Foreclosure filings were reported on 252,363 properties in June, a three percent decrease from May but a 53 percent increase from June 2007, RealtyTrac said today.

Per the report, one in every 501 households in the United States received a foreclosure filing during the month, with levels higher in the usual hotspots like Nevada, California, and Arizona.

RealtyTrac chief executive James J. Saccacio noted that June was the second straight month that more than a quarter million homes faced the prospect of foreclosure, and said recent data indicates that the epidemic hasn’t yet peaked.

“Foreclosure activity slipped 3 percent lower from the previous month, but the year-over-year increase of more than 50 percent indicates we have not yet reached the top of this foreclosure cycle,” he said.

“Bank repossessions, or REOs, continue to increase at a much faster pace than default notices or auction notices. REOs in June were up 171 percent from a year ago, while default notices were up 38 percent and auction notices were up 22 percent over the same time period.”

Essentially, properties that began the foreclosure process months ago are now owned by the issuing bank or mortgage lender, while those beginning the foreclosure process have slowed, partially because of new laws that protect at-risk homeowners.

For example, the state of Massachusetts recently passed legislation that extends the time period mortgage lenders must wait before initiating foreclosure proceedings from 30 to 90 days.

That has led to a precipitous drop in foreclosure starts, but did little to slow the number of foreclosure deeds, the final step of the foreclosure process, which hit an all-time high in the state during May.

This logic assumes that an artificial slowing in foreclosure filings could actually extend the mortgage crisis, and lead to a bump later down the road once these at-risk homeowners are no longer protected by such temporary laws, because as we all know, some foreclosures are simply not avoidable.

A number of other states and cities have implemented similar initiatives over the past few months that simply slow the process, though it’s unclear if they provide any meaningful long-term solution.

You’ve done your research, checked your credit reports to make sure they’re accurate, and you’re ready to get serious about buying a car. You feel more than ready to sign on the dotted line and drive home in your new ride.

It could happen. Or, you could drive home in your old vehicle, kicking yourself for having forgotten one of the documents you need to finalize the purchase. Here’s how to lay the groundwork for getting the deal done on the day you’re ready to buy.

Four Steps to Prepare to Buy a Car

Step 1:

You’ll want to talk to your insurance agent about what it will cost to insure the make and model you are considering buying. You don’t want that figure to be a surprise, and you also want to find out how soon you will need to notify your insurer you have the new vehicle.

Step 2:

Talk to your bank or credit union and get pre-approved for the loan you’ll need—and do this close to your planned purchase date. You may get something resembling a blank check (up to a certain maximum) that must be signed by you and the dealer. By getting pre-approved, you will know the total loan amount and interest rate you qualify for. Even if you plan to finance at the dealer, it can’t hurt to come in with a pre-approval; you are far less likely to agree to a longer term or higher interest rate because you really want to drive that new car home today. It can also help you stay within your budget by serving as a solid reminder of how much you planned to spend and how long you were willing to make payments — before the showroom floor made it so hard to remember.

Get matched with a personal

loan that’s right for you today.

Make sure you have your driver’s license and proof of auto insurance with you. You shouldn’t be driving without these documents anyway.

Step 4:

Obvious as this seems, be sure you have a way of funding your down payment. If it’s not cash, make sure the dealer accepts the form of payment you’re planning to use. (If you forget to do this, you would not be the first, but that would be little consolation.)

Expert Tip: Be cautious about having your credit pulled unnecessarily. Each inquiry made for the purpose of extending credit can cause a small, temporary decrease in your credit score. And while inquiries for the purpose of getting a car loan made in a two-week period should count as only one entry, we’ve heard from consumers who have told us their credit scores dropped as the result of multiple auto loan inquiries. Some dealerships now ask customers to fill out a credit application even before a test drive, and there are reports that some have checked credit without customer consent. It can help to keep an eye on your credit through this process for this reason. Hard inquiries into your credit require permission, and it can be illegal for your credit to be pulled without your approval in this manner. You can get a credit report summary and two credit scores, updated monthly for free on Credit.com, to track your standing.

Can You Purchase a Car with a Credit Card?

Speaking of your down payment, you may have wondered if this can be charged to a credit card — or if the entire car can be paid that way. The answer is yes and no. It is possible that the dealership will not accept a credit card payment for the car, as this can come with large merchant fees that lower their profits. However, if your credit is in good standing, then it is still possible.

A better option would be to use your credit card for just the down payment. Not only is this better for your credit, since using all of your available $10,000–$15,000 credit limit can damage your credit score, but it’s more likely to be accepted by the dealer.

Finally, you’ll want to use a credit card that has excellent benefits. An appropriate credit card can earn you big rewards on your car purchase or other auto-related purchases. We have given you a couple examples of worthy rewards cards below.

Planning to Trade In Your Car? Don’t Forget These Items for the Dealership

If you plan to trade in a car, you have a bit more to do.

You will need to bring the following items to the dealership:

Your car’s certificate of title (If it has gone missing, your state department of motor vehicles can tell you how to get it replaced.)

The car’s current registration

Your car keys and the owner’s manual

Your account number or a payment stub if you still have a car loan (We’re going to hope that if this is the case, your car is worth more than you owe.)

A clean car, paying special attention to areas out of sight but convenient for stashing things: under seats, over the visors, in the glovebox and in every corner of the trunk

Besides a new car, expect to come home with a good bit of paperwork. Pay special attention to the purchase and sale agreement. You will need the information there to get or update your insurance — and you might even need it at tax time next year if you bought a car that qualifies for a tax credit.

What Do I Need to Apply for an Auto Loan?

While you won’t need to drive all the way to a dealership to get an auto loan (you can simply apply online), you will still need some important documents in front of you to easily fill out the application.

