Guaranteed Rate’s PowerVP mobile app aims to enhance loan originators’ ability to keep in constant contact with customers anywhere, at any given time — 24/7.

The PowerVP app will create new loans; invite customers to complete a digital mortgage; send a one-click conditional approval letter; lock in rates; obtain real-time pricing and run a credit report, the company said in a release.

“It’s now entirely possible for us to qualify buyers for their dream home by the time they leave the open house. Agents submitting an offer at 8:30pm? Our sales team can get the pre-approval out at 8:35, away from their desks, all within this robust tool that will help them hustle smarter for our partners and deliver contract winning speed to our amazing customers,” Guaranteed Rate’s president & CEO Victor Ciardelli, said in a prepared statement.

The Chicago, Illinois-headquartered lender has more than 850 branches across the country and is licensed in 50 states and Washington, D.C.

The lender originated $10.6 billion in the second quarter, up from the previous quarter’s $7 billion — totaling $17.6 billion in the first six months of 2023, according to data from Inside Mortgage Finance.

Production volume in the first half of this year was down about 47% from the same period in 2022. As of June 2023, Guaranteed Rate had a 2.5% market share, IMF data showed.

In a shrinking mortgage market, the lender had two layoffs in August that affected tech staff as well as non-tech workers including loan originators, former employees who were affected told HousingWire.

The company had 2,149 sponsored LOs as of Thursday, according to the National Multistate Licensing System (NMLS).

Recent products launched by Guaranteed Rate include a down payment assistance program in July. G-Rate will provide 2% of the required 3% minimum down payment for a conventional loan or up to $2,000 — whichever is lower.

The Fannie Mae Flex Modification Program (FMP) is a mortgage assistance solution designed to relieve borrowers facing financial hardship.

Are you looking to improve your mortgage management but don’t know where to start? Handling mortgage payments is challenging, especially if you’re facing economic difficulties and don’t know where or how to get financial assistance. The Fannie Mae and Freddie Mac Flex Modification Program may be the solution you’re looking for.

Learn what you need to know about the Flex Modification Program: how it works, who qualifies for it, and how you can apply. This comprehensive guide will help you understand the many benefits of FMP for a more stable financial future.

In This Piece:

What Is the Flex Modification Program?

The Fannie Mae Flex Modification program is a mortgage assistance solution designed to relieve borrowers facing financial hardship. This program offers a flexible framework for loans that helps eligible borrowers to modify their monthly mortgage payments and avoid foreclosure.

Modifying the loan terms can make mortgage payments more affordable and sustainable for struggling homeowners.

Get matched with a personal

loan that’s right for you today.

Learn

more

How Do Fannie Mae and Freddie Mac Work?

The mortgage market has a few essential entities, including the government-sponsored enterprises called Fannie Mae and Freddie Mac. Their approach allows lenders to free up funds to provide more mortgage loans to borrowers.

But how does it work? Fannie Mae and Freddie Mac helped make mortgages more accessible by buying them from lenders. This allows lenders to have more money available to provide new mortgages to borrowers or invest in other financial opportunities. For example, if a lender originates a mortgage, they can sell it to Fannie Mae or Freddie Mac, who then include it in their portfolio or package it into mortgage-backed securities.

How Flex Modification Works

The Flex Modification Program offers loan modifications to eligible borrowers experiencing financial hardship. Here’s a breakdown of how the program operates:

Eligibility Requirements:

You must have a mortgage loan owned or guaranteed by Fannie Mae or Freddie Mac.

The mortgage loan must be at least 60 days delinquent or at risk of imminent default.

You must demonstrate a hardship that affects your ability to make timely mortgage payments.

Modification Terms:

The program aims to reduce your monthly mortgage payment to 20% or more below your pre-modification.

The modification may involve adjusting the interest rate, extending the loan term, or forbearing a principal portion.

The goal is to make the mortgage payment more affordable while ensuring it’s sustainable for you.

Application Process:

Apply to the Flex Modification Program through a loan servicer.

The loan servicer will assess your eligibility and collect the necessary documentation.

Once approved, the loan servicer will work with you to finalize the modification terms.

Why Should You Consider the Flex Modification Program?

Before considering the Flex Modification Program, it’s essential to understand its potential pros and cons.

Pros:

Lower monthly payments: The program aims to reduce your mortgage payment to a more affordable level, making it easier to manage your finances on time.

