Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

The primary credit scoring models are FICO® and VantageScore®, and both are equally accurate. Although both are accurate, most lenders are looking at your FICO score when you apply for a loan.

There’s a lot to learn about credit scores and credit reports and having more than one credit score can get confusing. When you don’t know which credit score and credit report is the most accurate, it can be difficult to know if you’ll qualify for a loan or the state of your credit health.

By understanding the different credit scores, you can save time and protect your credit. Each time you apply for a line of credit or a loan, it can lower your credit score, so it’s best to know the accuracy of your credit score before filling out applications.

Here, you’ll learn about the different credit scoring models, which score lenders use the most, and how to properly check your score.

What Is the Most Accurate Credit Score?

Although you may have different scores, they’re equally accurate based on the specific scoring model.

As the Consumer Financial Protection Bureau explains, “A credit report is a statement that has information about your credit activity and current credit situation such as loan paying history and the status of your credit accounts.”

Based on the information from your credit report, the credit bureaus give you a three-digit credit score. Two primary companies give you a score based on this information, but they weigh the information differently.

As long as the information on your credit report is accurate, your score will also be accurate. The only time your score may be inaccurate is if there is an error on your credit report, which you’ll need to challenge to request to have it removed or corrected.

Why Are There Different Types of Credit Scores?

There are two primary scoring models, and both may give you a different score. The main scoring model is through FICO, and the other common scoring model is VantageScore. Next, we’ll break down both scoring models so you have a better understanding of their similarities and differences.

FICO Scoring Model

FICO is a division of Fair Isaac and is the original company that created credit scores to help lenders assess risk in the 1960s. Based on five metrics on your credit report, FICO gives you a score that lenders use to get an idea of how likely you are to repay a loan.

The following are the five factors FICO uses for their model as well as how much they’re weighted:

Payment history: 35%

Amounts owed: 30%

Length of credit history: 15%

Credit mix: 10%

New credit: 10%

As you can see, the FICO model gives the most weight to how well you make your payments on time. The second most important factor is amounts owed, or known as credit utilization, and it represents how much you owe versus your overall available credit. They’re also looking at how much experience you have managing credit, the types of credit you have experience with, and how often you apply for new lines of credit or loans.

VantageScore Scoring Model

VantageScore 3.0 is the current version of the VantageScore scoring model. Like FICO, VantageScore is a company that gives you a credit score based on criteria from your credit report. The three major credit bureaus Equifax®, TransUnion®, and Experian® own VantageScore, and it was created in 2006 to give more people access to a credit score.

You’ll notice that VantageScore and FICO have similar scoring models but weight the scoring factors differently:

Payment history: 40%

Depth of credit: 21%

Utilization: 20%

Balances: 11%

Recent credit: 5%

Available credit: 3%

VantageScore also has one more scoring factor than FICO, and it’s for balances. This is the total amount of recently reported balances you owe, including delinquent balances.

Which Credit Score Is Used Most by Lenders?

Many consider the FICO score the more important to pay attention to. FICO states that the majorityof lenders prefer the FICO scoring model, and FICO’s website shows that 90% of lenders use their scoring model.

Which Credit Bureau Is Most Accurate?

In addition to the two primary scoring models, you will also find different scores with each credit bureaus. With Experian being the largest credit bureau, many people wonder how accurate the Experian credit score is. Much like the scoring models, your score is equally accurate with each of the individual bureaus based on the information reported to your credit report for that bureau.

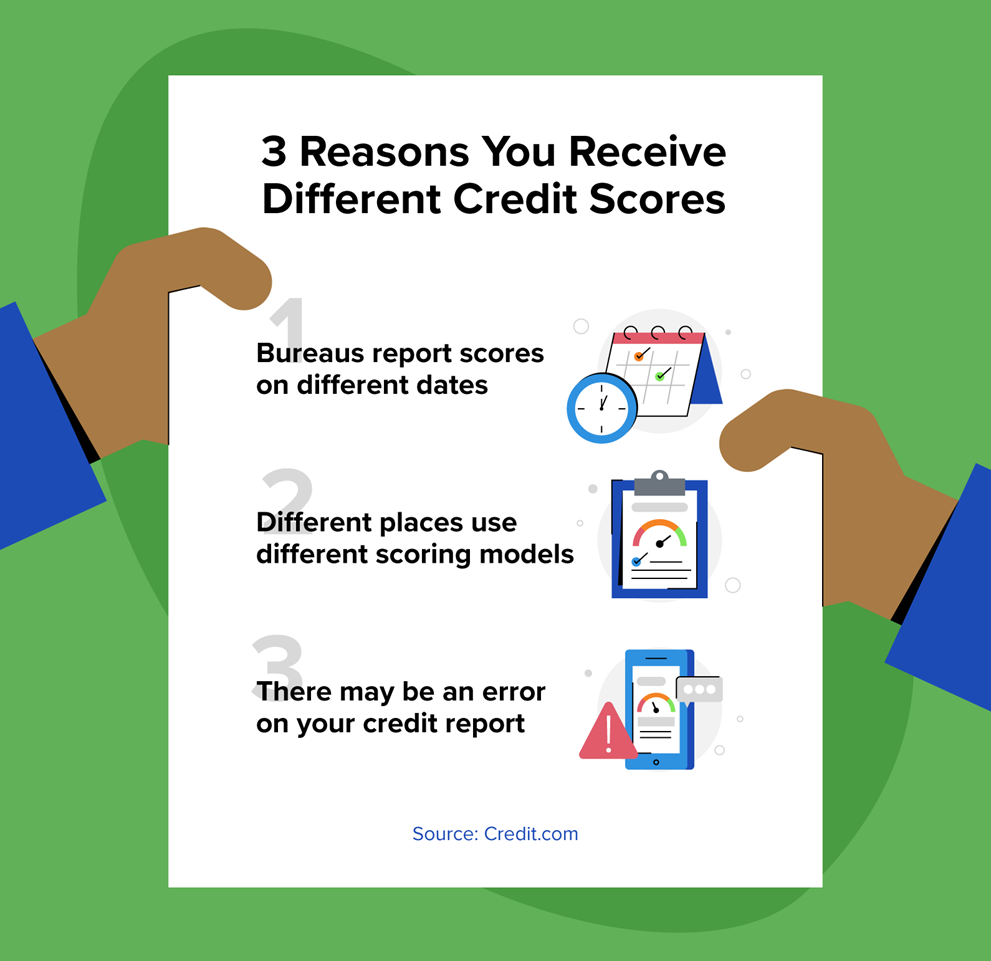

Three Reasons You Receive Different Credit Scores

Now that you have learned that your score should be accurate regardless of where you check, there may be some reasons why your credit scores differ. While slight differences in your score may be completely normal, there may also be an issue you’ll need to investigate.

The following are some common reasons you may receive different scores:

Different processing dates: The credit bureaus update your score regularly based on new information from your credit report. Each one updates the score on different dates, so you may just need to wait for your score to update with a particular bureau.

Different scoring models: Both FICO and VantageScore have gone through various versions throughout the years. Currently, FICO is on version 10, but FICO 8 is the most common version. VantageScore is on version 4.0, but many still use version 3.0. In some cases, a bureau may use a different version.

Errors on your credit report: The credit bureaus possibly received different information about payments you made or missed. It’s also possible the error is showing up for all three bureaus. If this happens, you may need to write a credit dispute letter.

How to Check Your Credit Report and Credit Score

One of the best ways you can ensure your credit score and credit report are as accurate as possible is to check them both regularly.

The law entitles you to a copy of your credit report for free under the Fair Credit Reporting Act (FCRA). To receive your free credit report, you can visit AnnualCreditReport.com.

You can check your credit score regularly, in various ways, and it won’t hurt your score. While hard credit inquiries can lower your score, credit monitoring allows you to see your score without harming it, according to the Consumer Financial Protection Bureau.

You can check your credit score for free right here at Credit.com. We also offer a free credit report card, which will give you a more in-depth look at the state of your credit health and what factors are impacting your score most.

How Monitoring Your Score Can Help Keep It Accurate

Many aspects of your financial life revolve around your credit score, so it’s helpful to keep an eye on it as best as possible. Your credit score determines whether or not you receive loans, how much your security deposits are, and where you can rent or buy a home.

A great way to check your credit score regularly is through Credit.com’s ExtraCredit® service. When you sign up for ExtraCredit, you’ll be able to track your FICO score with all three credit bureaus. It also comes with alerts, so you’re the first to know when something changes with your score or when there are potential errors. These are just a few of the features, so sign up for your seven-day free trial today!