What do you need?

Proof of identity through an ID or passport

Your credit report, which the lender can pull using your name, address, date of birth and social security number

A valid state-issued driver’s license

Proof of monthly income through pay stubs or social security income receipts

Proof of residence through mortgage statements or utility bills

Contact information for personal references (note: this may not be required)

Vehicle make and model

Proof of car insurance

Payment type (cash, credit, debit, etc.)

Your car’s registration if you are trading in the vehicle

The list is rather long, but having each document will speed up the process and prevent you from going back and forth between your files.

Get Your Auto Loan and Car with the Help of Credit.com

Make sure that you can qualify for an auto loan by checking your free credit score, provided through Experian. From there, you can apply for your auto loan with confidence and compare credit cards that can help you finance your new car.

Frequently Asked Questions

Will my credit rating affect my auto insurance rates?

You should choose auto insurance coverage based on your credit rating and overall coverage needs. Check out Credit.com for car insurance quotes and to compare rates.

How can I find a credit card with a low interest rate to charge my car purchase?

We don’t recommend that you put your entire purchase onto your credit card, but there are cards with low APR or no APR for up to 15 months available to compare. If you can pay off the remaining balance during this period, then these credit cards may be for you.

How good should my credit be to get a credit card that is appropriate for a car purchase?

You mentioned that hard inquiries can affect my credit score. What is a hard inquiry?

A hard inquiry is a credit check that indicates you have applied for credit, usually through a loan. Each time a hard inquiry is pulled from a different lender, your credit score can drop by up to 10 points, because it indicates that a lender has reviewed your credit and that you are trying to open up a new line of credit.

Note: At publishing time, the Chase Sapphire Preferred® Card and American Express Green card are offered through Credit.com product pages, and Credit.com is compensated if our users apply and ultimately sign up for this card. This content is not provided by the card issuer(s). Any opinions expressed are those of Credit.com alone, and have not been reviewed, approved or otherwise endorsed by the issuer(s).

Note: It’s important to remember that interest rates, fees and terms for credit cards, loans and other financial products frequently change. As a result, rates, fees and terms for credit cards, loans and other products cited in these articles may have changed since the date of publication. Please be sure to verify current rates, fees and terms with credit card issuers, banks or other financial institutions directly.

A FAFSA is an application for financial aid that determines your eligibility. This application will not appear on your credit report, and does not affect your credit score.

Congratulations on your high school graduation! You put in a lot of hard work to get that degree, and you deserve to celebrate. This might be your last summer of “freedom,” but that doesn’t mean you don’t have any responsibilities to take care of.

If you haven’t submitted the FAFSA—a crucial step toward receiving financial aid or taking out student loans—now is the time to buckle down and get to work. Even if you don’t think you’ll qualify for financial aid, we recommend getting familiar with the FAFSA, understanding its potential impacts on your credit score and financial future, and submitting an application.

Here’s what we’ll cover in this piece:

What Is the FAFSA?

FAFSA stands for Free Application for Federal Student Aid. It’s a one-stop application for all federal student loans, grants, work-study opportunities, and other financial aid sponsored by the US government. In order to qualify for federal financial aid, you must fill out a FAFSA.

Filling out a FAFSA is free, and the federal government provides more than $112 billion in FAFSA funds each year. States and other aid organizations may require you to fill out a FAFSA as part of their loan, scholarship, or grant applications as well.

Get matched with a personal

loan that’s right for you today.

Learn

more

Does the FAFSA Affect Your Credit Score?

The FAFSA is just an application for financial aid, which means it won’t affect your credit scores. You complete it to find out what type of financial aid you might be eligible for. The fact that you completed the FAFSA never shows up on your credit report—it’s not considered a credit inquiry—so it can’t impact your credit score.

Does Financial Aid Show Up on Your Credit Report?

The results of your FAFSA could impact your score depending on how you handle them. Financial aid that you don’t have to pay back, such as scholarship or grant money, doesn’t hit your credit report. It’s not debt, so there’s no reason for it to. But student loans can show up on your credit report.

Student loans, whether you qualified for them via the FAFSA or took out private student loans, are a form of debt. They may be reported to the credit bureaus. Paying those loans on time and as agreed could help improve your credit—and this is one way you can start building credit.

Missing payments or defaulting on student loans can hurt your credit. In this way, the outcome of the FAFSA could have an impact on your credit score.

Who Can Complete the FAFSA?

Anyone who is planning to attend a college or university in the next academic year can complete the FAFSA to find out what they qualify for. Completing the application isn’t a guarantee of any financial aid and it doesn’t create an obligation on your part—other than to tell the truth on the form. You may want to complete it each year to see what you qualify for.

Parents of dependent students can also complete the FAFSA. In these cases, it would be the parental household income that would be considered in determining what someone is eligible for.

The federal government does not consider credit scores or credit history when determining what someone is eligible for. The financial aid is decided mainly on financial need and income. You do have to meet some other requirements, such as having a valid Social Security number.

When Should You Complete the FAFSA?

The deadline for the FAFSA differs for each academic year, however, many schools have their own deadlines, as do states. They may process some financial aid based in part on the FAFSA. A good rule of thumb would be to complete the application as soon after October 1 as possible, to ensure you’re early enough to be eligible for the highest number of opportunities.

What Do You Need to Complete the FAFSA?

First, you have to create an FSA account. This is the account you use to complete the FAFSA, review any requests for additional information, and see what student aid you might be eligible for. Once you have an account, you will need the following to complete the application:

Your Social Security number and driver’s license number

Tax records for you and your parent for the qualifying year—typically it’s two years before the academic year in question

Any records of untaxed income and assets

A list of all the schools you want to apply to, as you’ll have to add them to the FAFSA

Can You Modify a FAFSA?

