Nestled in the heart of Utah Valley, Provo has increasingly been a topic of discussion for those looking to relocate.

Known for its close proximity to natural wonders like Provo Canyon and Utah Lake, it’s a location that offers both city life and natural retreat. However, with such growing attention, the question arises: Is Provo, Utah, a good place to live?

Geographic overview

Provo, located in Utah County, sits about 45 miles south of Salt Lake City. As part of the larger Provo-Orem metro area, it’s surrounded by breathtaking views, notably the majestic Wasatch Front mountains. The city enjoys a beautiful position by the Provo River, leading many to the popular Provo River Parkway Trail for outdoor activities.

Educational excellence: BYU and beyond

Central to Provo’s identity is Brigham Young University (BYU). As one of the top institutions in the country, BYU has significantly influenced Provo’s status as a college town. The presence of BYU means Provo is bursting with educational opportunities, from lectures at the BYU Museum and Bean Life Science Museum to events at the BYU campus itself.

Quality of life in Provo

Economic, cultural and safety factors drive movers to Provo in droves.

Economic stability

Provo’s unemployment rate is below the national average. The presence of institutions like BYU and the Provo City Center Temple ensures steady employment in the education and service sectors. Additionally, with a tech boom happening in the broader Salt Lake Valley, many are finding new job opportunities within a commutable distance from Provo.

Cultural richness

Provo is home to a rich blend of cultures. While there is a significant presence of members of The Church of Jesus Christ of Latter-day Saints, Provo is diverse in thought and lifestyle. The city houses several art galleries, theaters, and the iconic Provo City Center Temple, a testament to its rich history and cultural significance.

Safety

One of the notable features of living in Provo is its low crime rates. Both violent crimes and property crimes are below the national average, making Provo a safe environment for young families and college students alike.

Cost of living: breaking down the numbers

Is Provo Utah expensive to live in? Compared to other cities along the Wasatch Front, Provo’s cost of living is slightly below average. However, with the city’s growth, housing costs have been on the rise.

Housing market insights

The median home price in Provo has seen an upward trend over the past few years, though it remains competitive compared to Salt Lake City. Average rent for apartments is also reasonable, particularly given the high student population from BYU and Provo College. However, the demand for affordable homes has been steadily increasing.

Everyday expenses

When comparing Provo’s cost for groceries, transportation, and healthcare to the national average, residents find it reasonable and often below average. However, as with any city, certain luxuries or non-essentials can drive up living costs.

The heart of Provo: its people

With a population density of around 2,500 people per square mile, Provo is lively without feeling overcrowded. The median age skews younger, thanks in part to the influx of college students. Provo residents are generally known for their hospitality, community spirit and active lifestyles, taking advantage of nearby attractions like Provo Beach and Rock Canyon.

Before you pack: Moving to Provo insights

What do I need to know before moving to Provo Utah? Here are some considerations:

Outdoor Activities: With Provo River, Provo Canyon, and myriad trails, there’s always something to do outdoors. Whether you’re into hiking, fishing, or just picnicking, Provo has you covered.

Community Feel: Provo, often dubbed “Happy Valley”, has a tight-knit community. Neighbors often become lifelong friends, and community events are frequent.

Religious Considerations: As mentioned, Provo has a substantial Mormon population. While this brings a unique cultural flavor, it’s essential to be respectful and understanding of religious practices and holidays.

Public Transportation: The bus system in Provo is reliable, but having a car might be convenient for broader exploration and commuting.

Final verdict

Living in Provo offers a harmonious blend of city life and nature, academia and culture, community and individuality. With its reasonable cost of living, low crime rates and opportunities for both personal and professional growth, Provo stands out as one of the best cities in North Central Utah. Whether you’re a student at Brigham Young University, a young family looking to settle or anyone in between, Provo provides a backdrop for memories, experiences and growth.

In the balance of life’s considerations, the essence of Provo UT seems to be this: it’s more than just a city — it’s a community, an experience, and, for many, it’s home.

So, to the question, “Is Provo Utah a good place to live?” the answer resounds as a confident “Yes!” Search our Provo apartments for rent.

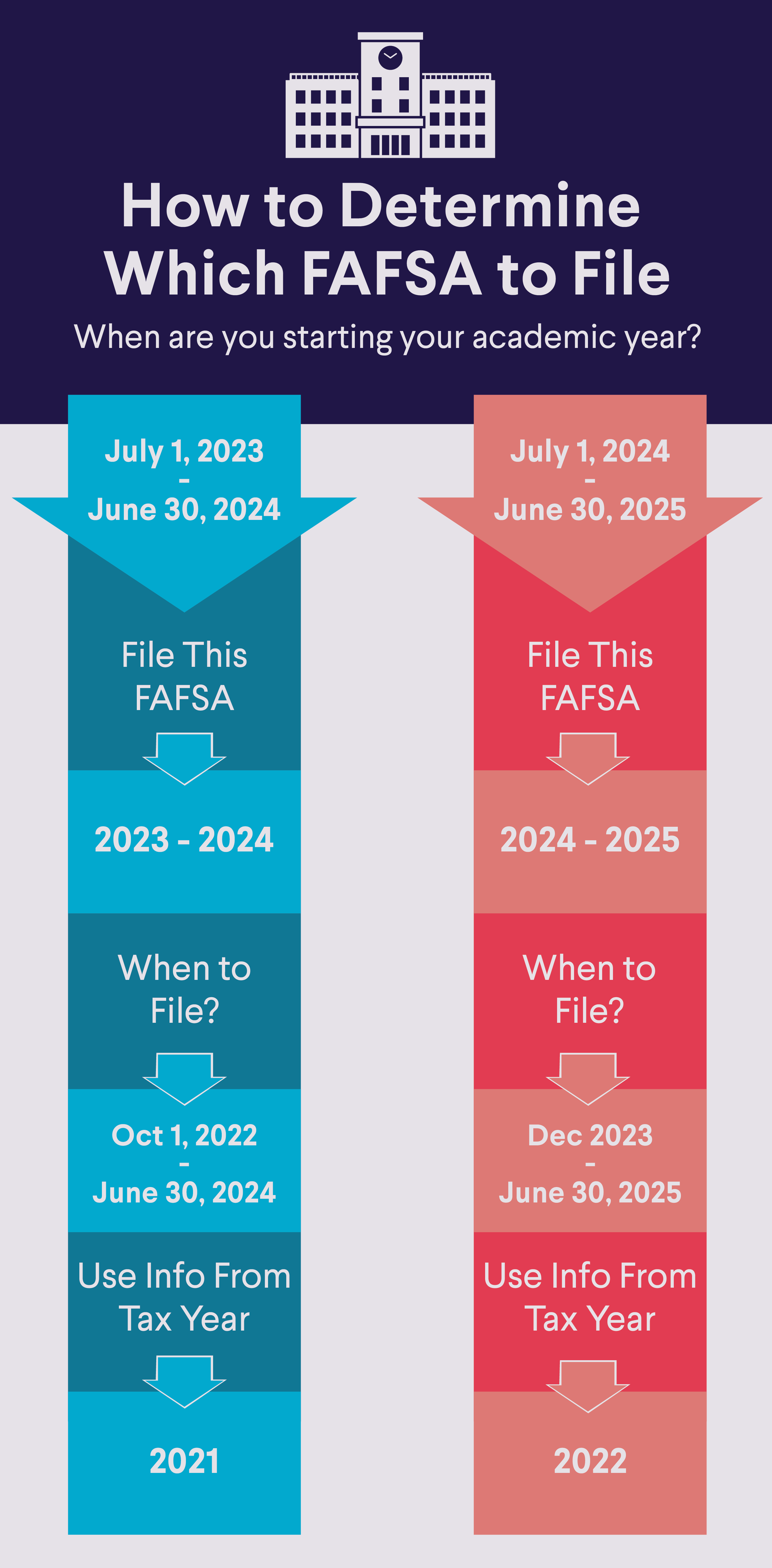

Editor’s Note: Due to major changes coming to the FAFSA, the form for the 2024-2025 academic year is delayed until December 2023. This article reflects the most recent information, but final details will not be available until the new FAFSA form is released.

