In San Francisco’s quaint, upscale community of Russian Hill, home to the famously crooked Lombard Street, a 4-bedroom home is now up for grabs.

And it comes with some of the best views money can buy.

Beautifully updated, the 4-bedroom, 2-bathroom single-family home features the timeless architecture typical for the area, and a rooftop terrace with a wet bar and phenomenal views of the San Francisco area facing south, west, and north — including views of Lombard Street which is a crossroad for this home.

Lombard Street, San Francisco. Photo credit: Aerial Canvas courtesy of Coldwell Banker Realty

Located at 2300 Leavenworth St, on the northeast corner of Leavenworth and Lombard, the 1913-built property is part of the historic Castle Court gated community — which has ties to the Fay family (Fay Brothers Soap Factory founder David Fay owned a house here too, later rebuilt by his descendants and now known as the Fay-Berrigan House and Park).

Listed for $3,495,000, the ideally located San Francisco home is listed with The Swann Group, affiliated with Coldwell Banker Realty.

Inside, the entry level offers a spacious flex space for a media room, office, or guest space, with a full bath and gym. The main living floor is up one level and features an open kitchen, dining, living, and office with South, West, and Northern views.

Photo credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker Realty

The top floor has three bedrooms, a full bath, and direct access to the rooftop terrace.

A true showstopper that makes the most of the home’s great San Francisco location, the rooftop terrace offers picture-perfect views of Alcatraz, Coit Tower, the Bay Bridge, the skyline of the financial district, and the world-renowned flowering crooked street.

Photo credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker RealtyPhoto credit: Aerial Canvas courtesy of Coldwell Banker Realty

Its sought-after location in Russian Hill places it mere moments away from the excellent amenities of Hyde Street, North Beach, the Polk Street corridor, and Fay Park.

More San Francisco homes

The real ‘Full House’ house in San Francisco and where to find it

Mrs. Doubtfire’s house is hiding in plain sight in San Francisco

San Francisco’s Most Famous Houses: How Much are the ‘Painted Ladies’ Worth?

Mortgage rates that spiked last year have continued to rattle Colorado Springs’ housing market in 2023.

In September, for example, year-over-year home sales fell for the 16th consecutive month, a recent Pikes Peak Association of Realtors market trends report shows.

Homeowners who were able to sell their properties within days — and even hours — two to three years ago waited more than five weeks, on average, last month for a buyer to come along, according to the report.

A Pikes Peak Regional Building Department report shows that while single-family building permits — which signal the construction of new homes — rose modestly in September compared with the same time last year, last month’s total nevertheless was the lowest for any September since 2011 and continued a mostly weak trend of building permit numbers for the year.

“The market was dramatically affected by the rapid, historical increase in mortgage rates,” said Gordon Dean, a real estate agent with Re/Max Advantage in Colorado Springs and the incoming board chairman of the Pikes Peak Association of Realtors.

From mid-2019 through 2021, 30-year, fixed-rate mortgages — the most common loan for homebuyers —plunged to an average of 3% and below nationally, according to mortgage buyer Freddie Mac.

Those historically low rates fueled homebuying nationwide and, combined with a shortage of new and existing properties available for purchase, sent home prices to record highs in markets such as Colorado Springs. Home sellers often fielded multiple offers for their properties and frequently received bids that topped their asking prices by thousands and tens of thousands of dollars.

When 2022 began, 30-year, fixed-rate loans averaged 3.22% nationally, Freddie Mac figures show.

After the Federal Reserve began to hike interest rates last year to curtail soaring inflation, however, mortgage rates began a steady ascent. By year’s end, after briefly topping 7%, long-term mortgage rates stood at 6.42%.

Long-term rates stayed below 7% for much of this year, but began to climb again in late summer. By mid-August, 30-year, fixed-rate mortgages had jumped again; on Thursday, they rose to a national average of 7.57%, which was the highest since 2000.

“Several factors, including shifts in inflation, the job market and uncertainty around the Federal Reserve’s next move, are contributing to the highest mortgage rates in a generation,” Sam Khater, Freddie Mac’s chief economist, said in a news release this month. “Unsurprisingly, this is pulling back homebuyer demand.”

And because many homebuyers felt priced out of the market because of higher rates or they no longer could qualify for a mortgage, the pace of buying, selling and construction slowed in Colorado Springs and the Pikes Peak region, along with other areas nationwide.

“I think it’s a good market because the demand is high,” said Grace Covington co-owner and co-CEO of Covington Homes, a Springs builder.

“We have a lot of people who are ready, willing and want to buy, (but) just not able because of interest rates.”

With the third quarter in the books, here’s a snapshot look at where conditions stand for Colorado Springs’ single-family housing market:

• Home sales have fallen and can’t get up — or so it seems.

Space Command decision expected to positively impact Colorado Springs real estate market

In September, Colorado Springs-area home sales totaled 1,008, a 22.1% decline from the same month last year, the Realtors Association’s market trends report and Gazette historical data show. Likewise, last month’s total was the fewest number of home sales for any September since 2013.

“That’s not much, literally,” real estate agent Harry Salzman of Salzman Real Estate Services and ERA Shields Real Estate said of September’s sales.

Other numbers in the association’s market trends report and Gazette historical data that underscore the slowdown in sales: Year-over-year home sales have dropped each month since June 2022; sales for the first three quarters of this year totaled 9,402, a 24% drop from the same period a year ago; and year-to-date sales for 2023 are at their lowest point since the same period in 2014.

Also, homes spent an average of 38 days on the market before selling in September, up from 25 days a year ago.

• Pickings still are relatively slim when it comes to finding a home to purchase.

The supply of homes listed for sale at the end of September totaled 2,484. On the one hand, that total rose 2.6% over August and was the highest for any month since October of last year.

Yet, from a historical standpoint, inventory is low. In pre-Great Recession years, September listings routinely topped 4,000, which provided homebuyers with many more choices, Gazette historical data show.

Residents in Colorado Springs’ outlying areas watch as growth creeps closer

Some owners who bought their properties or refinanced when mortgage rates were in the 3% neighborhood and are considering selling are holding on to their properties for now, which has contributed to the tight inventory, real estate experts say.

Sure, those homeowners might want to move up or downsize, but they’re not willing to abandon their rock-bottom mortgage rate and take on a new loan that’s in the 6% to 7% range, the experts say.

At the same time, some homebuyers who purchased in 2021 or 2022 haven’t seen their values appreciate enough to a point where they can sell their property and get the price they need to pay off their mortgage and real estate costs, said Patrick Muldoon, broker/owner and president of Colorado Springs real estate company Muldoon Associates.

As a result, those homeowners aren’t selling, he said. Instead, they’re calling the property management side of his business, Muldoon said, and looking to rent their homes. That keeps those properties from being added to the overall inventory of houses for sale.

“I can’t sell my house or I tried to sell my house or I’m upside down on my house and my next option is, I’m a forced landlord,’” Muldoon said he’s hearing from some homeowners.

• Despite slow sales, home prices rose in September.

The median price of homes that sold last month rose to $475,000, a 3.3% year-over-year increase, the Realtors Association report shows. It was the first year-over-year increase in median prices since November 2022.

But if sales fell in September, why did prices increase? Blame tight inventory, Salzman said.

“It’s got to be supply and demand. Not a doubt,” he said. “We don’t have very many selections for people to take a look at, no matter what the price range is. Particularly, even if you’re, say, under $500,000 in a purchase price? There’s not much inventory to select.”

As a result, some sellers can list their homes at prices that are a little more aggressive than a few months ago, Salzman said.