If you make a mistake or information changes, you can modify the FAFSA. If your income situation has changed drastically and is not well reflected by the tax return required by this year’s FAFSA, you can speak to the financial aid office at the school you’re attending or applied to. Those offices sometimes have options for addressing this issue.

Do You Have to Pay Back FAFSA Money?

Whether or not you have to pay back FAFSA money depends on the type of aid you receive. Certain need-based grants don’t have to be paid back. Student loans do.

What if You Don’t Qualify for FAFSA Money?

Federal student aid isn’t the only way to pay for college. For some, private student loans can be an option. Check out the student loan marketplace at Credit.com to see some of your options. And if you get some FAFSA money but it’s not enough to cover all your college expenses, you might consider applying for a college student credit card. Use it responsibly to help build your credit as you go through school.

Revvi Visa® Credit Card

Earn 1% Cash Back Rewards on All Purchases with Revvi!

The Perfect Card for Not-So-Perfect Credit

If approved, pay the $95 Program Fee to open your account

Fast and easy application process with a response provided in seconds!

Reports to All Three Major Bureaus to Build Your Credit History

Eligible for a Credit Line Increase after 12 months of on-time payments!

Choose between 2 free card designs and 4 Premium designs

With most of the year under our belt, the holiday season is just around the corner. No matter what you celebrate, this season is full of food, celebrating and spending time with loved ones.

While you’re hard at work prepping for the holiday season, scammers are too. A survey conducted by Experian found that a full 1 in 4. Americans have been a victim of identity theft or fraud in the holiday season. If you’re worried about scammers this year, don’t worry—we’ve got tips on how to look for holiday shopping scams this season.

When the pandemic hit in early 2020, COVID-19 scams became a popular method for criminals to get access to your information and steal your identity. However, the holidays are when these scammers go into overdrive, meaning it’s important to be extra cautious as you do your online shopping and holiday giving. Here are some of the most common holiday shopping scams to be aware of.

Illegitimate Charities

Many people use the holidays as a reason to be a bit more generous, but be careful before you make that donation. Many scammers create fake charities in an attempt to get you to donate. They get your money—and possibly access to your identity info—and no good ever comes from that generosity.

Check for social media presence, news stories, financial records and proof that any charity you’re considering donating to actually exists and has a good reputation.

I just watched a documentary on the dark web, and I will never feel safe using my credit card again!

Luckily I don’t have to worry about that. I have ExtraCredit, so I get $1,000,000 ID protection and dark web scans.

I need that peace of mind in my life. What else do you get with ExtraCredit?

It’s basically everything my credit needs. I get 28 FICO® scores, rent and utility reporting, cash rewards and even a discount to one of the leaders in credit repair.

It’s settled; I’m getting ExtraCredit tonight. Totally unrelated, but any suggestions for my new fear of sharks? I watched that documentary too.

…we live in Oklahoma.

Fake Online Stores

Online shopping is a convenient way to check off all the items on your list without having to actually brave the holiday crowds. However, it’s important to ensure that the sites you’re shopping from are actually legitimate. Scammers create fake online storefronts—sometimes even mimicking well-known retailers—and you don’t know it’s fake until the merchandise never comes or you start seeing evidence of identity fraud.

Empty Gift Cards

Gift cards are the perfect choice if you’re not sure what someone on your gift-giving list wants or if they like to pick out items themselves. But selling gift cards that have a $0 balance or have already expired is a common and remarkably easy scam. This happens most often on local sales sites, such as Craigslist and Facebook Marketplace.

Email Scams

Have you ever gotten an email about something you bought online—but you never actually purchased anything from that retailer? Maybe the email said you needed to reset your password or gave you a link to track your package. These are phishing email scams designed to get you to enter your personal info so scammers can use it for identity theft.

Shipping Problems

One of the biggest worries that comes with online shopping—especially with the supply chain issues that have come as a result of the COVID-19 pandemic—is whether the gifts will arrive on time. Criminals capitalize on this fear by sending out emails, texts and other communications letting you know there’s been an issue with your package. You’re asked to provide personal information such as your address, credit card info and birth date to confirm your order, but all you’re really doing is giving scammers the information they need to steal your identity.

While the holidays are a common time for shopping scams, it doesn’t mean there’s nothing you can do about it. Learn what to look for and how to protect yourself from identity theft with these tips.

1. Pay Attention to Website URLs

Online searches can lead you to scammer-run websites that unleash computer malware or collect credit card numbers for identity theft. Carefully read website domain names. Watch for unfamiliar vendors or missing letters, misspellings or other tweaks to the name of a legitimate company. Pay special attention to the last letters. For example, tiffanyco.mn indicates a Mongolia-based website, not the legitimate website for Tiffany & Co., tiffany.com.

2. Make Sure the Site Is Legitimate

Before ordering, check the “Contact Us” page for a phone number and physical address and the “Terms and Conditions” link detailing return policies and such. Unlike legitimate vendors, bogus websites are less likely to post these—or they’ll provide them in a suspicious manner, such as via a faxed request only.

How do you know if a holiday website is legit? Check the Better Business Bureau as well as Facebook and Google reviews before you buy from a new place. If the business doesn’t have any social media or online presence other than the website, that’s a red flag.

3. Only Buy Gift Cards From Retailers

Buy gift cards directly from the retailer and avoid shopping for discount gift cards through local swap sites. You may also want to buy gift cards online or from the checkout instead of the display racks, which are less secure. Fraudsters can peel off stickers to glean gift card codes, replace them in envelopes and wait for an unsuspecting shopper to buy them. Once purchased and activated, they enter stolen codes at the retailer’s website to make online purchases—leaving the intended recipient with a useless card.

