Mortgage tech company Xactus announced that its valuation solution Appraisal Firewall X has met federal requirements and is capable of fulfilling Fannie Mae property data collection orders.

Appraisal Firewall X connects mortgage lenders with vetted and trained property data collectors to deliver the value acceptance + property data and hybrid appraisal solutions, the company said in a release.

Fannie Mae’s value acceptance + property data extends an appraisal waiver as long as property data is gathered by a vetted and trained third party and a floor plan is delivered to a desktop underwriter.

Hybrid appraisals require a vetted and trained third party to inspect the property and gather data — including a floor plan — and deliver it to a licensed appraiser for a desktop appraisal. Xactus Appraisal Firewall X provides data for both processes.

Xactus also supports Freddie Mac’s ACE+ PDR (automated collateral evaluation plus property data report).

Freddie Mac’s ACE + PDR program and Fannie Mae’s Value acceptance + property data were designed to increase efficiencies for all stakeholders and lower costs in comparison to traditional appraisals while maintaining the high-risk mitigation standards employed by the government-sponsored enterprises (GSEs).

“At Xactus, we are focused on advancing the modern mortgage and prepared for the future of appraisals,” Shelley Leonard, president of Xactus, said in a statement. “We believe that Fannie Mae’s value acceptance + property data initiative as well as Freddie Mac’s ACE + PDR program will produce a better, more streamlined process for lenders and consumers.”

Fannie Mae’s program is part of its ongoing efforts to modernize the valuation component of the mortgage industry. Upon submitting a subject property to desktop underwriters, the lender will receive a notification indicating the process for which the property qualifies.

Broomall, Pennsylvania-headquartered Xactus, founded in 1928, has over 6,500 clients ranging from the largest bank and non-bank mortgage originators to credit unions and mortgage brokers.

Manufactured housing—prefabricated, factory built homes—can be an affordable option for lower-income homebuyers. But some borrowers may not qualify for mortgages and might have to turn to other kinds of financing with less favorable rates and terms.

Several federal agencies, Fannie Mae, and Freddie Mac have created new or modified existing loan programs to help manufactured home borrowers. But while the Department of Housing and Urban Development has planned program improvements, it doesn’t have a timeline for putting them in place. We recommended it do so.

A manufactured house being transported on a California highway in 2018

Agency Affected

Recommendation

Status

Department of Housing and Urban Development

The Secretary of Housing and Urban Development should ensure that the Commissioner of FHA implement planned changes to provide additional financing options for manufactured homes, including identifying options for greater securitization of manufactured home mortgages and personal property loans and establishing time frames and milestones for the actions. (Recommendation 1)

Open

<label class=”status-code-label”>Open</label><p class=”status-code-description”><p> Actions to satisfy the intent of the recommendation have not been taken or are being planned.</p></p>

When we confirm what actions the agency has taken in response to this recommendation, we will provide updated information.

Department of Housing and Urban Development

The Secretary of Housing and Urban Development should ensure that the President of Ginnie Mae implement planned changes to provide additional financing options for manufactured homes, including identifying options for greater securitization of manufactured home mortgages and personal property loans and establishing time frames and milestones for the actions. (Recommendation 2)

Open

<label class=”status-code-label”>Open</label><p class=”status-code-description”><p> Actions to satisfy the intent of the recommendation have not been taken or are being planned.</p></p>

When we confirm what actions the agency has taken in response to this recommendation, we will provide updated information.

HousingWire Editor in Chief Sarah Wheeler sat down with John Ashley, chief information officer and chief information security officer at PRMG, to talk about what the company is building versus buying, and how regulators are ramping up privacy and security standards.

Sarah Wheeler: Tell me a little bit about your background and what you’ve done at PRMG.

John Ashley: I’ve collaborated with PRMG since late 2005 and my background was network infrastructure and security. In my career, I’ve swung between enabling technology and securing it at the same time.

Within mortgage, we’ve done everything here at PRMG: multiple lending platform LOS systems, multiple changes of those systems, multiple changes of pricing engines, marketing systems, marketing platforms, CRMs, infrastructure security systems moving to the cloud for most of our infrastructure — I’ve been behind all of that over the last 10 to 15 years.

SW: How many tech people do you guys have?

JA: Within the IT department, we have about 60. So, we’re not little, but we’re not big, like some of these companies with 500 developers. We have smaller teams, but they’re very effective.

SW: At PRMG, do you generally build or buy technology?

JA: We do both. We have a development team and so we have software developers, system analysts, business analysts, quality assurance testers, and people that manage deployments. So, we can and do build stuff, but we tend to try to find solutions just for the speed of getting things up and we find ourselves doing a lot of integration or extending systems that we have.

A great example of this is the Encompass platform, which has been around a long time. And while it’s kind of long in the tooth in many respects, ICE has done a fantastic job in building out their back-end developer, connecting their API and micro services. So now you can extend so much from the Encompass platform. And we’ve taken other products and hooked them to Encompass — we have a pretty innovative work queuing system for our fulfillment people, within operations, that’s all been enabled by using a different third-party product. We tend to lean towards buying and extending, but we do a lot of custom stuff as well.

SW: What’s been the biggest change since you started at PRMG in 2005?

JA: I was going back through some old PRMG stuff and they had “the five tenets of mortgage lending success” and it was: product, pricing, compensation, marketing, and fulfillment. Well, technology is now the sixth tenet, because you can’t do any part of the other ones without the technology and that’s where the big change has happened. People are just clamoring for technology to get an edge, especially now.

The biggest shifts are just in the last two or three years. Back in 2020 and into 2021, you could go out in the parking lot with a net and just catch loans. We put a huge amount of effort into building a fantastic CRM platform, but you couldn’t get anyone to touch it — they were all too busy simply getting loans. And then that changed fast. Now, if you’re in the wholesale business, you need to know what every broker is, what all their people are doing, what kind of loans each of them are doing, and what’s your wallet share with every lender.

Of course, if I had to go back and pick a point in time that really changed mortgage data, it was the 2008 mortgage crisis and the regulations that followed. Now every mortgage that’s recorded has a lender name and it’s got the originator’s NMLS number on every single loan. And that enables just a tremendous amount of data that’s available to be collected and used. That didn’t exist before.

That’s how I can take any lender, any broker shop anywhere in the country, and show you exactly what their mix of business is on different types of loans — purchase or refinance — and what percentage is PRMG. I actually have the data.

SW: Let’s talk about the CRM you mentioned. We know that the time to build is in a slower market, but what does that look like?

JA: Well, within the IT world, we’re just as busy now as we were before, even though the business is slower. Before, we were just trying to hang on and keep the rivets from popping out, just from everything going so fast. But now it’s all into rebuilding. So, there is a lot of work on CRM, marketing platforms, but increasingly quite a bit around compliance, especially around privacy. That’s really become a burden.

But I do agree this is a time to build new capabilities when you have this kind of an opportunity. And we’re looking at changing platforms, looking at new point of sale systems, trying on a lot of technology. I mean, I can’t tell you how many people we talk to, and how many products we look at and ideas that we’ve been getting exposed to.

SW: Is there a type of technology that you’re seeing now, that people are pitching you, that you think is new and really exciting?

JA: One good example is we changed our product and pricing engine. We’ve been using the big common one on the market, Optimal Blue, for so many years, since about 2016 when we changed from another one. We wanted to be able to get more out of our product and pricing engine, so we made a shift this year over to a new platform, which is called Polly X. A pricing engine is something no one ever really wants to have to change because the whole world is tied into that: every product, you’ve got every overlay and everything else. And we’re also looking at changes for our wholesale lending technology to help streamline that.