The Free Application for Federal Student Aid, or FAFSA®, is a form students can fill out each school year to apply for college grants, work-study programs, federal student loans, and certain state-based aid.

By not filling out the form, or missing the FAFSA deadline, students may not receive financial aid that could help them pay for college. Indeed, the graduating class of 2022 left roughly $3.6 billion in need-based federal Pell Grants on the table by not completing the FAFSA, according to a new report by the National College Attainment Network (NCAN).

Typically, the FAFSA becomes available on October 1 for the following academic year. The 2024-2025 academic year, however, is an exception. Due to upcoming changes to the FAFSA (and some adjustments to how student aid will be calculated), the form will be available in December 2023.

It’s helpful to fill out your FAFSA as early as possible and not miss the important application deadlines, as there is a limited amount of aid available.

Read on for key federal, state, and institutional FAFSA deadlines to know.

What Is the FAFSA?

The FAFSA is the online form that you must fill out to apply for financial aid from the federal government, state governments, and most colleges and universities. The form requires students and their parents to submit information about household income and assets. That information is used to calculate financial need and determine how much aid will be made available.

If you are a dependent student, you will need to submit your parents’, as well as you own, financial information. If you are considered independent, you are not required to submit your parents’ financial information.

If you are already in school, remember that the FAFSA must be filled out every year, since income and tax information might have changed.

Federal financial aid includes student loans, grants, scholarships, and work-study jobs. In general, the eligibility requirements for federal aid state that for most programs, students:

• Must demonstrate financial need (though there is some non-need based aid, such as unsubsidized student loans) and,

• Must be a U.S. citizen or an eligible noncitizen, and

• Be enrolled in an qualifying degree or certificate program at their college or career school

For further details, take a look at the basic eligibility requirements on the Student Aid website. 💡 Quick Tip: You can fund your education with a low-rate, no-fee private student loan that covers all school-certified costs.

FAFSA Open Date and Deadline

File Your FAFSA for Next Year Close to December

Generally, it makes sense to submit the FAFSA promptly after the October 1st application release — or, in the case of the 2024-25 FAFSA, December 2023. Some aid is awarded on a first-come, first-served basis, so submitting it early could help improve your chances of receiving financial help for college.

File Your FAFSA for Last Year by June 30

You must file the FAFSA no later than June 30th for the school year you are requesting aid for. So, for the academic year 2023-24, you must file by June 30th, 2024, at the very latest, and for the academic year 2024-25, the final federal deadline is June 30th, 2025.

This FAFSA deadline comes after you’ve already attended and, likely, paid for school. You generally don’t want to wait this long. However, if you do, you can often receive grants and loans retroactively to cover what you’ve already paid for the spring and fall semester. Or, in some cases, you may be able to apply the funds to pay for 2023 summer courses.

State and institutional FAFSA deadlines

When the FAFSA is due is also dependent on where you want to go to college. Individual states and colleges have different deadlines — which may be much earlier than the federal deadline — for awarding financial aid to students. Here’s a look at two other key FAFSA deadlines to know.

Institutional FAFSA Deadlines

While students have until the end of the school year to file the FAFSA, individual schools may have earlier deadlines. These priority deadlines mean you need to get your FAFSA application in by the school’s date to be considered for the college’s own institutional aid. So if you are applying to several colleges, you may want to check each school’s FAFSA deadline and complete the FAFSA by the earliest one.

While filling out your FAFSA, you can include every school you’re considering, even if you haven’t been accepted to college yet.

State FAFSA Deadlines

States often have their own FAFSA deadlines. You can get information about state deadlines at Studentaid.gov. Some states have strict cutoffs, while others are just best-practice suggestions — so you’ll want to check carefully. States may have limited funds to offer as well.

Federal FAFSA Deadline

Typically, the FAFSA becomes available on October 1, almost a full year in advance of the year that aid is awarded. For the 2024-25 academic year, the FAFSA will open a few months later than usual — some time in December 2023. However, the federal government gives you until June 30th of the year you are attending school to apply for aid.

It’s generally recommended that students fill out the FAFSA as soon as possible after it’s released for the next school year’s aid to avoid missing out on available funds. Plus, there are often earlier school and state deadlines you’ll need to meet.

Recommended: FAFSA Delay: 5 Steps to Help Ensure Your State and College Aid Aren’t Affected

Taking the Next Steps After Submitting the FAFSA

So what happens after you hit “submit” on your FAFSA? Here’s a look at next steps:

• Wait for your Student Aid Report (SAR). If you submitted your FAFSA online, the U.S. Department of Education will process it within three to five days. If you submit a paper form, it will take seven to 10 days to process. The SAR summarizes the information you provided on your FAFSA form. You can find your SAR by logging in to fafsa.gov using your FSA ID and selecting the “View SAR” option on the My FAFSA page

• Review your SAR. Check to make sure all of the information is complete and accurate. If you see any missing or inaccurate information, you’ll want to complete or correct your FAFSA form as soon as possible. The SAR will give you some basic information about your eligibility for federal student aid. However, the school(s) you listed on the FAFSA form will use your information to determine your actual eligibility for federal — and possibly non-federal — financial aid.

• Wait for acceptance. Most college decisions come out in the spring, often March or early April. If you applied to a college early action or early decision, you can expect an earlier decision notification, often around December. Typically, you will receive a financial aid award letter along with your acceptance notification. This letter contains important information about the cost of attendance and your financial aid options.

Understanding Your Financial Aid Award

Receiving financial aid can be a great relief when it comes to paying for higher education. Your financial aid award letter will include the annual total cost of attendance and a list of financial aid options. Your financial aid package may be a mix of gift aid (which doesn’t have to be repaid), loans (which you have to repay with interest), and federal work-study (which helps students get part-time jobs to earn money for college).

If, after accounting for gift aid and work-study, you still need money to pay for school, federal student loans might be your next consideration. As an undergraduate student, you may have the following loan options:

• Direct Subsidized Loans Students with financial need can qualify for subsidized loans. With this type of federal loan, the government covers the interest that accrues while you’re in school, for six months after you graduate, and during periods of deferment.

• Direct Unsubsidized Loans Undergraduates can take out direct unsubsidized loans regardless of financial need. With these loans, you’re responsible for all interest that accrues when you are in school, after you graduate, and during periods of deferment.

• Parent PLUS Loans These loans allow parents of undergraduate students to borrow up to the total cost of attendance, minus any financial aid received. They carry higher interest rates and higher loan origination fees than Direct Subsidized and Unsubsidized Loans.

If financial aid, including federal loans, isn’t enough to cover school costs, students can also apply for private student loans, which are available through banks, credit unions, and online lenders.

Private loan limits vary by lender, but students can often get up to the total cost of attendance, which gives you more borrowing power than you have with the federal government. Each lender sets its own interest rate and you can often choose to go with a fixed or variable rate. Unlike federal loans, qualification is not need-based. However, you will need to undergo a credit check and students often need a cosigner.

Keep in mind that private loans may not offer the borrower protections — like income-based repayment plans and deferment or forbearance — that come with federal student loans. 💡 Quick Tip: Parents and sponsors with strong credit and income may find much lower rates on no-fee private parent student loans than federal parent PLUS loans. Federal PLUS loans also come with an origination fee.

The Takeaway

Completing the FAFSA application allows you to apply for federal aid (including scholarships, grants, work-study, and federal student loans). The FAFSA form is generally released on October 1st of the year before the award year and closes on July 30th of the school year you are applying for.

The 2024–25 FAFSA will be delayed until December 2023 due to changes the U.S. Department of Education is implementing to make the application more streamlined for students and families. That application will close on June 30, 2025. However, individual colleges and states have their own deadlines which are typically earlier than the federal FAFSA deadline.

If you’ve exhausted all federal student aid options, no-fee private student loans from SoFi can help you pay for school. The online application process is easy, and you can see rates and terms in just minutes. Repayment plans are flexible, so you can find an option that works for your financial plan and budget.

Cover up to 100% of school-certified costs including tuition, books, supplies, room and board, and transportation with a private student loan from SoFi.