4. Look for HTTPS Sites

When buying online, check the URL to see whether the website starts with “http://” or “https://.” The “S” is for “secure” and is your best bet for safe shopping. Some legitimate retailers may use http sites, but your information is much more vulnerable to attack in this case because it’s easier for hackers to get to it. Even with a secure page, avoid using public Wi-Fi hotspots for online shopping or other financial transactions.

5. Use Prepaid Gift Cards for Online Shopping

Consider buying prepaid cards for online shopping instead of using your actual debit or credit card. These cards are often reloadable for ease of use, and if your information does happen to be stolen, hackers will only have access to the amount on the card and not your entire bank account.

6. Take Care on Craigslist

On Craigslist or when answering local classified ads, deal only with sellers who provide a phone number you can verify. Don’t rely solely on email correspondence. Assume any request for wire-transfer payment is a scam, and be suspicious of prepaid debit card transactions. Using PayPal or a credit card is your safest bets.

7. Avoid Deals That Seem Too Good to Be True

Stay clear of prices from private sellers that seem too good to be true or are tied to hard-luck stories, such as a need to sell quickly because of divorce or military deployment. No one is selling the latest gaming console for only $50, no matter how hard up they are. These are common scams to get advance payment—and you’ll likely get no merchandise.

8. Don’t Open Holiday E-Cards From People You Don’t Know

Delete E-Cards or general holiday emails if you don’t know the sender. These mass-sent greetings likely contain malware. Legitimate card notifications should include a confirmation code to safely open the card at the issuing website.

9. Beware of Undeliverable Package Emails

Avoid emails claiming that FedEx, UPS, DHL or the U.S. Postal Service has an undeliverable package with links for details. The links will install malware that can log keystrokes to steal computer files and passwords. Unless you previously provided an email address, courier services won’t contact you this way. This scam baits you to call for details—at which point you’ll be tricked into making an expensive overseas call or revealing your personal and financial information. Look up the callback number yourself if you’re curious.

Gearing up for the holidays? Go ahead and enjoy your holiday shopping this year. Just be a little careful—keep an eye out for anything suspicious and make sure that any website you buy from is legitimate.

If you’re worried that you might already be a victim of identity theft or just want to keep a closer eye on your credit, ExtraCredit can help you know what’s going on with your credit report and spot identity theft as soon as it happens.

However, the total completed loan workouts (repayment plans, loan deferrals/partial claims, loan modifications) from 2020 and onward that were current decreased by three basis points to 73.43% in August. “While there was a monthly decline in the performance of post-forbearance workouts in August, overall mortgage servicing portfolios remain resilient,” Walsh noted in the report. “Compared … [Read more…]

Many people use the terms ATM card and debit card interchangeably, but these aren’t actually the same thing. To understand whether an ATM card is also a debit card, you have to know a bit about the history of these cards and what they’re used for.

We’ve got the details on ATM cards vs. debit cards below. Find out the difference and get answers to some common debit and ATM questions.

What Is the Difference Between ATM and Debit Cards?

ATM and debit cards look quite similar. They resemble credit cards and typically have bars you can swipe. They may also have secure chips. However, they aren’t the same and don’t serve the same purpose.

If the question is which came first, the ATM or debit card, the answer is ATM card. According to a report from the World Economic Forum, the patent for an early cash dispenser was filed back in 1960. ATMs became operational later that decade, along with automated teller machine cards—ATM cards. The first official debit card didn’t debut until 1972. It was called the ATM account debit card from City National Bank of Cleveland.

ATM cards were originally designed to do one thing. Instead of going to the bank to get money, you could take cash out of your checking account via a machine. These machines were connected by regional networks. While the cards were issued by banks, they could be used to withdraw money anywhere there was a machine for a potential fee.

As such, ATM cards are cards that are only used to interact at ATMs. Debit cards, on the other hand, have a wider function.

In the past, ATM networks began looking for new revenue streams. They started creating relationships with retailers and eventually joined forces with the credit card networks to create what we now know as debit cards. Debit cards can be used like credit cards at checkouts in person and online.

Most banks also issue debit cards that can act as ATM cards. However, an ATM-only card can’t act as a debit card. Debit cards have Mastercard or Visa logos on them, indicating which network they run on. ATM cards don’t have these logos.

Find Your Card Now

Privacy Policy

Pros and Cons of an ATM Card

Some banks will still issue an ATM-only card if an account holder asks for one. These cards can only be used at automatic teller machines.

Pros of ATM cards include:

You can get cash at any machine, creating flexibility for money management.

You can’t swipe the card to pay for goods and services, which can help reduce impulse purchases.

They may be a good tool to go along with a cash envelope budget system.

The main disadvantage of an ATM card is its limitation. You can’t use it to pay for goods and services. If you don’t have another payment method in your wallet, this can lead to you having to find an ATM and get cash anytime you want to purchase something.

Pros and Cons of a Debit Card

Most checking accounts come with the option for a debit card, and some banks issue one automatically. You can also get prepaid debit cards.

Pros of debit cards include:

Flexibility, as you can use your card at ATMs and pay for goods and services with it anywhere Visa or Mastercard is accepted

You may be able to swipe your debit card as a credit card for added protection

Options for managing your budget, as you can set limits on your debit card or get a prepaid debit card that limits how much you can spend

They’re a common and recognized financial tool that won’t raise eyebrows when you use them

The biggest con of a debit card is that it’s tied to your bank account. This can lead to impulse spending that brings your account balance low, even if you didn’t budget for the spending. You may also find your debit card is limited by daily or individual purchase amounts.