And when it comes to digital marketing, there’s nothing that’s off limits. I would say search engine optimization and customized websites for loan officers, those are areas where we’ve had some success.

The world of lead generation has really gotten tight, we’ve been looking at new ways to get better data there. We will get lower mortgage rates one day, right? So, we’ve been putting time into building and working on technology for call center tech, things of that sort.

And the CRM — we have our main CRM for retail and a different one for wholesale. But we were looking at actually doing some test implementations on a couple of other ones that are more interesting to really high producing loan officer teams.

And of course, lots of integrations — everywhere where you can build a connection. FinLocker is the company that we’ve been working with an integration to offer that kind of capability, they call it a financial locker for borrowers, where they keep all their data. And consumers can work and use tools to improve their credit and then one day they come back as a borrower or repeat borrower. Another company called Credit Evolve is a really legitimate credit counseling service and we try to move people there who need help.

So, we just try not to leave anything on the table. If somebody would have said two years ago, hey, we could have saved 59 loans out of the kazillion loans that we did, nobody would pay attention. But now it’s like, we could have saved 59 loans if we would have followed this process: it means something. It certainly means something in the pocket of those loan officers who can help those people get into a home.

SW: What do you see on the horizon that you think we should be paying attention to now?

JA: First, privacy is a huge area. In Europe, with GDPR, they’re pretty far ahead of us, but our government is catching up really fast. But the biggest thing is just the web of state regulations. Companies that learn how to navigate the privacy landscape are going to have a really strong competitive advantage. But it’s not an easy landscape to navigate. We wrangle with it every week.

For example, you have to have prior written consent from borrowers to do just about anything with their data. Even if you want to help them in some way — like referring them to a credit counselor or getting a homeowner’s policy — you have to have consent to do that. So, you’ve got to build that infrastructure into your system and then you can reuse that process over and over again on your different platforms.

Secondly, when you get into the security realm, that’s become very much a different world with the FTC — they’ve re-released a whole new set of safeguards, guidelines that fully took effect in June. And there are all kinds of new nationwide requirements for all mortgage lenders that are subject to that rule, things like using multifactor authentication, encrypting all of your data, a whole lot of requirements that I know a lot of smaller lenders are struggling with. We’re doing okay on it. But I know the trouble we’ve gone through to get to where we are, and I know how difficult it is, especially for lenders that maybe don’t have that experience.

SW: How does your background in security inform what you’re doing now at PRMG?

JA: I’d like to say it’s just kind of built into all my decision-making. If I was just a security officer, I would probably be more highly focused just there, but I’m also chief information officer, so we have to get things done and business has to move forward, so you have to find solutions.

There’s no perfection. I mean, if you think wow, I’m secure, all you need to do is go to a cybersecurity conference and listen to these guys get up there and tell you how you’re hosed. So there’s no perfection, there’s just best efforts and making sure that your choices are sound and you can document what you’re doing.

My background has served me well, but it’s a steady, long-term path toward building a secure company. It just doesn’t happen overnight or even in a year. It’s a multiyear plan.

SW: How do smaller companies cope with these kind of issues?

AJ: I think that’s going to be a real test now that the regulations are getting more teeth in them. Everyone’s getting into the game, every regulator, state and federal, and not just that, but all of your counterparties — your warehouse banks and the government sponsored entities, they all have their own audits and their own questionnaires. And they’re all checking the boxes and trying to ensure that everybody’s secure out there. So there is a lot of scrutiny and I think over time, smaller companies are going to remain at a disadvantage there.

SW: With your security background, what keeps you up at night?

JA: Actually, I sleep pretty good. But if I had to pick among the small things that bother me the most in the security world, I think it’s what everyone fears: these ransomware takedowns.

Everybody’s afraid of getting their systems encrypted, having someone get control of their data, and everybody has that same risk. And there are companies in the mortgage industry that have been taken down like that — I assume most of them had to pay the ransom.

And then beyond that is just any kind of large-scale data breach. I don’t see how you can really do business in this space without a strong cyber insurance policy, but I know there are companies out there that don’t have them because they can’t get them. We do. But that market is really tough and if you don’t have a good system, and good controls that you can demonstrate to the insurer, then you’re going to have a tough time getting coverage.

SW: What’s exciting about the future of technology and mortgage?

JA: There’s a lot of promise in artificial intelligence and machine learning. Just about everybody in this country is using that technology already — we have it in our cybersecurity systems. And I think the real promise in lending is what you can do to help speed the process: helping borrowers find the right product and helping underwriters in making decisions faster. I think that’s the exciting, fun part.

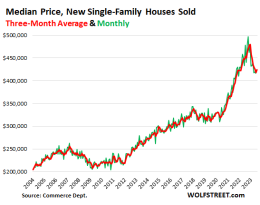

Homebuilders don’t have the luxury of outwaiting the market, or waiting for the Fed to slash rates, or whatever, they must build and sell homes, that’s their business, no matter what the conditions in the market.

And the market is struggling with 7%-plus 30-year fixed mortgage rates and sky-high prices, after a ridiculous free-money spike during the pandemic. Sales of existing homes have plunged by about 25% from the same period in 2018 and 2019, and by about 32% from the same period in 2021, because buyers have pulled back, and the people with 3% mortgages have left the housing market altogether, not putting their homes on the market and not buying homes either, not even looking at homes.

That plunge in sales might be OK with potential home sellers, thinking that this too shall pass, but it’s not OK with homebuilders, and they’ve been adjusting to this market by cutting prices, building at lower price points, buying down mortgage rates, and offering incentives, such as free upgrades.

The latter two – buying down mortgage rates and piling on incentives – don’t show up in the prices of the homes they sell. So the pricing data that we have from the Census Bureau about sales of new single-family houses do not include the costs of mortgage-rate buydowns and incentives.

With mortgage rate buydowns, the homebuilder subsidizes the mortgage payment.

The duration of the buydown can be for a few years, which effectively turns it into a teaser rate that can cause problems when the rate jumps to normal.

Or the rate-buydown can be for the entire term of the mortgage (“permanent”).

The big homebuilders have mortgage-lender subsidiaries that originate the mortgage for their customers and then sell the mortgage to Government Sponsored Enterprises, such as Fannie Mae, which will securitize the mortgages into MBS. For example, the mortgage-lender subsidiary of D.R. Horton is DHI Mortgage Company.

Having their own mortgage lender makes rate buydowns a lot simpler for homebuilders. This is similar to the “captive” auto lenders, such as Ford Credit offering 0% 36-month financing for F-150 XLTs at the moment.

The costs of the mortgage-rate buy-downs can be big, because the home prices are big, and buydowns effectively lower the sales price of the home.

But the costs of buydowns don’t show up in the national median price of new houses sold. The numbers only show the contract prices. July’s median price (green) and the three-month-moving average of the median price (red) of signed contracts dropped by roughly 12% from the peak in late 2022, according to Census Bureau data. Now figure in the cost of rate buydowns, and the prices would have dropped a lot lower:

Concerning the mortgage-rate buydowns, John Burns Research and Consulting, which among other things regularly surveys homebuilders, came out with an interesting note about mortgage-rate buydowns by homebuilders in Florida, based on its regular surveys of homebuilders, phone calls, community visits, etc., plus this time, to supplement the data: “our survey team visited 13 home builders, three land brokers, and a regional developer in Jacksonville and Orlando.”