Disclosure: Your 7 day trial will begin after agreeing to these terms. After your trial period, your subscription will automatically continue on the same day every month as the day you started your trial membership. The free trial is available for new ExtraCredit customers only. The credit card you provided will be charged $24.99 (plus any applicable tax) on the next business day and monthly; after your trial period unless you cancel. You may cancel at any time by downgrading your service level in your settings or by contacting us at [email protected]. Dishonored payments will result in an automatic downgrade to the free credit.com product.

In July 2021 alone, more than 700,000 new home sales were processed. While that sounds like a lot, the number is lower compared to 2020, due in part to a housing shortage. Pair that shortage with plenty of people looking to make a home purchase and you have a competitive market in 2021 and beyond.

You might think that these are just numbers—but understanding the housing market is pivotal to the mortgage approval process. If you’re considering buying a home, we’re here to guide you through the mortgage process. Get ready to be set up for success.

In This Piece

Understand Your Credit History and Score

The home loan approval process includes a pretty thorough credit check. While you might be able to get approved for an FHA mortgage loan with a credit score as low as 500, most traditional mortgage loans require at least a 620 or higher.

While your credit score might make or break you at the beginning of a mortgage application process, once you continue the process, your entire credit history becomes important. Mortgage lenders look at issues such as delinquencies or open collections accounts on your credit history. They may also require that you make good on any open collections accounts before your mortgage approval can go through.

It’s a good idea to understand your credit history and score months before you plan to apply for a home loan. That way, you have time to resolve any issues or dispute inaccurate negative information that could be dragging your score down.

You can get a free credit report from each of the major credit bureaus at AnnualCreditReport.com. You can also sign up for services such as ExtraCredit to get ongoing access to your credit reports and scores. ExtraCredit also includes features such as Build It that help you work on building your credit so you have a better chance at getting the mortgage loan—and rates—you want in the future.

Get matched with a personal

loan that’s right for you today.

Learn

more

Prepare Your Personal Finances for the Home-Buying Process

Your credit isn’t the only financial factor that impacts your mortgage application process. Yes, your history of on-time payments to other creditors is important. But so is your ability to make payments on the mortgage loan in the future. Lenders are likely to be concerned with:

Your debt-to-income ratio, or DTI. This is how much of your income you need each month to pay your existing debts. The lower this figure is, the better. According to the Consumer Financial Protection Bureau, most mortgage lenders won’t approve home loans that bring a consumer above 43% DTI.

Your income. In most cases, you’ll need to demonstrate that you have the income or other financial means to make your monthly mortgage payments. Your income can impact how much you can get approved for or whether you’re approved at all.

Your cash savings or other assets. If you need to make a down payment on your mortgage loan, you may need to demonstrate where that cash came from. You can get creative with sourcing your down payment within some rules, but you can’t always borrow it. And you can’t have cash show up in your account suddenly in the middle of your mortgage approval process without an explanation.

Understanding what mortgage lenders look at when considering you for a home loan could proactively help your case. Start early and work on reducing debt, increasing income and saving money for your down payment.

Decide What Mortgage You Can Afford

When you’re close to ready to start looking for a house and applying for a mortgage, take time to get an idea of how much mortgage you can actually afford. Start by taking a look at your budget—or create one if you don’t already have one.

Try to factor in expenses related to a new home, including savings for emergency repairs or maintenance. Once you know how much of a monthly payment you can afford, use an online mortgage calculator to test various loan and interest amounts. This helps you figure out your limits for home price, so you look for properties you can afford.

Research Potential Mortgage Options

Armed with knowledge about your budget, your credit and your overall financial status, hopefully you’re ready to do some research. Don’t apply yet—you want to apply for mortgages when you’re ready to make an offer on a home.

In the meantime, do some research. Talk to your bank, and maybe even reach out to a mortgage broker. That way, you’ll know your options and what you might qualify for.

Gather Documents to Apply for a Mortgage

During your research, make notes about what documents and items a mortgage lender requires for the application. Gather those documents and information before you apply for preapproval or a mortgage. You’ll save major time and hassle during the home loan approval process.

Some items you might need include:

Identification, such as a driver’s license or other government-issued ID.

Documentation of your income, such as paycheck stubs, W2 forms or tax returns.

Documentation of assets, especially assets like savings or investment accounts that might be involved in sourcing your down payment.

Your Social Security number for the credit check.

Documents showing you paid or settled any collections accounts or other negative issues on your credit report.

You may be asked for other items or documents throughout the mortgage underwriting process. When you apply for a mortgage make sure you’re available via email or phone, in case lenders have extra questions for you.

Consider Getting Pre-approved for a Mortgage

Getting pre-approved for a mortgage can be a good step. Preapproval doesn’t mean you’ve successfully completed the entire mortgage approval process. However, it does mean the lender did a cursory review of your credit history and score—as well as any income information you reported—and is fairly comfortable saying you’ll be approved with a certainrate.

Preapproval letters let you shop more confidently for a home. They also help demonstrate to sellers that you’re serious about your offer and will probably follow through without financial hiccups. In a competitive market with numerous offers on each home, this can make your offer more attractive to some sellers.

Apply for Mortgages Within a Short Period of Time

Finally, once you’re ready to purchase a home, ensure you apply for mortgages within a short period of time. Each time you apply for a loan, your credit is hit with a hard inquiry—which will bring your score down a bit. But the credit scoring models treat multiple mortgage applications within a short period of time as a single hard inquiry, because it’s assumed you may want to shop around for a good deal.

You should also be ready for the prospect of being approved with conditions. This means the mortgage lender will approve your loan as long as you meet certain conditions, which could include:

Providing supplemental documentation of credit history or income.

Satisfying the lender’s requirements for copies of banking statements or other documents.

Explaining an inconsistency or issue on your credit report.

Settling an old collections account or other debt.

Verifying where funds for a down payment came from.

Start Your Mortgage Application Process Today

Ultimately, being successful with the home loan application process comes down to being prepared and in good financial standing—or as in as good financial standing as you can. If you’ve gone through the above steps and are ready to apply for a mortgage, consider shopping for rates today.

Many people were thrown into financial turmoil at the beginning of the COVID-19 pandemic. Previously secure jobs disappeared, and monthly payments went from affordable to impossible overnight. A year later, borrowers are still catching up—and some are struggling to make ends meet. So, if you can’t afford your car payment, what are your options?

We have eight solutions to an unaffordable car loan in this article. Some are easier to implement than others—and some come with long-term credit implications:

How can you lower your car payments without refinancing? Before you do anything else, speak to your lender about modifying your auto loan. Call your auto loan company as soon as you can, and tell them about your financial troubles. Ask if they have any relief options for borrowers, including loan modifications.

Many lenders made changes to their modification policies in response to the COVID-19 pandemic. Temporary loan forbearance and extension programs, for instance, help borrowers get back on track.

Perhaps surprisingly, many lenders let borrowers in good standing pause their auto loans for a month once a year. Of course, you’ll have to make an extra payment at the end of your loan term to make up the difference—and you might have a little extra interest to pay.

2. Refinance Your Vehicle Loan

How do you get out of a car loan you can’t afford? The answer might be to refinance your vehicle. If you have a good payment history and a strong credit profile, use it to your advantage. Here are two ways to play the refinancing game:

Get matched with a personal

loan that’s right for you today.

Let’s imagine you bought your car for $20,000 two years ago. Your original 60-month auto loan came with a 5.5% interest rate, and your monthly payments are $382.02. Your current loan balance is $12,600.

If you extend your loan by five years, your monthly payments will drop to $241. You’ll have $141 more spending money each month—but you’ll pay more in interest over the life of your loan, plus you’ll have to make payments for a longer time period.

3. Trade in Your Car

If you can’t afford your car payment any more, consider trading in your vehicle. Think about your automotive needs—could you get away with a smaller car, for instance? Do you need a truck, or would it be easier to park a sedan in your driveway?

Swapping your SUV for a smaller model isn’t just environmentally friendly—it’ll also cost less to run. Switching from a new luxury vehicle to a slightly older regular brand auto, on the other hand, could cut your insurance bill significantly. Either choice will reduce your car payment.

If you do decide to trade in your car, get quotes from several dealerships. Then, negotiate a fair price with your favorite dealership and choose an alternative vehicle. If you’re not upside-down in your current loan—if you don’t owe more than it’s worth—you might even be able to trade upto a newer vehicle with better loan terms.

4. Let Someone Else Assume Your Loan

Some loans and leases are “assumable,” which means that they’re transferable from one party to the next. If you can’t make your loan payments any more but you want to avoid damaging your credit, consider passing the loan, and the vehicle, to someone else.

Before you agree to pass your car on, talk to your lender. Most lenders have minimum credit and income requirements for buyers—and the person you transfer your vehicle to will need to meet these terms.