FAQS

Can you use ATM cards at all ATMs?

Yes, you can generally use an ATM card at any automatic teller machine. This means you don’t have to look for an ATM that’s associated with your financial institution.

Are there fees for using different ATM cards at different brand ATMs?

Yes, there are fees for using ATM cards that aren’t associated with your financial institution or bank. Your bank might charge a fee for this activity, and you may also pay a fee to the ATM company.

What happens when an ATM transaction fails?

ATM transactions can fail for a few reasons. When they do, the machine notifies you of the failure and the reason. Some common reasons include:

You don’t have enough money in your account to cover the withdrawal.

The machine experienced a malfunction and couldn’t complete the process.

You entered an incorrect PIN.

Your card couldn’t be read by the ATM reader.

In cases where a technical malfunction or incorrect PIN entry caused the transaction to fail, you may be able to try again.

Are there any limits to how much can be withdrawn with debit and ATM cards?

Yes, banks set limitations on how much can be withdrawn with debit and ATM cards. There may be a limitation on how much you can withdraw in a single transaction. Daily limitations also usually exist. For example, your bank may only allow you to withdraw $300 at a time or $1,000 in a single day. No standards exist for these limitations—each financial institution decides for itself.

Which Is Right for You?

Ultimately, you have to decide whether an ATM or debit card is right for you. Take into account your own budget and the way you spend money. You should also consider what financial habits you need support for and which type of card would help.

You can get an apartment with bad credit, but it may take some strategizing. Apartment applicants with low credit scores can boost their odds by applying with a cosigner, paying more upfront, offering references, or changing the type of units they apply to.

In today’s housing market, you want every possible advantage on a rental application. While letters of recommendation and a solid rental history will get you far, more and more landlords want a high credit score. As a result, it isn’t uncommon to ask if you can get an apartment with bad credit.

While it takes some strategizing, you can get an apartment with low credit. To help you along, we’ll explain how credit impacts your application, explain steps you can take to compensate for low credit, and share tips on boosting your score.

How Credit Impacts Getting Approved for an Apartment

Many landlords and renters run a credit check as part of their rental application process. Like lenders, landlords check your credit to see if you can pay your bills on time. Because renting is an investment, property owners want to minimize risk. So, they assume tenants with high credit are more likely to pay their bills on time.

Remember that your credit score isn’t the only factor on a rental application. While a high score helps, the details on your credit report matter, too. How you got a high or low score can sway property managers one way or the other.

What Credit Score Do You Need to Rent an Apartment?

The score you need depends on the unit. Some rental companies provide an ideal range for their listings. A score of 620 or higher will generally keep landlords from denying your rental application. However, some landlords will expect more, while others don’t look at your score at all.

