs a zero-based budgeting philosophy. This feature provides a detailed outlook, encouraging users to assign every dollar a job.

On the other hand, Mint has an automated tracking system that offers an all-in-one snapshot of all financial accounts and spending categories.

Mint integrates your accounts, offering useful tips and an overview of your finances. Conversely, YNAB requires a manual categorization of income and expenses but affords more budgeting control. Similar to using the ideal household budget percentages.

The budgeting snapshot in Mint is best suitable for individuals seeking a hands-off approach, while YNAB is ideal for those who prefer an in-depth, hands-on budget strategy.

A great way to move digital from your budget binder with envelopes.

3. YNAB vs Mint: Goal Setting

The Goal Tracking feature in YNAB allows users to set various budgeting goals such as saving targeted amounts of money or conversely working towards getting out of credit card debt. This in-built functionality provides a structured pathway for users to stick to and pursue their financial objectives effectively.

Your interaction with your YNAB account through the goal-tracking tool ties back to YNAB’s four Simple Rules for Successful Budgeting, aiding in fiscal responsibility.

This innovative feature assists individuals in staying focused on their planned budgets, ensuring they are empowered to make strides toward their unique financial goals.

Mint however doesn’t offer this feature.

4. YNAB vs Mint: Interface

While YNAB is ideal for meticulous budgeters prioritizing forward planning, Mint is perfect for those seeking an easy-to-use, comprehensive glimpse of their financial standing.

YNAB’s interface is focused on budgeting, featuring tools for expense tracking, goal setting, and manual transaction input.

In contrast, Mint offers a comprehensive overview of your financial health, automatically categorizing expenses, tracking investments, and offering set-up alerts.

5. YNAB vs Mint: Categorization

Mint offers automated categorization of transactions, which eases the process of budgeting for the user. However, it doesn’t allow the removal of default categories, and the addition of new ones might take time due to server communication.

On the other hand, YNAB allows a deeper level of categorization, with an option to visually nest categories, and more effortless editing of these categories.

In my opinion, Mint’s categorization feature suits a casual budgeter looking for automation, while YNAB would be ideal for those desiring granular control over their personal budget categories.

6. YNAB vs Mint: Mobile App & Cross Platforms

Both YNAB and Mint offer comprehensive personal finance management via mobile apps, compatible with iOS, Android, and desktops.

YNAB stands out with its Apple Watch integrations and a slightly better syncing experience based on user reviews on Trustpilot1.

YNAB also syncs across a desktop app as well.

7. YNAB vs Mint: Alerts

Mint provides a wide selection of alerts, including low balances, upcoming bill payments, over-budget warnings, ATM fees, and unusual expenditure notifications.

These comprehensive alerts from Mint give a more thorough financial pulse check but can be overwhelming for some.

On the other hand, YNAB recently added live push notifications based on your preferences.

8. YNAB vs Mint: Syncing

YNAB leads the game when it comes to synchronization, outshining Mint. While Mint supports numerous banks, issues with synchronization often lead to grievances among its users. YNAB, on the other hand, offers smoother syncing and fewer complaints, proving its superiority.

Many users find YNAB’s syncing consistent and reliable.

Personally, I believe that if you prioritize seamless syncing and don’t mind spending $14.99 a month, YNAB becomes a clear choice.

However, if you’re okay with potential sync issues and prefer free usage, Mint could be more suitable.

It’s crucial to pick according to your priorities and needs.

9. YNAB vs Mint: Savings Accounts

Mint offers automatic expenditure tracking and classifies my spending into categories, providing a comprehensive view of where my money is going.

YNAB, on the other hand, empowers me to manually budget my net income each month, ensuring I don’t overspend and promoting a proactive approach to saving.

10. YNAB vs Mint: Investment Tracker

Mint offers investment tracking features, allowing users to view their investment portfolio and monitor performance.

In contrast, YNAB lacks this feature, not providing any investment tracking at all.

As a user, if you highly prioritize tracking investments in one place, you may lean towards using Mint. Conversely, if investment tracking is less important to you than budgeting, YNAB’s strong budgeting emphasis, despite its lack of investment tracking, makes it a considerable option.

11. YNAB vs Mint: Learning Curve with your Finances

YNAB has a steeper learning curve, necessitating a proactive approach to money management by assigning every dollar a purpose. Thus, YNAB gives you a free 34-day free trial to understand how to use the app.