5. Sell Your Vehicle

Do you need a vehicle right now, or can you use public transportation until your finances settle? If buses or trains are an option in your area, consider selling your vehicle privately and using the money to pay off the remainder of your loan. Doing so could help you escape a car payment altogether—plus private sales nearly almost generate more money than dealer trade-ins.

6. Turn the Keys In

Can you give your car back to the finance company? You sure can! Also called “voluntary repossession” or “voluntary surrender,” walking away from your vehicle is a last-resort option if you can’t refinance or sell your car.

Unfortunately, there are consequences associated with turning in your keys. On the one hand, the repo man won’t pay you a personal visit, which can save embarrassment. On the other, the lender might still try to collect money from you if you owe more than they can get for the vehicle at auction. A voluntary repossession will also show up on your credit report.

If you do decide to turn your keys in, contact your lender and tell them your intentions. Your lender will guide you through the process and let you know when and where to hand over your car.

7. Let Your Car Be Repossessed

The alternative to voluntary surrender is straight repossession. This option is perhaps the most stressful, and it can severely affect your credit. In a nutshell, you simply wait until you’re so behind with payments that your lender decides to repossess the vehicle. Then, your car—and anything you leave inside—is towed away. You might want to consider this as a last option—carefully look at your resources and consider exhausting your other options before you decide.

8. File for Bankruptcy

If you’re in a huge financial hole and you owe a lot of money beyond your car payment, you could consider bankruptcy. Bankruptcy is complicated and can pull your credit down for a decade, so it’s not an option to consider if there are any alternatives open to you. Before proceeding, take a good look at your finances and contact a well-regarded bankruptcy attorney.

Take Care of Your Finances with Credit.com

Whatever you decide to do, it’s important to keep track of your credit. Sign up with Credit Report Card to view your Experian VantageScore 3.0 and see a helpful credit snapshot, which you can use to create a financial plan.

Educating yourself about debt collection scams is one of the best ways to avoid them. And if fake debt collectors come calling or you suspect you’ve fallen victim to such scams, there are things you can do to protect yourself.

9 Tips for Preventing Debt Collection Scams

Verify the Debt Is Legitimate

Verify the Agency Is Legitimate

Check Your Credit Reports

Protect Your Information

Contact the Original Creditor

Understand Your Rights

File a Complaint

Contact the Credit Reporting Agencies

Remember Some Debt Is Legitimate

About Debt Collection Scams

The Federal Trade Commission reported that scam and fraud reports were up an unfortunate 70% from 2020 to 2021, and imposter scams were the main culprit. They accounted for $2.3 billion in losses in 2021.

Imposter scams include any scam that involves a person or entity pretending to be someone else. That includes debt collection scams where someone pretends to be a legitimate company collecting debt from you. Here are a few things you should know about debt collector scams:

They can happen to anyone, and some scammers are quite sophisticated. That means it can be possible for anyone to get tricked into giving these people money.

You have a right to verify debts before you agree to talk about payments.

Doing a bit of homework and following paperwork trails can help you avoid debt collection scams.

Keep reading to discover the steps you should take when you’re contacted by a debt collector or think you might be the target of a collection agency scam.

Verify the Debt Is Legitimate

You have the right to ask for verification of a debt when you’re contacted by a debt collector. Do this by disputing the debt in writing and asking the collection agency to send a validation letter, including the name and address of the original creditor for the debt.

A legitimate creditor will provide you with information that includes:

The amount you owe

The name of the original creditor

A notice of your rights, including your right to dispute the debt

If the agency is unable or unwilling to provide this information, they are either violating your rights as a consumer or may be attempting to scam you.

Verify the Agency Is Legitimate

Avoid cash-and-go scams and other issues by verifying that the collection agency contacting you is legitimate. Here are some steps you can take to do so:

Ask for everything in writing. Never negotiate or make payment based solely on a phone call.

Research the collection agency online. Look for a legitimate website or information on sites like the Better Business Bureau to find out if the business is real.

Call your state attorney general’s office to find out if there are any complaints about the agency and if it can legally operate in your state.

Check Your Credit Reports

Checking your credit reports or your free credit report card helps you understand whether you might owe a debt you didn’t know about. It also lets you see if someone has reported inaccurate information about a debt you don’t owe. When you know what’s on your credit reports and whether or not it’s accurate, fake debt collection calls can’t use that information to threaten you.

Protect Your Information

Sometimes fake debt collection callers want more than your money. They may also try to trick you into giving them enough personal information that they can steal your identity or sell the information to people who would. Protect your information by being careful what you say to these callers. Never answer questions like “Can you confirm your full name or your Social Security number” if someone calls you about a debt. If they called you, they should have the information they need to collect the debt and shouldn’t ask you to provide it.

Contact the original creditor to find out more about the debt, whether you think you owe it or not. If you do owe the debt, you may be able to negotiate a payment with the original creditor that’s less than you’d pay a debt collection agency.

Understand Your Rights

There are rules for sending someone to collections that businesses must follow, and there are also rules that govern how debt collectors pursue debts. For example, no collector can harass you, and if you’re being harassed, it could be a sign that the agency isn’t legitimate. If you’re on the phone with a debt collector threatening to serve papers, your best defense is knowing what laws are on your side.

File a Complaint

You can submit a complaint with the Consumer Financial Protection Bureau if you believe a debt collector is violating your rights or you’ve been targeted by a debt collection scam. You can also file a complaint with your state’s attorney general’s office.

Debt collection scams can be a sign that your information is at risk. To run one of these scams, someone has to have enough information to come up with a plausible-sounding debt in your name and contact you. It may be a good idea to freeze your credit report with the credit bureaus. That means no one can pull your credit report for the purpose of evaluating you for a loan or other debt unless you unfreeze your report—and no one impersonating you can cause that to happen, either.

Remember Some Debt Is Legitimate

Finally, remember that some debt is, unfortunately, legitimate. It may be shocking to hear from a collection agency about an old debt, but that doesn’t mean you don’t owe it. While you can ask that the debt collection agency stop contacting you, if the debt is real, you still owe it. Failing to pay it could result in a lawsuit or further action to collect from you.

Getting Back on Track After a Debt Collection Scam

If you think you’ve been the target of any type of financial scam, including a debt collector scam, it’s important to work to get your credit information and other accounts in order as soon as possible. Working with a credit repair organization can help you attend to those details while continuing to live your life.

This article has been updated. It was originally published Feb. 3, 2015.

Buying a used car can lower the cost of your purchase, letting you move into car ownership with a much smaller loan. This might also be beneficial if you don’t have the credit or income to qualify for a loan amount that would cover a new car price. You might get an even better deal if you buy a used car through a private seller. However, it’s important to ensure you’re protected from scams and engaging in a safe transaction.

This piece covers how to buy a used car from a private seller. That includes how to get a loan for a used car from a private seller.

In This Piece

How to Buy a Car from a Private Seller

When you’re buying a car from a private seller, there are some additional concerns you may not have when buying a vehicle from a dealership. Private sellers don’t have consumer reviews and brand reputation you can consider. So, you have to do some legwork to ensure you’re getting a good deal and aren’t getting scammed. Follow the steps below to buy a car from a private seller.

Shop Around for Local Deals

Start by understanding what you can afford. If you want to know how to finance a private car sale, start by getting an auto loan first. You can apply for auto loans online or with a local bank. Once you get pre-approved, you know how much used car you can afford.

Not sure if you can get approved for a car loan? Get your credit score first to see your odds of being approved and work toward improving your scores before moving forward with your purchase.

Privacy Policy

Use your loan pre-approval or cash on hand to set a budget for your car purchase. Avoid going outside that budget so you don’t have a financial hardship once you buy the used car.

Get matched with a personal

loan that’s right for you today.

Learn

more

Start researching cars that fit your needs. Read about cars you’re interested in online, and look into different considerations for older models. This helps you know what type of common issues to look for when you start checking out cars from private sellers.

Next, review the cars available from private sellers in your area. You can research options on Facebook marketplace, Auto Trader, eBay and any local classified publications, such as your city’s newspaper.

Contact the Seller

Once you spot a potential new-to-you ride, start by making contact with the seller. Take some time to feel them out and ensure they’re legitimate. Avoid meeting anyone by yourself or in a location you’re not comfortable with. If the seller is willing to come to a public location with the vehicle, that’s best. If not, take someone with you when you go to their home.

Ask to test-drive the vehicle. If you can have a mechanic or someone you trust who knows a lot about cars look over the vehicle, do so. You can also look up the CARFAX report on the vehicle using its VIN. This database and others like it provide some information about the vehicle’s history, including potential accidents, service records and how many owners the vehicle might have had.

Once you’re confident you’ve found the vehicle for you, start negotiations.