John Burns chose Jacksonville and Orlando because they’re “more rate sensitive than other Florida markets that attract a higher percentage of retirees who pay all cash and don’t need rate buydowns.”

In a prior note, John Burns said that 5.5% seems to be the “magic number” that makes home sales happen for homebuilders. This is what the survey found:

“Permanent buydown: Buying the 30-year fixed mortgage rate down permanently to 5.25% to 5.75% is making a positive difference in allowing home buyers to qualify for the home purchase.”

“Sub 5%: Builders will even buy the current rate down to 4.75% to 4.99% for inventory homes they want to sell quickly.

“Prepaying for even lower rates: Using a forward commitment, a builder’s mortgage company can originate FHA (Federal Housing Administration) or conforming mortgages at a below-market rate. Often, these buckets of money must be used within 60–90 days, so they work best when builders have nearly completed inventory.

“Temporary buydowns: A couple of Florida builders are using 2-1 temporary rate buydowns (a mortgage rate that is -2% lower in year one and -1% lower in year two) as part of a flex-cash program, allowing buyers to spend the dollars on closing costs, design center options, or a longer rate buydown. A move-up builder sees buyers accepting current elevated rates and planning to refinance when rates drop.

“Managing cancelation risk: One builder requires a 20% down payment from buyers receiving a 30-year rate buydown.

“Good to be big: Smaller production builders may struggle to compete for sales due to limited access or high costs of capital that curb their ability to provide inventory homes and rate buydowns.”

What about profit margins and appraisal issues?

“Builders did not express concerns regarding their margins, even though 30-year rate buydowns are expensive,” John Burns said.

“We have not heard of appraisal issues that could potentially stem from the heavy incentives offered but are monitoring for potential risk,” John Burns said.

And they’re hidden from the national house price data.

In the auto industry, rate buydowns are in lieu of cash incentives, such as rebates or dealer cash, and the customer chooses: either 0% financing or the cash incentives. The cash incentives translate into an explicit lower selling price that the customer sees in the sales contract and that then becomes part of the national data, such as the Average Transaction Price, new vehicle CPI, etc., and ultimately it percolates through to used vehicle values.

John Burns did not say, and I’m not aware of a similar pricing transparency among homebuilders where customers could choose, for example: on a $500,000 house, either a 5% 30-year fixed rate mortgage or, say a $50,000 discount on a deal funded with a 7.3% mortgage.

But the effective price difference due to the rate-buydown doesn’t show up in the numbers. And we don’t know just how far the effective prices of new houses have dropped; and appraisers – according to John Burns – have not yet caught on to it either.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

When you’re looking to purchase your first home, it’s a good idea to familiarize yourself with the different first-time homebuyer programs available in your area. They can help you afford this major purchase.

First-Time Homebuyer Programs

Programs vary in terms of their eligibility requirements and the types of assistance they offer, but all offer some form of financial aid. But what are these programs, and how do they work? Here’s what you need to know.

What Is a First-Time Homebuyer Program?

A first-time homebuyer program is a government-sponsored program designed to help people purchase their first home. Programs vary from state to state, but generally, they offer financial assistance in the form of low-interest rates, down payment assistance, and other incentives.

A few examples include:

The Federal Housing Administration (FHA)

The Veterans Affairs Homebuyer Assistance Program

The National Association of Realtors® (NAR)® Homebuyer Assistance Program

State-sponsored programs, such as the California New Home Grant Program, can also offer assistance.

Who Is Eligible for a First-Time Homebuyer Program?

Each program has its own eligibility requirements, which vary depending on the program and the state in which it is located.

However, generally speaking, you’re eligible if you purchase your first home and meet the criteria set by the program. These criteria can range from being newly divorced, a military veteran, or widowed to having a low income and getting ready to buy your first home. You may be eligible for other programs if you’ve already owned a home. Still, first-time homebuyer programs will automatically disqualify applicants attempting to purchase second homes or investment properties.

Get matched with a personal

loan that’s right for you today.

Learn

more

Related read: What Credit Score Do I Need to Buy a House?

How Do First-Time Homebuyer Programs Work?

Once you’ve determined that you’re eligible for a first-time homebuyer program, the next step is to find a program compatible with your needs. Programs typically offer a variety of incentives, such as low-interest rates or down payment assistance, to help you purchase your home. Once you have found a program you’re eligible for, you’ll need to submit an application and meet eligibility requirements.

Once you have been accepted into the program and met eligibility requirements, you’ll need to begin preparations for your home purchase. This may include searching for a qualifying home and making any necessary financial commitments. Finally, once all of the paperwork has been completed, and your financing has been approved, you can go ahead and purchase your home.

How Can I Use a First-Time Homebuyer Program?

There’s no one definitive answer to this question, as each program has different requirements and guidelines. However, if you’re approved for financial assistance, then the money will be given to help you purchase a home. Typically, these programs aren’t for rehabbing a home or house flipping. If you need help making repairs, consider instead getting a personal loan to finance home improvement. You’ll have a higher likelihood of getting approved for help covering repairs than a homebuyer’s program would offer.

The Bottom Line

A first-time homebuyer program can help you get into the market quickly and easily. They offer many benefits, including reduced interest rates and fees, waived closing costs, etc.

Are you quickly approaching the limit of your unemployment benefits? We’ve created a quick guide here to help walk you through your next steps. In this article, we’ll show you how to create a financial action plan, and then we’ll guide you through the latest extension to unemployment benefits. Finally, we’ll explain a few government-sponsored programs, some of which could help you make ends meet.

What Does It Mean to Exhaust Your Benefits?

Individual states manage and regulate their own unemployment benefits policies and requirements. On average, these benefits last for 26 weeks or about 6 months.

When you apply for unemployment benefits, caseworkers review your case and approve or disapprove benefits. If approved, a maximum amount is set for the value of benefits you can receive while you’re approved for benefits. Once your benefit payouts reach this maximum amount, you’ve exhausted your benefits.

What to Do If Your Benefits Are Exhausted

Once the unemployment office notifies you that your benefits are exhausted, you won’t receive any more payments after the designated date. This doesn’t mean you don’t have other options. Depending on your state regulations, you may be able to reapply for unemployment benefits.

If you receive a letter stating your benefits are ending or your renewal application for benefits has been denied, you have the right to file an appeal and try to overturn this decision. Instructions for how the unemployment benefits appeals process works in your state should come with your letter. Typically, you must submit a detailed letter explaining why you believe your benefits should be reinstated.

While you are waiting for the appeals process, consider applying the following steps. Think of them as a backup plan if the appeals process doesn’t go the way you want:

1. Create a Financial Action Plan

Before you do anything else, create an emergency financial action plan. You might not be able to overhaul your finances completely—but you can stem the flow of money to some degree. You might be able to shave a few dollars off your expenses every month, or temporarily stop making mortgage or loan payments. Here are a few ideas to get you started:

If you feel frustrated or helpless between jobs, create a daily schedule to motivate yourself—and stay as physically and mentally active as you can.

2. Apply for Government Assistance Programs

If your unemployment benefits run out, there are numerous other government assistance programs that may provide financial aid. Below is a look at several of these programs. In many cases, you can check your eligibility or even apply for these benefits online.

WIC

The Women, Infants, and Children, or WIC, program is a federal nutrition program that provides healthy foods to women who are pregnant or breastfeeding and children under the age of 5. The program gives eligible participants coupons they can exchange at the grocery store for specific food items, such as milk, cheese, and cereal.