SoFi Loan Products SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

SoFi Private Student Loans Please borrow responsibly. SoFi Private Student Loans are not a substitute for federal loans, grants, and work-study programs. You should exhaust all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

SoFi Private Student Loans are subject to program terms and restrictions, and applicants must meet SoFi’s eligibility and underwriting requirements. See SoFi.com/eligibility-criteria for more information. To view payment examples, click here. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

External Websites: The information and analysis provided through hyperlinks to third-party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Christmas is right around the corner, which means it’s time to decorate. Everyone has plans to create a magical, winter wonderland in their apartment, but there’s one vital thing yet to figure out — do you get a real Christmas tree or an artificial Christmas tree?

Both have their pros and cons, so how do you pick? Well, you better not pout and you better not cry because we’re telling you what you need to know.

A brief history of Christmas trees

Germany is credited with the first use of the Christmas tree starting in the 16th century, and German settlers in Pennsylvania made Christmas trees popular in America in the 19th century.

Ever since then, picking out and decorating a tree has become synonymous with the Christmas season.

Things to consider with artificial Christmas trees

Artificial Christmas trees have been around since the 19th century. Considering they started off as dyed goose feathers, it’s safe to say they’ve come a long way. You no longer have to pluck the goose to decorate your apartment.

Today, you can get a really nice looking tree from a local craft or big box store for a reasonable price. The cost of fake trees can be anywhere from $30 into the thousands depending on what you’re looking for. As you’re making your decision, here are a few reasons to consider a fake Christmas tree this year:

1. Variety of styles and options

There are a lot of different types and styles of trees to choose from. From the traditional-looking green pine tree to sparkling silver to trees dusted with fake snow, you can pretty much buy any type of pine you want for the holidays.

2. Ease of use

One of the benefits of choosing a fake tree as an apartment dweller is how easy it is to set up. Most fake Christmas trees come in a box, so it’s much easier to get it into the apartment, especially if you live in a building with a small elevator.

A great deal of fake Christmas trees come pre-decorated with lights attached. That alone saves you a lot of time and energy. They’re easy to maintain as you don’t have to water them and you also avoid needles constantly falling and cluttering up your space. It’s also not as much of a fire hazard as a real tree because there are no dead pine needles that could spark.

3. Reusability

Unlike a real Christmas tree that has a short life span, fake Christmas trees are a one-time purchase that can last you for years to come. You’ll never have to purchase a tree again and can use the same, beautiful tree year-over-year.

When you’re done with Christmas and it’s time to put away the decorations, all you have to do is break down the tree and stuff it back in the closet it came from.

4. Lack of pine smell

While fake Christmas trees have a lot of perks, there is a con. With a fake tree, you’ll miss out on the fresh pine smell that’s linked to Christmas. Of course, there are candles and other substitutes to fix this problem, such as Thymes Frasier’s dispensers, but at the end of the day, nothing is as good as the authentic smell. But, if you have allergies, a fake tree is a great solution.

Things to consider with real Christmas trees

Christmas tree shopping is one of the many joys of the Christmas season. The thrill of picking out which tree shall be yours is exciting and can be a great family tradition. There’s nothing like walking the rows, debating between the small, Charlie Brown-looking tree or choosing the largest tree in the lot. But there are some other things to consider, too.

1. Choose a unique tree each year

The experience of picking out a fresh tree each year is unforgettable. You can find great trees in your local forest and chop them down yourself. Or, if sawing at a stump for hours in the cold isn’t your thing, then you can go Christmas tree shopping at a local lot. Either way, you’ll be sure to get a tree that is special and doesn’t look like everyone else’s.

2. Fresh pine tree smell

With a fake tree, you won’t have the crisp pine tree smell. But, with a real tree, your apartment will smell like fresh pine the moment you bring the tree home. No diffuser or candle can quite replicate that balsam fir smell.

3. Size and upkeep

There’s the joy of decorating your tree and deciding which ornaments go where. But, you can safely decorate both fake and real trees, and a downside to having a real Christmas tree in an apartment is the sheer size.

It can be a pain to lug a massive pine up to your apartment and then take it back down only a couple weeks later. There’s also the matter of having to care for the tree, making sure it gets enough water on a regular basis. When you’re deciding between a real and fake Christmas tree, make sure you consider the upkeep involved with a real tree.

Your final decision

There are many pros and cons to real Christmas trees vs. artificial Christmas trees. At the end of the day, it’s really up to you and what’s best for your apartment.

Do you want the authentic feel of a real Christmas tree or do you want the ease of an artificial tree? Either one is a great option and will make your apartment feel like a Christmas wonderland.

Ashley Singleton is a writer who loves following and writing about current lifestyle, DIY and home improvement trends. You can read some of her other work on the Lady Spike Media website. In her spare time, she performs stand-up comedy in Los Angeles.

Many people love showing their holiday spirit with Christmas lights, whether just a strand of twinkle lights around a window or going all-out like the Griswolds.

While these lights are festive, it’s worth noting that they aren’t free. In fact, the cost of running holiday lights rose 13% last year, costing the average household $15.48 vs. $13.41 the prior year.

In this economy, every dollar can count, so if you want to learn how much it costs to run Christmas lights for a month and how to reduce that expense, read on.

Here, you’ll learn more about:

• How much do Christmas lights cost to run?

• How much does it cost to run Christmas lights for a month?

• How can you save money on your holiday light electric bill?

Factors Affecting the Cost of Running Christmas Lights

Running Christmas lights uses energy, which can translate to higher utility bills. How much of an increase you see in your electric bill can depend on a number of factors, including:

• How many strands of lights you use

• The type of bulbs used in each strand

• The number of hours you run your lights each day

• How many days you run Christmas lights for

• Where you live and what you pay per kilowatt hour for electricity.

All of these things can influence how large your Christmas lights electric bill turns out be once January rolls around. Understanding what you could wind up paying can help if affordably celebrating the holidays is your goal.

Keep in mind that other costs can drive up electric bills during the holidays, apart from Christmas lights. If you’re using the oven more often to prepare holiday meals, for example, that can result in a higher electric bill. You may also see a bigger bill if colder weather means the heat is kicking on more often or your kids are home all day using electronics more while school is out. Lowering your energy bill may require a multifaceted approach.

How Much Electricity Do Christmas Lights Use?

The amount of energy used by Christmas lights can depend on the type of bulb and the number of bulbs per strand. The most popular options for Christmas lights include incandescent mini lights, mini LED lights, and ceramic C7 lights.

So which type of bulb uses the most energy?

The simplest answer is to look at the wattage of Christmas lights, based on bulb size and number of bulbs per strand. For example:

• With C7 lights, for instance, you’re typically getting 25 lights per strand.

• With mini LED lights, you’ll normally have 50 bulbs for a 14-foot strand and 100 bulbs per 32-foot strand.

• With mini icicle lights, you often have 300 bulbs for a 26-foot strand.

Here’s how the average wattage for each one compares, though note that incandescent bulbs stopped being manufactured and sold in August 2023 (some people may still own and use strands of these, however):

• C7 lights: 5 watts

• C9 incandescent lights (2-¼” long): 7 watts

• Mini incandescent lights: 0.4 watts

• Mini LED lights: 0.07 watts

Between those three options, mini LED lights draw the least amount of energy per strand while C7 lights draw the most.

LEDs possibly lowering energy costs by up to 90% vs. the other options. Switching to LEDs could be a way to save money daily during the holidays.

Also note that you’d need four strands of C7 lights to equal the same number of bulbs in just one strand of incandescent or LED mini lights. This is important to understand because it can affect the number of kilowatt hours used and your overall energy costs.

Recommended: 23 Tips on Saving Money Daily

Cost of Running Christmas Lights

So how much do Christmas lights cost to run for a month? Or longer? Calculating your estimated cost of running Christmas lights matters when trying to lower your electric bill during the winter months. Again, what you’ll pay can depend on a variety of factors, including where you live and how much electricity costs.

The average household pays $0.17 cents per kilowatt hour for electricity, according to the U.S. Department of Energy, but prices may be significantly higher or lower in different parts of the country due to cost of living differences.