“You’re going to get a better price today because if you’ve got a buyer today at these interest rates, they’re a motivated buyer,” he said. “And when you’re a motivated buyer, sometimes you might have to pay a little more, like we did a couple years ago, because there’s no inventory.”

Sign up for free: News Alerts

Stay in the know on the stories that affect you the most.

Success! Thank you for subscribing to our newsletter.

5 growth hotspots around Colorado Springs: A closer look

Muldoon suggested that the latest figures showing an increase in median prices in September might be misleading. Some of the homes that sold last month are on the high end of the price range, which pushed up the overall median price, he said.

A real estate agent friend told him “we’re only grading the winners,” Muldoon said. “We’re looking at the stats and we’re only grabbing the houses that have sold, and those houses that have sold are the upper end of the bell curve.”

And some sellers still are getting top dollar for their properties, even as the market has cooled.

Attractive properties that are in good condition and priced correctly to reflect the current market and comparable homes in their neighborhood still can receive multiple offers — just not nearly as many as a few years ago, said Dean, of Re/Max Advantage.

“When you can provide someone in a desirable school district and great condition and, hypothetically, a stucco rancher with three bedrooms on the main (floor), that is a golden goose egg in the marketplace and I would be shocked if, priced correctly … it’s probably going to draw multiple offers,” Dean said.

In fact, he said he and his wife, Amy, who’s also a real estate agent, marketed a home that fit that description — and fielded a cash offer that came in about $15,000 over the seller’s asking price.

• The new home side of the housing market also has felt the effects of high mortgage rates.

In September, building permits issued for the construction of single-family, detached homes totaled 136, a slight, 1.5% increase over the same month a year earlier, according to the Pikes Peak Regional Building Department. That figure doesn’t include townhomes, condominiums or duplexes.

As Colorado Springs grows, 20-somethings are the fastest growing cohort

Even with last month’s increase, and an inflated number of permits that builders pulled in June in advance of a building code change taking effect, single-family permits for the first nine months of 2023 totaled 1,791 — a nearly 35% nosedive from 2,738 during the same period in 2022.

“The interest rate environment is certainly the main culprit for that,” said Tom Hennessy, president and CEO of Challenger Homes, one of Colorado Springs’ largest builders. “When you have interest rates pushing 8%, you’re just making affordability that much more difficult for that many more people.”

The difficulty in affording today’s higher mortgage rates stands in contrast to a generally positive outlook for the Springs, Hennessy said.

“What’s really kind of interesting is, there’s still people looking (for homes) and Colorado Springs’ economy is still generally pretty good,” he said. “Unemployment is still low. We still have a lot of jobs moving in. We have a lot of military in and out of the area. People want to buy. It’s just of matter of can they buy?”

Not only have buyers been stymied by high mortgage rates, but their costs for consumer goods, utilities and other expenses have soared because of inflation, said Covington, who’s co-CEO and co-owner of her homebuilding company with her husband, Ron.

Businesses saddled with high interest rates for loans have passed on their increased costs to consumers, which also affects their personal finances and their ability to buy homes, Grace Covington said.

“We really just need to get inflation under control and rates down again,” she said.

For now, Challenger, Covington and other builders continue to woo buyers with mortgage rate buydowns — incentive programs in which they effectively reduce, or buy down, a mortgage rate for the first few years of a loan to help buyers afford monthly payments and get them into a new home.

A year ago, builders also might have offered incentives such as discounts on premium lots or reduced prices on home upgrades to interest a buyer, Hennessy said.

Now, however, mortgage buydowns are the main focus for builders, he said.

“Today, it pretty much all deals with house payment and buying down the mortgage rate,” Hennessy said.

“The name of the game today is house payment. How can I get into a house with a payment that I can afford?”

• What’s ahead for Colorado Springs’ housing market?

That’s a question that every real estate agent and builder wants to know.

Who Are We? What the population numbers for El Paso County and Colorado Springs show

Salzman advices homebuyers who can afford a home to take the plunge now, even if prices remain high. The value of their investment always will appreciate over time, he said, and today’s 7% mortgage can be refinanced lower when rates fall.

Even if rates are high today, Salzman suggests that buyers talk with their mortgage lender to ask about getting a break on their loan origination fee in exchange for agreeing to refinance with the same lender in two to three years.

“Because their business is way down, anything is negotiable,” Salzman said of mortgage lenders.

A drop in mortgage rates, not surprisingly, would help boost sales and the overall market, Dean said. But how far would rates have to fall?

Six percent and below, he said, would help encourage borderline buyers to jump back into the market and persuade owners with a low mortgage rate to feel comfortable leaving it behind and accepting a higher rate to get the home they want.

“If we do see a reasonable drop, and I say reasonable, 6 flat on interest rates, we’re going to have a very robust market again,” Dean said.

Colorado Springs’ ‘beating heart?’ Check the pulse of downtown, mayor and area backers say

“For me personally, at the end of the day … it’s that interest rate that’s going to be the main driver for anybody,” he added. “Affordability. That’s affordability, in my opinion.”

Muldoon, however, echoed his previous bearish comments on the outlook for the housing market.

A recession in 2024, waves of layoffs, more bank failures, continued high interest rates and other national economic forces could have a ripple effect on local businesses and employers in Colorado Springs, Muldoon said. As a result, the local housing slowdown could continue and even worsen — with falling prices being one of the biggest impacts, he said.

“If Colorado Springs started showing signs of economic issues,” Muldoon said, “then you would see sellers start with some pretty swift reductions on prices.”

Rent prices are on the rise, with the average cost increasing 18% between 2017 and 2022. But buying a home requires a hefty down payment and good credit. Renting to own your home can give you the best of both worlds, but there are some downsides.

If you’re thinking about signing a rent-to-own agreement, it’s important to weigh the pros/cons of rent-to-own home deals. Here’s what you need to know before you sign on the dotted line.

What are rent-to-own homes?

When you own a home, part of your monthly payments goes toward paying off the principal. If you stay in the home long enough, you’ll own it.

The same doesn’t apply to rentals. Your monthly rent solely covers your costs of living in that home, whether it’s a condo, apartment, townhouse, or single-family house.

A rent-to-own home lets you pay rent to live on the property, with the option to buy it when the lease runs out. In some cases, a portion of your rent goes toward the purchase price, but that isn’t always the case.

How does rent-to-own work?

A rent-to-own agreement is essentially a lease agreement with an option to buy. Rent-to-own contracts should be read thoroughly. Those options can vary from one contract to another.

When you sign a rent-to-own contract, you pay an upfront fee called an option fee. This is typically 1 to 5% of the home’s purchase price, and it’s non-refundable.

It’s important to note that a lease does not relieve you of the requirements to buy a house. You’ll still have to qualify for a mortgage and make a down payment. It’s merely a way to buy yourself some time and possibly put some of your rent toward the purchase price of a home.

Lease Option vs. Lease Purchase

Before you sign, pay close attention to the lease agreement you’re signing. There are two types, and one contractually obligates you to buy the property.

Lease Option Agreement

A lease option agreement is the best deal of the two for you, the buyer. You’re signing a lease option contract that merely gives you first rights to the house when the lease is up. If you change your mind, find a better deal, or can’t qualify for a mortgage, you can find somewhere else to live and move your belongings out.

Since the option fee is nonrefundable, it’s important to note that you will lose money if you choose not to buy. Calculate this loss when you’re deciding whether to buy.

Lease Purchase Agreement

Unlike a lease option agreement, lease purchase agreements obligate you to buy at the end of the lease. Since it’s a contract, that means you’re legally obligated to purchase the house.