SNAP

The Supplemental Nutrition Assistance Program, or SNAP, provides low-income families with financial support to purchase food. To be eligible, you must meet specific income guidelines and resource limits. This support can help cover a portion of your grocery budget until you can secure a job.

Medicaid

If you don’t currently have health insurance, you may want to see if you qualify for Medicaid. This health insurance program helps income-eligible adults and children obtain health insurance. While Medicaid is a federal government program, each state sets its own eligibility guidelines. If you’re currently not working or working limited hours, you may qualify for Medicaid.

CHIP

If you don’t qualify for Medicaid, you may still be able to obtain health insurance for your children under the Children’s Health Insurance Program, or CHIP. In some states, pregnant women may also qualify for CHIP. There are no waiting periods or open enrollments with CHIP insurance. Instead, you can apply for this insurance at any time throughout the year.

Social Security Retirement

If you’re aged 62 or older, you may qualify for Social Security retirement payments. You should talk directly to a representative at your local Social Security office to find out how much you can earn a month on Social Security if you retire right now. Keep in mind that the longer you wait to start collecting Social Security, the higher your monthly payments may be.

Social Security Disability

If you have a medical condition that prevents you from working and is expected to last longer than 1 year, you may qualify for Social Security disability, or SSID, payments. The application and approval process can take 6 months or more, so it’s recommended to apply for these benefits as soon as possible if you believe you qualify.

SSI

If you or one of your dependent children has a medical condition that prevents or limits you from working but you’re low-income or don’t have enough work credits to qualify for SSDI, you may qualify for Supplemental Security Income, or SSI. If eligible, you can receive monthly payments and typically qualify for Medicaid automatically.

State and Community Benefits

Depending on where you live, there may also be a number of state and community programs that can provide extra support until you can find a job. For example, many local communities have food pantries and soup kitchens that may be able to provide you with supplemental food options. Some states also offer reduced or free internet and mobile phone services to low-income families. Your local public assistance office or county government offices should provide a list of services for you.

Grants, Scholarships and Loans

If you decide to use your time off to acquire new skills through a training or college program, you may be eligible for various grants, scholarships, and student loans. In some cases, the combination of these programs can cover your cost of living while you’re in school.

Housing Choice Voucher Program (Section 8)

Losing a job can make it difficult to keep up with your rent payments and put you at a higher risk for eviction. To help low-income families maintain secure housing, many states have a Housing Choice Voucher Program, also referred to as Section 8. If you qualify, this program can cover a portion or all of your rent to ensure you don’t lose your housing. Many areas have a waiting list for this program, so it’s recommended to apply for these benefits as early as possible.

3. Look into Self-Employment Assistance Programs

If you’re self-employed, you might be eligible for PUA and PEUC. Other programs, including grants and loans administered by the Self-Employment Assistance Program (SEA), are also available. Reach out to your nearest Secretary of State office to learn about state-centric programs for self-employed people and small business owners.

4. Consider Freelance or Part-Time Work

If you’re currently unemployed and finding it tough to get another job, you could consider part-time or freelance work—or you could start your own small business. Here are a few ideas to get you started:

You might find a permanent full-time job again soon, but why not use this time to study, or to try something completely new? To learn new skills at home, check out Coursera, and create a ZipRecruiter profile to keep looking for employment online.

5. Reach Out for Help

If you’ve gone through all the suggestions listed above and nothing feels doable, reach out for help. Resources like United Way 2-1-1 can help you find ways to pay for food, housing, medical, and financial expenses. Local charities, churches, and community organizations might also be able to help.

What Are Extended Benefits?

Extended benefits are extra benefits the government offers in emergency situations. For example, when the pandemic hit, many states offered extended benefits to deal with the high unemployment levels.

Will Unemployment Benefits Be Extended Again?

While pandemic-related extensions are now over, that doesn’t mean an end to unemployment benefits extensions. If unemployment rates are particularly high in a specific region of the country, the government may decide to offer extended benefits. If these extended benefits are in place, it allows you to receive benefits for a longer period.

Can I Get an Extension on Unemployment Benefits If I Have Exhausted My Benefits?

If your unemployment benefits have been exhausted, you may qualify for extended unemployment benefits if they’re available in your area. To apply for these benefits, you must complete the application. In many states, this application is online. If your area isn’t currently offering extended benefits, you can reapply for unemployment benefits to see if you qualify. If you think your benefits ended too soon, you can always appeal the decision.

LAS VEGAS – With mortgage rates headed to 8%, the current housing slump is unlikely to reverse course until 2025, due to the Federal Reserve’s continued ratcheting up of interest rates, mortgage experts said at a conference in Las Vegas.

Analysts continue to warn about overcapacity in the industry with too many lenders and employees to support current origination volumes.

Federal Reserve Chair Jerome Powell signaled last week that interest rates need to stay higher for longer to tame inflation and that it could raise interest rates once more this year. The Fed’s policies have hit potential homebuyers the hardest as mortgage rates approach their highest levels in 23 years, analysts said.

“If the Fed keeps rates where they are today, then I think you’re going to easily see 8% mortgages because the survivors in the mortgage market — once we get rid of another 50% of capacity — are going to want to make money and that’s how they’re going to do it,” said Christopher Whalen, chairman of Whalen Global Advisors, on Tuesday at the National Mortgage News Digital Mortgage conference in Las Vegas.

Mortgage industry analyst Christopher Whalen, left, and Julian Hebron of the Basis Point, center, discuss housing policy with the former head of the Federal Housing Finance Agency Mark Calabria, right, during the National Mortgage News Digital Mortgage Conference on September 26 at the Wynn Resort in Las Vegas.

Whalen was joined by Mark Calabria, a senior advisor at the Cato Institute and the former director of the Federal Housing Finance Agency, in a debate about current public policy and its effect on the mortgage market.

Calabria said the main obstacle to buying a home is finding a house that is affordable. He questioned the Biden administration’s public policy approach, which is focused primarily on providing access to credit to low and moderate-income communities at a time when mortgage rates are above 7% and home prices are still rising due to a lack of inventory.

“There’s just too much tension in Washington where the sense is that we’re going to make the mortgage market and mortgage policy the answer to all these other unrelated things which are real — there are very real social injustices we should fix — but the mortgage market is not the solution for all of them,” Calabria said. “I worry that mortgage policy is bearing the weight of trying to fix a number of things that really have very little to do with the mortgage markets.”

Calabria, the author of “Shelter from the Storm: How a COVID mortgage meltdown was averted,” described how he resisted repeated calls for a bailout of mortgage servicers early in the pandemic. The Federal Reserve had stepped in with a broad array of actions including lowering interest rates, sparking a massive refinance boom in 2020 and 2021. Calabria then applied an adverse market fee to refinances but exempted lower-income borrowers.

Julian Hebron, founder of the Basis Point, a consulting firm, and veteran mortgage executive, questioned whether the FHFA should be setting pricing in the mortgage market and asked whether it’s “appropriate for GSEs to raise fees to build capital to prepare for downturns.”

Calabria said the government-sponsored enterprises should be charging so-called g-fees for guaranteeing the timely payment of principal and interest on mortgage-backed securities because doing so covers projected credit losses from borrower defaults over the life of a loan.

“Ultimately, I don’t think the regulator should be driving prices,” Calabria said.

He also said Fannie Mae and Freddie Mac will remain in conservatorship for the foreseeable future but also envisions a way out of government control — by having the GSEs raise fees.