Complete the Sale

Once you and the private seller agree on a price for the vehicle, move forward with the transaction. Make sure you get any agreement in writing to protect yourself in the future. You may also want to pay by check so you have a paper trail demonstrating that money changed hands for the car.

Verify ownership documents when you complete the sale. If the individual has the title on hand, they should sign it over to you at that time. If the seller owes money on the car, there’s a lien on the title. You’ll need a bill of sale indicating you paid for the vehicle. The owner will then take your money to their bank to pay off the car so they can get a title to transfer to you.

Complete the Paperwork

Even if you go through a private seller and not a dealership, buying a car requires lots of paperwork. You’ll need to:

Ensure you have a receipt or bill of sale documenting the purchase

Get the title from the seller at the time of purchase or after the fact

Go to the DMV with the title and ask for a transfer of ownership, which includes the completion of a form and getting a new title

At the DMV, you may need to pay tax, title and registration

Depending on your state, you may have to pay sales tax on the vehicle purchase

Bottom Line

Always have a plan when you’re making large purchases. Create a budget and stick to it to avoid overcommitting yourself financially. Do the research to protect yourself from scammers. If a deal seems too good to be true, it may be.

If you need a loan to buy a used car from a private seller, start by comparing auto loan rates. Then, you can prepare yourself with everything you need to help finance your new car.

More Money-Saving Reads:

Article updated. Originally published July 15h, 2015.

In the United States, it’s illegal to drive a car without car insurance. Depending on the state you’re driving in, the consequences of doing so can range from a fine to a misdemeanor on your record. So, if you’re planning on hitting the road anytime soon, be sure to purchase car insurance to avoid penalties.

In this article, we’ve researched the average cost of car insurance by state to give you a better idea of how much to budget.

Key findings:

According to AAA, the national average cost of car insurance for a full-coverage policy was $1,588 in 2022.

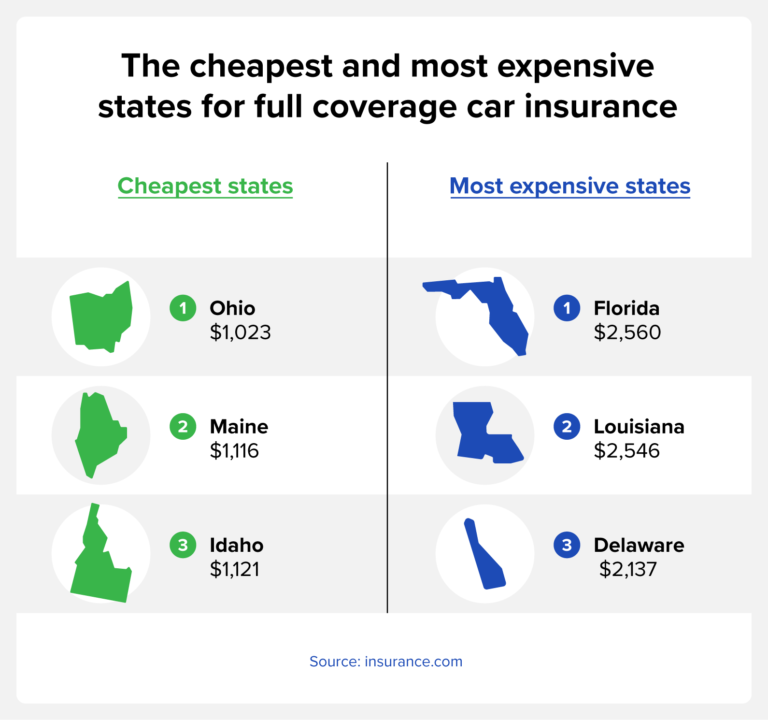

On average, the cheapest states for full coverage car insurance are Ohio, Maine and Idaho, while the most expensive states are Florida, Louisiana and Michigan.

USAA, Geico and State Farm offer the cheapest minimum coverage plans, while USAA, Geico and Nationwide offer the cheapest full-coverage insurance.

The average cost of car insurance tends to decrease with age, but starts to rise again around age 70.

Individuals with high credit scores pay lower car insurance premiums on average compared to those with poor credit.

How much is car insurance?

According to AAA, the national average cost of car insurance for a full-coverage policy was $1,588 in 2022. This figure is based on an under 65 years old driver who lives in the city or suburbs, has over six years of driving experience, and has not been involved in any accidents.

Average cost of car insurance by state

When calculating the cost of car insurance, the state you live in plays a role in how much you can expect to pay. This is because factors like population density, climate, road conditions and crime rate in your area can play a part in the likelihood that you’ll file a claim.

According to insurance.com, the cheapest states for car insurance if you’re looking for minimum coverage are Iowa, South Dakota and Wyoming costing an average of $263, $267, and $293, respectively. Meanwhile, the cheapest states for full coverage auto insurance are Ohio ($1,023), Maine ($1,116), and Idaho ($1,121).

The most expensive states for car insurance in terms of minimum coverage are New Jersey, Florida, and New York where drivers pay an average of $989, $908 and $875, respectively. For full coverage insurance, drivers in Florida ($2,560), Louisiana ($2,546), and Delaware ($2,137) pay the most in the country on average.

State

Minimum coverage

Full coverage

AK

$336

$1,359

AL

$420

$1,542

AR

$422

$1,597

AZ

$494

$1,617

CA

$582

$2,115

CO

$467

$1,940

CT

$773

$1,750

DE

$821

$2,137

FL

$908

$2,560

GA

$567

$1,647

HI

$389

$1,306

IA

$263

$1,321

ID

$326

$1,121

IL

$484

$1,578

IN

$384

$1,256

KS

$389

$1,594

KY

$717

$2,105

LA

$726

$2,546

MA

$523

$1,538

MD

$607

$1,640

ME

$330

$1,116

MI

$711

$2,133

MN

$479

$1,493

MO

$525

$2,104

MS

$434

$1,606

MT

$389

$1,692

NC

$396

$1,368

ND

$340

$1,419

NE

$350

$2,018

NH

$411

$1,307

NJ

$989

$1,901

NM

$376

$1,505

NV

$683

$2,023

NY

$875

$2,020

OH

$308

$1,023

OK

$352

$1,797

OR

$551

$1,244

PA

$398

$1,445

RI

$648

$1,845

SC

$628

$1,894

SD

$267

$1,581

TN

$368

$1,373

TX

$520

$1,875

UT

$526

$1,469

VA

$469

$1,321

VT

$306

$1,158

WA

$505

$1,371

WI

$375

$1,499

WV

$474

$1,610

WY

$293

$1,736

Average cost of insurance by company

Another factor that’s going to influence how much you can expect to pay for car insurance is the specific company you purchase your plan through.

According to U.S. News & World Report, USAA, Geico and State Farm offer the cheapest minimum coverage plans, while USAA, Geico, and Nationwide offer the least-expensive full-coverage insurance.

Farmers, Progressive, and Nationwide offer the most expensive minimum coverage rates while Allstate, Farmers, and Progressive offer the most expensive full coverage plans.

Insurance company

Minimum coverage

Full coverage

Allstate

$1,961

$2,138

American Family

$1,327

$1,388

Farmers

$1,782

$2,059

Geico

$1,064

$1,238

Nationwide

$1,347

$1,338

Progressive

$1,440

$1,650

State Farm

$1,191

$1,348

Travelers

$1,290

$1,448

USAA

$948

$1,056

Average cost of insurance by age

According to CarInsurance.com, the cost of both minimum and full coverage car insurance tends to decrease with age, as seen in the chart below. However, there is an uptick around age 70 where rates start to go back up.

Age

Minimum coverage

Full coverage

20

$1,109

$3,532

30

$539

$1,785

40

$520

$1,682

50

$496

$1,581

60

$482

$1,511

70

$554

$1,661

Average cost of insurance for young drivers

Young drivers are the most expensive age group to insure. Although there are a few exceptions, insurance rates decrease with age among young drivers.

Age

Minimum coverage

Full coverage

16

$2,402

$7,203

17

$1,971

$5,924

18

$1,706

$5,242

19

$1,234

$3,874

20

$1,109

$3,532

21

$884

$2,864

22

$794

$2,593

23

$736

$2,415

24

$690

$2,267

Average cost of insurance by credit score

According to the Insurance Information Institute, your credit score is a good indicator of how many insurance claims you’ll file. As a result, insurance companies use credit scores to determine risk, and those with a good credit score pay cheaper premiums. The Zebra found that individuals with poor credit pay approximately 114% more than those with great credit.

Credit score

Average annual rate

Very poor (300-579)

$2,887

Average (580-669)

$2,296

Good (670-739)

$1,912

Excellent (740-799)

$1,606

Exceptional (800-850)

$1,350

What factors affect your car insurance rate?