If you live in Connecticut, for example, you might pay an average of $0.21 cents per kilowatt hour. People living in Florida, however, might pay an average of $0.11 cents per kilowatt hour. Residents of Hawaii typically pay the most, currently spending $0.32 cents per kilowatt hour.

Here’s how to figure out how much you’ll pay for Christmas lighting:

• Multiply the wattage of the lights by the hours per day the lights will be on, then divide by 1,000 to find kilowatt hours per day

• Multiply kilowatt hours per day by your cost of electric usage to get the cost per day

• Multiply the cost per day by the number of days your lights will be on

Calculating the Cost of Christmas Lights

Now, for how much does it cost to run Christmas lights? Here’s a look at what it would cost to run C7 lights, C9, and mini incandescent lights, and mini LED lights for six hours a day for 30 days, using a price of $0.14 cents per kilowatt hour. Here’s what you’d pay for each one:

Bulb Type

Hourly Cost

Daily Cost

Monthly Cost

C7 (25 bulbs, 5 watts per bulb)

$0.0175

$0.105

$3.15

C9 (25 bulbs, 7 watts per bulb)

$0.025

$0.15

$4.50

Incandescent Mini Lights (100 bulbs, 0.45 watts per bulb)

$0.0063

$0.0378

$1.13

Mini LED Lights (100 bulbs, 0.07 watts per bulb)

$0.0042

$0.0252

$0.76

Keep in mind that these costs are for just one strand of lights, as noted. If you string together several strands on your tree, frame your windows with lights, and then drape your shrubs or street-facing windows outdoors with more, your costs will of course go up.

Also, in terms of what the average person spends on Christmas lights, it can vary by a state’s cost of living, as well as by what kind of bulbs are used. Louisiana residents who run LED lights, for example, would likely spend the least, since they are paying just over nine cents per kilowatt hour (currently the lowest rate in the US) and they would be using energy-saving bulbs. Meanwhile, Hawaiians who opt for incandescent bulbs would probably spend the most, since their bulbs use a considerable amount of power and they currently pay the highest national rate for energy of almost 33 cents per kilowatt hour.

💡 Quick Tip: Most savings accounts only earn a fraction of a percentage in interest. Not at SoFi. Our high-yield savings account can help you make meaningful progress towards your financial goals.

Tips to Save on Your Christmas Lighting Bill

If you’re looking for ways to lower your energy bill when you start plugging in your holiday lights, follow this advice.

Embracing Energy-Efficient LEDs

As mentioned, the wattage of Christmas lights plays an important part in determining how much you pay for electric bills over the holidays. Between C7 lights, incandescent lights and LED lights, LED lights are highly energy-efficient. According to the Department of Energy, residential LEDs that are ENERGY STAR rated use up to 75% less energy and last 25 times longer than incandescent lights.

People who use LED Christmas lights tend to pay far less than those using incandescent bulbs or C7 lights. So it follows that an easy way to save money on your electric bill and reduce energy usage would be to use mini LED lights as often as possible. Aside from that, LED bulbs emit less light and are less likely to overload sockets, making them a potentially safer option for Christmas lighting compared to other types of bulbs.

So if you still have some incandescent bulbs in your box of Christmas decorations, you may want to think about swapping them out for LEDs. (You won’t find incandescents made or sold in the US anymore either.)

Benefits of Solar-Powered Outdoor Lights

You might consider using solar-powered outdoor lights on your house over the holidays. These strands depend upon energy collected by small panels that gather and hold energy from the sun during the day.

These strands don’t plug in and draw no electrical power. So they can be especially easy and economical to use over the holidays.

Battery-Operated Lights for Smaller Displays

If you like to create smaller displays, you might consider battery-powered strands of lights. There is a wide range of how long these lights will stay illuminated, but this can be a good unplugged option to try for small-scale displays. While you do have to pay for the batteries, it can be cheaper than plugging in lights for weeks on end.

Recommended: 18 Common Misconceptions About Money

The Takeaway

A higher-than-usual electric bill can put a damper on your holiday celebrations. Estimating your potential costs beforehand can help you manage utility expenses. And you can decide whether it’s worth it to invest a little money in upgrading your current Christmas lights to energy-efficient options.

Having the right banking partner, such as one with budgeting tools, can also help make tackling high utility bills after the holidays easier.

Interested in opening an online bank account? When you sign up for a SoFi Checking and Savings account with direct deposit, you’ll get a competitive annual percentage yield (APY), pay zero account fees, and enjoy an array of rewards, such as access to the Allpoint Network of 55,000+ fee-free ATMs globally. Qualifying accounts can even access their paycheck up to two days early.

Better banking is here with up to 4.50% APY on SoFi Checking and Savings.

FAQ

Do LED Christmas lights use a lot of electricity?

Compared to C7 lights or incandescent mini lights, LED Christmas lights use the least amount of energy. Specifically, they can use up to 90% less energy while lasting longer. LED Christmas lights also emit less heat and can be easier to install than other types of holiday lighting.

Do Christmas lights raise your light bill?

Holiday lights can raise your electric bill during the winter months. How much it costs to run Christmas lights can depend on several things, including the type of bulbs used, how many light strands you’re running, how long you turn the lights on for, and the average cost of energy per kilowatt hour in your area. Using timers and switching to energy-efficient bulbs can be helpful for reducing your Christmas lights electric bill.

Do Christmas trees use a lot of electricity?

Christmas trees can use a lot of electricity, depending on the type of lights you use, the number of strands on the tree, and how long you leave your tree plugged in each day. Using mini LED lights can reduce electric costs for Christmas tree lighting, while using C7 bulbs to light your tree could result in a higher energy bill.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with direct deposit activity can earn 4.50% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Direct Deposit means a deposit to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Direct Deposit”) via the Automated Clearing House (“ACH”) Network during a 30-day Evaluation Period (as defined below). Deposits that are not from an employer or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, do not constitute Direct Deposit activity. There is no minimum Direct Deposit amount required to qualify for the stated interest rate.

SoFi members with Qualifying Deposits can earn 4.50% APY on savings balances (including Vaults) and 0.50% APY on checking balances. Qualifying Deposits means one or more deposits that, in the aggregate, are equal to or greater than $5,000 to an account holder’s SoFi Checking and Savings account (“Qualifying Deposits”) during a 30-day Evaluation Period (as defined below). Qualifying Deposits only include those deposits from the following eligible sources: (i) ACH transfers, (ii) inbound wire transfers, (iii) peer-to-peer transfers (i.e., external transfers from PayPal, Venmo, etc. and internal peer-to-peer transfers from a SoFi account belonging to another account holder), (iv) check deposits, (v) instant funding to your SoFi Bank Debit Card, (vi) push payments to your SoFi Bank Debit Card, and (vii) cash deposits. Qualifying Deposits do not include: (i) transfers between an account holder’s Checking account, Savings account, and/or Vaults; (ii) interest payments; (iii) bonuses issued by SoFi Bank or its affiliates; or (iv) credits, reversals, and refunds from SoFi Bank, N.A. (“SoFi Bank”) or from a merchant.

SoFi Bank shall, in its sole discretion, assess each account holder’s Direct Deposit activity and Qualifying Deposits throughout each 30-Day Evaluation Period to determine the applicability of rates and may request additional documentation for verification of eligibility. The 30-Day Evaluation Period refers to the “Start Date” and “End Date” set forth on the APY Details page of your account, which comprises a period of 30 calendar days (the “30-Day Evaluation Period”). You can access the APY Details page at any time by logging into your SoFi account on the SoFi mobile app or SoFi website and selecting either (i) Banking > Savings > Current APY or (ii) Banking > Checking > Current APY. Upon receiving a Direct Deposit or $5,000 in Qualifying Deposits to your account, you will begin earning 4.50% APY on savings balances (including Vaults) and 0.50% on checking balances on or before the following calendar day. You will continue to earn these APYs for (i) the remainder of the current 30-Day Evaluation Period and through the end of the subsequent 30-Day Evaluation Period and (ii) any following 30-day Evaluation Periods during which SoFi Bank determines you to have Direct Deposit activity or $5,000 in Qualifying Deposits without interruption.