“If you’re a CEO of one of these companies, it sucks being micromanaged, and I know that as somebody who micromanaged the CEOs,” he said. “If I was the CEO of one of these companies and I had the freedom to do it, I would jack up G-fees so I can build capital and get out two or three years earlier than I would otherwise. Because again, it sucks being in conservatorship for these companies, at least at the top.”

Calabria took office in 2019 and sought to end government control over Fannie Mae and Freddie Mac, which guarantee 70% of the roughly $12 trillion U.S. mortgage market. Though Calabria was confirmed by the Senate to a five-year term, he was fired in 2021 by President Biden following a Supreme Court ruling. Biden named Sandra Thompson as Calabria’s successor.

Whalen laid the blame for the current high interest rate environment squarely on the Fed and its actions in dropping rates in response to the pandemic. Roughly 90% of homeowners currently are locked in to mortgage rates below 6% and many are paying less than 4% on loans that were refinanced when the Fed held interest rates near zero. As a result, homeowners are not selling their properties, resulting in record-low inventory and a general gumming up of the mortgage market in a high-rate environment.

“The trouble is that the Fed’s actions through COVID distortéd the market so much that lenders are losing 200 to 250 basis points on every loan they make,” said Whalen. “Even though the agencies and the FHA subsidize the cost of mortgages, that’s really what they do, it’s not about getting a mortgage, it’s about how much does it cost every month, which goes across every product in America.”

Many forecasts that are well-founded in data have been upended by major events, such as COVID or a bank failure. Whalen said that the only way mortgage rates could get down to 6% or 6.5% in the near-term is if there is another bank failure.

“If we see another surprise in the banking market, the Fed is going to be forced to back off,” said Whalen, adding that he is concerned that interest rates are making asset prices go down. “If we see another failure, they are going to probably have to turn to the Treasury for support or tax the industry to raise cash because there won’t be three or four buyers out in the room.”

Inside: Are you looking for a way to help your kids learn about money? If so, Cash App for kids is the ideal answer. This guide will teach you how to manage money simply by using apps.

Ever wondered why it’s crucial for your kids and teens to have a cashless payment option?

In this digital age, teaching money management skills early to our younger generation is vital.

Having features likeCash App for kids is a great way to introduce them to responsible spending. Not only does it provide a secure method for purchases without the need for carrying physical money, but it also serves as an excellent tool for setting spending limits and tracking budgeting habits.

Plus, it’s a win-win for parents and teens as you can visually monitor transactions while they enjoy a sense of financial independence.

This post may contain affiliate links, which helps us to continue providing relevant content and we receive a small commission at no cost to you. As an Amazon Associate, I earn from qualifying purchases. Please read the full disclosure here.

What is Cash App?

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

It offers a range of services including a free custom Visa debit card and the option to receive paychecks up to two days earlier.

Additionally, with the Cash App, users can instantly buy and sell stocks commission-free and even trade in bitcoin.

Can a child have Cash App?

Yes, a child can have a Cash App account if they are 13 years old or older. However, it requires parental approval.

Remember, this gives your child the opportunity to learn money management, but it also comes with the responsibility of overseeing their spending.

Why would kids need Cash App?

Well, we are moving to a cashless world. There are thousands of stores and restaurants that only offer cash. We learned this when our son went to an MLB baseball game with his middle school. No cash. Only debit or credit cards were accepted as well as Visa gift cards.

So, we needed to give our kids an introduction to modern, simple, and secure ways of money management.

Cash App might be the perfect solution. Another great option is Greenlight for kids.

Cash App – Do More with Your Money

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

What are the benefits of using Cash App for kids?

Education: Cash App can be an effective way to teach your children about responsible money handling and the dynamics of a digital economy.

Control: You have the flexibility to set spending limits and disable certain features, ensuring responsible use of the application.

Security: Cash App’s encrypted connection adds an extra layer of security, keeping your kid’s transactions and personal data secure.

Emergencies and convenience: It’s an incredibly handy tool for sending cash to your kid during emergencies. No need to rush, just a tap on your phone, and you can send money.

What cash apps can 13 year olds use?

In today’s cashless society, it’s more important than ever for kids to learn how to manage money digitally.

Below are some alternatives to Cash App that serve well for 13-year-olds:

Description:

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track your child’s spending and saving habits.

Learn to earn, save, and invest together. The banking and investing app for kids and teens.

Comes with a debit card

Allows kids to make savings goals.

Limited deposit methods

Monthly fee

Starts at $4.99/month

Description:

Prepaid cards and a family finance app for kids, teens, and parents.

More than money.

A financial education.

If you want your child to learn money habits that match your values, you’re in the right place.

Description:

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

Description:

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track your child’s spending and saving habits.

Learn to earn, save, and invest together. The banking and investing app for kids and teens.

Comes with a debit card

Allows kids to make savings goals.

Limited deposit methods

Monthly fee

Starts at $4.99/month

Description:

Prepaid cards and a family finance app for kids, teens, and parents.

More than money.

A financial education.

If you want your child to learn money habits that match your values, you’re in the right place.

No bank account needed.

No fancy phone needed.

Affordable for all! Plus free trial!

Mobile setup is not user friendly.

No investing option.

$5.99 month or $3.33/month for 12 months

Description:

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

Only able to spend what is loaded on Card.

Free CashApp debit card.

No maintenance or annual fees.

Not FDIC insured.

No parental controls.

Remember, each app has its own unique strengths and weaknesses. Do some research and try out a few to see which one best suits your teen’s financial needs.

How do I create a Cash App account for my child?

Teaching kids about money management is vital for their financial future.

One excellent way to do this effectively is by setting up a Cash App account for children, giving them practical experience in handling finances while under a parent’s supervision. Also, known as a sponsored account.

This guide will walk you through the process of creating a Cash App account for your child and highlight the numerous benefits it offers.

Step 1: Download Cash App

To download Cash App, click this Cash App link to make sure you are in the right spot. Both you and your teen will need to do this step.

It’s easily recognizable – look for the white dollar sign on a green background. Once you’ve found it, simply hit ‘Install’ and sit back while your phone does the work.

Remember, this green goodness is only accessible to users in the United States.

When learning which payment type is best when trying to stick to a budget, you will be pleasantly surprised at how well Cash App works.

Step 2: Create an Account

This is a simple process. Both the teen and the adult will need to do this step separately. If as the parent you don’t have a Cash App account, then you will need to do this step.

To create a Cash App account, follow these steps:

Once installed, open the application and follow the on-screen instructions to set up your account.

You will have to enter your phone number or email address.

For security certification, the Cash App will send you a secret code to verify you. Enter it.

Select a $cashtag, which is a unique username to send and receive money (similar to Venmo)

Step 3: Connect a Bank Account

For the parent account, you need to complete this step and the teen will need to wait.

Remember, in “My Cash” you’ll spot the “Add Money” option for funding.

Open Cash App; it’s the icon with a white dollar sign on a green background.

Tap the top-right profile icon.

Navigate to “My Cash” – it’s a tab on the home screen.

Click “Link a Bank,” nestled within the options.

Follow the prompts to add your bank account or debit card info.

Once your card is linked, you’re all set.

Learn where can I load my Cash App card.

Step 4: Authorization Request of a Family or Sponsor Account

Now, you must link the two accounts together. Cash App calls this a sponsored account. There are one of two ways to accomplish this.