As you can see from the above charts, the cost of car insurance varies by the following factors:

Age: Typically, young drivers under the age of 25 and senior drivers over the age of 65 are charged more for car insurance.

State of residence: Since the minimum coverage required varies by state, your location is one of the factors that will influence the price.

ZIP code: In addition to your state of residence, your ZIP code will also play a role in the cost of insurance since your vehicle is more likely to be damaged in certain areas, such as ZIP codes with high crime rates. Typically, the cost of car insurance will be greater in cities than in rural areas.

Marital status: Statistically, married drivers are less risky than single drivers resulting in a lower insurance cost.

Gender: Based on risk, male teenage drivers tend to have the highest cost of car insurance of any demographic.

Credit history: Those with a low credit score tend to pay higher premiums than individuals with good credit.

Driving record: Since car insurance premiums are based on risk, individuals with a good driving record can expect to pay lower premiums, while those with a poor driving record may experience increased rates.

Car make and model: You may pay less if you drive a vehicle that insurance companies deem safe. On the other hand, you’re likely to pay more if you drive a small sports car since they pose a higher risk.

Mileage: Higher annual mileage increases the risk you’ll get into an accident and will likely raise your premiums.

High-risk violations: Driving under the influence andat-fault accidents are examples of violations that may result in you being considered a high-risk driver.

What’s the difference between full and minimum coverage?

Minimum coverage car insurance — liability coverage — is required in most states and is used if you’re at fault in an accident. This coverage will pay for damages and injuries of the other party when you’re responsible for the incident.

On the other hand, full coverage insurance, or collision coverage, includes liability coverage plus damage caused to your own vehicle. Keep in mind that lenders often require you to obtain full coverage insurance before you get an auto loan.

FAQ

Below, we’ve answered some common questions regarding the cost of auto insurance.

Can my driving record affect my car insurance rate?

Your driving record is one of the factors that affects your car insurance rate. As a result, those with traffic violations or accidents on their record can expect to pay higher premiums.

Does your car insurance cost go down after you pay off your car?

Your care insurance cost doesn’t typically go down after your pay off your car. However, you do have the option to decrease the amount of coverage on your vehicle once it’s paid off.

Which car insurance company is the cheapest?

As mentioned above, insurance companies that offer the cheapest plans include Geico, Auto-Owners, USAA and Erie.

Does car insurance decrease annually?

For young drivers in particular, car insurance rates decrease each year you renew your policy without filing a claim. You can expect to see the biggest drop in price at age 25.

The average cost of car insurance varies by factors including state, age, insurance company and credit score. Some factors, such as your age, are beyond your control, but other factors, such as your credit score, can be improved.

Check your credit score for free today to see if it’s a reason your car insurance is high.

Cyber-attacks are on the rise as hackers and criminals learn about and adapt to methods put in place by government agencies to prevent scams. The FBI’s Internet Crime Complaint Center (IC3) reported monetary losses totaling more than $1.4 billion in 2017. [1]

While anyone, regardless of age, can be a target of common money scams, many hackers specifically target seniors. Nearly 17% of reported cyber crimes in 2017 came from victims over the age of 60. And with losses of over $342 million, seniors are losing more money to scams than any other age group. [1] Considering the average age of retirement in the U.S. is 60, this trends is a serious threat to the financial security of many Americans as they enter retirement.

With an empty nest and retirement on the horizon, your senior years should be the time to pursue your passions—not get scammed out of your hard-earned savings.

This guide covers the basics of recognizing and preventing common online money scams, plus provides tips to help seniors navigate the online world safely.

Table of Contents:

Why Scammers Target Seniors

Pew Research shows that seniors are adopting technology, such as the Internet and smartphones, more than ever before. [2] If you’re among the technology adopters, you know how great technology is for connecting with your children and grandchildren who live far away and with friends you haven’t seen in years.

Con artists and scammers exploit seniors online believing that they aren’t Internet-savvy, despite many proving otherwise. Here are a few of the reasons seniors are a frequent target of scams online:

You generally have larger savings accounts and valuable assets.

You’re perceived as more trusting and polite.

You may not recognize and report the scam right away.

As you age, cognitive function and physical ability declines.

How to Recognize a Money Scam

As online scammers get increasingly sophisticated, certain types of fraud can be hard to spot even for the most adept Internet user. To keep from falling victim to scammers’ tactics, make yourself aware of common warning signs and stay vigilant. A gut feeling is always a good place to start. For example, if something feels too good to be true, it probably is. Also, if a request from someone you know feels out of character, trust your instincts and do your research before taking action.

An easy way to know if something is a likely con is to use the three U’s for identifying money scams.

Unexpected: If you receive an email from someone you trust making an unexpected or unusual request for money or personal information, contact them personally to confirm.

Urgent: If the tone of the message is threatening or asks you to act immediately, take time to think it over or tell a friend before acting. If you’re still unsure, check the IC3’s Alert Archive to see if there have been other incidents of the same scam.

Unsecure: Make sure the address bar reads “https://” and not “http://” when entering personal or financial information online. If a URL begins with “https://” that tells you the site is secure and protects information that’s transmitted. If you provide sensitive information to an unsecure site, it can easily be stolen.

Top 10 Online Scams That Affect Seniors

Scammers see senior citizens as easy victims, but you can prove them wrong by educating yourself on some of their common schemes. They often use things like healthcare, retirement savings and online dating to lure unsuspecting seniors into giving over their personal information. Here are 10 of the most common online schemes that target seniors.

1. Medicare Scams

If you’re 65 or older, you might rely on Medicare for your health coverage. Scammers know this and whenever Medicare sends out new cards or makes changes to its policies, they capitalize on opportunities to steal personal information. This can be done over the phone or by email. The scammer claims to be a Medicare representative and insists there’s a fee associated with getting you a new card or that your card has been compromised—neither of which is true.

According to Medicare.gov, “Medicare, or someone representing Medicare, will never contact you for your Medicare Number or other personal information unless you’ve given them permission in advance.”

How to protect yourself: Don’t respond to the email and mark it as junk or spam. If you need to speak with Medicare, call them directly at 1-800-MEDICARE (1-800-633-4227).

2. Health Insurance Scams

In order to make a profit, criminals may try to offer you health insurance plans that have little to no real value. In some cases, they may be selling discount cards or limited-benefit plans, but rarely explain how limited the coverage really is.

How to protect yourself: Never purchase insurance on the spot. Do your research on the company and thoroughly read the details of the coverage offered.

2. Counterfeit Medications

This scam is especially dangerous because it can cost you not only your money but your health. Prescription drugs aren’t cheap, and most seniors are dependent on a medication or two to maintain their health. Scammers exploit this by offering fake prescription medications for purchase online at a low cost. The number of counterfeit medication scams under investigation by the FDA is up four times since the 1990s. [3]

How to protect yourself: Always go through licensed medical professionals to get any prescriptions and pick up your medications at a local pharmacy. If you enjoy the convenience of ordering online, many reputable pharmacies allow you to refill your prescription online or have your medications delivered.

3. Phishing

Scammers often capitalize on your trust in people and institutions by posing as them in emails, on calls or in text messages. For example, the Social Security Scam is a form of phishing where scammers pose as government officials who need your social security information. Once they’ve gained your trust, they use that to gather personal, sensitive information like your Social Security number, bank/credit card information and/or passwords.

How to protect yourself: Always check the sender’s email address or phone number before clicking any links in emails or messages that request personal information.

4. Dating and Romance Scams

Online dating can be great for people of all ages—seniors included. But it’s important to practice the same kind of cautions online as you do in real-world dating. Online dating scams are one of the biggest and most costly scams, and scammers can break your heart and bank account if you’re not careful. It’s a red flag if someone builds a rapport with you only to turn around and ask for money. Even if the request seems heartfelt, like wanting to come see you, it could still be a play solely for money.

How to protect yourself: Take things slow, do your research and never send money to someone you don’t know personally. Even if you’ve met them, run the other way if they ask for money after you’ve known them only for a little while.

5. Investment Scams

In these cons, scammers take advantage of your need to build or maintain retirement savings. A lot of seniors are concerned about making their money last, which makes them vulnerable to ads or requests that promise high-profit, no-risk investments.

How to protect yourself: Stop and think, “Is this too good to be true?” Never accept an offer on the spot. If you’re not sure, talk it over with a trusted friend or check the IC3’s Alert Archive along with other online sources, such as the Scams and Frauds page on USA.gov.

6. Homeowner Scams

Seniors are at a point in life where they’re more likely to own their homes. While some may want to stay right where they are, others have grand dreams of moving to a new location—maybe somewhere warmer. In this scenario scammers work to identify the value of your property and then offer you a reassessment—for a fee, of course.

How to protect yourself: If you want to move, only work with a reputable realtor or go the for sale by owner route.