SoFi Bank reserves the right to grant a grace period to account holders following a change in Direct Deposit activity or Qualifying Deposits activity before adjusting rates. If SoFi Bank grants you a grace period, the dates for such grace period will be reflected on the APY Details page of your account. If SoFi Bank determines that you did not have Direct Deposit activity or $5,000 in Qualifying Deposits during the current 30-day Evaluation Period and, if applicable, the grace period, then you will begin earning the rates earned by account holders without either Direct Deposit or Qualifying Deposits until you have Direct Deposit activity or $5,000 in Qualifying Deposits in a subsequent 30-Day Evaluation Period. For the avoidance of doubt, an account holder with both Direct Deposit activity and Qualifying Deposits will earn the rates earned by account holders with Direct Deposit.

Members without either Direct Deposit activity or Qualifying Deposits, as determined by SoFi Bank, during a 30-Day Evaluation Period and, if applicable, the grace period, will earn 1.20% APY on savings balances (including Vaults) and 0.50% APY on checking balances.

Interest rates are variable and subject to change at any time. These rates are current as of 8/9/2023. There is no minimum balance requirement. Additional information can be found at http://www.sofi.com/legal/banking-rate-sheet..

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Nestled in Hidalgo County, the small city of Alamo, Texas, often emerges as a discussion point among people on a quest for a serene yet promising locale to call home.

The quaint charm often associated with smaller cities can sometimes transcend beyond the picturesque to also offer a quality of life that rivals, or in some instances, surpasses the bustling allure of much larger cities.

This comprehensive assessment dives into the various factors that encapsulate living in Alamo, Texas, with a thorough examination of its cost of living, demographics, amenities and proximity to other significant Texan hubs, ultimately aiming to answer the burning question: “Is Alamo, Texas, a good place to live?”

Demographics and community

The community within Alamo, TX is a reflection of the broader Rio Grande Valley’s demographic composition. With a population that hovers around the 19,000 mark, the town hosts a predominantly Hispanic populace. This cultural backdrop lends Alamo a unique blend of Texan and Mexican traditions, which not only enriches the social fabric but also manifests in the culinary, cultural and artistic offerings of this small city.

Economy and employment

A scrutiny of Alamo’s economic landscape reveals an unemployment rate slightly above the national average. However, this metric has been on a downward trajectory, thanks to burgeoning local businesses and the spillover of economic activities from neighboring cities. The median income in Alamo resonates with the laidback and modest lifestyle it champions.

Cost of living

One of the enticing facets of living in Alamo, Texas, is undoubtedly its cost of living. Statistically, Alamo’s cost of living indices fall below the national average, making it an affordable place especially when pitted against other cities in Texas.

The low cost of living can be largely attributed to the affordable housing market in the city, with the median home value significantly less than the state and national averages. Alamo’s cost of housing and overall living expenses are arguably its biggest selling point to prospective residents on a budget.

Housing market

In Alamo, the median home value stands as a testament to its affordability. Housing here is not only accessible but offers a variety of choices for different income levels. Whether you are looking to rent or buy, the market in Alamo is conducive for families, retirees and even single individuals. The median home value is appreciably lower compared to other cities, making homeownership a feasible dream for many.

Education

Education is a pivotal concern for families contemplating a move to Alamo, TX. The city hosts several public and private schools, delivering a standard of education that aligns with the state’s benchmarks. The proximity to universities and colleges in nearby cities also broadens the educational horizon for residents.

Healthcare and services

Quality healthcare services are within reach, with a number of healthcare facilities located in and around Alamo. The nearby city of McAllen, for instance, has a wider array of medical facilities, ensuring residents have access to specialized medical care whenever necessary.

Proximity to major cities

Nestled strategically in the Rio Grande Valley, Alamo’s location is within a convenient distance from major cities like McAllen and Edinburg. This proximity not only opens up a world of additional amenities and services but also employment opportunities for the residents of Alamo. Moreover, the accessibility to international borders with Mexico enhances the city’s appeal to a more global-minded populace.

Recreation and lifestyle

The lifestyle in Alamo leans towards the tranquil and family-oriented. Numerous parks, recreational facilities and community events held throughout the year contribute to a sense of belonging among residents. The close-knit community vibe is often cited in reviews as one of the endearing qualities of living in Alamo.

Crime and safety

The crime rate in Alamo is comparable to other small towns in Texas. The local law enforcement agencies are active and the community itself is known for its neighborly ethos, which contributes to the overall safety and peaceful living conditions in the city.

Conclusion

The allure of Alamo, Texas lies in its simplistic yet fulfilling lifestyle, far removed from the hustle and bustle synonymous with bigger cities. While it might lack some of the flashy amenities, its affordability, community-centric lifestyle and the promise of a serene living environment make it a compelling choice for individuals seeking a harmonious work-life balance.

However, as with any city, prospective residents should be aware of the economic conditions and be prepared for a lifestyle more serene and traditional compared to urban hubs like Austin or Houston. Looking for your Alamo dream home? Take a look at our available apartments for rent here.

Why Your Checking Account Should Contain as Little Money as Possible

By: Natasha Etzel |

Updated

Oct. 4, 2023 – First published on Oct. 4, 2023

A bank account is an excellent place to keep your money so it’s organized and readily available when needed. Many people keep their cash in a checking account. But, while you want to stash enough money in your checking account to cover your bills and everyday expenses, you want to avoid keeping all of your cash there. I’ll explain why here, and suggest a better place to stash your extra savings.Don’t miss out on interestThe average checking account doesn’t accrue interest. That means you won’t get rewarded for keeping money in your bank account. Instead of keeping all your cash in your checking account, you should only keep enough to cover your monthly expenses. You may want to keep a bit more than just enough to cover your bills. That way, you’ll be covered if you have an unexpected charge or a more costly bill than anticipated. How much extra should you have? It depends. For some people, a couple hundred extra dollars may be ideal. But for others, it may be a good idea to include a few hundred or up to an extra $1,000 in their checking accounts for extra wiggle room.But don’t keep every last dollar you have in your checking account. If you do, you’ll miss out on interest. Instead, move your extra savings into a bank account that accrues interest. With an interest-earning bank account, you’ll get rewarded as your cash sits in the bank. You could earn money with a savings accountMany people keep extra cash in a savings account. Review the bank’s annual percentage yield (APY) when considering a new savings account. This rate is the amount of money or interest you’ll earn over a year. The higher the APY, the more money you can make. You can take advantage of an attractive interest rate by opening a high-yield savings account. At the time of writing, the bank accounts on our best high-yield savings accounts list offer APYs ranging from 4.30% to 5.26%. If you have a significant amount of extra cash and keep it in an account like this, you can earn money without doing extra work. $5,000 in savings accumulates this much interest To determine how much interest you can earn by moving your extra cash to a savings account, multiply your initial deposit by the APY your bank account offers. This will show you how much interest you can earn by keeping your money in the bank for a year. Let’s imagine you have $5,000 extra sitting in your checking account right now. If you instead move that money to a high-yield savings account with an APY of 5% and you keep it in the bank for an entire year (and your APY doesn’t change; note that banks can raise or lower APYs at any time), you’ll earn $250. That’s much better than making $0 by keeping your savings in a checking account that doesn’t accrue interest. Now you can see why it pays to avoid keeping all your money in a checking account. You can earn extra money from interest by keeping your spare cash in a savings account that offers interest. For additional tips like this, check out our free personal finance resources.