Option #1 – Parents Initiate the Request

To invite someone 13-17, then open the app:

Tap the Profile Icon on your Cash App home screen

Select Family

Tap Invite a teen

Follow prompts to share links using text or email

Option #2 – By the Teen

On the Home Screen, tap the Cash App profile icon.

Proceed to Family Accounts and choose the option “I’m a Teen”.

Complete the Cash App for Kids application form with your details including your name and birthday.

Hit the Request Approval button.

Enter the name, email, phone number, or $CashTag of your parent/guardian.

Lastly, tap Send. This will send an authorization request to your parent or guardian’s Cash App account. They need to approve this request before you can start using the app.

Note: You can’t add funds, send payment, or request a Cash Card until this authorization is approved.

Step 5: Have Your Child Design and Order a Free Cash Card

Now, the fun part! Ordering your own Cash App Card.

Designing and ordering your Cash Card is packed with creativity and ease.

Customize your card to represent your unique personality, with choices ranging from the material, font size, and base design, to text lines.

You can seek inspiration from an array of cool Cash App Card design ideas. Notably, the glow-in-the-dark cards are quite popular among minors.

The whole process is about making your debit card unmistakably yours.

Step 6: Limitations on Certain Features

Certain financial apps cater to teens by setting limits on transactions.

For example, a teen on Cash App can send and receive up to $1,000 every 30 days. This safeguard is designed to prevent overspending and encourage smart budgeting practices.

Furthermore, parents and guardians have the option to impose their own customized spending limits through the app according to their teen’s financial maturity. However, it’s essential to keep in mind, that these apps are not recommended to be used by teens just like regular accounts due to the risks of misspending and overspending.

Be aware that certain transactions are blocked, including bars, dating services, and rental car services

Encourage your kids to use robust, unique passwords and activate features like PIN lock and facial ID to enhance security.

You can ensure safety by setting a PIN, turning on notifications, and limiting money requests to ‘contacts only’.

This is similar to understanding the advantages of mobile phones for kids.

Step 7: Pick a unique $Cashtag

Tell your child to select a unique and fun $Cashtag for their Cash App account. It’s like a username and can be used in transactions.

Emphasize the originality of the $Cashtag as it needs to be unique.

Expert Tip: To secure their $Cashtag, avoid using personal information like birthdate or social security number. Instead, opt for quirky, fun, and uncommon word combinations.

Step 8: Send & receive money

Cash App provides an easy-to-use platform for instantly transferring money between friends and family at no cost.

A few quick taps allow users to request, receive, or send money, presenting a convenient method for paying a dinner, settling rent with roommates, or any other financial interactions.

In addition, users get a free custom Visa debit card, which they can order directly from the Cash App for both virtual and physical use. The card enables users to make purchases from any merchant accepting Visa cards.

Plus, with the Cash Boost feature, users gain from immediate discounts at select restaurants, stores, applications, and websites when they use their Cash App card.

An Alternative – Use Greenlight Debit Card for Kids

Looking for an all-in-one alternative to the Cash App for your kids?

Explore the Greenlight Debit Card for kids – a superb choice for money management and financial education.

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track their child’s spending and saving habits.

Plus it offers 1% cash back on all purchases and up to 2% interest on savings, this card is accepted anywhere MasterCard is used and comes with built-in features that include educational programming and real-time notifications for every transaction.

Greenlight

The Greenlight debit card is a kid-friendly financial tool designed for comprehensive money management education.

Parents can monitor and control card usage, set spending limits, and track your child’s spending and saving habits.

Pros:

Offers a comprehensive financial education pathway

Broad acceptance due to affiliation with Mastercard

Parents retain control over spending limits

Real-time notifications improve security

Cashback rewards are an added bonus

Cons:

Greenlight charges a monthly fee starting from $4.99

Limitations on direct deposits

No possibility for payments from Paypal, Venmo or Apple Cash

Kids under 13 require parental access

Some transaction types are blocked

It’s an innovative and secure financial platform for kids, with plans starting at $4.99 a month.

Safety Measures for Using Cash App for Kids

Educating children about safety measures while using cash apps and debit cards is crucial in today’s digital age.

With increased online scams, it’s important that kids understand the equivalence of digital cash to real money and how to protect their accounts.

This brief overview will highlight key practices to ensure your child’s safety when handling digital transactions.

1. Know the App’s Safety Features

Knowing the app’s safety features is crucial for maintaining security while using cash apps.

These features can include password protection, two-step verification, and biometric scans such as fingerprint or facial ID. Many apps also offer robust encryption to secure data and transactions.

Keeping abreast of the app’s safety protocols not only helps safeguard against potential scams but also instills a better understanding of digital literacy. Understanding these safety measures and functionalities can greatly lessen the likelihood of falling victim to fraudulent activities.

Make sure they don’t learn how to unlock borrow on CashApp!

2. Talk to Your Kids About Money

It is essential to talk to your children about financial literacy from an early age especially if your parents never spoke about money.

Start by making them aware of the concept of saving by using tools like a piggy bank and elucidate the value of delayed gratification.

As they mature, introduce them to the functionalities of debit cards and apps like Cash App that provide hands-on experience in managing finances. Teach them about budgeting, saving, and investing in an age-appropriate manner.

Above all, impart the message that money doesn’t just grow on trees and that every purchase needs to be evaluated against future needs and plans.

3. Use Account Alerts to Stay Up to Date

Account alerts on Cash App are not only handy but critical to your kid’s financial safety. Setting them up is a breeze.

Firstly, head to the “Notification” tab in your app settings.

Thereafter, opt for “Account alerts” and switch it on. This will ensure you’re notified of all transactions.

For an added layer of security, enable “Suspicious activity” alerts; this helps to flag any odd movements swiftly.

4. Set Up a Strong Account Passwords

It is crucial to ensure that your online accounts are secured with robust and unique passwords.

Complex passwords that incorporate a mix of uppercase and lowercase letters, numbers, and special characters can provide a strong line of defense against unauthorized access. Also, you should look at changing these passwords regularly, which further enhances security.

Using a password manager, either online or paper-based, can assist in maintaining and keeping track of different account credentials, maximizing security while minimizing the risk of forgetting passwords.

However, if opting for a paper-based version, it is crucial to store it in a secure and confidential location to prevent unauthorized access.

5. Have a Conversation About Scams and Fraud

The proliferation of digital transactions and cash transfer apps has given rise to numerous scams, making it critical for users to look out for fraud.

Online scams can result in financial loss, with cash apps often not assisting in the recovery of misdirected funds due to errors or fraudulent activities.

Additionally, cybercriminals use these scams to steal personal data, leading to issues like identity theft and fraudulent transactions. Furthermore, the anonymity of digital platforms enables scammers to disappear without a trace after executing a scam, sometimes befriending and exploiting minors.

Therefore, everyone must stay vigilant about potential scams to protect their money, personal information, and overall digital safety.

Key Tips to Watch for:

Discuss current scams happening. Use reliable resources to educate them about how fraud works and precautions to take.

Teach them to *slow down* during transactions to avoid sending money to the wrong contacts.

Advise against sending money to strangers to avoid being scammed.

6. Check Bank Accounts for Any Unauthorized Payments

As a parent, it is essential to regularly check your teen’s checking accounts linked to their mobile wallet for unauthorized payments.

By staying vigilant, you can detect suspicious activity early and prevent possible instances of fraud.

Tracking their spending patterns also helps you understand if they are managing their digital money wisely or if there are sudden changes in their spending habits.