Protection from foreclosure: By modifying your loan, the program can help you avoid the devastating consequences of foreclosure.

Improved financial stability: By participating in the Flex Modification Program, you can regain control of your financial situation. Providing you with a sense of stability and peace of mind, allowing you to focus on rebuilding your financial health.

Simplified application process: Applying for the program is relatively straightforward, and you can work directly with your loan servicer to navigate the process.

Potential principal reduction: The FMP may offer this, which means that a portion of the outstanding loan balance could be forgiven or deferred, reducing the overall amount owed. This can be particularly beneficial if you owe more on the mortgage than your current property value.

Preservation of homeownership: One of the primary goals of the FMP is to help borrowers preserve their homeownership. The program offers a viable alternative to foreclosure by providing a framework for loan modifications.

Cons:

Extended loan term: Modifying your loan may result in a more extended repayment period, meaning you’ll make mortgage payments for longer.

Impact on credit score: While participating in the program doesn’t directly affect your credit score, the delinquency prior to modification might be reported on your credit report.

Limited availability: The program is specifically for Fannie Mae or Freddie Mac borrowers with owned or guaranteed loans. You won’t qualify for this program if either entity doesn’t back your loan. However, other programs may exist. Contact your lender if you’re struggling to make your mortgage payments.

Remember, these pros and cons will vary based on your circumstances. It’s essential to consult with your loan servicer and thoroughly review the modification terms to understand the potential benefits you may receive from participating in the program.

Who Qualifies for the Flex Modification Program?

The Flex Modification Program is designed for borrowers struggling with mortgage payments due to financial hardship.

To qualify for the program, you must meet the following criteria:

Loan ownership: The mortgage loan must be owned or guaranteed by Fannie Mae or Freddie Mac.

Delinquency or imminent default: Borrowers must be at least 60 days delinquent on their mortgage payments or at risk of imminent default.

Demonstrated hardship: Borrowers need to demonstrate a hardship that affects their ability to make timely mortgage payments. Hardships may include job loss, income reduction, medical expenses, divorce, or other significant life events.

Additionally, you must comprehend what a “hardship” entails to be considered for a loan modification. Each situation is evaluated individually, but common examples of hardships include loss of income, disability, serious illness, divorce, or the death of a co-borrower.

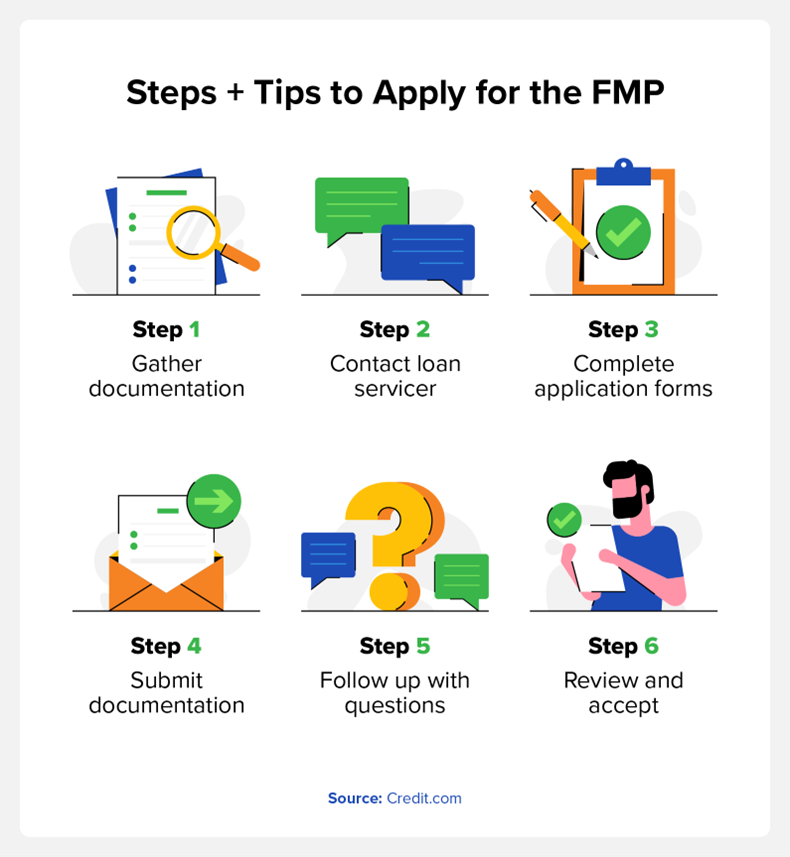

How to Apply for the FMP

If you believe you meet the eligibility requirements for the Flex Modification Program, you can follow these steps and tips to apply:

Gather documentation: Prepare the necessary documents, such as proof of income, bank statements, tax returns, and any other documentation required by your loan servicer.