3 Reasons I Don’t Like Aldi as Much as I Used To

By: Maurie Backman |

Updated

Sept. 13, 2023 – First published on Sept. 13, 2023

At some point in 2022, I discovered Aldi and began shopping there weekly. I found that I was able to save money on my grocery bill by purchasing certain produce items there. And since I happen to have an Aldi adjacent to my local Costco, it wasn’t particularly out of my way.But over the past few months, I’ve become less enamored with Aldi. Here’s why.1. The selection is just too limitedAldi — at least near me — is a minimally stocked grocery store. The shelves aren’t loaded the way they are at my nearby ShopRite and Stop & Shop.To be fair, this was the case when I first started shopping there. But because there’s just not a lot of selection, I’m generally limited to only buying a few items when I pop into Aldi.Not so long ago, I was running into Aldi for some fruit, which I usually buy there, and I needed to grab shredded cheddar cheese. Normally, I get that at Costco, but I didn’t want to run next door to Costco and wait in a line for cheese alone. Unfortunately, though, Aldi didn’t have the cheese I needed, so I had to make an extra stop anyway.2. The inventory is too inconsistentNot only is there a limited selection of food items I can buy at Aldi, but sometimes, I can’t even find the five or six things I’m looking for. Aldi was once my go-to source for avocados, since it’s an expensive purchase and Aldi tends to sell them for less than Costco (at least in my area). But the last few times I stopped at Aldi, avocados weren’t in stock.And that’s happened to me with other things, too. Over the past several months, I’ve struggled to find everything from cucumbers to strawberries at Aldi as well.3. What the store saves me on groceries, I lose via lost working hoursShopping at Aldi still has the potential to save me a little money on groceries. At a time when supermarket prices are up 3.6% on an annual basis, that helps.The problem, however, is that even though Aldi is right near Costco in my neighborhood, thereby allowing me to combine those trips, it still takes time to visit an extra supermarket. I have to find parking, wait in a checkout line, and spend time searching the shelves.While it’s nice to save $2 here and $3 there, the reality is that a stop at Aldi might cost me 20 or more minutes of work — especially when I don’t manage to find the things I need. And losing out on that work time often means forgoing more than $2 or $3 of income. So from a time perspective, it’s just not worth it.Shopping at Aldi could make sense for a lot of people. If you’re someone with flexibility in your schedule and grocery list, and you’re not so picky about the brands you bring home, then it could pay to spend the time visiting Aldi, even if you don’t always manage to find all the things you need. But I’ve reached the point where shopping at Aldi makes less and less sense for me, so I’ll most likely stop going there unless it’s a one-off basis.

7 Little-Known Gift Cards You Should Always Buy at Costco

By: Steven Porrello |

Updated

Sept. 29, 2023 – First published on Sept. 29, 2023

Costco gift cards are one of the warehouse’s best deals. Costco often will add 10% to 30% of value when you buy its gift cards in a bundle. It would be one thing if the gift cards were for places you’d never shop, like Bed, Bath, and Beyond (R.I.P.). But Costco gift cards are surprisingly varied and include many restaurants and retailers you’re probably already spending money with.So if you, like me, pinch pennies for your finances, here are seven gift cards you should always buy at Costco.1. Jiffy LubeCostco will add 25% of value when you buy a set of two $50 Jiffy Lube eGift cards for $74.99. While Jiffy Lube doesn’t offer the cheapest oil change on the market (Walmart will likely take the gold for that), its technicians do go through rigorous training via the Jiffy Lube University to ensure no accidental damage is done to your vehicle. If quality trumps price for your vehicle, this deal will save you $25 off your next oil change (limit of five per membership).2. Alaska AirlinesPacific Northwesterners will appreciate this deal — Costco will give you a $500 eCertificate to Alaska Airlines for $449.99. That comes to 10% off your next Alaska Airlines flight (limit of four per membership).3. Southwest AirlinesIf that was the first time you’d heard of Alaska Airlines, here’s a gift card package with a more familiar airline: Southwest. Costco will add 10% of value when you buy $500 of Southwest Airlines gift cards for only $449.99.4. Cinemark TheatresIn a great deal for moviegoers, you can buy a $50 Cinemark Theatres eGift card for only $39.99 at Costco. That’s an extra 20% of value that you can use for movie tickets, food, drinks, or merchandise (limit of 10 per membership).5. Miller PaintPainting your house ain’t cheap. Interior paint jobs will cost about $2 to $6 per square foot, according to the home improvement site HomeAdvisor, while exterior paint jobs can cost about $1.50 to $4 per square foot. To ease those costs, Costco will sell you $100 of Miller Paint gift cards for $69.99 — a whopping 30% of extra value.6. SpafinderIf you thought the cost of painting your house was bad, imagine how your back will feel after hours of painting walls. To ease that pain, Costco has an irresistible gift card deal: two $50 eGift cards for $79.99 to be used at thousands of spas and salons across the country. You can also use them at participating yoga and fitness studios (limit of 10 per membership).7. Synergy RestaurantsOne of the more interesting gift card packages I’ve come across, this extremely lucrative deal — two $50 eGift cards for a sticker price of $69.99 — will help you foot the bill at hundreds of local restaurants in numerous cities across Arizona, California, Colorado, Nevada, New Mexico, and Texas. This is perhaps one of the best deals I’ve seen and can be perfect for locals in those states and travelers who are visiting them.Most members don’t realize how many gift cards Costco actually sells. In fact, these seven packages only scratch the surface. Next time you’re at your local Costco warehouse, be on the lookout for gift card packages, which are often found at the ends of aisles. You might find a deal you can’t get anywhere else.

5 Amazing Costco Buys for Less Than $10

Costco is a favorite among bargain hunters. But because it’s a place where you typically buy in bulk, it’s often not great when you only want to spend a few bucks. Believe it or not, though, there are some deals at Costco for $10 or less. Here are five amazing Costco finds that will set you back no more than $10.1. Rotisserie chickenNot surprisingly, the $4.99 rotisserie chicken tops this list. Costco debuted its famed bird for $4.99 way back in 1994. It briefly raised the price by $1 during the Great Recession in 2008, then knocked it back down to $4.99 one year later. Had Costco raised its prices to keep up with inflation since 1994, that chicken would cost $10.48 today.Costco’s rotisserie chicken will always be a fan favorite for those looking for an effortless dinner. Just be aware: Costco keeps the prices low because its rotisserie chicken is what’s called a loss leader. The warehouse giant is willing to lose money selling them because it knows it can get customers into stores, where they’ll probably buy more than just a chicken.2. Hot dog and soda comboCostco has raised the prices of many of its food court items in recent years, but the price of one perennial favorite shows no signs of budging: the hot dog and soda combo, which has cost $1.50 since it debuted in 1985. Adjusted for inflation, the hot dog and soda combo should cost $4.28. Last year, during a quarterly earnings call, Costco chief financial officer Richard Galanti said the warehouse giant could keep the $1.50 price point “forever.”3. Kirkland Signature Creamy Almond ButterYou can use almond butter as a salad dressing ingredient, slather it on toast, put it in baked goods, or just eat it straight from the jar. If you’re the type who likes to devour almond butter by the spoonful, you don’t want to pass up a 27-ounce jar of Kirkland Signature Creamy Almond Butter, available for just $7.99. That works out to less than $0.30 per ounce. By comparison, a 16-ounce jar of Trader Joe’s Creamy Almond Butter Salted costs $6.99.4. Olde Thompson Kosher Sea Salt, 5 lbsSea salt has plenty of uses that go beyond cooking. You can use it for cleaning, as an exfoliant for your skin, and sprinkle it around your garden to keep unwanted bugs away. For just $5.99, you can score a 5-pound jar of Olde Thompson Kosher Sea Salt and keep it handy for all your household and kitchen needs.5. Bisquick Pancake & Baking Mix, 96 OuncesBisquick is another one of those things that’s handy to keep in your pantry. You can use it to whip up a quick batch of pancakes or waffles for breakfast or keep it on hand for a variety of baked good recipes. A 96-ounce box of Bisquick is available at Costco for $8.89. It’s normally priced at $10.99, but there’s a $2.10 manufacturer’s discount that’s good through Oct. 8, 2023.What are the best deals at Costco?Since Costco tends to sell large quantities, you’ll typically find that a lot of the best deals cost well above $10. Regardless of the exact price, it usually makes sense to buy products at Costco that have a long shelf life. For example, even if you find great deals on fresh produce and milk, you probably don’t want to load up on these items unless you’re feeding a large crowd, as they’ll go bad quickly.Also, make sure you look beyond the grocery department for savings. For example, getting your prescriptions from Costco Pharmacy or using Costco to fill up your gas tank could also save you money.If you want to maximize the benefits of your membership, try shopping with a Visa credit card that offers rewards. (Costco only accepts Visa credit cards.) That way you can earn travel rewards or cash back when you load up on groceries and other necessities.