Remember, it is better to be proactive in monitoring these accounts, as most money transfer app funds are not FDIC insured, making the recovery of accidental transfers or payments a challenging task.

7. Ability to Give Your Kids an Allowance

If you choose to do so, giving your kids an allowance on Cash App is a safe and effective way to teach them about responsible money management. It provides hands-on experience while putting the power of monitoring in your hands.

To set this up, simply create an account for your minor and periodically send money to it as an allowance. They can spend or save it, while you observe their spending habits.

This is a simple way for kids and teens to start managing a small amount of money.

Cash App – Do More with Your Money

Cash App is a user-friendly financial services platform that allows users to instantly send, receive, and invest money.

Simple way to save on everyday spending and back the way you want.

Which cash app will you choose for your kids

To sum it up, equipping your kids with financial responsibility via Cash App or Greenlight is an intelligent move.

These apps provide a platform for learning about savings, investments, and the value of money.

Although risk exists its potential scams, with proper guidance, your teen can safely navigate this. The added perks of trading, direct cash exchanges, and options like BusyKid and Bankaroo can further enrich their financial literacy journey.

So, which digital wallet will you pick for your kid’s first leap into financial independence?

Know someone else that needs this, too? Then, please share!!

Colorado-based lender Loan Simple brought on Jim Anderson as its new chief marketing officer.

Anderson, who started the new role in September, will oversee all aspects of the firm’s marketing, branding and demand-generation efforts.

“With over 20 years of experience at Finance of America (FoA), Stearns Lending, Certainty Home Loans, CNN, Accenture and The Weather Channel, he brings innovative, business-building, marketing strategies to Loan Simple,” the company said in a LinkedIn post on Thursday.

Anderson brings nearly seven years of experience in the mortgage industry with his latest stint as CMO at FoA.

He spent more than two years at FoA where his responsibilities included setting a strategic marketing vision, plan and budget, and overseeing a team of on and offshore marketing professionals.

Prior to Finance of America, Anderson held CMO positions at Stearns Lending and Certainty Home Loans. Anderson won HousingWire’s Marketing Leader Award in 2021.

Loan Simple originated $411 million in production volume across 1,293 loans in 2022, according to mortgage data platform Modex. The lender has 71 sponsored MLOs with 14 active branches across the country, according to the Nationwide Multistate Licensing System (NMLS).

Are you looking for the best side jobs for teachers? Teaching is a great career choice and teachers are very much needed in the world. Unfortunately, though, it is not the highest-paying job that exists. Due to that, you may be looking to find ways to make extra money as a teacher. Side hustles for…

Are you looking for the best side jobs for teachers?

Teaching is a great career choice and teachers are very much needed in the world. Unfortunately, though, it is not the highest-paying job that exists. Due to that, you may be looking to find ways to make extra money as a teacher.

Side hustles for teachers are great because they can help you make extra income, pay off debt, save for a vacation, and more.

Teachers have many useful skills, which make them a great fit for many different side hustles alongside their main teaching job.

Quick Summary on Side Jobs For Teachers:

Online tutoring and selling lesson plans are popular side jobs for teachers that use their existing skills

Selling crafts, selling printables, or teaching online courses can be a nice creative outlet

Short-term and seasonal side gigs like coaching sports or teaching summer school may be better for your schedule than year-round gigs

Best Side Jobs For Teachers

There are 36 side jobs for teachers listed below. If you want to skip the list, here are some jobs that you may want to start learning more about first:

Below are 36 side hustles for teachers.

1. Sell educational printables

Selling educational printables can be a great way for teachers to make extra income and it is great for anyone who wants to learn how to make passive income as a teacher.

An educational printable is a teaching resource, either digital or physical, that educators create to help with learning.

Other teachers buy these for their classes and so do parents.

Educational printables are things like math problems, vocabulary cards, and science experiments. They work for different grades and learning goals, making it an easy way to add to regular teaching or homeschooling. You can share these resources online or print them for in-person classes, making them a helpful tool for improving education.You can learn more at How I Make $400,000 Per Year Selling Educational Printables.

Do you want to make money selling printables online? This free training will give you great ideas on what you can sell, how to get started, the costs, and how to make sales.

2. Tutor online or in person

Tutoring services or helping kids get ready for standardized tests either online or in person can be a great side hustle for teachers.

This option can be a natural fit, as you can use your teaching skills to tutor students.

To start, check out different online tutoring websites like Tutor.com or you can also do in-person tutoring sessions. For in-person tutoring sessions, you can contact local tutoring companies or promote your services on social media or in local Facebook parent groups for your area.

3. Sell your lesson plans

As a teacher, you already make lesson plans for your classes. You can actually sell your lesson plans, earn extra money, and help other teachers.

The most popular platform for this kind of side job is Teachers Pay Teachers (TPT). Here, you can upload your lesson plans, activities, assessments, and other educational resources. Each time someone purchases one of your items, you’ll earn some income.

Lesson plans need to be well-organized, easy to understand, and tailored to specific grade levels and subjects (such as fifth grade math). You should include clear objectives and step-by-step instructions to make your lesson plans more appealing to potential buyers.

4. Coach a school sport or other after-school program

Coaching a school sport is something that you can do within your own school district as many schools are in need of help with their sports teams.

Some sports and after-school programs that can be a teacher’s side hustle include soccer, basketball, volleyball, and track-and-field, as well as clubs such as yearbook, chess, choir, and more.

5. Start a dog bakery

Starting a dog bakery can be a fun side job for teachers who love both dogs and baking.

You can make an extra $500 to $1,000, or even more, each month by making treats for dogs. You can make dog treats like cupcakes, cookies, cakes, and more.

You can learn more at How I Make $4,000 Per Month Baking Dog Treats (With Zero Baking Experience!).

6. Sell crafts on Etsy

Selling crafts on Etsy can be a great way to make extra money by being creative.

Etsy is a website where people from all over can buy and sell handmade and digital products.

Some ideas for products you can create and sell on Etsy that are teaching-related include:

Classroom decor items

Educational games and activities

Customized planner pages and stickers

Flashcards and study materials

Of course, you can create things that aren’t related to teaching at all, such as knitwear, jewelry, and more.

7. Sell on Teachers Pay Teachers

Teachers Pay Teachers (TPT) is a site specifically for educators to buy and sell educational materials, and this is a popular teacher side hustle. If you’ve developed lesson plans, worksheets, or other teaching tools for your classroom, you can share and earn from them on TPT.

I know I talked about selling education printables and lesson plans above, but I want to talk more about Teachers Pay Teachers in its own section because it is such a popular teacher side hustle.

You can sell:

Lesson plans and unit studies

Worksheets and printable activities

PowerPoint presentations and interactive notebooks

Posters, charts, and visual aids

For example, I looked on Teachers Pay Teachers and searched for third grade lesson plans. There, I found over 49,000 results such as math lesson plans about rounding, substitute teacher plans for third graders, reading comprehension lesson plans, and more. Here’s an example of one that you can look at.

The average teacher on Teachers Pay Teachers can make around $300 to $500 extra, but there are some teachers that make hundreds of thousands of dollars extra each year.

8. Babysit

As a teacher, you may find that babysitting is an easy side job to pick up, and, depending on where you live, you may be able to earn around $15 to $25 an hour. Parents love hiring teachers as babysitters because they have so much experience with children.

While babysitting, you’ll find that your existing skills from teaching make a difference in providing the best care possible.