Mint, however, requires minimal user input post-account linkage and auto-categorizes your spending. For sheer ease of use, Mint might appeal to novices looking for automated budget tracking.

On the other hand, users wishing to take charge of their finances might appreciate YNAB’s proactive, behavior-altering approach. Despite having a steeper learning curve, YNAB offers an abundance of online tutorials and customer support, making the learning process manageable and rewarding.

The same is true when you are learning to use the biweekly budget template.

12. YNAB vs. Mint: Data Security

Data security is a paramount concern when utilizing online budgeting apps as they deal with sensitive financial information.

Apps like YNAB and Mint incorporate stringent security measures to protect user data.

For instance, YNAB uses a one-way salted and hashed password system and data encryption.

Mint, on the other hand, employs two-factor authentication and a Touch ID sensor for iOS for enhanced security.

Nonetheless, it’s important to note that while these apps provide bank-level security, Mint does anonymize and sell user data to advertisers.

13. YNAB vs Mint: Advertising

YNAB derives income primarily from subscription fees offering an ad-free experience, holding a straightforward revenue model. In contrast, Mint generates income through affiliate commissions by advertising financial products to users and selling anonymized user data!

Mint, contrastingly, is a free app reliant on ads and sells anonymized user data for third-party advertisements.

From my perspective, if avoiding ads and preserving data privacy matters to you, YNAB’s approach might be more appealing. However, if you prefer a free service and don’t mind the ads, Mint would be suitable.

14. YNAB vs Mint: Customer Support

When evaluating the customer support of Mint and YNAB, it’s evident that YNAB takes a more well-rounded approach.

With a commitment to respond to email queries within 24 hours, YNAB also provides educational resources such as the “get started” class, their blog, and user forums. This is in contrast to Mint, which, despite offering live chat support, has had reports of slow response times.

Both platforms offer online training materials, but YNAB seems more comprehensive and responsive in its support-providing role. Overall, YNAB appears to be the preferred choice when customer support is a primary consideration.

15. YNAB vs Mint: Cost

Mint is a free, ad-supported budgeting app while YNAB is a subscription-based model of $14.99 monthly or $99 annually.

However, for individuals seeking in-depth surgical budgeting capabilities without concerns for associated costs, YNAB’s price might represent a great investment.

Given the claimed average user saves $600 in two months and $6,000 in the first year.2

For those budgeting with minimal funds, the free price tag of Mint might be more attractive, but you are giving away your privacy.

Pros and Cons of YNAB vs Mint

Our Favorite

Key Features:

YNAB offers a comprehensive approach to budgeting, helping you plan monthly budgets based on your income. It also offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

YNAB’s superior synchronization skills make it the winner in this area. YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners

YNAB provides an option to manually add and upload transactions from accounts each month, a feature that Mint does not offer.

YNAB prioritizes user privacy, requires an opt-in to access budgeting data, and doesn’t sell user data.

Key Features:

Mint offers a centralized platform for monitoring all your financial accounts, including credit cards and bank accounts.

It provides a complete financial overview at a glance through the auto-population of data from linked accounts.

Mint’s features include detailed reporting in multiple categories, free credit score access, and exceptional compatibility with financial institutions.

The service is free, funded by ads and offers, and it best serves those who wish to categorize spending, budget their monthly expenses, and access all financial details from one place.

Lack of investment tracking feature

Customer service is only accessible via email, which might not be ideal for urgent queries

Steep learning curve which requires time and effort to navigate through.

Mint, which belongs to Intuit, automatically accesses all data and sells the data. Thus, an intrusion of privacy.

Budgeting feature doesn’t enable effective planning of future expenses.

Mint suffers from more technical glitches and synchronization issues.

Ads included in the free version of Mint can be obtrusive and may deter users.

$14.99 monthly or $99 annually

Free to Use, But Served Ads and They Sell your Data.

Offers a 100% money-back guarantee at any point of use.

Does not require credit card information to signup, a departure from the usual free trial model)

Our Favorite

Key Features:

YNAB offers a comprehensive approach to budgeting, helping you plan monthly budgets based on your income. It also offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

YNAB’s superior synchronization skills make it the winner in this area. YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners

YNAB provides an option to manually add and upload transactions from accounts each month, a feature that Mint does not offer.

YNAB prioritizes user privacy, requires an opt-in to access budgeting data, and doesn’t sell user data.

Lack of investment tracking feature

Customer service is only accessible via email, which might not be ideal for urgent queries

Steep learning curve which requires time and effort to navigate through.