5 Ways to Turn $100 Into Passive Income

By: Chris Neiger |

Updated

Oct. 1, 2023 – First published on Oct. 1, 2023

Creating passive income is one of the best ways to build wealth and protect your personal finances from an emergency, like losing a job or having your salary cut. According to U.S. Census Bureau data, about 20% of Americans have some level of passive income, with the average amount earned from passive income being $4,200 annually.Passive income strategies aren’t get-rich-quick schemes, and many initially require a significant time investment. The good news is that many can be started with $100 or less. Here are a few inexpensive ways you can start generating passive income.1. Buy stocksSome people think that owning stocks is only for rich people. It’s not. In fact, 61% of Americans own stocks, according to Gallup. And while you won’t get rich investing $100, you do have the potential to easily make money.You can open an online brokerage account for free and typically buy stocks for either little or no fees these days. The hard part is figuring out what company you think will do well over the long term so that you get the largest return.Let’s look at one popular company that many people own stock in: Apple. Let’s say you invested $100 annually over the past 10 years to buy Apple’s stock and reinvested any dividends you received to buy more shares. Thanks to Apple’s phenomenal growth over the past decade, your stock would be worth $4,848 — a 385% return on your investment.Of course, picking stocks can be difficult. If you want to potentially earn passive income in the market without picking specific stocks, you may want to buy shares of an exchange-traded fund (ETF). These funds follow market indices and can be purchased for as little as $1, thanks to online platforms that allow you to purchase fractional shares.2. Rent out an extra roomThis one is super easy and might cost you $0 if you already have the extra space. The latest Census Bureau data shows that 27.6% of Americans live alone. This means that many Americans may have a spare room in their home that could be transformed into a passive income stream.While it’s not for everyone, renting out a room in your home could be one of the easiest ways to generate passive income because you’re already in the space — either renting or as a homeowner — so all you need to do is find a roommate and collect their rent payments.This could be a very lucrative way to boost your income, considering that rent prices have skyrocketed over the past few years.3. Rent out your carWith 13% of full-time Americans working from home right now and 28% on hybrid schedules, many cars are sitting unused throughout the work week. With some planning and effort, your vehicle could quickly begin generating income through car-sharing websites like Turo.You can list your vehicle on the site for free and pay Turo a fee when you’ve rented out the vehicle. Turo says the average annual income for one car on its site is $10,516. Of course, some work is required to keep the vehicle clean and coordinate pick-up and drop-off. Still, renting out your vehicle could be a low-cost way to earn semi-passive income.4. Create an online courseMany people have accumulated many skills through jobs and even hobbies. You likely know how to get certain things done that someone else would find very useful — and pay for.There are many online platforms — including Udemy, Skillshare, and Thinkific — where you can create your own professional course and then sell it to an established online audience.You’ll need to do a fair amount of work upfront creating your course — including planning the sessions, recording videos, and making other content — but once you have it up and running, you can earn passive income from your hard work.Some course-creating platforms charge a monthly fee, while others may take a percentage of each sale you make. But while this option isn’t free, it’s certainly inexpensive.5. Start a dropshipping businessThere are many different businesses that fall under the dropshipping category, including selling T-shirts online or print-on-demand content like notebooks and journals.The startup cost for dropshipping businesses is low because you don’t buy any inventory and don’t have to rent an office or retail space. Instead, you’ll spend money setting up a website and potentially selling ads to market your products. You can even become a seller on Amazon and sell products without investing in your own online shop.You’ll have to invest significant time on the front end to build your business. Still, once you’ve found a niche and have established the relevant products, dropshipping allows you to spend minimal time keeping up the business while still making online sales.Keep these things in mindWhile all of these ideas will cost you little money and have the potential to generate passive income, you’ll still need to invest time and mental energy in setting them up. For example, you may need to do a lot of research before setting up a dropshipping business or launching an online course.Like anything worthwhile, be patient and take small steps to get started. You likely won’t be an overnight success, but making any progress toward generating passive income will move you further toward your personal financial goals.

If you are looking for the best online jobs for teens, then you have come to the right place. Here are the best online jobs for teenagers, even if you have no experience. There are many ways to make money online, and as a teenager, you may be interested in learning how you can as…

If you are looking for the best online jobs for teens, then you have come to the right place. Here are the best online jobs for teenagers, even if you have no experience.

There are many ways to make money online, and as a teenager, you may be interested in learning how you can as well.

Whether you are 13 years old or 19 years old, there are many different legitimate online jobs for teens that you may be interested in learning more about.

Related content:

Online Jobs For Teens

There are many online jobs for teens listed below. If you want to skip the list, here are some virtual jobs for teens that you may want to start learning more about first:

Start a website

While I was around 21 years old when I started my blog, I know of a few people who started theirs as teenagers.

A blog can be a great online job to start when you’re young, as you can decide how to build your blog, how you earn an income, and the schedule you put toward it.

Blogging has allowed me to travel full-time, work from home, have a flexible schedule, earn a high income, and love what I do.

You can easily learn how to start a blog with my free How To Create a Blog Course.

Here’s a quick outline of what you will learn:

Day 1: Why you should start a blog today

Day 2: What topic to blog about

Day 3: Tutorial on how to start a blog on WordPress

Day 4: How to make money with your blog

Day 5: How to make passive income on your blog

Day 6: How to get pageviews to your blog

Day 7: Tips to see success with your blog

Out of all of these online jobs for teens, blogging is by far my favorite. It does take a little more time to start making money, but it’s very flexible and fits with any kind of schedule.

Create a TikTok account

You have most likely heard of TikTok.

There are over 1.5 billion users on TikTok, and many people are able to earn an income on this social media platform doing many different things.

From personal finance tips to comedy, day in the life to travel, and more, there are many different topics you can cover on your own TikTok account through making social media content.

If you want to learn how to make money online for teens, this is a fun one.

You can learn more at How I Make Money On TikTok – How I Grew To 350,000 Followers and Made $60,000 In 6 Weeks.

Begin a YouTube channel

Everyone has heard of YouTube, and pretty much everyone has watched at least one YouTube video in their life.

In fact, according to YouTube, there are over 2 billion people who watch at least one video on YouTube each month.

Many people have goals of starting a YouTube channel and making money, but not many people ever actually start.

You can learn more at How I Grew From 0 Subscribers To Over $100,000 On YouTube In Less Than One Year.

Resell items online

If you are looking for a flexible job as a teenager, one to look into may be reselling items online, such as on Craigslist, eBay, or Facebook Marketplace. There are many other online marketplaces as well.

Plus, it’s something that anyone can start because many of us own things that we could probably sell.

And, there are always things that you can buy for a low price and possibly resell for a profit. Or, you may even be able to find free things that people are throwing away and sell that as well.

This is such a profitable idea that my friend was able to make $133,000 in one year through buy-and-sell flipping and with working only 10-20 hours per week.

Since then, they have turned this into an even bigger and more profitable business!

Some of the best items that they’ve resold include:

Something they bought for $10 and flipped for $200 just 6 minutes later

A security tower they bought for $6,200 and flipped for $25,000 just one month later

A prosthetic leg that they bought for $30 at a flea market and sold for $1,000 on eBay the very next day

A lift that they found in the trash (and asked the owner for permission to take) that they sold online for $7,500

You can learn more at How I Made $40,000 In One Year Flipping Items.

They also have a helpful free webinar, Turn Your Passion For Visiting Thrift Stores, Yard Sales & Flea Markets Into A Profitable Reselling Business In As Little As 14 Days. I recommend checking it out.

Sell printables on Etsy

If you are looking for a way to make money at home and be your own boss, then creating printables may be for you.

A printable is a digital product that can be downloaded and printed at home. You make them once and then sell them on a website such as Etsy for people to buy. You wouldn’t have to print anything, instead, you are simply selling the download.

Items such as grocery shopping checklists, weekly meal plans that someone puts on their fridge, gift tags, and quotes to be framed are all printables.

This can be a great way to make money at home as a teenager because you create one digital file download per product, and you can then sell them an unlimited amount of times.

You can sign up for this free ebook that helps you figure out where to start when it comes to selling printables on Etsy.