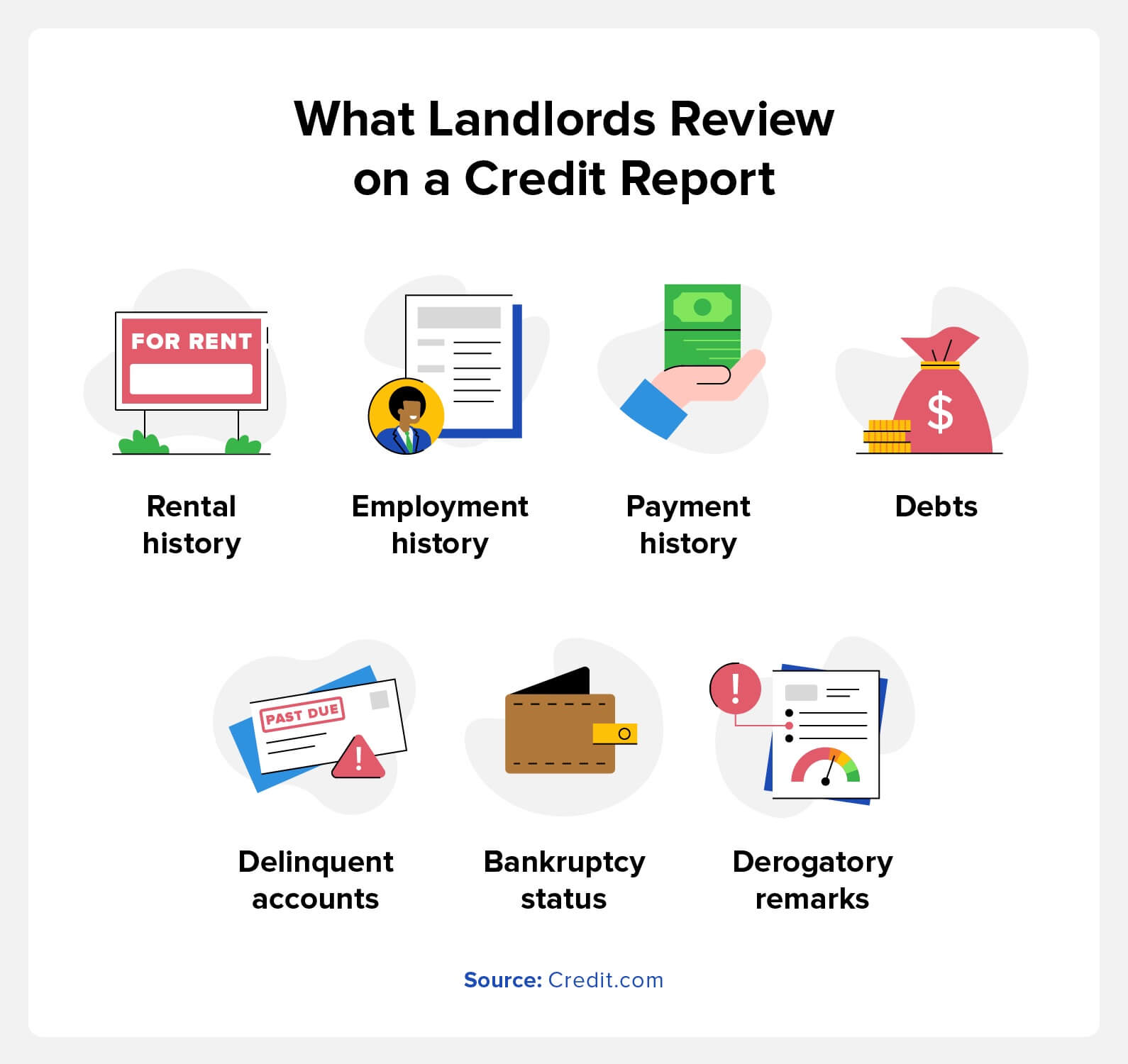

What Do Landlords Look for on a Credit Report?

Renters may treat your credit score like a headline, but there’s more to a credit report than a number. Credit reports tell a story about your spending habits and income. To help landlords pick reliable tenants, a rental credit check includes:

Rental history: Some landlords report rent payments to credit bureaus. As a result, evictions, broken leases, and late or missing payments may appear.

Employment history: Current or past employers may show up on a credit report. Typically, they only appear if you listed them on a credit card application or loan.

Payment history: Credit reports show your history of payments to lenders. Late or missing payments will lower your score and work against your rental application.

Debts: Current and past debts show up on your credit report. By providing payslips, landlords can calculate your debt-to-income ratio. If you make enough to repay your debts responsibly, that improves your application.

Delinquent or collections accounts: An account is delinquent if you miss a payment due date. If you miss enough payments for lenders to transfer your account to a collection agency or sell it to a debt buyer, it becomes a collections account. Both of these hurt your credit score.

Bankruptcy status: Bankruptcy filings will affect your credit score. Landlords may take recent bankruptcies as a sign that you’re a high-risk tenant.

Derogatory remarks: These remarks refer to negative items on your credit report. They include auto repossessions or foreclosures. They hurt your score and hamper a rental application.

Landlords gauge the risk they pose by looking at how applicants spend their money. Someone with a high income but a history of late payments may not make the cut. On the other hand, someone who filed for bankruptcy years ago may be more responsible now.

How to Get an Apartment with Bad Credit

While a low score sets you back, you can learn how to get approved for an apartment with low credit. By following these methods, you can get a leg up in rental applications:

Make an Upfront Payment

Putting down more money upfront can give you an edge on rental applications. Landlords will usually request a security deposit or the first and last month’s rent upfront. To sway a landlord’s opinion, offer the first three months’ rent or put down a higher security deposit.

At the end of the day, renting is an investment. If you can show your landlord that you’ll give them a reliable ROI, it’s all the more likely they’ll accept you. As a bonus, paying more in advance saves you a financial burden for the next few months.

Find a Guarantor or Cosigner for Your Apartment

If a landlord can’t trust you to make payments, you can get someone to sign your lease with you. Someone with a great credit score who signs on with you can assuage a property manager’s worries. However, remember that the person who helps you takes on financial risk. You have two options for this approach:

Cosignerssign a rental agreement with you and share the financial responsibility for it. They must do so on your behalf if you can’t or won’t pay rent.

Guarantors share cosigners’ responsibilities, but they have fewer rights. More specifically, they vouch for you and can make payments on your behalf. However, they aren’t entitled to reside in your unit.

Offer References and Supporting Documents

While credit reports outline your financial history, you aren’t the sum of your spending decisions. You can offer other documents to show your responsibility in an apartment application. Additionally, these documents can prove you can pay rent each month. Some examples of supporting documents include:

Payslips: Offer pay stubs that show you make enough money to pay rent each month.

Letters of recommendation: Reference letters from a friend or employer can attest to your character and responsibility.

Proof of reliable rental history: Account statements and landlord testimonials can prove you always pay rent on time.

A snapshot of your savings account: If all else fails, you can show landlords you have the money to make rent. Be sure to censor sensitive information on your snapshot.

Utility payments: A history of on-time utility payments shows your trustworthiness.

Find Apartments to Rent with No Credit Check

While credit checks are common, not all landlords require one. While these properties aren’t the most competitive, that isn’t always a problem. Apartments with no credit check tend to cost less than ones with one.

If you’re looking for another option, some landlords advertise units with low credit requirements. Again, these properties set a low credit requirement for a reason. That said, if you inspect the unit and it looks good, this route can save you a headache. As you live in low-credit apartments, you can build your score for future applications.

Adjust Your Expectations

If you can’t get around a credit check, reassess the kinds of apartments you can apply for. This isn’t to say you should only apply to units in poor condition. Instead, consider what you’re willing to compromise on. You may have an easier time qualifying for an apartment:

Farther away from your work or downtown area

Without amenities like a gym or pool

That doesn’t include parking

With less square footage than you’d prefer

If you apply with a roommate

Bear in mind that compromising on these points means the apartment may cost less. While living in a less-than-ideal unit, you can save and rebuild your credit while renting. When it comes time to look for a new apartment, you’ll have better odds of getting the one you want.

Tips to Raise Your Credit Before Renting an Apartment

If you plan to send rental applications down the line, you should work to improve your credit. Bear in mind that increasing your credit score takes time. To see a major change, expect months or even a year of work. In that time, follow these tips to improve your credit:

Pay Your Bills on Time

A person’s payment history can make or break their credit score. Central to that payment history: whether you paid your bills on time. Making timely and consistent payments plays a big role in improving your credit score. On top of that, timely payments prove your reliability to a landlord, boosting your chance of getting approved.