This can be risky for a couple of reasons. Once you’re in the house, you may see issues you didn’t notice when you were first touring the house. Things could change with the neighborhood or your circumstances that you couldn’t know at the outset.

But the biggest issue with a lease purchase contract could simply be that you aren’t eligible for a mortgage to buy the house. Make sure you know, up front, what penalties or liabilities you’ll face if you can’t buy the house when your lease is up.

Even though both agreements operate differently on your end, they do obligate the seller to give you the option to buy when your lease expires. This puts you in a position to own a home at a predetermined future date, giving you the opportunity to start planning.

Length of a Rent-to-Own Agreement

Rent-to-own contracts start with a lease period that can be up to five years but is usually less than three. The thought is that the rental period will give a renter time to qualify for a mortgage. During this time, you’ll work on building your credit, if necessary, and saving for a down payment.

In some cases, a rent-to-own arrangement could have renewal terms. That means if you reach the end of the lease and want more time, you can extend the lease. With this option, though, the property owner could increase your monthly rent or the purchase price.

Preparing for Homebuying

During your lease term, you’ll make each monthly rent payment in exchange for remaining in the house. But it’s important during that time that you work toward purchasing the house when your time is up. Here are some things to do to boost your chances of landing a mortgage once your lease expires.

Boost Your Credit Score

Your rent-to-own deal requires that you qualify for a mortgage once the term is up. To do this, you will need to meet the minimum credit score requirements. You can get a free copy of your credit report each year at AnnualCreditReport.com, but there are also credit monitoring services that can help you stay on top of things.

Although requirements can vary from one lender to the next, Experian cites the following credit scores as necessary to land a mortgage:

FHA: If you qualify, a Federal Housing Association loan will accept credit scores as low as 500.

USDA loans: Those who meet the requirements can qualify with a score as low as 580.

Conventional loan: Generally 620 or higher, but some lenders require 660 at minimum.

VA loans: Eligible military community members and their families can obtain loans with scores as low as 620.

Jumbo loan: These loans cover houses at a higher price, so you’ll need a score of at least 700.

Save for a Down Payment

In addition to a good credit score, you’ll need to put some money down on your new home. Down payment requirements vary by loan type, but it’s recommended that you put at least 20% down. That means if you’re buying a $200,000 home, you’ll need at least $40,000 by closing.

There are lower down payment options, but if you choose those, your mortgage payments will include something called private mortgage insurance. This will increase your monthly payment by $30 to $70 per $100,000 borrowed.

If you can’t save up 20%, you may qualify for an FHA loan, which requires as little as 3.5% down. Both VA and USDA loans have zero down payment options, and there are programs offering down payment assistance to those who qualify.

The best part about rent-to-own properties, though, is that some come with rent credits. With a rent credit, a percentage of your rent will go toward your required down payment. Calculate in advance how much you’ll have in that escrow account at the end of your lease to make sure you save enough to supplement it.

What are the pros of rent-to-own?

Rent-to-own homes can be a great option, especially during a tight housing market. If there’s a house you want to buy, but you can’t make a down payment or your credit isn’t where it should be, it could be a great workaround. Here are some of the biggest benefits of rent-to-own agreements.

Rent May Go Toward Purchase Price

Depending on the terms of the rental agreement, renting to own could help you work toward paying for the home. Instead of the full amount of your rent being pocketed by a landlord, a percentage of your rent could go toward the eventual purchase price. Before signing, pay attention to rent credits and try to negotiate the best deal possible.

The Purchase Price Is Locked In

When a landlord agrees to a lease option, the home’s purchase price is written into the contract. That price will typically be higher than what the market says it’s currently worth. This means if the U.S. housing market sees an unexpected increase, you’ll be buying the home for less than its value. Even if the market dips, once you purchase the house and remain there for a few years, you may be able to sell it at a profit.

You’ll Buy Extra Time

For many renters, the rent-to-own period provides time to qualify for a mortgage. If you’ve researched all the options and found you’re close but not quite there yet, a rental period could be just what you need.

Before you choose this option, though, take a look at your circumstances. If substantial existing debt and poor credit mean you won’t qualify, you may need more than the few years you’ll get with a rent-to-own agreement.

No Moving Necessary

Let’s face it. Moving can be a pain. You have to pack everything up, line up a moving truck and get help moving, and unpack your items once you’re in the new location.

With a rent-to-own agreement in place, you skip the hassle of moving. You’ve already been in that home, making monthly rent payments, for at least a couple of years. You’ll simply go through the closing process and switch from rent payments to mortgage payments.

What are the cons of rent-to-own?

If you can get a mortgage, that’s always going to be a better option than renting or leasing to own. But there are some instances where renting without the buy option could be better for you. Here are some things to consider.

Rent-to-Own Home Maintenance

Before you sign any lease agreement, it’s important to read the fine print. One thing to note, specific to own agreements, is who will be responsible for maintenance during the rent-to-own period. If you rent without the promise of eventual ownership, your landlord will take care of those costs. In some cases, rent-to-own agreements require the renter to handle all repairs.

But there’s an upside to handling repairs on your own. To your landlord, the property is technically yours. That means you likely will give it more TLC. Still, it’s well worth it to pay for a home inspection before you agree to a rent-to-own agreement. This will identify any serious issues that will need to be addressed before you buy.

Option Fee

One distinguishing feature of a rent-to-own property is the option fee. This is usually between 1 and 5% of the purchase price and is non-refundable. That means if you don’t ultimately qualify for a mortgage, you’ll lose that money.

Home Values Could Drop

Property values aren’t guaranteed. Your landlord estimates the value of the property, but if you’re in a rising market, you might get that home at a steal. While that’s good news for you, the reverse can happen. If housing prices drop substantially during that time frame, you could find yourself buying a property for more than it’s worth.

Contract Breaches Can Be Costly

Rental agreements are a legal obligation. If you don’t pay your rent, your landlord can evict you and keep your security deposit. But rent-to-own contracts bring an additional level of risk. Missed payments mean you could be evicted and lose all the money you’ve put in. That includes the upfront fee and any rent credit you’ve earned.

All that money will also be lost if you can’t qualify for a mortgage when your rental time is up. These agreements can give you some breathing room. However, if your low credit scores, income, lack of a down payment, or employment situation make you ineligible for a mortgage, you could be searching for another rental while losing everything you’ve paid on the lease-to-own home.

Steps to Buy a Rent-to-Own Home

Once you’ve decided renting to own is the route you want to take, you may wonder what to do next. The following steps can help you ensure you get the best deal in a rent-to-own agreement.

1. Find a Home

This is more challenging than it might sound, especially if you’re looking in a competitive real estate market. Rent-to-own homes are extremely rare, so you may have to find a home for sale and try to negotiate this type of setup.

Typically, homeowners become renters when they can’t sell their homes. This means your rent-to-own contract might be on a home that’s in a less desirable or convenient area of town. For someone whose home has been on the market for a while, being able to collect rent money with the promise of a sale in a few years can be a huge relief.

For best results, find a real estate agent who can help you track down a home and negotiate with the seller. The National Association of REALTORS® maintains a directory of real estate agents, but you can also ask for a referral or find real estate agents nearby who have brokered these types of deals recently.

2. Research the Home

Even if it’s tough to find a lease-to-own home in your area, don’t snatch up the first one you find. Crunch the numbers to make sure the rent and purchase price make financial sense for you. Look at the sale history of the home to verify that the owner’s estimated purchase price is somewhat within what the median home price will likely be when your lease expires.