I recommend reading about this further at How I Make Money Selling Printables On Etsy to learn more about one of the best jobs for stay-at-home moms.

Note: Etsy account owners must be at least 18 years of age to sell on Etsy. If you are between the ages of 13 and 17, you can sell on Etsy if you have the appropriate permission and direct supervision of your parent or legal guardian. Your Etsy account must be registered with the parent or legal guardian’s information.

Create and sell stickers

Another fun way to make money online as a teenager is to sell stickers.

My friend started with no graphic design skills and didn’t even know how to create stickers when she first started. It’s something she learned as she went, and she now earns over $100,000 each year with her sticker business.

I interviewed her here on Making Sense of Cents and she answered questions such as:

Do I need to be a graphic designer to make and sell stickers?

Why do people buy stickers online?

Do stickers sell well online?

How much money can I make selling stickers as a small business idea?

You can head over to How To Make $1,000+ A Month Selling Stickers Online to read more.

Make Canva templates

Canva is an online graphic design website. On Canva, you can sell premade designs to other Canva users so that they can edit and customize them.

Some examples of Canva templates include ebooks, workbooks, Pinterest pins, and more.

Creating Canva templates can be a great way to make extra money because you just need to create them once, and you can sell them an unlimited amount of times.

People all around the world use Canva to help with the graphic design side of their business, and templates make their lives so much easier.

Working just a few hours a week, I know someone who is able to earn $2,000 each month from selling Canva templates from home.

Do you have questions such as:

What is a Canva template and what is Canva?

Why would someone buy Canva templates? What is the benefit?

I have no tech skills, can I still create and sell Canva templates?

You can head to this article to learn more at How I Make $2,000+ Monthly Selling Canva Templates.

Voice over acting

Voice-over actors are of all ages, and you probably hear them all the time!

A voice-over actor is the person you hear but usually do not see on radio ads, YouTube videos, documentaries, e-learning courses, audiobooks, TV commercials, video games, movies, and cartoons.

This job doesn’t require previous experience or special skills – you just need to have the voice the company is looking for.

You can learn more about how to become a voice-over actor at How To Become A Voice Over Actor.

Answer online surveys

Not too long ago, one of the ways I made extra money to pay off my student loan debt was by answering paid online surveys.

You will not get rich from taking surveys, but it can help you to earn a little bit of extra money in some of the spare minutes that you may have throughout the day. Plus, you may get free items occasionally to review as well.

Companies will pay you to take surveys because they want to see what people think of their product and their company. They seek out real opinions from real people.

Here are some of the survey companies that are open to teenagers (along with their minimum age requirements):

American Consumer Opinion – Age minimum – 14 years old

Survey Junkie – Age minimum – 12 years old

MyPoints – Age minimum – 13 years old

Branded Surveys – Age minimum – 16 years old

Swagbucks – Age minimum – 13 years old

InboxDollars – Age minimum – 12 years old

Pinecone Research – Age minimum – 18 years old

User Interviews – Age minimum – 16 years old

Some of the above will even pay you to review music, play video games, or test mobile apps as a part of their research.

Sell items on Amazon

We have all heard of Amazon.

It is a website full of items sold by people like you and me.

In the first year that my friend Jessica’s family ran their Amazon FBA business together, working less than 20 hours a week total, they made over $100,000 profit!

You can learn more by reading How To Make Money From Home Selling On Amazon, such as answers to questions like:

How Jessica started selling on Amazon FBA

What exactly Amazon FBA is

How to choose what to buy and sell

How much a person can expect to earn

The positives of selling on Amazon, and more

Customer service support

If you are looking for a more traditional style of online job, such as working for someone else, then finding a customer service representative job may be something to look into. This way, you can start earning money right away, right after you get hired, instead of attempting to build a business.

There are many companies that hire for customer service support at home, even if you are young. Most will want you to be at least 16 years old or 18 years old to start.

As a customer service representative, you may be responsible for tasks such as:

Answering questions from customers about a product

Troubleshooting and helping with issues that a customer may have with a product

Processing orders

Assisting with returns

Handling feedback and customer complaints

And so much more.

Virtual assistant

As a virtual assistant, you would be helping a person or small business owner with administrative and business tasks. You would be their assistant but working in your own home instead.

I have been a virtual assistant in the past, and I now have virtual assistants of my own. They are lifesavers!

You do not need to have previous experience in order to start as a virtual assistant, instead, you need to be willing to learn so that you can help a business run more smoothly.

Many, many people and companies are looking for virtual assistants, as they play such an important role.

As a virtual assistant, you may be able to start at around $15-$20 an hour, or even much more. This will depend on the type of work you are providing, the experience that you have, the field you will be working in, and more. As a full-time virtual assistant, you may be able to earn over $10,000 a month once you gain experience.

As a virtual assistant, you may be doing tasks such as:

Managing a company’s social media accounts, such as by being their social media manager

Managing a person or company’s calendar

Scheduling appointments or travel

Creating or assisting with slideshows or presentations

Email management

Communicating with clients or customers

And so much more.

Different companies and employers will need different work to be done – it simply depends on who you will be working for and what they need to be completed.

You can learn more at How I Earn $10,000 Per Month From Home as a Virtual Assistant.

Start an online store

I feel like so many young adults are starting online stores, and it completely makes sense.

It’s something you can do from home, and there are ways to do it that don’t involve storing inventory or taking up a large amount of your valuable time.

Plus, you can make extra cash or even a full-time income.

And, there are so many different things that you can sell online.

From pet items, skincare, fitness products, subscription boxes, and accessories, to clothing, crafts, and more, the list is endless.

You can learn more about this topic at How I Make Over $10,000 Monthly With My Online Store In Less Than 10 Hours Per Week.

Write an ebook

Yes, you may be able to make extra money as a teenager by writing an ebook, and you can do it all from your home.

Anyone can write an ebook, no matter how young you may be.

There are many different genres that you can choose from, such as fantasy, fiction, nonfiction, mystery, and more.

If this is one of the online jobs for teens you’d like to learn more about, read How I Make $200 Each Day In Book Sales.

Find online tutoring jobs

Are you looking for a flexible side hustle as an online tutor?

If there is a subject that you are knowledgeable in, such as math, English, science, etc., then you may want to see if you can find students that you can tutor.

To become an online tutor, you can simply create a tutor profile on a tutoring platform, create a listing on Fiverr, reach out to people that you know, and more.

Learn more at The Best Online Tutoring Jobs – A Flexible Way To Make More Money.

Freelance write

Becoming a freelance writer can be a great online job for teens because there is a growing number of jobs out there for freelance writers, and many people start with no previous experience.

A freelance writer is someone who writes for a number of different clients, such as a website, blog, magazine, and more.

You can learn more in the article How To Become A Freelance Writer.

Proofread

If you have a passion for reading and often find mistakes in written content, then you may want to learn how to become a proofreader.

Freelance proofreading is a flexible and detail-oriented job that only requires a laptop or tablet, an internet connection, grammar skills, and a good eye for finding mistakes.

Proofreaders look for punctuation mistakes, grammar, misspelled words, lack of consistency, and formatting errors.

If you want to find online proofreading jobs, I recommend watching this free 76-minute workshop all about how to get started proofreading.

Recommended reading: 20 Best Online Proofreading Jobs For Beginners (Earn $40,000+ A Year).

Tips for online jobs for teens

Below, I want to share some tips for you on how to manage an online job for high schoolers. Having an online job as a teenager means that you may have some questions, such as how to avoid scams, how to balance school and work, how to open a PayPal account when you are underage, and more.

How to avoid online job scams

While there are many, many legitimate online jobs for teens, there are scams as well. Due to that, I want to share my best tips so that you can avoid scams but still find an online gig.

Some of my tips to avoid scams:

Research the company and the position to make sure they are real and a company that you would like to work for.

Search on the Better Business Bureau to learn more about the company and read their reviews.

Research the company online to see if there are any mentions of it being a scam. I like to type in “Company name + Scam” into a search engine and see what pops up.

Always be careful if the company asks you to pay money.

Before you give out any personal information, such as your social security number, you should make sure it is a real job that they are offering you.