Contact your loan servicer: Inform your loan servicer about your interest in the Flex Modification Program.

Complete application forms: Your loan servicer will provide the necessary forms and guidance to complete the application process.

Submit documentation: Submit all the required documentation and the completed application forms to your loan servicer.

Follow up and provide additional information: Be proactive in promptly following up with your loan servicer and providing any additional information they request.

Review and accept the modification terms: Once your loan servicer evaluates your application, they will provide you with the proposed modification terms. Review them carefully and, if acceptable, sign and return the necessary paperwork to proceed with the modification.

Remember, each loan servicer may have a specific application process, so it’s crucial to communicate directly with them to ensure you have all the necessary information and are following the correct steps. Having to redo the application process due to easily-avoided mistakes is the last thing you need.

Other Mortgage Payment Help Options

What if I don’t qualify? What can I do? Other mortgage payment assistance options are available if the FMP is not the right fit.

Fannie Mae and Freddie Mac offer additional programs catering to different circumstances. Some of these options include:

Home Affordable Modification Program (HAMP): This aims to help homebuyers struggling with financial hardship and mortgage payments.

Repayment plan: Allows you to catch up on missed mortgage payments by adding a portion of the past-due amount to your regular expenditures over an agreed-upon period.

Forbearance: Temporarily suspends or reduces your mortgage payments with this program. It can be for a specific period, providing short-term relief during financial difficulties, so you can reassess the situation.

But before you move forward with one of these, it’s essential to analyze your alternatives and consult with your loan servicer to determine the best course of action based on your specific circumstances.

FAQs

Let’s address some frequently asked questions about the Flex Modification Program:

Does the Flex Modification Program Affect Your Credit Score?

Participating in the Flex Modification Program doesn’t directly impact your credit score. However, the delinquency prior to modification might be reported on your credit report

What if Fannie Mae or Freddie Mac Doesn’t Own My Loan?

If your loan isn’t owned or guaranteed by Fannie Mae or Freddie Mac, you won’t be eligible for the Flex Modification Program. However, you should contact your loan servicer to inquire about other available mortgage assistance options or loan modification programs specific to your loan type.

How Long Does the Flex Modification Program Last?

The duration of the Flex Modification Program varies depending on the specific terms of the modification. Typically, the program aims to provide long-term mortgage relief by modifying the loan terms to make payments more affordable and sustainable for the borrower.

The revised terms may involve extending the loan term or adjusting the interest rate. It’s important to discuss the duration of the modification with your loan servicer, as it will depend on your circumstances and the terms agreed upon.

Can I Qualify for the Flex Modification Program if I’ve Previously Received a Loan Modification?

If you have previously received a loan modification, you may still be eligible for the Flex Modification Program. However, the specific requirements and eligibility criteria may change depending on your previous modification and the current guidelines set by Fannie Mae and Freddie Mac.

It’s crucial to communicate with your loan servicer and provide them with all the necessary information regarding your previous modification. They will assess your eligibility based on your unique circumstances and guide you through the application process.

Remember, these answers are general guidelines, and you must consult with your loan servicer to get accurate and personalized information based on your situation.

What Are the Next Steps?

The Fannie Mae Flex Modification Program provides borrowers with a potential lifeline during financial hardship. It aims to make mortgage payments more manageable and sustainable by offering loan modifications. If you’re facing challenges with your mortgage payments, exploring the Flex Modification Program and other mortgage payment help options can help you find the assistance you need.

To take control of your mortgage management and improve your financial well-being. Consult with your loan servicer for accurate and personalized information based on your situation, and research different mortgage rates to make informed financial decisions.

This article originally appeared on The Avocado Toast Budget.

This post is sponsored by Credit.com.

Here at the ATB, we are all about budgeting in a way that works for you and finding realistic ways to feel more confident with your money.