3. Research the Seller

The seller needs to be looked into as well. This is even more important with rent-to-own agreements since this person will be your landlord for the entire lease period. If you see any red flags during your interactions with the seller, move on.

4. Choose the Right Terms

Before you make a real estate purchase, you would have a closing attorney review the documents. The same goes for a rent-to-own agreement. Run all the paperwork past a real estate attorney to make sure there’s nothing in the contract that will hurt you in the long run.

Your real estate agent should be able to negotiate the best terms for you, including how each rent credit will help you build equity and what happens at the end of the lease.

5. Get a Property Inspection

Any time you make a home purchase, it’s essential to know what you’re buying. The same is true for rent-to-own properties. A home inspector can check things out and make sure you aren’t purchasing a home with serious issues.

6. Start Preparing to Buy

Once you start making rent payments, it’s time to start preparing for your eventual home purchase. Chances are, you’ll have to make a sizable down payment on a home loan, so plan to have that ready. Also, keep an eye on your score with all three credit bureaus and make sure you’ll qualify.

A rent-to-own contract can be a good deal for both the buyer and the seller. It can give you time to save money and improve your credit score. A real estate lawyer should take a look at your contracts and make sure your best interests are protected.

Bottom Line

Rent-to-own homes present a unique option for potential homeowners. This approach offers the opportunity to enter the homeownership arena at a slower pace, allowing individuals to build credit, save for a down payment, and experience living in the home before making a final purchase decision.

However, the rent-to-own path isn’t free from drawbacks. Potential buyers should be wary of unfavorable terms, higher monthly payments, and the risk of losing money if they decide not to buy. Ultimately, like all significant decisions in life, choosing a rent-to-own option requires careful consideration and thorough research.

Frequently Asked Questions

Where can I find rent-to-own houses?

Rent-to-own houses can be found through specialized websites dedicated to these types of listings, local real estate agents familiar with the concept, or sometimes through classified advertisements in local newspapers or online platforms.

Can I find rent-to-own homes on Zillow?

Yes, Zillow does list rent-to-own homes. When searching for properties, you can filter the search results to show only rent-to-own options. However, availability may vary based on the region and market conditions.

How long is the typical rent-to-own contract?

The typical lease term ranges from one to five years, but terms can vary based on the agreement between the homeowner and tenant.

Do I have to buy the house at the end of the lease?

No, the decision to buy is optional. However, if you decide not to purchase, you may lose any upfront fees or additional monthly amounts set aside for the potential purchase.

Can the seller change the purchase price once set?

Generally, the purchase price is fixed in the initial agreement. However, some contracts may have clauses allowing price adjustments based on market conditions.

What happens if the property value decreases during the lease period?

If the home’s value decreases and you’ve agreed on a set purchase price, you could end up paying more than the current market value. It’s crucial to negotiate terms that protect your interests.

Who is responsible for repairs and maintenance?

The agreement should clearly outline these responsibilities. In most cases, the tenant bears the responsibility for maintenance and repairs during the lease term.

What’s the benefit of a rent-to-own agreement for sellers?

Sellers can generate rental income while waiting to sell, often at a premium. It also widens the pool of potential buyers, especially those who need time to improve their credit or save for a down payment.

How do property taxes work in a rent-to-own agreement?

In a rent-to-own scenario, the property taxes are typically the responsibility of the homeowner, as they still retain ownership of the property during the rental period. However, the specific arrangement can vary based on the terms of the agreement.

Some contracts may stipulate that the tenant pays the property taxes directly or reimburses the homeowner. It’s crucial for both parties to clearly understand and agree upon who will cover the property tax obligation before entering into a rent-to-own contract.

If I don’t buy, do I get a refund for the extra money paid?

Typically, the extra money paid above regular rent, often referred to as “rent premium,” is forfeited if you decide not to buy.

Is the rent in a rent-to-own agreement higher than usual?

Often, yes. A portion of the monthly rent may be used for the potential down payment or purchase price, making it higher than the average rent for similar properties.

What’s the difference between rent-to-own and mortgage?

Rent-to-own is an agreement where a tenant rents a property with the option to buy it at the end of the lease. No bank is involved initially, and the tenant isn’t obligated to buy. A mortgage, on the other hand, is a loan specifically for purchasing a property. The buyer borrows money from a bank or lender and agrees to pay it back with interest over a predetermined period.

Does rent-to-own hurt your credit?

A rent-to-own agreement, in itself, doesn’t usually affect your credit. However, if the homeowner reports late payments to credit bureaus, it could hurt your credit score. On the positive side, consistently paying on time and eventually securing a mortgage can benefit your credit.

What is another name for rent-to-own?

Rent-to-own agreements can go by various names, including:

Lease to purchase

Lease option

Rent-to-buy

Rent-to-purchase option

Lease purchase

Each of these terms represents the concept of renting a property with the potential option to buy it after a set period.

Many people are lured into the world of real estate investing by stories of millionaires who started their journey with no money down or no steady employment. But the reality is that making money in real estate isn’t easy; a good credit score, investment capital and steady income can help in the beginning.

You’ll also need to grasp the nuances of the local real estate market and learn how to manage financial aspects such as cash flow and property taxes. While real estate buying, selling, and renting may not be much like a game of Monopoly, it is possible to earn steady side income, supplement your retirement, or even build a full-time real estate investment business with the right tools, knowledge, and patience.

Unlike mutual funds, the stock market, cryptocurrency or many other investments, real estate is tangible. Real estate is a concrete asset—one can see, touch, and even reside in. That gives investors a sense of security. However, it also creates unique challenges.

Managed well, the stability and passive income from rental properties can be a safety net against more volatile investments.

This guide is here to clarify the process for beginners. It aims to empower you to make informed decisions, reduce risks, and lay a strong foundation for your real estate investing journey.

Benefits of Investing in Real Estate

The allure of real estate goes beyond the mere ownership of tangible assets. It presents a robust suite of financial benefits that have the potential to amplify wealth and provide stability in uncertain times. As we navigate the advantages, it becomes evident why many seasoned investors prioritize real estate in their portfolios.

Steady and Passive Income

Real estate investing, especially in rental properties, stands out for its potential to provide a consistent revenue stream. When you own a rental property, the monthly or quarterly distributions from tenants contribute to steady income, which can safeguard your finances against unexpected events or economic downturns.

This consistency contrasts with the often erratic nature of the stock market, which can fluctuate daily based on global events, company performances, and other factors. Additionally, for those aiming to attain financial freedom, the passive income generated from real estate can be a step closer to achieving that goal. Over time, as the mortgage payment decreases or remains static, rental rates may rise, increasing your monthly cash flow.

Appreciation Potential

Every investor dreams of their assets appreciating, and real estate often doesn’t disappoint. While there can be periodic downturns in the real estate market, historical trends suggest that properties generally gain value over the long run.

This means that not only can investors benefit from rental income, but they can also potentially see substantial gains when they choose to sell the property.

Tax Benefits

Navigating the world of taxes can be intricate, but real estate investors often find several advantages here. The ability to deduct mortgage interest and property taxes from taxable income can be a significant financial boon.

Furthermore, strategies like depreciation allow real estate investors to offset rental income, reducing their tax burden. Consulting with a financial advisor can help investors maximize these benefits and understand other potential tax advantages, such as 1031 exchanges or deductions related to property management.

Diversification

The saying “don’t put all your eggs in one basket” is sound investment advice. Diversification is a fundamental strategy to mitigate risks. By adding real estate to an investment portfolio, investors introduce a separate asset class that doesn’t directly correlate with the stock market or mutual funds. This can provide a buffer, ensuring that a downturn in one sector doesn’t wholly derail an investor’s financial trajectory.