Pay Down Any Debt

Paying down debts is one of the best ways to improve your credit score. For this reason, someone who takes on and pays off debt won’t get punished for the debt they take on. Paying off debts shows your fiscal responsibility and proves your finances are on an upward trajectory.

Paying off any kind of debt can improve your score. The main ones to look out for include:

Credit card debt

Student loans

Medical debt

Auto loans

Become an Authorized User for Credit Piggybacking

If you don’t have the resources to boost your credit alone, you can try credit piggybacking. Credit piggybacking lets you benefit from a friend or family member who pays down their debts. By becoming an authorized user on their account, your credit report reflects their payoffs.

You can break the process into a few steps:

Find a friend or family member you trust to spend responsibly.

Become an authorized user on one of their credit cards or lines of credit.

As they pay down their debts, this will show up on your credit report.

By piggybacking on their credit payoffs, your score will improve.

Dispute Credit Report Errors

Sometimes, a low credit score isn’t your fault. Credit reporting errors can come from major credit reporting agencies or the companies giving them information. Credit reporting errors aren’t uncommon, so you should review your report for issues.

Credit reports may contain errors related to:

Accounts held by another person with a similar name to you

Accounts opened by fraudsters who committed identity theft

Closed accounts that still read as open

Accounts incorrectly labeled as delinquent or in collections

Payments that don’t get reflected in your report

Multiple listings of the same debt

Accounts with inaccurate balances or credit limits

To dispute credit report errors, contact the credit bureaus and the company that reported inaccurate information to them. You want to provide supporting documentation that proves the report contains errors. While you can send a dispute by phone, this doesn’t leave a paper trail. Instead, mail a dispute letter or use an online form.

FAQs on Renting an Apartment with Bad Credit

You may still have questions about getting approved for an apartment. To help you out, we’ve answered FAQs on renting apartments with bad credit.

Is 500 a High Enough Credit Score for an Apartment?

You can rent an apartment with a credit score of 500. While it might take you out of the running for expensive units, you should still have a good chance of renting:

Apartments with low credit requirements

Apartments with no credit requirements

Apartments you apply to with a cosigner or roommate.

Can I Reapply for an Apartment After I Get Denied for Bad Credit?

You can apply for the same apartment after getting denied on your first attempt. That said, some renters may throw out your application or ignore it. If you reapply, try to improve your credit and finances between applications.

Do Landlords Need Permission to Run a Credit Check?

Landlords need your permission to run a credit check. The Fair Credit Reporting Act calls rental applications a “permissible purpose.” This gives them the right to view your credit. However, that doesn’t mean landlords can check your score without your consent.

Improve Your Credit for an Apartment with Credit.com

Managing apartment applications is hard enough, even without a low credit score. However, you can get an apartment with bad credit by following the right steps. You’ll see more housing opportunities by learning how credit works, reviewing strategies for getting an apartment with low credit, and following tips to boost your score.

If you’d like a way to streamline raising your credit for rental applications, Credit.com can help. Our rent and utility reporting services ensure that your on-time payment gets reflected on your report. Even if your landlord doesn’t report payments, our tool helps build your credit with every rent payment reported.

Residential Funding Co., a unit of GMAC’s real estate unit ResCap, is reportedly suing a number of mortgage brokers it worked with who originated so-called bad loans.

According to a report from the Minneapolis Star Tribune, the mortgage lender has already filed more than a dozen federal lawsuits against companies nationwide that allegedly misrepresented borrower information on now non-performing loans.

Additionally, the suits claim that the defendants failed to do their due diligence on borrowers they represented, seemingly allowing their customers to acquire loans that were more likely to fail than their credit risk implied.

The Bloomington-based company is calling on the alleged fraudsters nationwide to buy back the soured loans, which range in size from $21,000 to more than $1 million.

While this article may make it appear as if mortgage lenders are the unknowing victims of “mortgage fraud”, it should be noted that many of the loan officers and underwriters at these large companies often facilitate and perpetuate the problem.

In fact, driven under immense pressure to perform and hit monthly sales figures, many sales associates and accompanying sales managers at these nationwide lenders are often encouraged to “make the loan work,” despite any warning signs that may appear along the way.

It’ll be interesting to see if the lawsuits are successful, given the fact that borrower misrepresentation seemed rampant at nearly every step of the loan process, even on Wall Street.

Guaranteed Rate’s PowerVP mobile app aims to enhance loan originators’ ability to keep in constant contact with customers anywhere, at any given time — 24/7.

The PowerVP app will create new loans; invite customers to complete a digital mortgage; send a one-click conditional approval letter; lock in rates; obtain real-time pricing and run a credit report, the company said in a release.

“It’s now entirely possible for us to qualify buyers for their dream home by the time they leave the open house. Agents submitting an offer at 8:30pm? Our sales team can get the pre-approval out at 8:35, away from their desks, all within this robust tool that will help them hustle smarter for our partners and deliver contract winning speed to our amazing customers,” Guaranteed Rate’s president & CEO Victor Ciardelli, said in a prepared statement.

The Chicago, Illinois-headquartered lender has more than 850 branches across the country and is licensed in 50 states and Washington, D.C.

The lender originated $10.6 billion in the second quarter, up from the previous quarter’s $7 billion — totaling $17.6 billion in the first six months of 2023, according to data from Inside Mortgage Finance.

Production volume in the first half of this year was down about 47% from the same period in 2022. As of June 2023, Guaranteed Rate had a 2.5% market share, IMF data showed.

In a shrinking mortgage market, the lender had two layoffs in August that affected tech staff as well as non-tech workers including loan originators, former employees who were affected told HousingWire.