$14.99 monthly or $99 annually

Offers a 100% money-back guarantee at any point of use.

Does not require credit card information to signup, a departure from the usual free trial model)

Key Features:

Mint offers a centralized platform for monitoring all your financial accounts, including credit cards and bank accounts.

It provides a complete financial overview at a glance through the auto-population of data from linked accounts.

Mint’s features include detailed reporting in multiple categories, free credit score access, and exceptional compatibility with financial institutions.

The service is free, funded by ads and offers, and it best serves those who wish to categorize spending, budget their monthly expenses, and access all financial details from one place.

Mint, which belongs to Intuit, automatically accesses all data and sells the data. Thus, an intrusion of privacy.

Budgeting feature doesn’t enable effective planning of future expenses.

Mint suffers from more technical glitches and synchronization issues.

Ads included in the free version of Mint can be obtrusive and may deter users.

Free to Use, But Served Ads and They Sell your Data.

Who should use YNAB?

From my experience, YNAB works best for those who are ready to seriously manage their money and spend some time learning a new budgeting approach. Its use of the zero-based budgeting system not only makes you more intentional with your money but also demands active participation in decision-making.

YNAB’s ability to link to your accounts and its multitude of educational resources available are admirable features I’ve used.

YNAB offers detailed financial tracking and built-in education, but its monthly subscription fee and suitability for a specific budgeting style may be limiting for some.

However, it comes with a monthly or annual cost – a worthy investment for those searching for a robust, hands-on, and future-focused budgeting tool. Most YNAB budgets agree they save multiples of the subscription cost.

However, it can be less suitable for those not ready for a hands-on approach or those sensitive to subscription pricing.

Who should use Mint?

On the other hand, Mint is an all-in-one app that automatically tracks and categorizes your spending.

Based on my experience, Mint is an excellent tool for novice-level budgeters seeking to track their expenses, set budgets, and manage their finances with ease. This budgeting app allows a comprehensive view of all your financial accounts, which differentiates it from YNAB.

If you’re comfortable seeing ads and not needing investing features, Mint could be a perfect fit. However, if you require the ability to assign multiple savings goals to one account or a bill pay feature, YNAB may be more suitable for you.

Therefore, Mint is most applicable for beginners seeking a free and user-friendly budgeting platform.

YNAB vs. Mint: Which is better for you?

As a content writer and budgeting app user, I find Mint and YNAB are unique in their offerings.

Mint automatically tracks and categorizes your spending, providing an intuitive picture of where your money goes, ideal for beginners in budgeting.

In contrast, YNAB promotes a proactive approach, helping to set and monitor budgets, hence perfect for those with specific financial goals. To sum up, Mint offers a simplified, passive overview, while YNAB is excellent for a detailed, forward-thinking approach to managing finances.

Personal preferences and needs really influence the choice here. Do you need intricate control and don’t mind paying a fee? YNAB might be your fit. Prefer automation and want a free option? Mint could work for you.

YNAB vs Mint: Verdict

As an expert in personal finance tools, I’ve explored both YNAB and Mint.

In my experience, there are distinct differences between YNAB and Mint. For my readers, I recommend YNAB.

YNAB, with its laser-focused approach towards budgeting, is a boon for individuals needing extensive assistance in the budgeting arena. You learn to assign every dollar with intention, thereby gaining a higher degree of control over your finances.

This proactive approach will help you to be financially independent faster.

To sum up, if detailed budgeting is your priority, choose YNAB.

YNAB

Enjoy guilt-free spending and effortless saving with a friendly, flexible method for managing your finances.

Pros:

Comprehensive approach to budgeting, helping you plan monthly budgets based on your income.

Offers expert advice, making it suitable for those who require an in-depth, forward-thinking budgeting strategy.

Superior synchronization skills make it the winner in this area.

YNAB has extra features like goal setting for budgeting, shared budgeting tools for partners.

Option to manually add and upload transactions from accounts each month.

YNAB prioritizes user privacy.

Start 34 Day Free Trial

However, for a more holistic financial insight with less emphasis on budgeting, Mint might be the better choice.

Now, make sure to check out our Quicken Review.

Source

TrustPilot. “YNAB Review.” https://www.trustpilot.com/review/ynab.com. Accessed on September 27, 2023.

YNAB. “YNAB Pricing.” https://www.ynab.com/pricing/. Accessed on September 27, 2023.

Know someone else that needs this, too? Then, please share!!