Leverage

Leverage, in the context of real estate investing, refers to the ability to use borrowed capital to increase the potential return on an investment. When you purchase property with a mortgage loan, you’re often putting down only a fraction of the property’s total cost, while still reaping the benefits of its entire value in terms of appreciation and rental income.

This magnifies the return on investment, as the gains and income generated are based on the property’s total value, not just the down payment. It’s a powerful tool but should be used wisely. Over-leveraging or not accounting for potential rental vacancies can turn leverage into a double-edged sword.

Types of Real Estate Investments

As one dives deeper into the world of real estate, it becomes evident that this asset class is multifaceted, with various avenues to explore and invest in. The right choice often depends on an investor’s goals, risk tolerance, budget, and expertise. Here’s a closer look at some prominent types of real estate investments:

Residential Properties

Residential properties cater to individuals or families. They range from single-family homes to duplexes, triplexes, high-rise buildings with apartments, and other multi-unit properties. You may encounter the term “MDU” or “MUD,” which stand for multi-dwelling unit or multi-unit dwelling, to describe anything more than a single family home, or SFR (single family real estate).

Investing in residential real estate, especially the SFR market, is often a beginner’s first step due to its familiarity and the perpetual demand for housing. While these properties can be a reliable source of rental income, investors should be prepared for the challenges tied to property management, tenant turnover, and ongoing maintenance.

Commercial Real Estate

When one thinks of skyscrapers lining city horizons or sprawling office parks in suburban locales, that’s commercial real estate. These properties are tailored to businesses, and can include complete corporate headquarters or individual offices.

Commercial leases often run longer than residential ones, offering the potential for stable, long-term rental income. However, the entry point can be higher, with larger down payments and a more extensive due diligence process. Additionally, commercial real estate values can be closely tied to the business environment of the locality.

Industrial

Industrial real estate encompasses properties like warehouses, distribution centers, and manufacturing facilities. They’re integral to business operations, ensuring products move efficiently from manufacturers to consumers.

Investing in this sector can offer substantial rental yields, especially if the property is strategically located near transportation hubs. However, the nuances of industrial real estate, such as zoning laws and environmental concerns, necessitate a more in-depth understanding than residential or commercial sectors.

Retail

This sector includes shopping malls, strip malls, and standalone stores. What’s unique about retail real estate is that leases sometimes include a provision where the landlord gets a percentage of the store’s profits, termed as “percentage rent.”

In a thriving commercial area, retail properties can be quite profitable, with long-term leases and the potential for appreciating property values. However, investors should be mindful of shifts in consumer behavior and the evolving retail landscape, especially with the rise of e-commerce.

Multi-Purpose Commercial

A new breed of commercial real estate has emerged to compete with the growth of e-commerce. Multi-purpose commercial spaces blend housing units with office space and retail, often adding hospitality and entertainment venues.

Typically, these spaces are the domain of large real estate investment and property management firms. But if you invest in commercial office space or retail, you will be competing with these multi-purpose properties for tenants, so they are worth acknowledging.

Real Estate Investment Trusts (REITs)

For those not keen on direct property ownership, REITs present an attractive alternative. These are companies that own, operate, or finance income-producing real estate across various sectors. What makes REITs distinctive is that they’re traded on stock exchanges, similar to stocks.

By investing in a REIT, you’re buying shares of a company that manages a portfolio of properties, thus gaining exposure to real estate without the hassles of property management. Moreover, by law, REITs are required to distribute at least 90% of their taxable income to shareholders, leading to potentially attractive dividend yields. However, it’s essential to remember that like all publicly traded entities, REITs can be subject to market volatility.

9 Ways to Invest in Real Estate

Investing in real estate can seem tricky for beginners. But, with time and patience, anyone can master it. Focus on simple investment methods first to get to know your local property scene, meet experienced investors, and learn how to handle money wisely. As you learn and grow, you can dive into more complex investment options.

Here are some great ways for beginners to start in real estate:

1. Wholesaling

Acting as the bridge between property sellers and eager buyers, this method primarily focuses on securing properties at a rate below the prevailing market value. The secured contract is then transferred to an interested buyer, ensuring a margin for the wholesaler.

2. Prehabbing

Unlike intensive property renovations, prehabbing is about amplifying a property’s appeal through minimalistic enhancements. These properties, once given their facelift, usually attract investors with a keen eye for larger renovation projects.

3. Purchasing Rental Properties

An avenue promising consistent returns, this involves acquiring properties to lease them out. For those not inclined towards the intricacies of landlord duties, there’s always the option of hiring seasoned property management professionals.

4. House Flipping

A strategy that has garnered significant attention, house flipping involves a cycle of purchasing, upgrading, and promptly reselling properties, aiming for a profit. The emphasis is on swift transactions and keen market acumen.

5. Real Estate Syndication

Envision a collective where like-minded investors come together, pooling both resources and expertise. Such collectives venture into large-scale property acquisitions, and the ensuing profits or rental incomes are distributed among the participants.

6. Real Estate Investment Groups (REIG)

Primarily, these are conglomerates that steer their operations around real estate investments. By amassing capital from a plethora of investors, they dive into acquisitions of sizeable multi-unit residences or commercial holdings.

7. Investing in REITs

Real Estate Investment Trusts (REITs) revolve around the ownership and meticulous management of properties that yield income. However, investors don’t have to handle the management themselves. Instead, participants can relish the benefits of the real estate sector without the responsibilities of direct property ownership.

8. Online Real Estate Platforms

A fusion of technology with real estate, these platforms seamlessly connect potential investors with vetted property developers. This synergy enables backers to finance promising property ventures and, in exchange, enjoy periodic returns that encompass interest.

9. House Hacking

A blend of homeownership and investment, house hacking is about maximizing the potential of a multi-unit property or a single-family home. Investors live in one segment while leasing out the remaining portions. This dual approach can significantly reduce or even negate monthly housing expenses, serving as an excellent introduction to the world of property management for novice investors.

6 Steps to Get Started in Real Estate Investing

Starting on the path of real estate investing requires careful planning, due diligence, and a methodical approach to ensure that your investments are sound and have the potential for fruitful returns. Whether you’re dreaming of becoming a millionaire real estate investor or merely looking to diversify your investment portfolio, following a structured process can be the key to success. Here’s a step-by-step breakdown:

1. Assess Your Financial Health

Every investment journey should begin with introspection. As an aspiring real estate investor, it’s essential to have a clear understanding of your current financial standing. Ask yourself questions like:

How much capital am I willing to invest?

What are my short-term and long-term financial goals?

Do I have an emergency fund set aside?

Evaluating your risk tolerance is equally crucial. Some might be comfortable flipping houses, while others might prefer the steadiness of rental properties. Consulting a financial advisor at this stage can provide insights tailored to your financial health, enabling you to make informed decisions as you proceed.

2. Dive Deep into Market Research

Knowledge is power in the world of real estate. The local market can be significantly different from national or even statewide trends. Delve deep into understanding:

The demand for rental properties in your target area.

The average property values and rental rates.

The historical appreciation rates.

Any upcoming infrastructure projects or urban development initiatives.

Furthermore, familiarize yourself with real estate terminology. Phrases like “cap rate,” “loan-to-value,” and “operating expenses” will become a regular part of your vocabulary. The better informed you are, the more confidently you can navigate your investments.

3. Assemble Your Real Estate Team

No investor is an island. Success in the real estate business often hinges on the strength and expertise of your team. Look for professionals with a proven track record and positive reviews. Your team might include:

Real estate agents who understand the investor’s perspective.