7. Sweepstakes and Lottery Scams

These scams use a surprise factor to trick you into thinking you need to click something to “claim a prize.” It can come as an email, a web pop up or even within a web page you’re reading.

How to protect yourself: If you receive an email that claims you’re a winner, it’s almost guaranteed to be a scam. On the off chance that you actually signed up for a sweepstakes, check your email inbox to see if you have a confirmation of your signup from the same email address. Better, yet, pick up the phone and call the company before you click on a link in an email or on a website.

8. Fake Charities

Seniors may feel more compelled to donate to those in need or contribute to disaster aid, but unfortunately fake charities often try and get donations after a natural disaster.

How to protect yourself: Do your research. Call a number to speak with someone from that charity or search the charity name and a phrase like “scam” or “fraud” in Google. You can also use the organizations listed by the FTC to research reputable charities.

9. Malware Scams

Using antivirus software is a great way to protect yourself from fraud. Unfortunately, scammers often pose as antivirus providers and instead install malware on your computer. These advertisements are often pop ups or web page ads.

How to protect yourself: Make sure anything you download to your computer is from a reputable source and never give anyone you don’t trust remote access to your computer.

10. Threats and Extortion

These types of scams utilize fear to get the desired outcome. Typically the scammer tells you that something terrible is going to happen if you don’t give them money or personal information.

How to protect yourself: Never act impulsively. Consider whether the scenario seems realistic. If you’re unsure or scared, talk to a friend. If the caller acts like a relative, hang up and call them back to ensure it is, in fact, your relative and not a stranger pretending to be your relative.

How to Protect Yourself Online

It’s good to know the basics about scams and the accompanying warning signs, but there are steps you can take to further protect your computer and online identity from fraud including. settings, tools and government resources.

Keep your firewall turned on. A firewall monitors incoming and outgoing network traffic to prevent unauthorized access to and from a private network. It protects your computer from hackers attempting to crash it or gain sensitive information.

Keep your computer’s operating system up-to-date. Make sure your computer software is up-to-date. You can usually subscribe to automatic updates online. If you keep your system updated, your computer will continue running smoothly and you’re sure to have the latest fixes for any security holes.

Turn on two-factor authentication. Two-factor authentication requires both a password and an additional piece of information to access your account. The second piece of information is typically a message sent to your phone or a code generated by an app or token.

Look out for unsecure networks and websites. If you get a warning message saying “Unsecure Wi-Fi Detected,” don’t visit any banking websites or store any passwords while on that network.Also, most browsers will warn you when you visit an unsecure site. The feature should already be enabled on most computers, but if not, make sure you enable this setting.

Install or update antivirus software. Antivirus software prevents malicious software programs from installing on your computer. Malware programs allow others to see your computer activity. Be wary of any ads on the Internet for these types of software as they are often not real solutions and instead are fraudulent.

Use a password manager. A password manager, like LastPass or Dashlane, lets you have a unique, strong password for every secure website—in other words, not your grandchild’s birth date. You won’t have to remember them all, because the password manager stores and encrypts your passwords for your protection.

Check your credit often. Major changes toyour credit can indicate potential fraud. Consider signing up for a free credit score and checking it every few weeks as a way to watch for changes.

Find Information About Active Scams

What To Do If You’re the Victim of a Scam

The best thing to do if you suspect you’ve been the victim of a scam is to report it. IC3 chief Donna Gregory says, “We want to encourage everyone who suspects they have been victimized by online fraudsters to report it to us.” IC3 receives over 800 complaints a day on average, so don’t let embarrassment keep you from reporting something.1 Reporting a scam helps law enforcement investigate similar scams and take action to bring the scammers to justice.

Steps to Take After Fraud

To report a scam, file a claim online at www.ic3.gov. You’ll be asked to provide complete information about the crime as well as any additional relevant information.

Once you’ve reported the scam to authorities, you also want to take action against any other loss. IC3 recommends that victims take actions, such as contacting banks, credit card companies and/or the credit bureaus to block accounts, freeze accounts, dispute charges or attempt to recover lost funds.

Keep a close watch on your credit reports and consider using credit monitoring tools.

In February 2018, the Justice Department made a coordinated sweep of elder fraud cases that resulted in several initiatives to reduce the number of annual cases. [4] This included building local, state and federal capacity to fight elder abuse, supporting research to improve elder abuse policy and practice, and helping older victims and their families.

Each year the number of Internet crimes increases and scammers become more sophisticated, but spreading knowledge and awareness is one of the best ways to combat the issue. Arming yourself with a basic understanding of the dangers online can help you protect yoursel f from fraud.

Additional Resources

Sources:

1 Federal Trade Commission Latest Internet Crime Report Released

2 Pew Research Center Tech Adoption Climbs Among Older Adults

3 National Council on Aging Top 10 Financial Scams Targeting Seniors

4 United States Department of Justice Justice Department Coordinates Nationwide Elder Fraud Sweep of More Than 250 Defendants

While full-on Crayola-like green conjures less than complimentary connotations—green with envy; green around the gills; the grass is always greener—take the hue down a notch by mixing in some gray or black and the color yields a whole different experience. Deep-green hues evoke nature in a more meditative manner. Such elements feel nearly spiritual; think of jade, pines, and seaweed. Green is the color of the outdoors and it nurtures the soul. So, pull deep green-decor into your home.

One might balk at the thought of a green dresser, but Acerbis’s Storet subtly teases color out of a rich walnut. Think of it as a functional fern in the corner of your bedroom. Astreus Clarke’s Roebling lamp is a minimalist and earthy green marble alternative to a banker’s lamp with a lollipop-green glass shade. And, it looks as home in a library as on a nightstand. Sara Hayat’s Bevel sofa is a statement piece around which one builds a room; luscious green velvet upholstery is much more inviting than gray. Dive into deep green; we consider a timeless neutral.

Acerbis back in 1994, and the 150-plus-year-old Italian furniture firm recently updated the cabinet’s wood surface. That said, its defining feature is the glossy, lacquered horizontal moldings, which come in a dozen colors both serious and playful, including dark green. $19,173

Sara Hayat scoured industry sources near and far to find a fill that would give the Bevel a bit of bounce while ensuring its cushions would retain their pebble-like shape. Indeed, each velvet-upholstered seat cradles a person perfectly. As it should: It takes the team about a month to hand-stitch this low-slung belted beauty. $28,495

Minotti who passed away in August, played with the idea of balance in the Solid Steel coffee table, despite the heavy-metal inference of its moniker. Party-ready glossy and mirrored finishes belie the architectural geometry of the streamlined, staggered slabs. Even with its fashion-forward feel (or backward: the materials reference 1970s glamour), it evokes an unflinchingly Bauhaus sensibility. Price upon request

Astraeus Clarke found inspiration in N.Y.C. The Roebling table lamp takes its form, albeit loosely, from the Brooklyn Bridge and its name from the bridge’s engineers, John A. Roebling and his wife, Emma. The lamp’s deep-green marble pillars support a gable-shaped top that hides the light source. But there’s a twist: That top segment pivots 360 degrees, allowing the user to direct illumination as needed. $12,500

New Ravenna. Duo, a waterjet mosaic, features boxy, mustard-toned cross-stitches that punctuate a large, dark grid over elegant marble with green veining. The coastal Virginia–based company replicates the texture of stone that has been well-worn by salt air, ensuring your kitchen, bath, or patio looks suitably lived-in. $229 per square foot

This correlation between the average cost of living and credit card limit continues when we look at the 10 states with the lowest average credit card limit. In the chart below, the states marked with an asterisk are also on the list of states with the lowest cost of living.

State

Average Credit Card Limit

Average Credit Score

Mississippi*

$21,676

667

Arkansas

$24,570

683

West Virginia*

$24,684

687

Alabama*

$25,621

680

Louisiana

$25,781

677

Kentucky

$25,962

692

Oklahoma*

$26,041

682

Indiana*

$26,676

699

Idaho

$26,871

711

Iowa*

$27,052

720

Source: Experian, Wisevoter

How Are Credit Card Limits Determined?

Credit card companies use several factors to determine your limit, which they review periodically over time. Some factors count more than others, varying by the credit card issuer.

Your Credit Score

A higher credit score indicates you are more likely to pay your debts, which tells credit card issuers you are lower-risk. As a result, people with higher credit scores often have higher credit card limits.

According to FICO®, a variety of factors determine credit scores, including:

Payment history: Your payment history determines 35% of your credit score, which shows how likely you are to pay your debts on time.

Credit utilization rate: Your credit utilization rate is the ratio of the debt you owe to the total amount of credit available to you. You can factor your credit utilization rate by dividing your current balance by your total credit limit and multiplying the result by 100. A healthy credit utilization rate is considered anything below 30% —any higher and potential lenders may consider you overextended.