Now that 2020 is (finally) over, here are ways that you can start to take hold of your finances and build confidence with your money in 2021.

Write down your short, medium and long term financial goals

I’m a big believer that you don’t need to stress over how to maximize the value of every dollar you come across.

Much of personal finance is behavioral and relies on us finding value in how we navigate our money!

Because of this, I found it incredibly helpful to sit down and brainstorm short, medium and long-term financial goals to decide what I wanted my money to do for me.

Write down your short, medium and long term financial goals

Here’s how I break it up:

Short-term goals – less than two years

Medium-term goals – 2 – 10 years

Long-term goals – 10+ years

Feel free to dream big!

We want to make realistic and attainable goals, but we also want to allow ourselves to dream about what we really want our lives to look like, and how our money plays a role in that.

Get to know your credit score

Wanna know a secret? I avoided my credit score for the longest time.

Turns out, once I finally faced my credit score, I became more empowered to understand how my credit score affects my finances and what I could do to change it.

While free resources can give you a ballpark estimate of your credit score, that score isn’t very useful and certainly isn’t what creditors see!

Knowing your true score, and seeing your credit reports from all three major credit bureaus, gives you security and control over how to navigate your credit score going forward.

While it can be daunting, credit plays an important role in our lives from renting, to car insurance, to mortgages, to career opportunities and more.

That’s why it’s important that you stay informed of what your credit actually looks like that’s why I signed up for ExtraCredit’s free trial!

Set up automatic savings

Automating your savings is LIFE CHANGING.

Setting up automatic savings is often referred to as “paying yourself first” because you are prioritizing saving money for Future You.

There are tons of different savings goals that you can put this money toward, but the important part right now is to set up automatic savings so you can set it and forget it.

Trust me—you miss that money a lot less if you never see it in your account in the first place.

If you have automatic deposits at work, it’s super easy to add a savings account and have a certain % or dollar amount go into that account every month without it EVER hitting your checking.

In my opinion, this is the best way to go. Out of sight, out of mind.

You’re way less likely to touch this money, and you’ll be shocked at how much it grows over time!

If this isn’t an option for you, you’re not out of luck. You can set up automatic savings transfers into your savings account from your checking account through your bank.

Find a budget that works for you

Here at the ATB, we are all about budgeting in a way that makes sense for you and your life.

Budgeting doesn’t have to be stressful and restrictive. It should actually be freeing and allow you to feel more confident and in control of your money!

There’s no one right way to budget, and there are TONS of different types of budgets depending on your income and financial goals.

Personally, I use a zero-based budget which allows me to track and decide where every single dollar I have is going.

If you have big savings goals, low income or high debt, I definitely recommend checking out a zero-based budget.

Learn how to increase your credit score

Your credit score has a bigger impact on your life than just determining your eligibility for loans.

Credit can impact your ability to rent, job opportunities, car insurance rates and more.

Once you know what your credit score is, it’s important to understand what makes up your credit score, and what steps you can take to increase it.

There are five factors that influence your credit score:

Payment History

Amounts Owed

Length of Credit History

New Credit

Credit Mix

Payment History makes up 35% of your credit score, so it is the most important factor.

ExtraCredit gives you the ability to report rent and utility payments, adding new tradelines to your credit profile. Adding payment history to your credit file.

And if you need help working to repair your credit, you can also use the Restore It feature to get an exclusive discount from a leading credit repair company. Remember: your best credit score is an accurate one.

Understanding how to increase your credit can take a lot of stress out of your finances and help you feel more in control of your credit future.

Make a debt payoff plan

I paid off $20k in CC debt in less than a year, and in order to do that, I needed a concrete plan of how I was going to tackle my debt.

Prior to that point, I had just been throwing a little bit here and there, hoping that my balance would eventually decrease.

Shockingly, that never happened.

Once I decided to use the debt avalanche to tackle my credit card debt, I was able to calculate how much extra money I could throw at my debt every month in order to make progress toward my debt free goal.

With this method, I paid the minimum payments on all of my debt except for the one with the highest interest.

With the highest interest debt, I put any extra money I had toward paying that down.

This gave my money more of a purpose than just throwing extra money here and there at my different debts.

It was also reassuring and motivating to see the loan amount decrease drastically as I threw the extra money I had towards it.