Property managers to streamline tenant interactions and maintenance.

Lawyers specializing in real estate transactions.

Accountants familiar with the tax implications of real estate investments.

4. Explore Financing Options

The path to acquiring a property is paved with various financing methods. Traditional mortgages are common, but the real estate industry offers other mechanisms like:

Hard money loans.

Private money loans.

Real estate syndication where multiple investors pool resources.

Seller financing.

Each of these has different pros and cons, interest rates, and repayment terms. Understand each deeply to determine which aligns best with your financial strategy.

5. Analyze Potential Properties

The crux of real estate investing is ensuring that the numbers make sense. Before purchasing, assess the property’s potential for generating rental income. Break down:

Monthly mortgage payments

Property taxes

Maintenance costs

Potential vacancy rates

Your goal should be a positive cash flow, where the monthly income from the property (rent) exceeds all these expenses.

6. Negotiate and Close the Deal

Once you’ve zeroed in on a property, the negotiation phase begins. Here, understanding the property’s market value, any existing damages or repair needs, and the local real estate market dynamics can give you an edge.

When it comes to closing, be aware of all associated costs. These might include inspection fees, title insurance, and escrow fees. Being well-informed can help you negotiate these fees and ensure that you’re not overpaying.

Risks and How to Mitigate Them

Like any investment, real estate comes with its set of challenges and uncertainties. The difference between successful real estate investors and those who falter is often the ability to anticipate risks and prepare for them. Here’s an exploration of some prevalent risks in real estate and actionable steps to manage them:

1. Market Fluctuations

Real estate markets can be volatile, with property values rising and falling based on a myriad of factors.

Mitigation: To protect against market downturns, it’s essential to buy properties below their market value. Conducting comprehensive research and seeking expert investment advice can help investors make informed decisions. Remember, real estate is often a long-term game, so a short-term dip can be offset by long-term appreciation.

2. Unexpected Repairs and Maintenance

Properties can often come with surprises, from plumbing issues to roof repairs.

Mitigation: Regular property inspections can catch potential problems before they become major expenses. Setting aside a buffer fund specifically for maintenance can also cushion the financial blow of unforeseen repairs.

3. Vacancy Periods

There might be periods where your property remains unoccupied, leading to loss of rental income.

Mitigation: Properly vetting and building a good relationship with tenants can lead to longer lease periods. Diversifying your investment properties across different areas can also help, as vacancy rates might vary from one location to another.

4. Legal and Tax Implications

Real estate investors can sometimes find themselves entangled in legal disputes or facing unexpected tax bills.

Mitigation: Regular consultations with a tax professional or attorney familiar with the real estate industry can keep investors informed and protected.

Long-term Strategy and Growth

Real estate investing is not just about making a quick buck; it’s about building lasting wealth. Adopting a long-term perspective and continuously refining your strategy can pave the way for consistent growth in the real estate industry. Here’s how:

1. Define Your Real Estate Identity

Are you more comfortable with a buy-and-hold strategy, where properties are retained for long-term growth and steady rental income? Or do you thrive on the excitement of flipping houses, where properties are bought, renovated, and sold for profit? Understanding your preference can help tailor your investment strategy.

2. Reinvestment is Key

For those adopting a buy-and-hold strategy, reinvesting the rental income can substantially grow your real estate portfolio. By channeling profits into purchasing additional properties, investors can benefit from compounded growth.

3. Diversify Your Portfolio

As you gain experience, consider diversifying across various real estate sectors. Branching out into commercial real estate or exploring real estate investment trusts (REITs) can provide additional avenues for income and growth.

4. Continue Your Education

The real estate industry is continually evolving. By staying updated on market trends, attending seminars, and networking with other real estate professionals, you can adapt your strategy and seize new opportunities as they arise.

5. Scale Strategically

A real estate empire begins with just one property. With time, dedication, and a sound strategy, it’s possible to grow your holdings into a substantial full-time income. As you scale, ensure you’re not overextending; always prioritize the quality of investments over quantity.

Key Tips for Beginners

Embarking on a journey into real estate investing can be thrilling, yet the complexities of the industry can sometimes overwhelm beginners. Simplifying the learning curve is essential for novice investors to make informed decisions and find success. Here are some pivotal tips to guide those just starting out:

1. Start Small and Scale Gradually

Many millionaire real estate investors began their journey with a modest property. Purchasing a smaller, more manageable property as your first investment can help you navigate the nuances of the real estate business without being overwhelmed. As you gain confidence and experience, you can then venture into bigger and more diverse properties to scale your portfolio.

2. Prioritize Education

The world of real estate is vast and ever-evolving. Leverage online real estate platforms to learn about market trends, investment strategies, and financing options. Additionally, joining real estate investment groups can be invaluable. These groups not only provide mentorship but also offer opportunities to share resources, insights, and deals with other investors.

3. Location is Crucial

In the real estate realm, location often takes precedence over the type or condition of a property. A mediocre house in a prime location can fetch better returns than a grand mansion in a less desirable area. Research local market dynamics, neighborhood amenities, future development plans, and other location-specific factors before making an investment decision.

4. Networking is Key

Surrounding yourself with knowledgeable people can fast-track your learning process. By connecting with seasoned real estate investors, you can gain insights from their experiences, avoid common pitfalls, and even discover potential partnership opportunities. Attend local real estate seminars, join investor forums online, and participate actively in real estate conferences to grow your network.

5. Stay Updated and Adapt

The real estate industry is not static. Market conditions, property values, and investment strategies can change. Being adaptable and staying updated on industry trends will ensure you remain ahead of the curve and can capitalize on new opportunities.

6. Always Conduct Due Diligence

Before diving into any real estate transaction, thorough due diligence is imperative. From understanding property taxes and zoning laws to estimating potential repair costs and evaluating tenant profiles, leaving no stone unturned will protect you from potential setbacks.

8 Terms Beginner Real Estate Investors Should Know

Venturing into real estate can feel like you’ve entered a world with its own language. Don’t worry; everyone feels this way at the start. Knowing basic real estate terms can help you communicate confidently and make informed decisions.

Dive into these essential terms every beginner should grasp:

Appreciation: Appreciation is the increase in the value of a property over time. It’s one of the primary ways real estate investors make money, especially in growing markets. Appreciation can result from factors like inflation, increased demand, or improvements made to the property.

Capitalization rate (cap rate): Think of the cap rate as a tool to gauge the potential return on a property. It’s a percentage derived from comparing a property’s net operating income to its current market price.

Cash flow: This term captures the money dance – what’s coming in and what’s going out. In the context of rental properties, it means the rental earnings minus all the costs. Positive cash flow indicates you’re earning more than you’re spending.

Equity: Equity represents the value of ownership in a property. It’s calculated by taking the market value of the property and subtracting any outstanding mortgage or loans against it. As an investor pays down their mortgage or if the property appreciates in value, their equity in the property increases. This equity can be tapped into for various financial needs or reinvested.

Leverage: This term refers to the concept of using borrowed money, often in the form of a mortgage, to invest in real estate. It allows investors to purchase properties with a small down payment and finance the remainder. When used correctly, leverage can amplify returns, but it can also increase the risk if property values decline.

Net operating income (NOI): Simplified, NOI is the profit made from a property after deducting all operational costs. It’s your rental income minus all the expenses, showing the true earning potential of a property.

Real estate owned (REO): An REO property is one that didn’t sell at a foreclosure auction and is now owned by the bank. These properties are often sold at a lower price because banks aim to sell them quickly, making them attractive to investors.