9. Teach English as a second language online

Teaching English as a second language (ESL) online is a popular side job for teachers. As an online ESL teacher, you can help students learn English and work from home.

Most jobs require you to be a fluent English speaker with a bachelor’s degree.

10. Teach summer school

One of the obvious ways for teachers to make extra money in the summer is to teach summer school.

It’s a great way to make use of your teaching skills while earning extra income. Plus, summer school takes place during summer break, so it should fit well with your schedule of already being off from school.

11. Summer camp counselor

Another great option during the summer months is to become a summer camp counselor.

As a counselor, you’ll supervise children in activities such as sports, arts, and crafts. Camps are always looking for instructors with teaching experience, making this a good side job for educators.

12. Grade papers

Grading papers as a side job may appeal to you if you’re looking for a more flexible, at-home option.

Companies such as Measurement Inc. hire teachers to grade student work, such as essays and test answers.

They are hiring evaluators to score in the subjects of English, mathematics, science, and more and pay starts at $15 per hour.

13. Work at a restaurant

If you’re looking for something completely different from teaching, you could take a part-time job at a restaurant.

Working in restaurants can be a good fit for teachers because they often offer flexible hours that can align with your teaching schedule. You can choose jobs like being a server, host, and more.

14. Proofread

As a teacher, you are probably already a great proofreader and are able to spot mistakes easily. With these skills, proofreading can be a great side job. By proofreading, you can help authors, website owners, students, and more improve their writing while earning some extra income.

Even the most skilled writers can make mistakes in grammar, punctuation, and spelling. That’s why hiring a proofreader can be very helpful for pretty much anyone and everyone.

If you want to find online proofreading jobs, I recommend watching this free 76-minute workshop all about how to get started proofreading.

Recommended reading: 20 Best Online Proofreading Jobs For Beginners (Earn $40,000+ A Year).

15. Blog

Blogging can be a fun way for you, as a teacher, to make extra money from home. Many blogs are run by teachers, and I completely get why – you can blog in your spare time and you don’t have to stick to any formal schedule.

To start your own blog, first, choose a topic that you’re interested in writing about, maybe something related to your teaching field or a hobby you enjoy.

You can make money from your blog in ways such as:

Affiliate marketing – Share links to products or services related to the topic you are writing about, and earn a commission for sales generated from your referral links.

Advertising – Include display ads or sponsored posts on your blog.

Courses and ebooks – You can create courses or ebooks related to your area of expertise, and sell them through your blog.

Since I began Making Sense of Cents, I’ve made more than $5,000,000 from my blog, and it all started as a side job.

Learn more at How To Start A Blog FREE Course.

Similar to blogging, a teacher could also start a YouTube channel, a TikTok, and more.

16. Freelance write

If you are looking for side jobs for teachers from home, then becoming a freelance writer can be a great choice.

Freelance writers write content for blogs, websites, magazines, newspapers, advertising companies, and so much more.

You can find different writing jobs on platforms like Upwork and Fiverr, or even find clients on your own, such as by reaching out to websites that you are interested in writing for.

Recommended reading: 14 Places To Find Freelance Writing Jobs – (Start With No Experience!)

17. Transcribe

An online transcriptionist’s job is to listen to video or audio files and then type out everything that they are hearing. There are many different types of transcriptionists, such as legal, general, and medical transcriptionists.

This job requires strong typing and listening skills, and you can work from home on your own schedule.

Transcriptionists earn around $15 to $30 per hour on average.

I recommend watching FREE Workshop: Is a Career in Transcription Right for You? You’ll learn how to get started as a transcriptionist, how you can find transcription work, and more.

Recommended reading: 18 Best Online Transcription Jobs For Beginners To Make $2,000 Monthly

18. Flip used items for resale

Flea market flippers find underpriced items at flea markets, yard sales, and thrift stores, then resell them for a profit. This job requires a good eye for finding valuable items that you believe can be sold for a higher price.

As a teacher, you could find and sell items in the evening, on the weekends, over holiday breaks, and in the summer. You get to make your own schedule, and it can be however many or few hours as you want.

Some items that you can resell include:

Vintage furniture

Collectibles, such as toys, coins, stamps, books, and more

Sporting equipment

Clothing

Electronics

I recommend signing up for a helpful webinar on this topic, How To Turn Your Passion For Visiting Thrift Stores, Yard Sales & Flea Markets Into A Profitable Reselling Business.

19. Bookkeep

Bookkeepers are people who keep track of all the money-related things for businesses. Bookkeepers do tasks like:

Tracking income

Organizing expenses

Making financial reports

This is typically a flexible job that you can do from home on your own time.

You can join the free workshop that focuses on finding virtual bookkeeping jobs and how to begin your own freelance bookkeeping business by signing up for free here.

Recommended reading: How To Find Online Bookkeeping Jobs

20. Sell Canva templates

Creating and selling Canva templates online allows you to work from home in your free time.

A Canva template is like a pre-designed layout that you can use for creating things like social media graphics, Pinterest pins, ebooks, or presentations. It is a helpful starting point if you’re not very skilled at designing from scratch. Business owners, marketing professionals, nonprofit organizations, educators, event planners, restaurants, and more buy templates all the time.

Canva templates come with blank spaces where buyers can add their own words or pictures, adjust colors and fonts, and more. They’re useful for people who want their graphics to look high quality without spending a lot of time in the process (or perhaps they don’t know how to do it so templates help them a lot!).

Making and selling Canva templates can be a great way to earn extra money as you only need to create them once, and then you can sell them as many times as you’d like.

Recommended reading: How I Make $2,000+ Monthly Selling Canva Templates

21. Rover (walk and watch pets)

Rover is a website that links pet owners with pet sitters and dog walkers. You can do this job on the weekends throughout the year, or simply only open up your schedule during the summer months. It is up to you.

Getting started is easy on Rover – you set up a profile that talks about your experience with pets and the services you can provide, like dog walking, pet sitting, and house sitting.

Then, you will receive requests from customers and talk about pricing. Rover takes care of processing payments, and you’ll receive payments directly into your account.

You can sign up for Rover here.

22. Care.com

Another platform for finding pet and house sitting side jobs is Care.com. Care.com is not limited to pet care and includes other caregiving services, such as childcare and senior care.

You can browse available jobs in your area and apply to those that match your skills and interests. Care.com also allows clients to contact you directly for your services after you’ve created a profile. Once a job is completed, you’ll receive payment through the site.

23. Be a virtual assistant

A virtual assistant provides administrative, technical, or creative support to clients from home.

Some of the tasks you might do as a virtual assistant include managing schedules, responding to emails, making travel arrangements, handling social media accounts, and even writing articles or creating presentations.

If you want to become a virtual assistant, I recommend taking the free workshop called 5 Steps To Become a Virtual Assistant.

Recommended reading: Best Ways To Find Virtual Assistant Jobs

24. Be a food photographer

Food photography can be a fun and creative way to earn extra income during your free time. Food photographers do just that – take pictures of food.

Whether you’re working directly for restaurants, magazines, or on a freelance basis, this job allows you to use your skills and interests to create beautiful images.

You can learn more at How To Become a Food Blog Photographer And Earn Over $50,000 Each Year.

25. House sit

As a teacher, you might be looking for ways to make some extra money during breaks or weekends. One option to consider is house sitting, and this is when you watch someone’s home (such as watering their plants and collecting mail) and sometimes take care of pets while their owners are away. People also hire house sitters so that their homes aren’t sitting empty because a visible presence can deter potential thefts.