Length of credit history: The longer your credit history, the better picture a lender has of your risk level. A short history isn’t necessarily bad unless it contains a poor payment history and high utilization rate.

Recent hard inquiries: A hard inquiry is a record of a lender checking your credit. Too many hard inquiries in a short period can lower your credit score temporarily, so experts recommend six months between hard inquiries.

Credit card companies also use your credit score to determine your interest rate, so keeping an eye on your score with free credit reports is important.

Monthly Income

Credit card issuers want to know if you have monthly income to ensure you can pay your debts. The higher your monthly income, the more likely you are to get approved for a higher credit limit.

Monthly Expenses

Credit card companies look at your total monthly expenses, especially compared to your monthly income. Generally, they’ll look at your monthly housing costs (mortgage or rent), although they may also ask for information about other regular expenses such as utilities. Your monthly expenses are then compared to your monthly income to determine your credit card limit.

High monthly expenses won’t hurt your credit card limit as long as your monthly income is high enough to cover them.

Debt-to-Income Ratio

Credit card issuers also examine your debt-to-income ratio when determining your credit card limit. Experts consider anything under 36% to be a good debt-to-income ratio for a credit card.

To calculate your DTI ratio, divide your total recurring monthly debt (mortgage, auto loan, student loans, existing credit card debt, etc.) by your gross monthly income (how much you make before taxes) and multiply the answer by 100.

Your History with the Issuer

If you already have a positive credit history with the company issuing the credit card, they may be more likely to give you a higher credit limit. However, if they feel you have too many cards or a rocky credit history with them, they may issue a lower credit limit.

The Issuer’s Credit Approval Policies

Every credit card company wants to avoid risk and crafts a specific set of policies to determine how much credit to extend to a cardholder. Its policies may consider elements not listed here or weigh factors differently than another company, which is why credit card limits are not standard across companies.

Current Economic Outlook

When the economy is healthy, credit card companies may be more open to taking risks and offer higher credit card limits. However, when the economy is uncertain, such as during the pandemic, issuers are less likely to take risks, offering lower credit card limits for new cardholders.

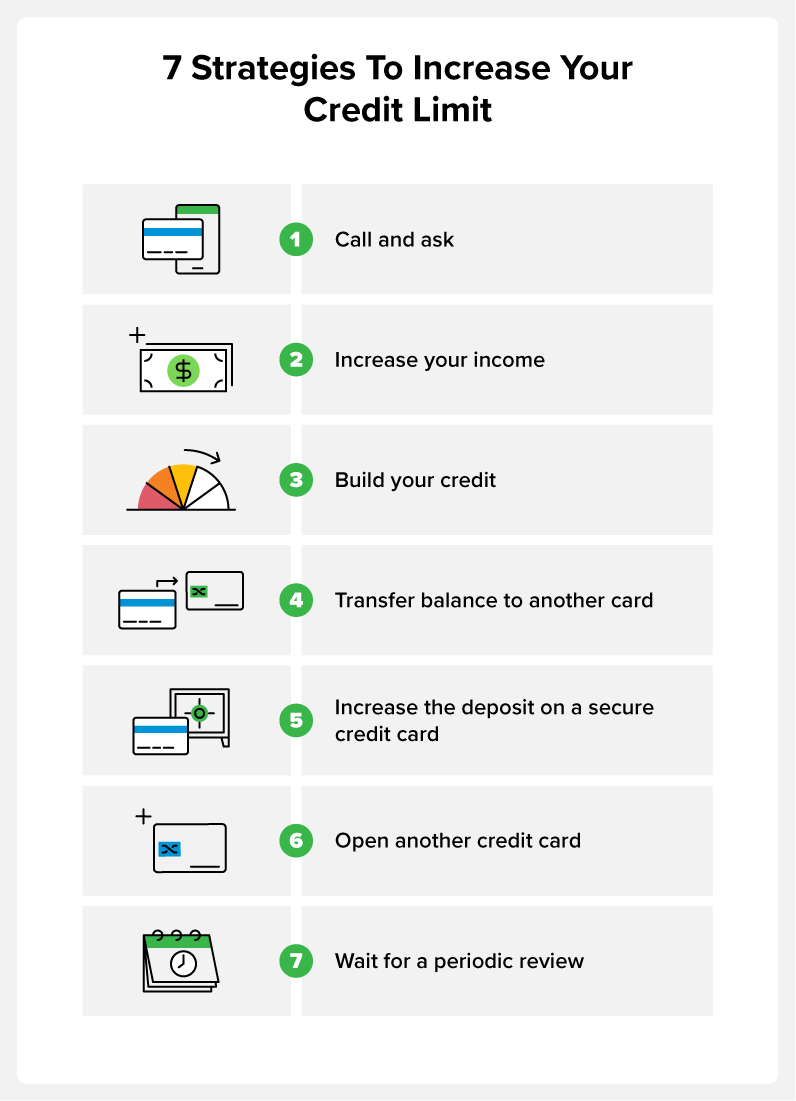

How to Get a Higher Credit Limit

A low credit card limit isn’t necessarily bad, but it can make getting approval for additional loans or credit challenging if your credit utilization rate is too high. It can also put large purchases, such as an appliance or unexpected car repair, out of reach.

To get a higher credit card limit:

Call your credit card issuer and ask for an increase. Call the customer service number on the back of your card and ask the representative for a higher credit card limit. Only consider this if you are trying to lower your credit utilization rate to raise your credit score. They look for six months of on-time payments and will ask for updates on your annual income, employment status, and monthly expenses before deciding.

Increase your income. Since monthly income is a factor in your credit limit, increasing your monthly income can boost your credit card limit. Ask for a raise at work, get a second job, or start a side hustle. When your credit card issuer sees you have more income, they may offer you a higher credit limit. You can update this information with them anytime by contacting them directly, or you can wait until they discover it in a periodic review of your status.

Build your credit. Pay your bills on time and pay down debt to increase your credit score. Over time, your credit score should increase, which can lead your credit card issuer to raise your credit limit.

Transfer the balance from one card to another. Some credit cards allow you to transfer debt from one account to another in a credit transfer. If you have multiple credit cards and one allows credit transfers, transfer the debt from one card to another. This won’t increase your credit card limit overall, but it can increase the amount of credit available on a specific card.

Increase your deposit on a secure credit card. If your card is a secured credit card, your credit card limit directly correlates to your security deposit. Add more to your security deposit, and you’ll have a higher credit card limit.

Open another credit card. This won’t increase the credit card limit on your current card, but it will expand how much credit is available to you. Avoid temporarily dinging your credit score by waiting six months between credit card applications.

Wait. Most credit card companies annually review your account, and as long as you pay your bills on time, they can likely naturally increase your credit card limit.

You can also always pay off purchases immediately rather than waiting until the end of your payment period to gain access to more credit without increasing your credit limit.

Credit scores strongly indicate what your potential credit card limit will be, so learn more about yours today. Before applying for a new credit card, get a sense of where you stand with a credit report card. Then use the tools and features in ExtraCredit to see where you need to work toward your credit goals to qualify for a higher credit card limit.

FAQ

Here are some answers to common questions regarding credit card limits.

What Happens if I Go Over My Credit Limit?

If you try to make a purchase over your credit limit, most credit card companies will deny the transaction. Some may allow the purchase but charge a fee, although most companies have abandoned this practice.

If I Request an Increase to My Credit Limit, Will That Impact My Credit Score?

When you request an increase to your credit card limit, your credit score may drop if your credit card issuer places a hard inquiry on your credit score. This can temporarily lower your credit score, and not all credit card companies do so.

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

A score of 850 is the highest credit score possible, and to achieve it you need a great credit payment history, low credit utilization rate, and credit lines that have been open for many years.

Many people are curious to know how to get the highest credit score possible, and while it’s an ambitious goal, do you actually need this high of a credit score? Although having the highest possible credit score is great, you don’t need the highest score to live a financially healthy life.

In this article, you’ll learn how to get the highest credit score as well as how credit score ranges work and the benefits of a high credit score.

Key Takeaways:

The highest credit score possible is 850 using the FICO® scoring model.

FICO’s credit scoring model ranges from 300 to 850, and anything over 740 is considered very good.

To achieve a perfect credit score, you need to make your payments on time, have both revolving and installment credit lines, and keep a low credit utilization rate.

The credit scoring factor that takes the most time is credit age, which means you need lines of credit that have been open for many years.

How Do You Get the Highest Credit Score?

If you’re trying to get the highest credit score of 850, you need to make all your payments on time and have a good mix of credit, a low utilization rate, and very old lines of credit. As mentioned earlier, this is an ambitious goal that not many people achieve. In fact, an Experian® report shows only 1.31% of people had perfect FICO credit scores as of Q3 2021.