The company had 2,149 sponsored LOs as of Thursday, according to the National Multistate Licensing System (NMLS).

Recent products launched by Guaranteed Rate include a down payment assistance program in July. G-Rate will provide 2% of the required 3% minimum down payment for a conventional loan or up to $2,000 — whichever is lower.

Whether you’re a parent proudly financing higher education for your child or a student signing on the dotted line for your own student loans, it’s important to understand how those debts can impact your future. Do parent PLUS loans affect getting a mortgage, for example? The short answer? Yes, any student loan you’re responsible for can impact your chances of getting approved for a mortgage. Find out more below.

In This Piece:

Do Student Loans Impact Getting a Mortgage?

Student loans are a type of debt. So if they’re in your name, they can impact your chance of getting a mortgage in the future. Luckily they can have a positive impact in some situations, especially if you have good financial habits.

It’s important to note that student loans only impact your ability to get a house if you’re the one who’s responsible for paying the loan. Parent PLUS loans affect getting a mortgage if you’re the parent who’s signed as the responsible party, for example, but they wouldn’t impact your child’s chances at a mortgage.

But if a student took out a loan with the parent as a cosigner, the loan impacts both people’s credit. It might impact the chances of getting a mortgage for either party.

How Do Student Loans Impact Your Ability To Get a Mortgage?

Student loans are often pretty hefty. The average cost of attending a four-year college or university is $35,331, so you’re looking at total loans that are tens of thousands of dollars. That’s nothing to scoff at, nor is it a small mark on your credit report. Find out how it impacts your mortgage application below.

Student Loans Reduce How Much You Can Save for a Down Payment

You may not have to start paying back your student loans until you’re out of college or a forbearance period has passed. But the time will come when you’ll need to make those monthly payments. Depending on how much you borrowed and what your terms were, student loan payments can be a big hit to your monthly budget.

Get matched with a personal

loan that’s right for you today.

Learn

more

That hit makes it harder to save money quickly for a down payment. While options do exist for mortgage loans with a lower down payment or even no down payment, not being able to save limits your choices.

Mitigate this impact by:

Asking your mortgage broker for information about options with low down payment requirements.

Applying for down payment assistance to help you cover the costs of down payments.

Working to increase your income so you can save more money.

Keeping other types of debts and expenses low to facilitate savings.

They Increase Your Debt-to-Income Ratio

Any amount of debt you have to pay back increases your debt-to-income ratio (DTI). Mortgage lenders look at DTI to understand whether you can afford the payments on any loan you take out.

There’s not a single hard-and-fast rule for where your DTI needs to be to get a mortgage, but the Consumer Financial Protection Bureau notes that 43% is a good number to consider. That means your total debt payments monthly, including any prospective mortgage, should be no more than 43% of your total monthly income. Some lending programs may have stricter DTI requirements.

Here’s an example to demonstrate how a student loan can change DTI. If you have student loan payments of $500 a month, a car loan of $500 a month and credit card payments totaling $300 per month, you have $1,300 in debt. If you want to get a loan to pay for a home and the loan would result in a $1,200 a month mortgage, that’s a total of $2,500 per month.

If you only make $5,000 a month, your debt-to-income ratio would be 50%. That may be too high for a favorable mortgage loan to be approved. If you take out the student loan and keep all the other factors the same and the DTI is now 40%. That’s a better DTI for most mortgage loans.

Offset the impact of student loans by reducing your other debts. For example, in the above example, you could work to pay off the credit card debt before you apply for a mortgage. You might also refinance the car loan, bringing your monthly payment down to $300. That would leave you with a 40% DTI.

Student Loans Impact Your Credit Score

Most lenders do report student loans to one or more of the credit bureaus. This is actually good news, because paying your student loans on time can help you build credit and have a positive impact on your credit score. On the flip side, if you miss payments or end up defaulting on your student loans, the negative impact on your credit can bring your score down and keep you from getting approved for a mortgage.

Keep this from being a problem by paying your student loans on time every month. Consider setting up auto bill pay so you don’t have to worry about accidentally missing a payment. You may also want to find out more about the required credit score to buy a house so you know what you’re shooting for.

Does Applying with FAFSA Effect Buying a House?

No, completing FAFSA doesn’t impact your credit at all. And it doesn’t mean you’re taking out a student loan. FAFSA simply lets you apply for any potential student financial aid that might be available for you. You’re then offered aid that you can choose from.

More Tips for Ensuring a Successful Mortgage Application

Doing a bit of homework before you apply for a mortgage can increase your chances of success. Here are some things to do related to your student loans:

Consolidate multiple student loans into one if possible, which will reduce the total amount you have to pay each month. This makes it easier to save and can reduce your DTI.

If student loans report as deferred on your credit report, get the specific payment amounts from the servicer or a payment letter from the servicer stating an approximation of what the payments will be when they come due and payable.

Avoid any student loan delinquencies, especially in the last 12 months. Ignoring this could result in your application being denied for a government loan such as an FHA- or VA-backed mortgage. Government programs are strict about delinquencies on federal debt, which is what a student loan is.

If any student loans are paid in full but your credit report shows a current payment obligation, provide supporting documentation showing it’s been fully paid off to the mortgage company.

Review your credit reports before you start the mortgage application process. If there are inaccuracies on your credit reports related to student loans—or anything else—file a dispute and request the credit bureau to investigate and correct the information.

Learn More About Mortgages Today

It’s also a good idea to learn more about how a mortgage works and read up on terms you need to know in a mortgage glossary. The more you know, the more confident you’ll be in the entire process. For the best information on your credit, consider signing up for ExtraCredit, where you can get 28 of your FICO scores and a report card that helps you understand what you need to do to improve your scores.