Return on investment (ROI): In simple terms, ROI measures the bang you get for your buck. It’s calculated by comparing the profit you made to the amount you invested. The higher the ROI, the better your investment performed.

Conclusion

Real estate investing offers an avenue to diversify your portfolio, generate steady income, and potentially achieve long-term growth. With due diligence, a clear strategy, and the right team, beginners can successfully navigate the complexities of the real estate industry and lay the foundation for a prosperous investment journey. Remember, every millionaire real estate investor started with their first property. Your journey is just beginning.

If you’re shopping for a luxury home, what can you do if you are self-employed or highly leveraged and won’t qualify for, or don’t want, a traditional mortgage?

Many buyers simply pay cash for their homes. According to ATTOM, a property-data provider, 33.12% of all sales nationally of single-family homes over $1 million in the second quarter of 2023 were cash deals.

But there are other ways to pay for a luxury home when a traditional mortgage product isn’t a good fit. Here are some creative alternatives to consider.

More: Gilded Age Townhouse in the Heart of Manhattan’s Upper West Side Offers Three Terraces and Two Gardens

Collateralize your investment portfolio.

These loans, known as investment credit lines, asset-based loans or margin loans, allow you to borrow against the securities you already hold in your brokerage account, whether they are stocks, bonds or alternative investments. The advantages, according to Michael Silver, a certified financial planner in Boca Raton, Fla., are that they have no application fees or closing costs, no financial documentation is required and your credit score and debt-to-income ratio aren’t considered. “It’s strictly based on your assets,” he said. “So, if somebody is highly leveraged or if they’re high-net worth but have bad credit, none of that matters.”

The interest rate on a margin loan fluctuates, however, and rising rates or declining asset values can result in the institution requiring the borrower to come up with additional assets to secure the loan. Silver said the interest rates on margin loans are typically 1% to 2% over the federal-funds rate (which was between 5.25% to 5.5% on Oct. 6) and that most institutions will fund about 60% to 70% of the value of the pledged assets. These loans are beneficial for home buyers who don’t want to sell their assets to avoid paying capital-gains taxes, and borrowers who are self-employed or lack sufficient documentation to qualify for a mortgage. “I also recommend margin loans for people who want to buy a house and come in aggressively with cash, but they need to sell their current house,” Silver said. “If they got a bridge loan, they would have to go through the bank application process, but you can get a margin loan in a week.”

MANSION GLOBAL BOUTIQUE: Cozy Pieces to Outfit Your Home for Fall

Consider a cross-collateral loan.

Cross-collateralization can be used to purchase a primary home, a second home or an investment property. It simply means that multiple assets are used as security for a loan. For example, if you’re buying a $1 million house, and you apply for a traditional mortgage at an 80% loan-to-value ratio to avoid paying for private mortgage insurance, you would qualify for an $800,000 mortgage and have to come up with $200,000 in cash. If you own another home free and clear, by using a cross-collateral loan, the lender would combine the appraised values of both homes and finance up to 70%, the maximum loan-to-value ratio typically used by lenders who offer cross-collateral loans, according to Sarah Alvarez, vice president of mortgage banking for William Raveis Mortgage. So if your other home is worth $500,000, you would qualify for a $1,050,000 loan (70% x $1.5 million). “That allows you to get 100% financing for the million-dollar purchase, and private mortgage insurance is not required,” Alvarez said. The lender will mortgage both properties to secure the loan. The interest rate charged on a cross-collateral loan depends on a number of factors but is usually comparable to a traditional mortgage, Alvarez said.

Liquidate assets.

Another alternative financing method is to liquidate assets. In tight markets, offering to pay cash and close quickly can give buyers a competitive advantage. This strategy is usually best for home buyers who have substantial assets that can be liquidated quickly and easily, such as a stock portfolio, rather than real estate, which is a nonliquid asset that can take months to convert to cash. Bear in mind that liquidating assets can be a taxable event that triggers capital-gains taxes. Be wary of cashing out your 401(k) or other retirement account for cash. You’ll have to pay income tax on the money you withdraw from a 401(k), plus if you’re under age 59½, the Internal Revenue Service will assess a 10% penalty, although there are some exceptions to the penalty such as for total and permanent disability.

It’s common for home buyers to purchase a property in a certain school district.

This ensures their children can attend a specific school if they’ve got their eye on one in particular.

Heck, even those without kids might favor a certain home because it resides in a highly-sought after district.

Now Zillow has made it easier for prospective home buyers to find properties in attendance zones or school districts simply by using the search bar.

When using the company’s mobile app, you’ve got the option to search by school, just as you would city or neighborhood.

Search by School on Zillow to Find a Home in Your Desired District

The latest update to the Zillow app allows home shoppers to search by school attendance zone or school district.

Simply open the app and navigate to the search bar. Instead of typing in a certain city or neighborhood, type the name of a school you like.

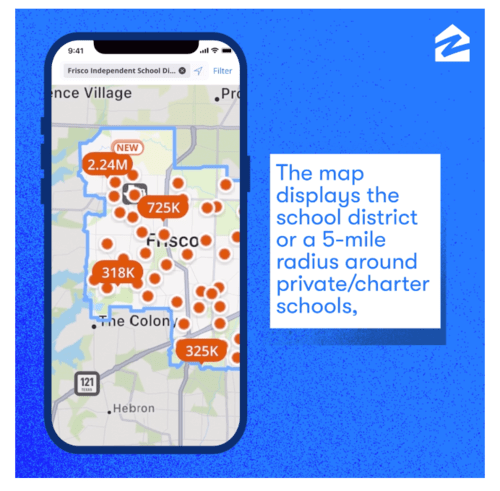

From there, Zillow will automatically display the attendance zone boundaries on the associated map in the app.

You’ll be able to see properties that are available for sale (or rent) within the attendance zone selected.

And if you search for open enrollment, or for a charter or private school without an assigned boundary, Zillow will display homes within a 5-mile radius surrounding the school.

The new search-by-school feature also allows home shoppers to receive instant or daily alerts when new for-sale or for-rent homes within their preferred school district or attendance zone come online.

That way you’ll be the first to know if a property meeting your school district needs pops up.

Since homes in desirable school districts are often quite popular, this can provide a competitive edge over other prospective buyers.

Those who are logged-in users will also see auto-complete suggestions for relevant schools and school districts based on their search history.

As always with any sort of property details, be sure to double-check that the home is indeed in the school district.

While it’s helpful to have this information generated automatically, it’s always smart to verify that the details are accurate.

This functionality is currently available on Zillow’s iOS mobile app and will launch on Android by the end of 2024 (it will be on the web sometime next year).

School Districts Are Very Important to Home Buyers

While there are a number of reasons why home buyers choose their properties, school district is a biggie, especially for those in their 30s.

And the prime first-time home buyer age is around 34, so most home buyers are going to be very focused on the associated school district.

As noted, even those without kids (or no interest in having kids) should be concerned with school districts as they can impact valuations pretty significantly.

You’ll often find that property values (and list prices) are notably higher in highly-sought after school districts.

This means a home seller can unload their property for a premium, or rent it out for more to a family who wants to reside in the district.

But it is also typically means you’ll pay more for it, and/or face more competition when attempting to buy the property.

Per Zillow’s Consumer Housing Trends Report, 75% of home buyers in their 30s emphasize the importance of school district selection.

Additionally, 67% of buyers in their 40s and 61% of first-time buyers consider school district a highly important factor in their home search.

This trend also seems to be growing, with the percentage of buyers who considered school districts highly important rising to 52% in 2023 after holding steady at 43% from 2018 to 2021.