A perfect credit score is also a moving target. Periodically, there are changes to what contributes to your credit score. For example, in 2017 there were major changes like how medical bills and public records are reported to the credit bureaus. Fortunately, these changes were in favor of the consumer, but there may be future changes that could lower your score.

FICO, the primary scoring model used by lenders, also regularly updates how it scores. Although it uses the same five factors, the latest FICO Score 10 has an updated predictive method it uses to provide consumers with a credit score.

The Credit Profile of People with a Perfect Credit Score

Should you decide to work toward a perfect credit score, it’s helpful to know what separates the average credit score from the perfect credit score. Obviously, those who manage to get a perfect credit score are doing something different than the average person. Experian regularly publishes credit and other financial data, and they analyzed data from the third quarter of 2021 to see what differentiates good credit scores from perfect credit scores.

Consumer Averages

Average for People With an 850 FICO Score

FICO® Score

714

850

FICO® Score

3.9

5.9

Credit card balance

$5,221

$2,558

Number of retail credit cards

3

4.2

Retail credit card balance

$1,046

$182

Auto loan balance

$20,987

$17,074

Personal loan balance

$17,064

$32,872

Mortgage balance

$220,380

$205,057

Non-mortgage balance

$21,539

$16,482

Total tradelines ever delinquent

1.8

0

As you can see, there’s quite a bit to learn from those with perfect credit scores. They have more credit cards than the average person, but they keep their credit card balance much lower. They also have lower balances on their auto loans and have no delinquencies on their credit report.

What Factors Affect Your Credit Score?

The information on your credit report is used to calculate your credit score, and there are different factors credit scoring companies consider when generating your score. Below are the five primary factors used by FICO. They’re weighted, which means some factors contribute more to your score than others:

Payment history (35%): how often you pay your bills on time

Credit utilization (30%): how much you owe vs. your available balance

Credit age (15%): how old your lines of credit are

Credit mix (10%): how many different types of lines of credit you have

New credit (10%): how often you apply for new lines of credit

Payment history and credit utilization account for 65% of your score, so you’ll want to focus on these areas by paying all your bills on time and keeping your utilization rate under 30%. Ideally, you’ll also want the longest credit history possible, which is why it’s good to open up lines of credit when you’re younger and keep the accounts open.

Your credit mix is a blend between revolving credit and installment credit. Revolving credit lines include credit cards and personal lines of credit, whereas installment credit includes auto loans and home loans.

What’s the Credit Score Range?

Credit scores range from 300 to 850. Within the overall range, different scores are considered poor, fair, good, very good, or excellent. Some lenders or services require a minimum credit score for applicants, so it’s helpful to know where you stand.

FICO Score Range

According to FICO is the primary scoring model lenders look at to determine your potential level of risk. Rather than looking at your entire credit report, this score gives lenders a rough idea of how well you pay your bills on time and how much experience you have managing lines of credit. Below is the FICO score range, but FICO also offers industry-specific scores for auto loans and other industries.

Poor: 300-579

Fair: 580-669

Good: 670-739

Very good: 740-799

Excellent: 800-850

VantageScore Range

VantageScore isn’t used as often as FICO, but some lenders will take this score into consideration. This scoring model was created by the three major credit bureaus in 2006 as an alternative to FICO. Not only is the VantageScore range different from FICO, but it also uses a slightly different scoring model.

Very poor: 300-499

Poor: 500-600

Fair: 601-660

Good: 661-780

Excellent: 781-850

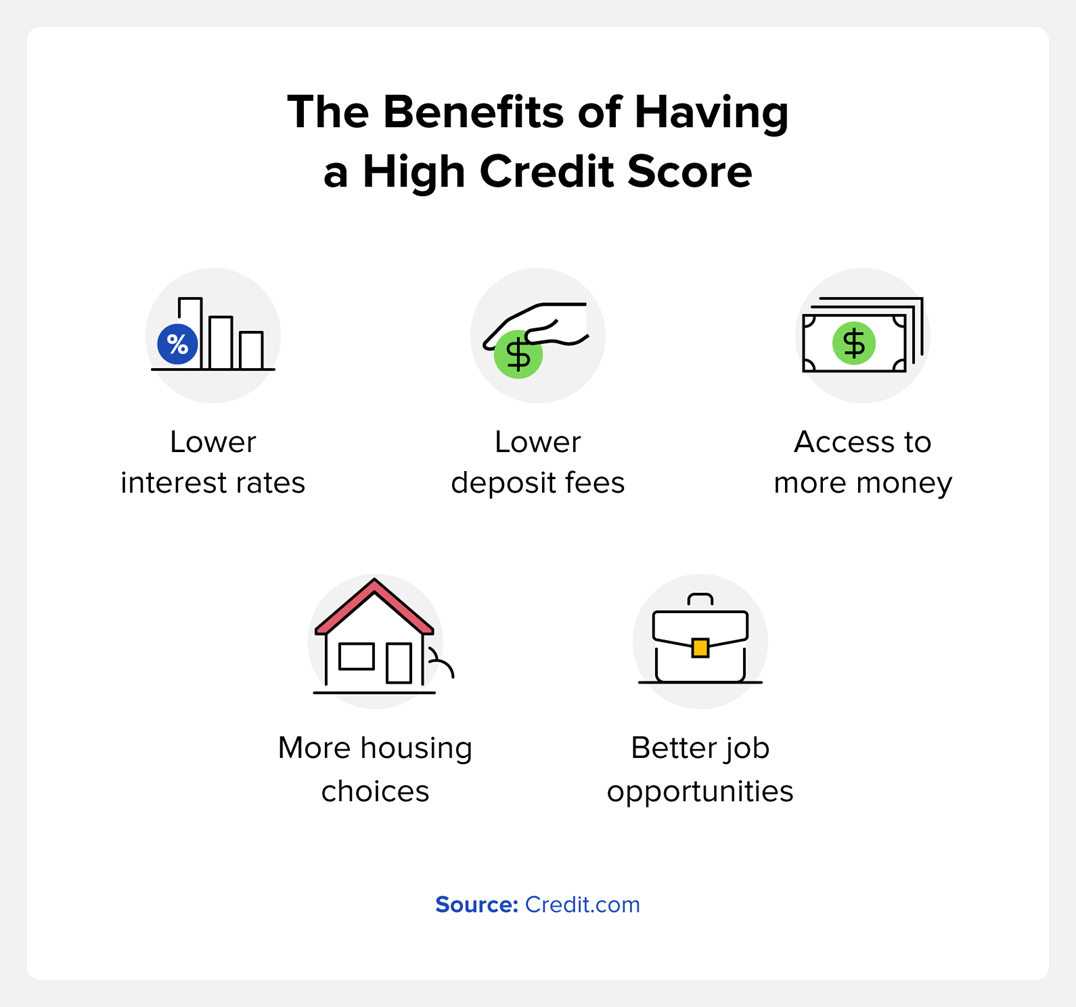

What Are the Benefits of a High Credit Score?

Although you may not be able to reach a perfect credit score for a while, there are many benefits to simply having a high credit score. Remember that a good credit score may be in the 600s, but you’ll receive more benefits as your score gets higher.

Some of the main benefits of having a high credit score include:

Lower interest rates: Loans and lines of credit come with interest charges that are a percentage of the overall cost. When you have a high credit score, these rates are much lower.

Lower deposit fees: When you sign up for certain services, like a new cell phone provider, they may check your credit score for a deposit. A higher score often means little to no deposit fee.

Access to more money: Should you need a loan, a higher credit score can get you approved for a larger amount assuming you have the income.

More housing choices: Whether you’re renting or buying, a good credit score gives you better options.

Better job opportunities: Some jobs check your credit as part of the application process, and a bad score may prevent you from getting hired.

Perfect Credit Score FAQ

Next, we answer some of the most commonly asked questions about achieving the perfect credit score.

Can You Get a 900 Credit Score?

No. The highest credit score possible is 850.

Is 770 a Good Credit Score?

A 770 credit score is good, but it’s technically considered a “very good” score in the FICO credit score range. A good score in that range is between 670 and 739.

Can You Have a Credit Score of 100?

No. The lowest credit score you can get is 300, but any score below 579 is considered “poor” in the FICO credit score range.

How Credit Monitoring and Additional Reporting Can Help Your Credit Score

If you’re looking to improve your credit score or even reach the perfect credit score of 850, a great place to start is with credit monitoring. When you have credit monitoring, you’re able to regularly check your credit score and be alerted when anything triggers a change to your score from your credit report.

For credit monitoring and a variety of other features, sign up for Credit.com’s ExtraCredit® program. You can also get a free credit report card to see where your current credit health stands and where you can improve.