Homes Tend to Appreciate More in Good School Districts

Back in 2016, I wrote that you should buy a home in a good school district even if you don’t have kids because they tend to appreciate more than those in not-good districts.

A study by ATTOM Data Solutions analyzed average test scores from about 19,000 elementary schools nationwide that covered nearly 46 million single-family homes and condos.

They discovered that in zip codes with at least one good school, the average estimated home value was 77% higher than in zip codes without any good schools.

Despite being more expensive, these good school district properties increased an average of $74,716 since the time of purchase, compared to just $23,311 for the not-good districts.

In other words, the purchase price might be higher to start, because it’s located in a good school district, but over time it should outperform properties located in the not-good school districts.

This might explain why there are even single-family home investors who are actively targeting properties in “elite school districts” these days.

While I don’t necessarily endorse that approach, since it makes getting into good school districts even more competitive for young families, it makes business sense.

All that being said, school districts aren’t everything. It can also pay off to buy a home near a Starbucks, a Target, or a Whole Foods or Trader Joe’s.

But ultimately, you should love the home you make an offer on, and want it for a variety of reasons that go beyond it’s potential monetary value.

Read more: When should you start looking for a house?

AI and data-led fintech company Pagaya Technologies named Sanjiv Das as president. Das, a former CEO of Caliber Home Loans, will begin his new role on Oct. 16.

His responsibilities include overseeing the strategy and growth of Pagaya’s commercial business – including its single-family rental business and its subsidiary Darwin Homes – as it continues to enhance its tech-enabled product offering and expand its new and existing lending partnerships, the firm said in a news release.

“We’re excited to welcome Sanjiv as President of Pagaya. His global perspective and extensive entrepreneurial experience in the financial sector and capital markets, as well as his proven track record of building and growing global businesses at scale, uniquely positions him to guide Pagaya’s lending network and innovative product offerings in this next stage of growth,” Gal Krubiner, Pagaya’s co-founder and CEO, said.

Das spent six years as CEO of Caliber Home Loans — a NewRez-owned residential mortgage lending company — until January 2022.

Das’ career also includes positions as CEO, president and chairman of the board of directors for Citigroup‘s mortgage division. He has also held senior roles at Morgan Stanley, American Express and Bank of America.

The executive replaces Ashok Vaswani, who served as Pagaya’s president since June 2022. Vaswani will serve as an advisor to Pagaya for a smooth transition for Das.

“Under Vaswani’s leadership, Pagaya has successfully onboarded new, large partners and expanded its AI-driven lending network, enabling access to more financial opportunities for their customers,” the firm said.

Pagaya, founded in 2016, provides comprehensive consumer credit and residential real estate solutions for its partners, their customers and investors, according to the firm’s website. The fintech has more than 600 employees across two offices in New York and Tel Aviv, Israel.

The firm has been in the real estate business since 2020. Pagaya also offers personal loans, auto loans, credit cards and point-of-sale (POS) financing.

In January 2023, Pagaya acquired proptech Darwin Homes to capitalize on the rental market.

Targeting the single-family rental market, Pagaya shared plans to combine its AI tech and data network with Darwin’s software, operations and mobile app to create a “tech-forward” real estate platform that benefits residents, investors and service operators, the firm said at the time of acquisition.

Home builder confidence took a hit in September as average mortgage rates for a 30-year fixed-rate loan stayed above 7%.

Builder confidence in the market for newly built single-family homes in September fell five points to 45, according to the National Association of Home Builders / Wells Fargo Housing Market Index released Monday. This follows a six-point drop in August.

The monthly index looks at current sales, buyer traffic and the outlook for sales of new-construction homes over the next six months. September’s reading is the first time in five months that overall builder sentiment levels dropped below the break-even measure of 50.

“The two-month decline in builder sentiment coincides with when mortgage rates jumped above 7% and significantly eroded buyer purchasing power,” said Alicia Huey of the NAHB.

Home builder sentiment had been rising earlier this year, riding the wave of demand caused by lack of inventory in the existing home market. But confidence dropped for the first time this year in August, as rates climbed.

In addition, builders continue to grapple with a shortage of construction workers and buildable lots, which is further adding to housing affordability challenges, said Huey.

All three dimensions of the new housing market evaluated saw declines in September: The index gauging current sales conditions fell six points to 51. The component charting sales expectations in the next six months also declined six points to 49. And the gauge measuring traffic of prospective buyers dropped five points to 30.

“High mortgage rates are clearly taking a toll on builder confidence and consumer demand, as a growing number of buyers are electing to defer a home purchase until long-term rates move lower,” said Robert Dietz, NAHB Chief Economist. “Putting into place policies that will allow builders to increase the housing supply is the best remedy to ease the nation’s housing affordability crisis and curb shelter inflation. Shelter inflation posted a 7.3% year-over-year gain in August, compared to an overall 3.7% consumer inflation reading.”

New homes have become an attractive alternative for buyers frustrated by extraordinarily low inventory of existing homes as homeowners hunker down with their ultra-low mortgage rates of 2%, 3%, 4% rather than selling and becoming a buyer at a 7% rate.

As mortgage rates stayed above 7% over the last month, more builders cut prices to boost sales, according to NAHB.

In September, 32% of builders reported dropping home prices, compared to 25% in August. That’s the largest share of builders cutting prices since last December. The average price discount is 6%.

Meanwhile, 59% of builders provided sales incentives of all forms in September, more than any month since April.

This available inventory and price flexibility has gotten the attention of first-time homebuyers.

According to the NAHB, 42% of new single family home buyers were first time buyers so far this year. That’s significantly higher than the 27% of first time buyers purchasing new construction homes during the same time period in 2018, when the market was more typical.

Market trends in the past decade The white paper presented the differences between 2013 and 2023. Mortgage rates were just 3.98% back in 2013 and are sitting at 7.21% year to date. The number of new single-family homes completed in 2013 was 569,000 compared to more than one million in 2023 YTD. The average price … [Read more…]

The interest rate spread between conforming loans and jumbo mortgage rates stood at 1.36 percent this week, according to the BanxQuote Index.

The national average 30-year fixed-rate was as high as 6.63 percent for a conforming loan and 7.99 percent for a comparable jumbo loan, the company said.

That spread is much higher than the typical disparity in rates, which BanxQuote said generally remained within a quarter of a point or less up until August 2007, when the secondary mortgage market collapsed.

“The Jumbo-Conforming Mortgage Spread started widening from 0.16 percent in late July 2007, reaching a peak of 1.90 percent in late March 2008, and narrowing somewhat since then,” said Norbert Mehl, CEO of BanxQuote.

“Nevertheless, this extraordinarily high spread, combined with rising mortgage rates, tighter credit standards and disappearing adjustable rate jumbo mortgages, continues to present a challenging outlook for the housing, mortgage and banking markets, and particularly for the luxury end of the real estate market.”

Adding insult to injury, 30-year fixed-rate loan rates on both conforming and jumbo mortgages are up 0.48 percent and 0.47 percent, respectively, from last week.

A friend I spoke with today who works at Wells Fargo told me that the current rate on a 30-year fixed-rate mortgage is 6.5 percent for conforming, 6.75 percent for conforming jumbo, and 8.625 percent for standard jumbo.

The quoted rate is for an owner-occupied, single-family residence, with a 700 Fico score, 80 percent loan-to-value ratio, and full documentation.

The good news is conforming jumbo loans are actually pricing pretty closely to conforming loans, but jumbo loans above the new temporary loan limits remain extremely high.